|

市场调查报告书

商品编码

1907311

聚丙烯酰胺:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Polyacrylamide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

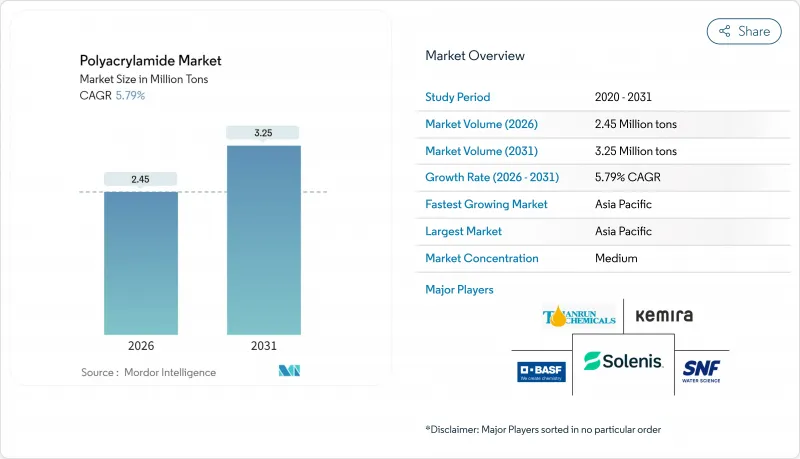

预计到2026年,聚丙烯酰胺市场规模将达到245万吨,高于2025年的232万吨。预计到2031年将达到325万吨,2026年至2031年的复合年增长率为5.79%。

推动这项扩张的关键因素包括市政和工业污水处理对高性能凝聚剂的需求不断增长、传统型页岩完井作业中超高分子量减磨剂的快速应用,以及日益严格的零液体排放法规。此外,中国对水利基础设施的数十亿美元投资以及BASF的大规模产能扩张也使市场相关人员受益,这确保了原材料的稳定供应并缩短了供应链。

全球聚丙烯酰胺市场趋势与洞察

在提高石油采收率(EOR)的应用日益广泛

石油生产商正以高性能高聚丙烯酰胺(HPAM)配方取代水基驱油化学品,即使在具有挑战性的储存中,也能达到6%至27%的增采率。北美页岩地层的现场试验表明,超高分子量聚丙烯酰胺能够在高盐环境和低至120°C的温度下稳定黏度,从而减少化学品补充频率和停机时间。此外,氧化石墨烯增强的HPAM提高了热稳定性,释放了在高温、高压、深层储存中进行三次采油的潜力。市场领导正在扩展专门的研发平台,以开发针对特定储存化学性质的聚合物驱油方案。这使得企业能够透过服务合约和高级产品定价创造价值,而提高采收率目前已成为聚丙烯酰胺市场成长最快的收入来源。

市政和工业污水处理中对凝聚剂的需求不断增长

公共产业报告称,与传统凝聚剂相比,新型絮凝剂可降低高达 95% 的浊度,同时减少化学品消费量。亚太地区的工业用户正在转向采用先进的凝聚剂系统,以满足美国环保署 (EPA) 的零排放标准并实现製程用水的再利用。用于去除重金属的新配方正在填补镉和铬的监管空白,从而扩大目标客户群。这些趋势将支撑聚丙烯酰胺市场在水处理领域的长期扩张。

残留丙烯酰胺单体的健康和致癌性问题

监管机构将食品接触材料中的丙烯酰胺残留量限制在0.2%以下,化妆品中的丙烯酰胺残留量限制在0.1%以下,这迫使生产商投资于更严格的纯化製程。加州65号提案的分类以及国际癌症研究机构(IARC)将其列为可能致癌性,都提高了标籤标註和监测的要求。合规措施可能会增加生产成本,并延迟产品核可,从而降低潜在需求。拥有先进品质保证实验室的製造商可以将此限制转化为竞争优势,而中小企业则面临被市场淘汰的风险,这可能会减缓聚丙烯酰胺市场的整体成长。

细分市场分析

预计到2025年,粉状聚丙烯酰胺将占聚丙烯酰胺市场规模的43.78%,这主要得益于其易于批量加工以及大规模市政计划运输成本低廉。然而,液态乳液正迅速普及,预计到2031年将以6.10%的年复合成长率(CAGR)增长,这主要归功于其即时溶解性和分子量保持性,能够减少页岩完井作业和高温工业迴路中的製程停机时间。

包装形式的改变也反映了这一趋势。北美正从桶装转向IBC吨桶,以提高现场计量精度;而中国供应商则在扩建反相乳液反应器,以将活性聚合物含量提高到50%。因此,儘管粉末在对成本高度敏感的供水事业仍保持优势,但乳液在性能至关重要的细分市场中正获得更高的附加价值,这标誌着聚丙烯酰胺行业正向特种化学品领域走向成熟。

本报告按物理形态(粉末、液体、乳液/分散体)、应用领域(提高石油采收率、水处理凝聚剂、土壤改良剂等)、终端用户行业(水处理、石油天然气、纸浆造纸等)和地区(亚太地区、北美、欧洲、南美、中东和非洲)对聚丙烯酰胺进行分析。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占据全球聚丙烯酰胺市场份额的49.92%,年复合成长率达6.20%,主要得益于中国450亿美元的水处理项目。该地区产能扩张与本地需求的良性循环使其免受供应衝击,并维持了定价权。印度的化学工业走廊和日本在膜技术领域的领先地位进一步推动了这一增长,而东南亚国家则受益于製造地的转移,这些基地需要先进的废水处理解决方案。

北美是高利润率强化采油(EOR)和减摩级产品的关键市场,页岩气开发延长了产品生命週期,并为SNF等供应商提供了收购配套成品油公司的机会。美国环保署(EPA)的零排放法规进一步促进了工业污水计划的稳定销售。欧洲的销售成长速度有所放缓,但仍是生物基创新领域的标竿。该地区的绿色采购政策正在推动可生物降解凝聚剂的研发,而化学和采矿业的特殊应用则支撑了对聚合物的潜在需求。

中东和非洲是新兴成长型市场,丰富的油田和矿产资源推动了当地产能的扩张。在南美洲,铜和锂的繁荣带动了对沉淀助剂的需求,而政府主导的水利基础设施现代化计划也扩大了潜在需求。这种地理多元化是支撑聚丙烯酰胺市场永续成长的核心因素。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在提高石油采收率(EOR)的应用日益广泛

- 市政和工业污水处理中对凝聚剂的需求不断增长

- 采矿活动的扩张带动了对定居辅助用品的需求

- 政府关于零液体排放和污泥减量的法规

- 页岩完井作业向超高分子减磨剂过渡

- 市场限制

- 残留丙烯酰胺单体的健康和致癌性问题

- 欧洲对生物基凝聚剂的需求日益增长

- 中国和独联体丙烯腈原料供应链的脆弱性

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依实体形态

- 粉末

- 液体

- 乳液/分散体

- 透过使用

- 提高石油产量

- 水处理凝聚剂

- 土壤改良剂

- 化妆品中的黏合剂和稳定剂

- 其他用途

- 按最终用户行业划分

- 水处理

- 石油和天然气

- 纸浆和造纸

- 矿业

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AnHui JuCheng Fine Chemicals Co. Ltd

- Anhui Tianrun Chemical Industry Co. Ltd

- Ashland

- BASF

- Beijing Hengju Chemical Group Co. Ltd

- Beijing Xitao Technology Development Co. Ltd

- CHINAFLOC

- Envitech Chemical Specialities Pvt. Ltd

- Kemira

- Liaocheng Yongxing Environmental Protection Science & Technology Co. Ltd

- Qingdao Oubo Chemical Co. Ltd

- Shandong Tongli Chemical Co. Ltd

- SNF

- Solenis

- Syensqo

- Universal Fine Chemicals SPC

- Yixing Cleanwater Chemicals Co. Ltd

第七章 市场机会与未来展望

Polyacrylamide market size in 2026 is estimated at 2.45 million tons, growing from 2025 value of 2.32 million tons with 2031 projections showing 3.25 million tons, growing at 5.79% CAGR over 2026-2031.

Rising demand for high-performance flocculants in municipal and industrial wastewater treatment, the rapid adoption of ultra-high-molecular-weight friction reducers in unconventional shale completions, and stricter zero-liquid-discharge mandates are the primary forces driving this expansion. Market players are also benefiting from China's multibillion-dollar investments in water infrastructure and BASF's large-scale capacity additions, which secure raw material availability and shorten supply chains.

Global Polyacrylamide Market Trends and Insights

Growing Utilization in Enhanced Oil Recovery (EOR)

Oil producers are replacing water-based flooding reagents with high-performance HPAM formulations that add 6%-27% incremental recovery, even in harsh reservoirs. Field results from North American shale plays confirm that ultra-high-molecular-weight polyacrylamide stabilizes viscosity under high salinity and 120 °C, cutting chemical top-ups and downtime. Graphene-oxide-reinforced HPAM further boosts thermal stability, unlocking tertiary recovery opportunities in deep, hot reservoirs. Market leaders are scaling dedicated research and development platforms to tailor polymer flooding packages to reservoir-specific chemistries, capturing value through service contracts and premium product pricing. As a result, enhanced oil recovery now represents the fastest-growing revenue stream within the polyacrylamide market.

Increasing Demand for Flocculants in Municipal and Industrial Wastewater Treatment

Utilities report up to 95% turbidity reduction with lower chemical consumption versus conventional coagulants. Industrial users in Asia-Pacific are migrating to advanced flocculant systems to meet EPA-style zero-discharge limits and recycle process water. New formulations that target heavy-metal removal address cadmium and chromium compliance gaps, broadening the addressable client base. These dynamics underpin the long-term expansion of the polyacrylamide market in water treatment.

Health and Carcinogenicity Concerns Over Residual Acrylamide Monomer

Regulators limit residual acrylamide to below 0.2% in food-contact materials and 0.1% in cosmetics, forcing producers to invest in tighter purification regimes. California's Proposition 65 classification and IARC's probable carcinogen status intensify labeling and monitoring obligations. Compliance raises production costs and slows product approvals in consumer-facing segments, trimming potential demand. Producers with advanced QA laboratories can turn the constraint into a competitive edge, but smaller firms risk market exit, softening overall polyacrylamide market growth.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Mining Activities Driving Demand for Sedimentation Aids

- Government Mandates on Zero-Liquid-Discharge and Sludge Reduction

- Rising Preference for Bio-Based Flocculants in Europe

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The powder segment held a 43.78% share of the polyacrylamide market size in 2025, supported by ease of bulk handling and lower freight costs for high-volume municipal projects. However, liquid emulsions are gaining rapid traction, with a 6.10% CAGR forecast to 2031, because instant solubility and molecular-weight preservation reduce process downtime in shale completions and high-temperature industrial circuits.

Packaging shifts illustrate the trend: drum-to-IBC conversions are rising in North America to improve onsite dosing precision, while Chinese suppliers are expanding inverse-emulsion reactors that raise active-polymer content to 50%. Powder therefore retains its stronghold in cost-sensitive water utilities, but emulsions capture incremental value in performance-critical niches, underscoring the maturation of the polyacrylamide industry toward specialized chemistries.

The Polyacrylamide Report is Segmented by Physical Form (Powder, Liquid, and Emulsion/Dispersions), Application (Enhanced Oil Recovery, Flocculants for Water Treatment, Soil Conditioner, and More), End-User Industry (Water Treatment, Oil and Gas, Pulp and Paper, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific captured 49.92% of the global polyacrylamide market share in 2025 and is growing at a 6.20% CAGR, propelled by China's USD 45 billion water-treatment program. The region's self-reinforcing loop of capacity expansion and local demand insulates it from supply shocks and sustains pricing power. India's chemicals corridor and Japan's membrane-technology leadership add further impetus, while Southeast Asian states benefit from manufacturing relocations that demand advanced effluent solutions.

North America remains a powerhouse for high-margin EOR and friction-reducer grades, with shale activity extending product lifecycles and enabling suppliers like SNF to acquire complementary completion-fluid firms. EPA zero-discharge rules further underpin steady sales into industrial wastewater projects. Europe shows slower volume growth but is a bellwether for bio-based innovation; its green-procurement policies stimulate research and development in biodegradable flocculants, while specialty applications in chemicals and mining uphold baseline polymer demand.

The Middle East and Africa are emerging growth theaters, leveraging abundant oilfields and mining prospects to justify local capacity additions. South America's copper and lithium boom likewise drives sedimentation-aid uptake, while government projects to modernize water infrastructure broaden addressable demand. Geographic diversification therefore remains central to sustaining resilient expansion in the polyacrylamide market.

- AnHui JuCheng Fine Chemicals Co. Ltd

- Anhui Tianrun Chemical Industry Co. Ltd

- Ashland

- BASF

- Beijing Hengju Chemical Group Co. Ltd

- Beijing Xitao Technology Development Co. Ltd

- CHINAFLOC

- Envitech Chemical Specialities Pvt. Ltd

- Kemira

- Liaocheng Yongxing Environmental Protection Science & Technology Co. Ltd

- Qingdao Oubo Chemical Co. Ltd

- Shandong Tongli Chemical Co. Ltd

- SNF

- Solenis

- Syensqo

- Universal Fine Chemicals SPC

- Yixing Cleanwater Chemicals Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Utilization in Enhanced Oil Recovery (EOR)

- 4.2.2 Increasing Demand for Flocculants in Municipal and Industrial Wastewater Treatment

- 4.2.3 Expansion of Mining Activities Driving Demand for Sedimentation Aids

- 4.2.4 Government Mandates on Zero-Liquid-Discharge and Sludge Reduction

- 4.2.5 Shift Toward Ultra-High-Molecular-Weight Friction Reducers for Shale Completions

- 4.3 Market Restraints

- 4.3.1 Health And Carcinogenicity Concerns over Residual Acrylamide Monomer

- 4.3.2 Rising Preference for Bio-Based Flocculants in Europe

- 4.3.3 Supply-Chain Vulnerability of Acrylonitrile Feedstock in China and CIS

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Physical Form

- 5.1.1 Powder

- 5.1.2 Liquid

- 5.1.3 Emulsion/Dispersions

- 5.2 By Application

- 5.2.1 Enhanced Oil Recovery

- 5.2.2 Flocculants for Water Treatment

- 5.2.3 Soil Conditioner

- 5.2.4 Binders and Stabilizers in Cosmetics

- 5.2.5 Other Applications

- 5.3 By End-User Industry

- 5.3.1 Water Treatment

- 5.3.2 Oil and Gas

- 5.3.3 Pulp and Paper

- 5.3.4 Mining

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AnHui JuCheng Fine Chemicals Co. Ltd

- 6.4.2 Anhui Tianrun Chemical Industry Co. Ltd

- 6.4.3 Ashland

- 6.4.4 BASF

- 6.4.5 Beijing Hengju Chemical Group Co. Ltd

- 6.4.6 Beijing Xitao Technology Development Co. Ltd

- 6.4.7 CHINAFLOC

- 6.4.8 Envitech Chemical Specialities Pvt. Ltd

- 6.4.9 Kemira

- 6.4.10 Liaocheng Yongxing Environmental Protection Science & Technology Co. Ltd

- 6.4.11 Qingdao Oubo Chemical Co. Ltd

- 6.4.12 Shandong Tongli Chemical Co. Ltd

- 6.4.13 SNF

- 6.4.14 Solenis

- 6.4.15 Syensqo

- 6.4.16 Universal Fine Chemicals SPC

- 6.4.17 Yixing Cleanwater Chemicals Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

2026年全球聚丙烯酰胺市场报告

2026年全球聚丙烯酰胺市场报告 聚丙烯酰胺市场机会、成长要素、产业趋势分析及2026年至2035年预测

聚丙烯酰胺市场机会、成长要素、产业趋势分析及2026年至2035年预测 聚丙烯酰胺奈米球市场:依合成方法、粒径、分子量、应用及通路-2026-2032年全球预测聚丙烯酰胺市场(造纸用):依离子电荷、分子量、形态、应用和最终用途划分,全球预测(2026-2032年)

聚丙烯酰胺奈米球市场:依合成方法、粒径、分子量、应用及通路-2026-2032年全球预测聚丙烯酰胺市场(造纸用):依离子电荷、分子量、形态、应用和最终用途划分,全球预测(2026-2032年) 聚丙烯酰胺市场-2026-2031年预测聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测

聚丙烯酰胺市场-2026-2031年预测聚丙烯酰胺市场按应用、类型、分子量和形态划分-2025-2032年全球预测 湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年)聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测)

湿强树脂的全球市场:各类型树脂,各用途 - 产业动态,市场规模,机会分析,预测(2025年~2033年)聚丙烯酰胺市场规模(按类型、应用、地区、范围和预测) 全球聚丙烯酰胺市场(2025年)

全球聚丙烯酰胺市场(2025年) 聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034)

聚丙烯酰胺(PAM)全球市场需求、预测分析(2018-2034)