|

市场调查报告书

商品编码

1936660

香精市场机会、成长要素、产业趋势分析及预测(2026-2035年)Flavors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

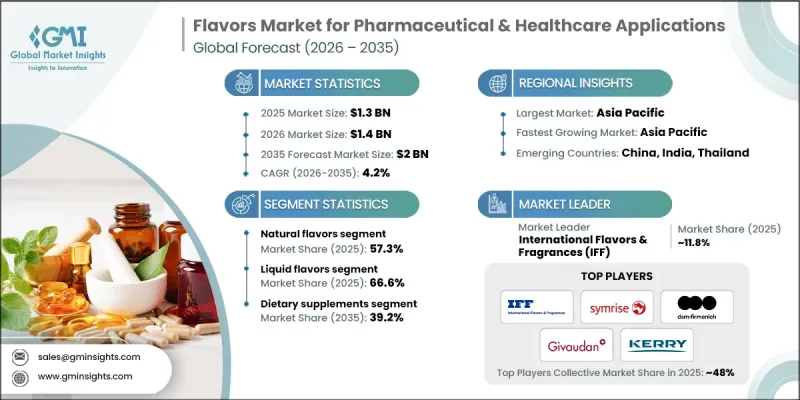

全球医药和保健应用香精市场预计到 2025 年将达到 13 亿美元,到 2035 年将达到 20 亿美元,年复合成长率为 4.2%。

该市场为製药和保健品製造商提供功能性香精系统,旨在提升药品和保健食品配方的偏好、提高患者依从性并改善整体感官品质。这些解决方案旨在消除不良口味、改善配方可接受性,并满足不断变化的法规和消费者期望。药用级香精适用于多种配方类别,在优化剂量、实现感官平衡和配方一致性方面发挥关键作用。药品产量持续成长、消费者对健康产品的日益增长的需求以及香精科学的不断创新共同推动了市场的发展。製造商正大力投资先进的掩味技术和以性能为导向的香精开发,以支持各种治疗应用。与此同时,该行业正经历着向洁净标示、更加重视天然成分以及需要符合监管标准和全球医疗保健体系中不断变化的消费者偏好的透明配方方法的转变。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 13亿美元 |

| 预测金额 | 20亿美元 |

| 复合年增长率 | 4.2% |

2025年,天然香料市占率达到57.3%,预计2026年至2035年将以4.2%的复合年增长率成长。其市场主导地位得益于其在药品製剂中的高接受度、与洁净标示理念的契合以及在多个产品类型中始终如一的卓越表现。这些香料解决方案在有效优化口味的同时,也能确保符合监管要求和製剂稳定性。与药品成分和剂型的广泛兼容性进一步巩固了其在全球主要生产区域的主导地位。

预计到2025年,液体香精製剂市场份额将达到66.6%,并预计到2035年将以4.2%的复合年增长率增长。此细分市场的主导地位归功于其与製药生产流程的高效整合、均匀分散性和可靠的香精输送。液体系统能够实现均匀的感官特性,同时兼顾可扩展性和运作效率。其对各种配方需求的适应性不断增强,进一步巩固了其在全球医药和医疗保健产品开发中的作用。

预计到2025年,美国医药和医疗保健应用香精市场规模将达3.276亿美元。推动美国市场成长的主要因素包括持续的製药生产活动、日益复杂的製剂配方以及对能够遵守用药和产品差异化的香精系统的强劲需求。先进的生产基础设施和製剂技术的不断创新也持续支撑着美国市场的稳定需求。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按口味

- 未来市场趋势

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依口味分類的市场估计与预测,2022-2035年

- 天然香氛

- 水果口味

- 薄荷味

- 香草口味

- 巧克力口味

- 其他的

- 合成/人工香料

- 其他的

第六章 按类型分類的市场估算与预测,2022-2035年

- 液态香精

- 粉/干香精

- 膏状/凝胶状香精

- 其他的

第七章 按应用领域分類的市场估算与预测,2022-2035年

- 非处方药

- 营养补充品

- 维生素和矿物质

- 蛋白质和胺基酸

- 膳食纤维

- 欧米伽脂肪酸

- 其他的

- 治疗性营养

- 医学营养

- 婴儿营养

- 运动营养

- 临床营养不良

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- International Flavors &Fragrances(IFF)

- Symrise AG

- DSM-Firmenich

- Givaudan

- Takasago International Corporation

- Kerry Group

- Sensient Technologies

- MANE SA

- Glanbia Nutritionals

- Prinova(Nagase Group)

- Metarom Group

- Roquette

- FONA International

- Keva Flavours

- Sensapure

The Global Flavors Market for Pharmaceutical & Healthcare Applications was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 2 billion by 2035.

The market supports pharmaceutical and healthcare manufacturers by providing functional flavor systems designed to improve palatability, support patient adherence, and enhance overall sensory quality in medicinal and wellness formulations. These solutions are engineered to neutralize unpleasant taste profiles, improve formulation acceptance, and align with evolving regulatory and consumer expectations. Available across multiple formulation categories, pharmaceutical-grade flavors serve critical roles in dosage optimization, sensory balance, and formulation consistency. Ongoing growth in pharmaceutical production volumes, increasing consumption of health-focused products, and continuous innovation in flavor science are collectively shaping market momentum. Manufacturers are investing heavily in advanced taste-masking techniques and performance-focused flavor development to support a wide range of therapeutic applications. At the same time, the industry is undergoing a clean-label transformation, with growing emphasis on naturally sourced ingredients and transparent formulation practices that align with regulatory standards and shifting consumer preferences across global healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $2 Billion |

| CAGR | 4.2% |

The natural flavors segment accounted for 57.3% share in 2025 and is expected to grow at a CAGR of 4.2% from 2026 to 2035. Their dominance is supported by strong acceptance across pharmaceutical formulations, alignment with clean-label initiatives, and consistent performance across multiple product categories. These flavor solutions offer effective taste optimization while maintaining regulatory compliance and formulation stability. Their broad compatibility with pharmaceutical ingredients and delivery formats reinforces their leading position across major production regions worldwide.

The liquid flavor formats segment held a 66.6% share in 2025 and is forecast to grow at a CAGR of 4.2% through 2035. This segment leads due to efficient incorporation into pharmaceutical manufacturing processes, consistent dispersion, and reliable flavor delivery. Liquid systems support uniform sensory outcomes while enabling scalable production and operational efficiency. Their adaptability across diverse formulation requirements continues to strengthen their role in pharmaceutical and healthcare product development globally.

U.S. Flavors Market for Pharmaceutical & Healthcare Applications generated USD 327.6 million in 2025. Growth in the country is driven by sustained pharmaceutical manufacturing activity, rising formulation complexity, and strong demand for flavor systems that enhance compliance and product differentiation. Advanced production infrastructure and continuous innovation in formulation technologies continue to support steady demand across the United States.

Key companies active in the Global Flavors Market for Pharmaceutical & Healthcare Applications include Givaudan, DSM-Firmenich, Sensient Technologies, International Flavors & Fragrances, Kerry Group, MANE SA, Takasago International Corporation, Glanbia Nutritionals, Metarom Group, Prinova under the Nagase Group, Roquette, Keva Flavours, Sensapure, FONA International, and Symrise AG. These players maintain competitive positions through innovation, regulatory expertise, and diversified flavor portfolios. To strengthen their presence, companies in the pharmaceutical and healthcare flavors sector focus on continuous investment in research and development to enhance taste-masking efficiency and formulation performance. Strategic expansion into high-growth regions and long-term partnerships with pharmaceutical manufacturers help secure stable demand. Many firms emphasize clean-label innovation and natural ingredient sourcing to align with regulatory trends and customer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By flavor

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Flavor, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Natural flavors

- 5.2.1 Fruit-based flavors

- 5.2.2 Mint flavors

- 5.2.3 Vanilla flavors

- 5.2.4 Chocolate flavors

- 5.2.5 Others

- 5.3 Synthetic / artificial flavors

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Liquid flavors

- 6.3 Powder / dry flavors

- 6.4 Paste / gel flavors

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 OTC drugs

- 7.2 Dietary supplements

- 7.2.1 Vitamins & minerals

- 7.2.2 Proteins & amino acids

- 7.2.3 Dietary fibers

- 7.2.4 Omega fatty acids

- 7.2.5 Others

- 7.3 Therapeutic nutrition

- 7.4 Healthcare nutrition

- 7.4.1 Infant nutrition

- 7.4.2 Sports nutrition

- 7.4.3 Clinical malnutrition

- 7.4.4 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 International Flavors & Fragrances (IFF)

- 9.2 Symrise AG

- 9.3 DSM-Firmenich

- 9.4 Givaudan

- 9.5 Takasago International Corporation

- 9.6 Kerry Group

- 9.7 Sensient Technologies

- 9.8 MANE SA

- 9.9 Glanbia Nutritionals

- 9.10 Prinova (Nagase Group)

- 9.11 Metarom Group

- 9.12 Roquette

- 9.13 FONA International

- 9.14 Keva Flavours

- 9.15 Sensapure