|

市场调查报告书

商品编码

1959288

V2X 资料品质保证市场机会、成长要素、产业趋势分析及 2026 年至 2035 年预测V2X Data Quality Assurance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

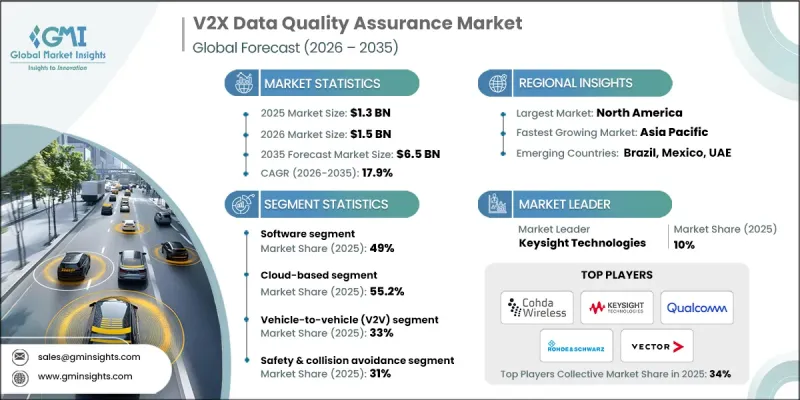

2025 年全球 V2X 数据品质保证市场价值为 13 亿美元,预计到 2035 年将达到 65 亿美元,年复合成长率为 17.9%。

这一成长反映了汽车生态系统和交通基础设施在互联出行、自动驾驶技术进步以及数位化道路基础设施整合的推动下,正加速转型。产业相关人员正积极应对由不断演进的通讯标准、网路安全要求、监管协调、智慧基础设施投资以及进阶检验要求等因素所带来的结构性变化。随着车联网(V2X)成为智慧型运输系统(ITS)的基础,对稳健的测试、检验和监控框架的需求持续成长。向下一代无线技术的过渡以及车辆、路侧和云端互操作系统的日益复杂化进一步推动了市场扩张。持续检验讯息的准确性、延迟、认证和可靠性对于维护运行完整性至关重要。随着全球部署的扩展,相关人员正优先考虑容错架构和标准化合规框架,以确保在2035年建立一个安全、可靠且高效能的车联网生态系统。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 13亿美元 |

| 预测金额 | 65亿美元 |

| 复合年增长率 | 17.9% |

V2X 资料品质保证产业的关键组成部分之一是安全凭证管理系统 (SCMS),这是一个由美国运输部定义的公开金钥基础建设,所有 V2X 部署都必须采用。该架构支援基于凭证的身份验证,从而实现加密通信,旨在保护匿名性的同时,确保资料的完整性和真实性。该框架还支援识别和移除受损及不合规的设备,从而在互联行动网路中强化持续的、反馈驱动的品质保证循环。

软体领域预计在2025年将占据49%的市场份额,并在2026年至2035年间以19%的复合年增长率成长。这一主导地位凸显了软体驱动的检验工具在管理V2X生态系统的技术复杂性方面发挥的关键作用。核心产品包括通讯协定分析解决方案、网路模拟环境、自动化测试框架、一致性检验平台和即时监控系统。联邦机构采用的开放原始码智慧型运输系统软体计画进一步加强了这个生态系统。品质保证平台必须检验SAE J2735标准中规定的各种讯息格式,以确保安全、交通管理、旅客资讯和路侧通讯交换的可靠性。

预计到2025年,基于云端的部署模式将占据55.2%的市场份额,且成长速度最快,到2035年复合年增长率将达到18.8% 。云端对应平臺因其初始投资要求低、扩充性、部署速度快以及软体更新高效等优势,正受到汽车零件供应商、出行Start-Ups和区域运输机构的青睐。透过将检验环境迁移到云端基础设施,企业无需建造资本密集型设施即可使用先进的测试工具。远端和分散式检验功能使运作不同地理区域的车辆和基础设施系统能够无缝连接到集中式品质保证环境。

预计到2025年,北美V2X数据品质保证市场规模将达到3.535亿美元,并在2026年至2035年间以17.5%的复合年增长率成长。美国拥有许多优势,包括高联网汽车普及率、先进的数位道路基础设施以及成熟的汽车和技术生态系统,这些都为互通性测试和讯息检验工具提供了支援。跨多个州的大规模联网汽车部署需要持续的效能监控和系统的品质检验,以确保运作安全和通讯可靠性。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 联网汽车和自动驾驶汽车的广泛应用。

- 政府关于V2X安全标准的强制规定

- 在安全性至关重要的应用中,对即时资料检验的需求日益增长。

- 智慧交通基础设施的发展

- V2X通讯中网路安全的需求

- 产业潜在风险与挑战

- 高昂的实施成本和基础设施成本

- 多重标准 V2X 环境(DSRC 与 C-V2X)的复杂性

- 缺乏统一的全球标准

- OEM厂商间互通性挑战

- 市场机会

- 新兴技术:5G-V2X 和 6G-V2X 技术

- 智慧城市和智慧交通系统基础设施扩建

- 售后服务需求不断成长

- 人工智慧驱动的预测数据品质解决方案

- V2X相容于电动车充电(V2G)品质保证

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国联邦V2X法规和频段分配

- 加拿大 - 连网和自动驾驶汽车安全框架 (CASF)

- 欧洲

- 德国、欧盟智慧交通系统和国家倡议

- 英国-脱欧后的V2X柔软性

- 法国——国家车联网试验与智慧交通系统战略

- 义大利——智慧交通系统试点计画和智慧基础设施

- 亚太地区

- 中国工信部C-V2X强制性法规与标准

- 印度—新兴的V2X和汽车互联法规

- 日本——智慧交通系统连结性与频率政策

- 澳洲—技术中立的智慧交通系统政策

- LATAM

- 墨西哥 - NOM车辆安全标准

- 阿根廷 - 国家交通法 24.449

- 中东和非洲

- 南非共和国 - 道路交通法(1996 年)

- 沙乌地阿拉伯—交通运输法律与2030愿景交通运输政策

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 基于有效性的检测机制

- 机器学习方法(多层感知器、支援向量机、深度学习)

- 人工智慧和机器学习在数据品质方面的应用

- 用于V2X资料完整性的区块链

- 新兴技术

- 用于即时检验的边缘运算

- 量子抗性密码技术的发展

- 数位双胞胎与模拟技术

- 5G网路切片提升V2X质量

- 当前技术趋势

- 专利分析

- 价格分析

- 软体授权定价模式

- 硬体价格趋势

- 专业服务收费系统

- 使用案例和成功案例

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 最佳实践和实施指南

- 设计品质保证框架

- 实施最佳实践

- 数据品管最佳实践

- 安全最佳实践

- 效能优化最佳实践

- 监理合规最佳实践

- 引言场景和模型

- 都市区实施方案

- 主要道路发展方案

- 农村和偏远地区的部署场景

- 混合技术引入方案

- 特殊环境场景

- 产品和服务基准测试

- 软体功能比较矩阵

- 硬体技术规格基准测试

- 服务组合和服务等级协定比较

- 定价和总拥有成本分析

- 未来前景与机会

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依组件划分,2022-2035年

- 软体

- 资料检验和清洗

- 分析与异常检测

- 即时监测与分析

- 模拟和测试平台

- 合规和报告软体

- 硬体

- 感应器

- 通讯模组

- 边缘/处理单元

- 汽车单元(OBU)

- 路侧单元(RSU)

- 服务

- 咨询

- 系统整合

- 引言和部署

- 维护和支援

- 培训和文檔

第六章 市场估算与预测:依部署类型划分,2022-2035年

- 现场

- 基于云端的

第七章 市场估计与预测:依性别分類的互联互通情况,2022-2035年

- 车对车(V2V)通信

- 车路通讯(V2I)

- 车行通讯(V2P)

- 车联网(V2N)

- 其他的

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 安全/防碰撞

- 交通管理与优化

- 自动驾驶和进阶驾驶辅助系统

- 车队管理

- 其他的

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 汽车製造商

- 政府机构

- 车队营运商

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十一章:公司简介

- 世界玩家

- Anritsu

- Cohda Wireless

- IPG Automotive

- Keysight Technologies

- NI(National Instruments)

- Qualcomm Technologies

- Robert Bosch

- Rohde & Schwarz

- Vector Informatik

- VIAVI Solutions

- 本地球员

- Autotalks

- Commsignia

- Continental

- DEKRA

- Denso

- NOFFZ Technologies

- NXP Semiconductors

- Savari

- SEA Datentechnik

- Valeo Telematik

- 新兴科技创新者

- ADAS iiT

- Allion Labs

- msg

- Neusoft

- u-blox

The Global V2X Data Quality Assurance Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 17.9% to reach USD 6.5 billion by 2035.

The growth reflects accelerating transformation across automotive ecosystems and transportation infrastructure, fueled by connected mobility, autonomous driving advancements, and digital roadway integration. Industry participants are navigating structural shifts driven by evolving communication standards, cybersecurity mandates, regulatory alignment, smart infrastructure investments, and advanced validation requirements. As vehicle-to-everything communication becomes foundational to intelligent transportation systems, demand for robust testing, verification, and monitoring frameworks continues to expand. Market expansion is further supported by the transition to next-generation wireless technologies and the increasing complexity of interoperable vehicle, roadside, and cloud-based systems. Continuous validation of message accuracy, latency, authentication, and reliability is essential to maintain operational integrity. As deployment scales globally, stakeholders are prioritizing resilient architectures and standardized compliance frameworks to ensure safe, secure, and high-performance V2X ecosystems through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 17.9% |

A critical component of the V2X data quality assurance industry is the Security Credential Management System, a public key infrastructure framework defined by the US Department of Transportation and required across V2X implementations. This architecture enables encrypted communication supported by certificate-based authentication, designed to protect anonymity while safeguarding data integrity and authenticity. The framework also supports the identification and removal of compromised or non-compliant devices, reinforcing a continuous feedback-driven quality assurance loop within connected mobility networks.

The software segment accounted for 49% share in 2025 and is forecast to grow at a CAGR of 19% from 2026 to 2035. This dominance underscores the essential role of software-driven validation tools in managing the technical complexity of V2X ecosystems. Core offerings include protocol analysis solutions, network simulation environments, automated test frameworks, compliance validation platforms, and real-time monitoring systems. Open-source intelligent transportation software initiatives introduced by federal agencies have further strengthened the ecosystem. Quality assurance platforms must verify diverse message formats standardized under SAE J2735, ensuring reliability across safety, traffic management, traveler information, and roadside communication exchanges.

The cloud-based deployment models segment held 55.2% share in 2025 and is expanding at the fastest CAGR of 18.8% through 2035. Cloud-enabled platforms are gaining adoption among automotive suppliers, mobility startups, and regional transportation agencies due to lower upfront investment requirements, scalability, rapid deployment, and streamlined software updates. By shifting validation environments to cloud infrastructure, organizations can access sophisticated testing tools without building capital-intensive facilities. Remote and distributed validation capabilities allow vehicles and infrastructure systems operating in different geographic regions to connect seamlessly to centralized quality assurance environments.

North America V2X Data Quality Assurance Market generated USD 353.5 million in 2025 and is projected to grow at a CAGR of 17.5% from 2026 to 2035. The US benefits from strong connected vehicle adoption rates, advanced digital roadway infrastructure, and a mature automotive and technology ecosystem supporting interoperability testing and message validation tools. Large-scale connected vehicle deployments across multiple states require continuous performance monitoring and structured quality validation to maintain operational safety and communication reliability.

Key companies operating in the Global V2X Data Quality Assurance Market include Anritsu, Rohde & Schwarz, Vector Informatik, Keysight Technologies, NI (National Instruments), VIAVI Solutions, IPG Automotive, Cohda Wireless, Qualcomm Technologies, and Robert Bosch. Companies in the V2X Data Quality Assurance Market are strengthening their market position through strategic technology partnerships, advanced R&D investments, and expansion of cloud-native testing platforms. Leading players are focusing on interoperability validation solutions aligned with evolving 5G NR-V2X and future 6G standards. Many firms are integrating AI-driven analytics into quality monitoring platforms to enhance anomaly detection and predictive diagnostics. Strategic collaborations with automotive OEMs, infrastructure providers, and telecom operators are accelerating ecosystem integration.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Connectivity

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of connected and autonomous vehicles

- 3.2.1.2 Government mandates for V2X safety standards

- 3.2.1.3 Rising need for real-time data validation in safety-critical applications

- 3.2.1.4 Growth of smart transportation infrastructure

- 3.2.1.5 Demand for cybersecurity in V2X communications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and infrastructure costs

- 3.2.2.2 Complexity of multi-standard V2X environments (DSRC vs C-V2X)

- 3.2.2.3 Lack of unified global standards

- 3.2.2.4 Interoperability challenges across OEMs

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging 5G-V2X and 6G-V2X technologies

- 3.2.3.2 Smart city and ITS infrastructure expansion

- 3.2.3.3 Growing aftermarket services demand

- 3.2.3.4 AI-driven predictive data quality solutions

- 3.2.3.5 V2X-enabled electric vehicle charging (V2G) quality assurance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal V2X rules & spectrum allocation

- 3.4.1.2 Canada - safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national initiatives

- 3.4.2.2 UK- Post Brexit V2X flexibility

- 3.4.2.3 France- National V2X testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging V2X & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Plausibility-based detection mechanisms

- 3.7.1.2 Machine learning approaches (MLP, SVM, deep learning)

- 3.7.1.3 AI and machine learning for data quality

- 3.7.1.4 Blockchain for V2X data integrity

- 3.7.2 Emerging technologies

- 3.7.2.1 Edge computing for real-time validation

- 3.7.2.2 Quantum-safe cryptography development

- 3.7.2.3 Digital twin and simulation technologies

- 3.7.2.4 5G network slicing for V2X quality

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Software licensing pricing models

- 3.9.2 Hardware equipment pricing trends

- 3.9.3 Professional services pricing structure

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Best practices and implementation guidelines

- 3.12.1 Quality assurance framework design

- 3.12.2 Deployment best practices

- 3.12.3 Data quality management best practices

- 3.12.4 Security best practices

- 3.12.5 Performance optimization best practices

- 3.12.6 Regulatory compliance best practices

- 3.13 Deployment scenarios and models

- 3.13.1 Urban deployment scenarios

- 3.13.2 Highway deployment scenarios

- 3.13.3 Rural and remote deployment scenarios

- 3.13.4 Mixed technology deployment scenarios

- 3.13.5 Special environment scenarios

- 3.14 Product and service benchmarking

- 3.14.1 Software feature comparison matrix

- 3.14.2 Hardware technical specifications benchmarking

- 3.14.3 Service portfolio and SLA comparison

- 3.14.4 Pricing and total cost of ownership analysis

- 3.15 Future outlook and opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Data validation & cleansing

- 5.2.2 Analytics & anomaly detection

- 5.2.3 Real-time monitoring & analytics

- 5.2.4 Simulation & testing platforms

- 5.2.5 Compliance & reporting software

- 5.3 Hardware

- 5.3.1 Sensors

- 5.3.2 Communication modules

- 5.3.3 Edge/processing units

- 5.3.4 On-board units (OBUs)

- 5.3.5 Roadside units (RSUs)

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 System integration

- 5.4.3 Implementation & deployment

- 5.4.4 Maintenance & support

- 5.4.5 Training & documentation

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 On premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Vehicle-to-vehicle (V2V)

- 7.3 Vehicle-to-infrastructure (V2I)

- 7.4 Vehicle-to-pedestrian (V2P)

- 7.5 Vehicle-to-network (V2N)

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Safety & collision avoidance

- 8.3 Traffic management & optimization

- 8.4 Autonomous driving & ADAS

- 8.5 Fleet management

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Automotive OEMs

- 9.3 Government Agencies

- 9.4 Fleet Operators

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Anritsu

- 11.1.2 Cohda Wireless

- 11.1.3 IPG Automotive

- 11.1.4 Keysight Technologies

- 11.1.5 NI (National Instruments)

- 11.1.6 Qualcomm Technologies

- 11.1.7 Robert Bosch

- 11.1.8 Rohde & Schwarz

- 11.1.9 Vector Informatik

- 11.1.10 VIAVI Solutions

- 11.2 Regional Players

- 11.2.1 Autotalks

- 11.2.2 Commsignia

- 11.2.3 Continental

- 11.2.4 DEKRA

- 11.2.5 Denso

- 11.2.6 NOFFZ Technologies

- 11.2.7 NXP Semiconductors

- 11.2.8 Savari

- 11.2.9 SEA Datentechnik

- 11.2.10 Valeo Telematik

- 11.3 Emerging Technology Innovators

- 11.3.1 ADAS iiT

- 11.3.2 Allion Labs

- 11.3.3 msg

- 11.3.4 Neusoft

- 11.3.5 u-blox

2026年全球车对车通讯市场报告2026年全球汽车V2X市场报告

2026年全球车对车通讯市场报告2026年全球汽车V2X市场报告 车联网(V2X)市场机会、成长要素、产业趋势分析及2026年至2035年预测。

车联网(V2X)市场机会、成长要素、产业趋势分析及2026年至2035年预测。 全球汽车V2X技术市场规模、份额、趋势和成长分析报告:2026-2034年

全球汽车V2X技术市场规模、份额、趋势和成长分析报告:2026-2034年 全球汽车AR/VR使用者体验市场预测(至2034年),按车辆类型、技术、分销管道、应用、最终用户和地区划分

全球汽车AR/VR使用者体验市场预测(至2034年),按车辆类型、技术、分销管道、应用、最终用户和地区划分 汽车广角扩散器市场按产品类型、原料、推进方式、车辆类型、应用和最终用途划分-2026-2032年全球预测全球V2X通讯和网路市场预测至2032年:按通讯类型、组件、性别、应用和地区划分

汽车广角扩散器市场按产品类型、原料、推进方式、车辆类型、应用和最终用途划分-2026-2032年全球预测全球V2X通讯和网路市场预测至2032年:按通讯类型、组件、性别、应用和地区划分 汽车V2X市场规模、份额和成长分析(按通讯类型、交付类型、推进类型、连接性别、车辆类型、技术和地区划分)—产业预测(2026-2033年)

汽车V2X市场规模、份额和成长分析(按通讯类型、交付类型、推进类型、连接性别、车辆类型、技术和地区划分)—产业预测(2026-2033年) 汽车V2X市场(至2035年):依连接类型、通讯类型、车辆类型、推进类型、技术类型、地区、产业趋势及预测车对车 (V2V) 通讯市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2024-2032)

汽车V2X市场(至2035年):依连接类型、通讯类型、车辆类型、推进类型、技术类型、地区、产业趋势及预测车对车 (V2V) 通讯市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测 (2024-2032)