|

市场调查报告书

商品编码

1936645

抗痘化妆品市场机会、成长要素、产业趋势分析及2026年至2035年预测Anti-acne Cosmetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

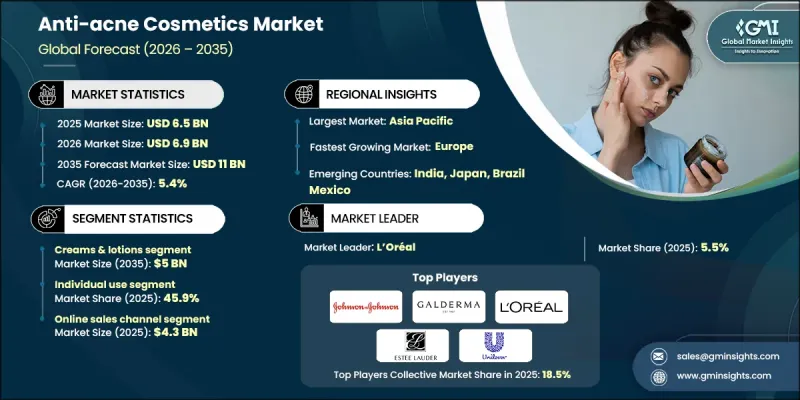

全球抗痘化妆品市场预计到 2025 年将达到 65 亿美元,到 2035 年将达到 110 亿美元,年复合成长率为 5.4%。

市场成长主要受清洁美容运动的兴起以及消费者对天然有机成分护肤品日益增长的偏好驱动。消费者对合成化合物潜在副作用的担忧日益加剧,促使他们优先选择成分较温和、无毒且天然的保养品。这种消费行为的转变正在重塑整个产业的研发策略,製造商纷纷调整产品配方以符合洁净标示的要求。消费者对皮肤健康的日益关注,以及个人护理支出的成长,持续支撑着市场需求。此外,人们对永续美容实践的日益重视,以及有利于环保产品的法规结构,也推动了市场的长期扩张。随着护肤程序越来越注重成分和健康,抗痘化妆品正被不同年龄和肤质的消费者广泛接受,这预示着市场将在2025年以后保持稳步增长。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 起始值 | 65亿美元 |

| 预测金额 | 110亿美元 |

| 复合年增长率 | 5.4% |

预计到2025年,乳霜和乳液类产品市场收入将达29亿美元,到2035年将达到50亿美元。由于其多功能性和易用性,该品类持续保持主流地位。消费者更倾向于选择外用产品,这些产品不仅有助于控制痤疮,还能提供保湿、调理和长期护肤等额外功效。消费者对多功能护肤方案的需求不断增长,进一步推动了抗痤疮乳霜和乳液类产品的需求。

预计到2025年,个人使用细分市场将占45.9%的市场份额。此细分市场的成长主要得益于消费者对价格实惠、方便在家使用的祛痘解决方案的需求日益增长。这种转向自我护理的趋势减少了对频繁专业治疗的依赖,从而节省了时间和成本。这一趋势反映了消费者对个人化护肤和自主选择产品的更广泛需求,也印证了个人消费者在推动整体市场成长的重要性。

预计到2025年,美国抗痘化妆品市场份额将达到74.5% 。主导地位得益于消费者的高度认知、非处方护肤品的高渗透率以及先进皮肤科解决方案的广泛应用。此外,知名高端品牌的存在、数位行销的影响以及对经临床检验的化妆品日益增长的需求,共同推动了市场渗透率的持续成长。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 产业影响因素

- 司机

- 青少年和成年人痤疮盛行率不断上升

- 意识提高和皮肤科咨询量增加

- 配方和递送系统的创新

- 产业潜在风险与挑战

- 消费者偏好和趋势的变化

- 仿冒品品

- 机会

- 智慧护肤与个人化结合

- 永续性和清洁美容趋势

- 司机

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 依产品类型

- 按地区

- 监管环境

- 标准和合规要求

- 区域法规结构

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 差距分析

- 风险评估与缓解

- 波特五力分析

- PESTEL 分析

- 消费行为分析

- 购买模式

- 偏好分析

- 消费行为的区域差异

- 电子商务对购买决策的影响

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 面具

- 乳霜和乳液

- 洗面乳和化妆水

- 其他的

第六章 2022-2035年按价格分類的市场估计与预测

- 低价位

- 中号

- 高价位范围

7. 依最终用途分類的市场估计与预测,2022-2035 年

- 个人使用

- 水疗中心及美容院

- 皮肤科诊所

- 其他的

第八章 按分销管道分類的市场估算与预测,2022-2035年

- 在线的

- 电子商务

- 我们的网站

- 离线

- 超级市场/大卖场

- 专卖店

- 其他(个体店、百货公司等)

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- AbbVie

- Bayer

- Beiersdorf

- Estee Lauder

- Galderma

- Honasa Consumer

- Johnson &Johnson

- L'Oreal

- Mario Badescu

- Natura &Co

- Pierre Fabre

- Shiseido

- Sunday Riley

- Teva

- Unilever

The Global Anti-acne Cosmetics Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 11 billion by 2035.

Market growth is strongly influenced by the expanding clean beauty movement and the rising preference for natural and organic skincare formulations. Consumers are increasingly prioritizing products made with gentle, non-toxic, and naturally derived ingredients, driven by growing concerns about the potential side effects of synthetic compounds. This shift in consumer behavior is reshaping product development strategies across the industry, with manufacturers responding by reformulating offerings to align with clean-label expectations. Rising awareness of skin health, combined with increased spending on personal care, continues to support sustained demand. Additionally, growing interest in sustainable beauty practices and supportive regulatory frameworks promoting environmentally responsible products are reinforcing long-term market expansion. As skincare routines become more ingredient-conscious and wellness-oriented, anti-acne cosmetics are gaining wider acceptance across diverse age groups and skin types, supporting consistent growth beyond 2025.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $11 Billion |

| CAGR | 5.4% |

The creams and lotions segment generated USD 2.9 billion in 2025 and is expected to reach USD 5 billion by 2035. This segment remains dominant due to its versatility and ease of application. Consumers favor topical formats that not only help manage acne but also deliver complementary benefits such as moisturization, skin tone enhancement, and long-term skin maintenance. Changing consumer expectations toward multifunctional skincare solutions continue to strengthen demand for creams and lotions within the anti-acne category.

The individual-use segment accounted for 45.9% share in 2025. Growth in this segment is driven by increasing consumer preference for accessible, affordable, and convenient acne care solutions used at home. The shift toward self-care routines has reduced reliance on frequent professional treatments, offering time and cost efficiency. This trend reflects a broader movement toward personalized skincare and independent product selection, reinforcing the importance of individual consumers in driving overall market growth.

United States Anti-acne Cosmetics Market held 74.5% share in 2025. Market leadership is supported by strong consumer awareness, high adoption of over-the-counter skincare products, and widespread availability of advanced dermatological solutions. The presence of established premium brands, combined with digital marketing influence and growing demand for clinically validated cosmetic products, continues to accelerate market penetration.

Key companies operating in the Global Anti-acne Cosmetics Market include L'Oreal, Johnson & Johnson, Unilever, Estee Lauder, Beiersdorf, Galderma, Shiseido, Bayer, AbbVie, Natura & Co, Pierre Fabre, Sunday Riley, Mario Badescu, Honasa Consumer, and Teva. Companies in the Anti-acne Cosmetics Market are strengthening their market position through product innovation, clean-label reformulations, and sustainability-focused strategies. Leading players are investing in research to develop gentle yet effective formulations that align with natural and dermatologically tested standards. Expansion across digital and direct-to-consumer channels is improving brand reach and customer engagement. Firms are also leveraging influencer marketing, personalization tools, and targeted product portfolios to capture specific consumer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Price

- 2.2.4 End Use

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of acne among adolescents and adults.

- 3.2.1.2 Growing awareness and dermatological consultations.

- 3.2.1.3 Innovation in formulations and delivery systems.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Changing consumer preferences and trends

- 3.2.2.2 Counterfeit and imitation products

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart skincare and personalization.

- 3.2.3.2 Sustainability and clean beauty trends.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By product type

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Gap analysis

- 3.10 Risk assessment and mitigation

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behaviour analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behaviour

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Masks

- 5.3 Creams & lotions

- 5.4 Cleansers & toners

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Price, 2022-2035 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Individual use

- 7.3 Spas and parlors

- 7.4 Dermatological clinics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-Commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets/Hypermarkets

- 8.3.2 Specialty Stores

- 8.3.3 Others (Individual stores, Departmental stores, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Bayer

- 10.3 Beiersdorf

- 10.4 Estee Lauder

- 10.5 Galderma

- 10.6 Honasa Consumer

- 10.7 Johnson & Johnson

- 10.8 L'Oreal

- 10.9 Mario Badescu

- 10.10 Natura & Co

- 10.11 Pierre Fabre

- 10.12 Shiseido

- 10.13 Sunday Riley

- 10.14 Teva

- 10.15 Unilever

抗痘化妆品市场分析及预测(至2035年):依类型、产品、技术、成分、应用、剂型、部署方式、最终用户及功能划分痤疮治疗药物市场分析及预测(至2035年):依类型、产品、技术、应用、剂型、最终用户、给药途径、治疗阶段及溶液分类

抗痘化妆品市场分析及预测(至2035年):依类型、产品、技术、成分、应用、剂型、部署方式、最终用户及功能划分痤疮治疗药物市场分析及预测(至2035年):依类型、产品、技术、应用、剂型、最终用户、给药途径、治疗阶段及溶液分类 全球抗痘化妆品市场规模、份额、趋势和成长分析报告(2026-2034)

全球抗痘化妆品市场规模、份额、趋势和成长分析报告(2026-2034) 抗痘化妆品市场-全球产业规模、份额、趋势、机会和预测:按类型、最终用户、配方、分销管道、地区和竞争格局划分,2021-2031年

抗痘化妆品市场-全球产业规模、份额、趋势、机会和预测:按类型、最终用户、配方、分销管道、地区和竞争格局划分,2021-2031年 抗痘化妆品市场规模、份额及成长分析(按产品类型、性别、最终用途和地区划分)-产业预测(2026-2033 年)

抗痘化妆品市场规模、份额及成长分析(按产品类型、性别、最终用途和地区划分)-产业预测(2026-2033 年) 痤疮治疗市场规模、份额和成长分析(按产品类型、剂型、给药途径、年龄层、分销管道和地区划分)—产业预测(2026-2033 年)

痤疮治疗市场规模、份额和成长分析(按产品类型、剂型、给药途径、年龄层、分销管道和地区划分)—产业预测(2026-2033 年) 痤疮药物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

痤疮药物市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 2025 年至 2033 年痤疮药物市场规模、份额、趋势及预测(按痤疮类型、药物类别、药物类型、给药途径和地区划分)

2025 年至 2033 年痤疮药物市场规模、份额、趋势及预测(按痤疮类型、药物类别、药物类型、给药途径和地区划分) 全球痤疮化妆品市场预测(至 2032 年):按产品类型、成分类型、性别、年龄层、价格分布范围、分销管道和地区划分

全球痤疮化妆品市场预测(至 2032 年):按产品类型、成分类型、性别、年龄层、价格分布范围、分销管道和地区划分 抗痤疮化妆品市场规模、份额、趋势分析报告:按产品类型、性别、最终用途、地区、细分市场预测,2025-2030 年

抗痤疮化妆品市场规模、份额、趋势分析报告:按产品类型、性别、最终用途、地区、细分市场预测,2025-2030 年