|

市场调查报告书

商品编码

1936628

船舶推进发动机市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Marine Propulsion Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

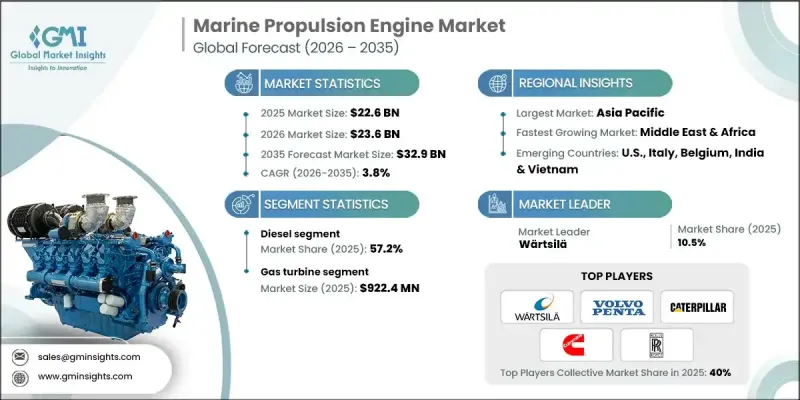

全球船舶推进引擎市场预计到 2025 年将达到 226 亿美元,到 2035 年将达到 329 亿美元,年复合成长率为 3.8%。

全球范围内为减少海上作业排放而不断加大力度,推动了市场成长,迫使船队营运商重新评估推进技术,以满足长期监管要求。市场需求正转向更清洁、更有效率的推进系统,这些系统能够运作替代燃料和低碳燃料,同时保持可靠性和动力性能。船舶推进引擎作为核心机械系统,透过整合推进组件将能量转化为可控运动,从而产生船舶航行所需的推力。全球贸易量的成长和航线的延长,促使人们需要更耐用、更有效率、性能更稳定的引擎。商业、海上和政府部门针对老旧船舶的船队更新计划,推动了对数位化先进推进平台的投资。整合即时监控、数据分析和预测性维护功能的智慧引擎架构正日益受到重视,以提高运作和全生命週期效率。船东也倾向于灵活的推进配置,这种配置能够在不影响耐用性和运作稳定性的前提下,可支援燃料适应性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 226亿美元 |

| 预测金额 | 329亿美元 |

| 复合年增长率 | 3.8% |

预计2035年,风能和太阳能船舶推进引擎市场规模将达15亿美元。混合动力推进架构将可再生能源与船上储能和控制系统结合,随着营运商寻求在低负载运转条件下优化燃料利用,混合动力推进架构正日益受到青睐。先进的能源管理框架在改善负载平衡和排放性能的同时,也支援更有效率的航程规划。

预计2025年,燃料电池船用推进引擎市占率将达到3.9%。随着船舶营运商为遵守不断变化的环境法规而寻求零排放推进方案,燃料电池的应用正在逐渐增加。可扩展的系统设计和模组化整合方法能够实现逐步部署,同时确保运行冗余并适应各种船舶需求。

预计到2025年,美国船舶推进引擎市场将占据68.6%的市场份额,市场规模达22亿美元。这一增长主要得益于国内海事活动的增加,包括沿海航运、内河航运和近海作业,从而推动了对高效高性能推进系统的需求。此外,造船业,特别是商船和军舰的大量投资,也进一步促进了市场扩张,因为新船越来越多地采用低排放气体和数位化技术的引擎。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 製造能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 船用推进引擎成本结构分析

- 价格趋势分析

- 副产品

- 按地区

- 新的机会与趋势

- 数位化和物联网集成

第四章 竞争情势

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪錶板

- Key partnerships &collaborations

- Major M&A activities

- Product innovations &launches

- Market expansion strategies

- 策略倡议

- 竞争标竿分析

- 创新与科技趋势

第五章 2022-2035年依产品分類的市场规模及预测

- 柴油引擎

- 风能/太阳能

- 燃气涡轮机

- 燃料电池

- 蒸气涡轮

- 天然气

第六章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 丹麦

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 越南

- 新加坡

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 伊朗

- 安哥拉

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

第七章 公司简介

- AB Volvo Penta

- Anglo Belgian Corporation

- Caterpillar

- Cummins

- Deere &Company

- Deutz AG

- HD Hyundai Heavy Industries Engine &Machinery

- Ingeteam

- Isuzu Motors Engine Sales

- Masson Marine

- Mitsubishi Heavy Industries

- Nanni

- Perkins Engines

- Rolls-Royce

- Scania

- Steyr

- Vetus

- Wartsila

- Yamaha Motor

- Yanmar Marine International

The Global Marine Propulsion Engine Market was valued at USD 22.6 billion in 2025 and is estimated to grow at a CAGR of 3.8% to reach USD 32.9 billion by 2035.

Market growth is shaped by the intensifying global push to lower emissions across maritime operations, prompting fleet operators to reassess propulsion technologies for long-term regulatory alignment. Demand is shifting toward cleaner, more efficient propulsion systems capable of operating on alternative and low-carbon fuels while maintaining reliability and power output. Marine propulsion engines serve as the core mechanical systems that generate thrust for vessel movement by converting energy into controlled motion through integrated propulsion components. Rising global trade volumes and extended shipping routes are reinforcing the need for engines that deliver greater endurance, efficiency, and performance consistency. Fleet renewal programs targeting aging vessels across commercial, offshore, and government segments are driving investment in digitally advanced propulsion platforms. Intelligent engine architectures that incorporate real-time monitoring, data analytics, and predictive maintenance capabilities are increasingly prioritized to improve uptime and lifecycle efficiency. Shipowners are also favoring flexible propulsion configurations that support fuel adaptability without compromising durability or operational stability.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $22.6 Billion |

| Forecast Value | $32.9 Billion |

| CAGR | 3.8% |

The wind and solar-based marine propulsion engine segment is projected to reach USD 1.5 billion by 2035. Hybridized propulsion architectures that combine renewable inputs with onboard energy storage and control systems are gaining traction as operators seek to optimize fuel usage during low-demand operating conditions. Advanced energy management frameworks are improving load balancing and emissions performance while supporting more efficient voyage planning.

The fuel cell-based marine propulsion engines segment accounted for a 3.9% share in 2025. Adoption is gradually increasing as vessel operators pursue zero-emission propulsion options aligned with evolving environmental mandates. Scalable system designs and modular integration approaches are enabling gradual deployment while ensuring operational redundancy and adaptability to different vessel requirements.

United States Marine Propulsion Engine Market held a 68.6% share in 2025, generating USD 2.2 billion. This growth is being fueled by increasing domestic maritime activity, including coastal shipping, inland waterways, and offshore operations, which are driving demand for efficient, high-performance propulsion systems. Substantial investments in shipbuilding, particularly for commercial and naval fleets, are further bolstering market expansion, as new vessels are increasingly being equipped with low-emission, digitally enabled engines.

Key participants active in the Global Marine Propulsion Engine Market include Wartsila, Caterpillar, Rolls-Royce, Yanmar Marine International, Cummins, AB Volvo Penta, Mitsubishi Heavy Industries, Scania, Deutz AG, HD Hyundai Heavy Industries Engine & Machinery, Yamaha Motor, Perkins Engines, Anglo Belgian Corporation, Vetus, Nanni, Masson Marine, Ingeteam, Steyr, Deere & Company, and Isuzu Motors Engine Sales. These companies maintain competitive positioning through innovation, portfolio diversification, and global service networks. To strengthen their foothold in pharmaceutical and healthcare-related marine applications, propulsion engine manufacturers are prioritizing reliability, precision control, and low-emission performance. Companies are developing propulsion solutions optimized for vessels supporting medical logistics, offshore healthcare access, and temperature-sensitive cargo transport. Strategic investments focus on noise reduction, vibration control, and stable power delivery to protect sensitive onboard equipment. Manufacturers are also expanding service agreements and remote diagnostics to ensure uninterrupted operations in critical missions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of marine propulsion engine

- 3.8 Price trend analysis

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Emerging opportunities & trends

- 3.10 Digitalization and IoT integration

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Wind & solar

- 5.4 Gas turbine

- 5.5 Fuel cell

- 5.6 Steam turbine

- 5.7 Natural gas

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 Italy

- 6.3.4 France

- 6.3.5 Russia

- 6.3.6 Denmark

- 6.3.7 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.4.6 Vietnam

- 6.4.7 Singapore

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 Iran

- 6.5.4 Angola

- 6.5.5 Egypt

- 6.5.6 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

- 6.6.3 Mexico

Chapter 7 Company Profiles

- 7.1 AB Volvo Penta

- 7.2 Anglo Belgian Corporation

- 7.3 Caterpillar

- 7.4 Cummins

- 7.5 Deere & Company

- 7.6 Deutz AG

- 7.7 HD Hyundai Heavy Industries Engine & Machinery

- 7.8 Ingeteam

- 7.9 Isuzu Motors Engine Sales

- 7.10 Masson Marine

- 7.11 Mitsubishi Heavy Industries

- 7.12 Nanni

- 7.13 Perkins Engines

- 7.14 Rolls-Royce

- 7.15 Scania

- 7.16 Steyr

- 7.17 Vetus

- 7.18 Wartsila

- 7.19 Yamaha Motor

- 7.20 Yanmar Marine International

电动船舶吊舱推进器市场:按船舶类型、推进系统、应用和终端用户产业划分-全球预测,2026-2032年

电动船舶吊舱推进器市场:按船舶类型、推进系统、应用和终端用户产业划分-全球预测,2026-2032年 2026年全球船舶推进发动机市场报告

2026年全球船舶推进发动机市场报告 船舶推进发动机市场-全球产业规模、份额、趋势、机会、预测:按发动机类型、应用、船舶类型、地区和竞争对手划分,2021-2031年

船舶推进发动机市场-全球产业规模、份额、趋势、机会、预测:按发动机类型、应用、船舶类型、地区和竞争对手划分,2021-2031年 船舶推进发动机市场规模、份额和成长分析(按燃料类型、应用、船舶类型和地区划分)—产业预测(2026-2033 年)船舶推进及辅助动力市场-全球产业规模、份额、趋势、机会及预测,依燃料类型、应用、功率等级、船舶类型、地区及竞争格局划分,2020-2030年预测船舶推进发动机市场按发动机类型、功率输出、发动机布置、安装方式、发动机转速等级、船舶类型和最终用户划分 - 全球预测 2025-2032核能船舶推进系统市场(依核子反应炉类型、推进系统、船舶类型和最终用户)—全球预测,2025 年至 2030 年

船舶推进发动机市场规模、份额和成长分析(按燃料类型、应用、船舶类型和地区划分)—产业预测(2026-2033 年)船舶推进及辅助动力市场-全球产业规模、份额、趋势、机会及预测,依燃料类型、应用、功率等级、船舶类型、地区及竞争格局划分,2020-2030年预测船舶推进发动机市场按发动机类型、功率输出、发动机布置、安装方式、发动机转速等级、船舶类型和最终用户划分 - 全球预测 2025-2032核能船舶推进系统市场(依核子反应炉类型、推进系统、船舶类型和最终用户)—全球预测,2025 年至 2030 年 船舶电动吊舱驱动器市场,规模,占有率,趋势,产业分析报告:各推动类型,额定输出,各安装类型,各控制系统,各终端用户,各地区,2025年~2034年的市场预测

船舶电动吊舱驱动器市场,规模,占有率,趋势,产业分析报告:各推动类型,额定输出,各安装类型,各控制系统,各终端用户,各地区,2025年~2034年的市场预测 船舶吊舱驱动市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

船舶吊舱驱动市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 船舶推进发动机市场按发动机类型、功率输出、燃料类型和地区划分

船舶推进发动机市场按发动机类型、功率输出、燃料类型和地区划分