|

市场调查报告书

商品编码

1936654

聚丙烯酰胺市场机会、成长要素、产业趋势分析及2026年至2035年预测Polyacrylamide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球聚丙烯酰胺市场预计到 2025 年将达到 65 亿美元,到 2035 年将达到 108 亿美元,年复合成长率为 5.2%。

受水处理和污水管理系统技术的进步推动,市场正经历显着扩张。快速的都市化、日益严格的环境法规以及对高效水资源管理解决方案不断增长的需求,促使各国政府和企业对市政和工业水处理基础设施进行大规模投资。聚丙烯酰胺作为高性能凝聚剂,在污泥脱水、固液分离和废水净化方面发挥关键作用。对水质和法规遵循的长期承诺持续推动市场需求。此外,采矿和纺织等行业的成长也促进了市场扩张。在采矿业,聚丙烯酰胺有助于尾矿管理和水资源回收,从而提高营运效率和资源利用率。在纺织业,它支持上浆、染色和污水处理等工艺,契合了人们对永续生产和废水管理日益增长的关注。总而言之,监管力道的加大和工业用水量的增加,持续为全球聚丙烯酰胺市场创造强劲的成长机会。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 65亿美元 |

| 预测金额 | 108亿美元 |

| 复合年增长率 | 5.2% |

阴离子聚丙烯酰胺(APAM)市场预计到2025年将达到31亿美元,主要得益于其在市政和工业污水处理、采矿製程以及石油开采等领域的广泛应用。 APAM具有絮凝效率高、成本效益好以及符合监管要求等优点,使其成为大规模固液分离和废水处理的首选材料,尤其是在环境法规严格的地区。在用水量大的工业领域持续使用,进一步巩固了其在产品组合中的主导地位。

预计2025年,水和污水处理市场规模将达26亿美元,预测期内复合年增长率(CAGR)为4.7%。聚丙烯酰胺在该领域发挥重要作用,尤其是在市政和工业污水处理厂的絮凝、污泥处理和固液分离方面,因此受益匪浅。都市化加快、废水法规日益严格以及处理基础设施的现代化,正在推动该领域的成长。市场对高效且价格合理的水处理解决方案的需求,将确保成熟市场和新兴市场都能保持持续的高销售量。

预计到2025年,北美聚丙烯酰胺市场将占据20%的份额,其中美国将贡献该地区的大部分收入。该地区的成长得益于完善的水处理基础设施和强劲的油气产业。严格的污水排放环境法规、市政污水处理厂的广泛应用以及聚合物在石油开采中的重要作用是推动市场需求的主要因素。北美市场已趋于成熟,预计在持续的基础设施投资和高品质水处理解决方案日益普及的推动下,该市场将保持稳定成长。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 全球推广先进的废弃物处理和处置技术

- 采矿和纺织业的趋势

- 页岩气和緻密油产量不断成长

- 产业潜在风险与挑战

- 原物料价格波动

- 对残留单体实施严格监管

- 与丙烯酰胺毒性相关的环境问题

- 市场机会

- 水处理应用需求不断成长

- 提高石油采收率(EOR)和采矿扩张

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 阴离子聚丙烯酰胺(APAM)

- 阳离子聚丙烯酰胺(CPAM)

- 非离子型聚丙烯酰胺(NPAM)

- 两性聚丙烯酰胺

- 其他的

第六章 按类型分類的市场估算与预测,2022-2035年

- 粉末

- 乳液

- 液体

- 其他的

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 水和污水处理

- 提高石油采收率(EOR)

- 采矿和矿物加工

- 农业

- 纤维和染色

- 化妆品和个人护理

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- SNF Group

- Kemira Oyj

- BASF SE

- Ashland Global Holdings Inc.

- NNA Polymers, Inc.

- Wego Chemical Group Inc.

- Catalynt Solutions, Inc.

- Chinafloc Chemical Co. Ltd

- Henan Hangrui Environmental Protection Technology

- Shandong Shuiheng Chemical Co. Ltd

- Anhui Tianrun Chemicals Co. Ltd

- Zibo East Polymer Co. Ltd

- Welldone Chemical Group

- Henan Secco Environmental Protection Tech Co. Ltd

- Beijing Hengju Chemical Group Co., Ltd.

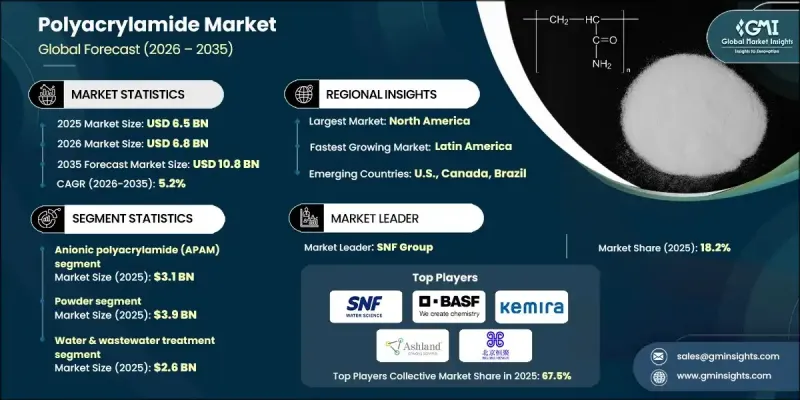

The Global Polyacrylamide Market was valued at USD 6.5 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 10.8 billion by 2035.

The market is experiencing significant expansion, driven by advancements in water treatment and wastewater management systems. Rapid urbanization, stricter environmental regulations, and the need for efficient water management solutions are encouraging governments and industries to invest heavily in municipal and industrial water treatment infrastructure. Polyacrylamide, a high-performance flocculant, plays a vital role in these systems by aiding sludge dewatering, solid-liquid separation, and effluent purification. Long-term commitments to water quality and regulatory compliance are continuously driving demand. Furthermore, growth in sectors such as mining and textiles is expanding the market footprint. In mining operations, polyacrylamide supports tailings management and water recovery, improving operational efficiency and resource utilization. In the textile industry, it assists in processes like sizing, dyeing, and wastewater treatment, aligning with the growing emphasis on sustainable production and effluent management. Overall, increasing regulatory enforcement and industrial water consumption continue to create strong growth opportunities for polyacrylamide globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.5 Billion |

| Forecast Value | $10.8 Billion |

| CAGR | 5.2% |

The anionic polyacrylamide (APAM) segment reached USD 3.1 billion in 2025. Its widespread adoption in municipal and industrial wastewater treatment, mining processes, and oil recovery applications is a key driver. High flocculation efficiency, cost-effectiveness, and regulatory compliance make APAM the preferred choice for large-scale solid-liquid separation and effluent management, particularly in regions with stringent environmental laws. The polymer's continued use in water-intensive industries strengthens its dominance within the product mix.

The water and wastewater treatment segment was valued at USD 2.6 billion in 2025 and is estimated to grow at a CAGR of 4.7% during the forecast period. As the primary application of polyacrylamide, this segment benefits from its critical role in flocculation, sludge handling, and solid-liquid separation in municipal and industrial plants. Rising urbanization, regulatory oversight of effluent discharge, and upgrades in treatment infrastructure reinforce the segment's growth potential. The demand for effective, affordable water treatment solutions ensures sustained high-volume sales in both mature and emerging markets.

North America Polyacrylamide Market accounted for 20% share in 2025, with the majority of regional revenue coming from the United States. Growth in this region is supported by extensive water treatment infrastructure and a robust oil and gas sector. Stringent environmental regulations on wastewater discharge, widespread use in municipal purification facilities, and polymers' role in oil recovery are key factors driving demand. North America is a mature market offering stable growth due to continuous infrastructure investment and increasing adoption of high-quality water treatment solutions.

Key players operating in the Global Polyacrylamide Market include Chinafloc Chemical Co. Ltd, BASF SE, SNF Group, Anhui Tianrun Chemicals Co. Ltd, Henan Hangrui Environmental Protection Technology, Kemira Oyj, Ashland Global Holdings Inc., Beijing Hengju Chemical Group Co., Ltd., Wego Chemical Group Inc., Catalynt Solutions, Inc., Shandong Shuiheng Chemical Co. Ltd, Zibo East Polymer Co. Ltd, NNA Polymers, Inc., Henan Secco Environmental Protection Tech Co. Ltd, and Welldone Chemical Group. To strengthen their position, companies in the polyacrylamide industry are focusing on several strategic initiatives. They are investing in R&D to produce more efficient, environmentally friendly, and cost-effective polymers. Strategic partnerships, mergers, and acquisitions allow them to expand geographically and gain access to new customer segments. Firms are adopting advanced manufacturing technologies to improve quality and operational efficiency while reducing production costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Form

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Global advent of advanced waste treatment & disposal technologies

- 3.2.1.2 Developments across mining & textile industries

- 3.2.1.3 Expansion of shale gas & tight oil production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile raw material prices

- 3.2.2.2 Stringent residual monomer regulations

- 3.2.2.3 Environmental concerns over acrylamide toxicity

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand in water treatment applications

- 3.2.3.2 Expansion in enhanced oil recovery (EOR) and mining

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Anionic polyacrylamide (APAM)

- 5.3 Cationic polyacrylamide (CPAM)

- 5.4 Non-ionic polyacrylamide (NPAM)

- 5.5 Amphoteric polyacrylamide

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022 - 2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.3 Emulsion

- 6.4 Liquid

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Water & wastewater treatment

- 7.3 Enhanced oil recovery (EOR)

- 7.4 Mining & mineral processing

- 7.5 Agriculture

- 7.6 Textiles & dyeing

- 7.7 Cosmetics & personal care

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 SNF Group

- 9.2 Kemira Oyj

- 9.3 BASF SE

- 9.4 Ashland Global Holdings Inc.

- 9.5 NNA Polymers, Inc.

- 9.6 Wego Chemical Group Inc.

- 9.7 Catalynt Solutions, Inc.

- 9.8 Chinafloc Chemical Co. Ltd

- 9.9 Henan Hangrui Environmental Protection Technology

- 9.10 Shandong Shuiheng Chemical Co. Ltd

- 9.11 Anhui Tianrun Chemicals Co. Ltd

- 9.12 Zibo East Polymer Co. Ltd

- 9.13 Welldone Chemical Group

- 9.14 Henan Secco Environmental Protection Tech Co. Ltd

- 9.15 Beijing Hengju Chemical Group Co., Ltd.

2026年全球聚丙烯酰胺市场报告

2026年全球聚丙烯酰胺市场报告 聚丙烯酰胺奈米球市场:依合成方法、粒径、分子量、应用及通路-2026-2032年全球预测聚丙烯酰胺市场(造纸用):依离子电荷、分子量、形态、应用和最终用途划分,全球预测(2026-2032年)

聚丙烯酰胺奈米球市场:依合成方法、粒径、分子量、应用及通路-2026-2032年全球预测聚丙烯酰胺市场(造纸用):依离子电荷、分子量、形态、应用和最终用途划分,全球预测(2026-2032年) 聚丙烯酰胺:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

聚丙烯酰胺:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 聚丙烯酰胺市场-2026-2031年预测聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测

聚丙烯酰胺市场-2026-2031年预测聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测 湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年)聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测)

湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年)聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测) 全球聚丙烯酰胺市场(2025年)

全球聚丙烯酰胺市场(2025年) 聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034)

聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034)