|

市场调查报告书

商品编码

1959290

汽车区域架构及网域控制器市场:机会、成长要素、产业趋势分析及2026年至2035年预测Automotive Zonal Architecture and Domain Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球汽车区域架构和网域控制器市场价值为 49 亿美元,预计到 2035 年将达到 207 亿美元,年复合成长率为 16.1%。

市场成长的驱动力在于汽车电子设备设计和整合方式的根本性转变。汽车製造商正从高度分散的电子系统转向更集中、以软体为中心的架构。传统的汽车设计依赖众多独立的电控系统,这些单元透过庞大的线路网路连接,导致车辆重量增加、生产复杂性提高以及製造成本上升。区域架构重新思考了这种方法,它基于车辆的实体区域组织电子设备,并透过高速资料网路连接它们,从而显着减少了布线需求。这种精简的结构有助于提高能源效率、简化组装流程,并推动向具有数位化可更新功能的软体定义车辆的过渡。先进的通讯协定加速了来自感测器和车载系统的数据处理,而改进的电源分配则有助于优化车辆性能,尤其是在电动平台上。这些综合优势正在加速全球汽车产业的采用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 49亿美元 |

| 预测金额 | 207亿美元 |

| 复合年增长率 | 16.1% |

网域控制器架构市场占有率高达 64.2%,预计到 2025 年将创造 32 亿美元的市场规模。汽车製造商倾向于集中式运算系统,因为这种系统可以将多种车辆功能整合到少量高性能单元中。透过将驾驶辅助、资讯娱乐和车身电子设备等领域整合到单一控制器中,製造商可以降低系统复杂性和布线密度。与传统的汽车电子设计相比,这种方法还提高了可扩展性,并有助于实现更高级的软体功能。

预计到2025年,乘用车市占率将达到89.7%,到2035年市场规模将达到181亿美元。由于先进数位功能和互联技术的日益集中化,该领域的普及率很高。高产量和消费者对创新的需求使得乘用车成为实施基于区域和集中式电子系统的主要平台,从而能够高效管理复杂的车辆功能。

美国汽车业专用架构域控制器市场预计到2025年将达到14亿美元。软体定义汽车平臺的强劲发展正在重塑该地区市场,製造商优先采用集中式电子架构以支援远端软体更新和快速功能部署。这种转变正在推动电动车和下一代汽车对网域控制器解决方案的需求不断增长。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 车辆电气化进展

- 软体定义车辆的普及应用不断扩大

- 对ADAS(高级驾驶辅助系统)的需求不断增长

- 增强的空中下载 (OTA) 更新功能

- 产业潜在风险与挑战

- 网路安全与功能安全挑战

- 开发和整合高度复杂

- 市场机会

- 电动汽车和混合动力汽车平台的发展

- 汽车乙太网路技术的进步

- 扩展以软体为中心的汽车生态系统

- 自动驾驶商用车领域的新机会

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 联邦通讯委员会

- 美国国家公路交通安全管理局(NHTSA)

- 加州空气资源委员会(CARB)

- 加拿大运输部

- 欧洲

- 欧盟委员会

- 联合国欧洲经济委员会世界汽车法规协调论坛

- 车辆认证机构

- 亚太地区

- 中华人民共和国工业与资讯化部(工信部)

- 日本汽车标准化国际中心

- 汽车业标准(AIS)

- 拉丁美洲

- 巴西汽车工业协会(ANFAVEA)

- INMETRO

- 国家公路安全委员会

- 中东和非洲

- 海湾标准组织

- 南非标准局

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响和对社区的贡献

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 架构与系统设计

- 网域控制器架构基础知识

- 区域建筑设计原则

- 混合架构实施策略

- 集中式和分散式计算模型

- 高效能运算(HPC)的集成

- 车辆伺服器架构

- 区域网关设计与部署

- 软体定义车辆(SDV)策略

- 服务导向架构(SOA)的实施

- 中介软体平台和标准

- 自动驾驶车辆中的区域架构

- ADAS领域在区域系统中的集成

- 自动驾驶的感测器融合架构

- 即时数据处理要求

- 冗余和容错系统

- 专注的感知与决策

- 案例研究

- 未来前景与机会

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依建筑类型划分,2022-2035年

- 网域控制器架构

- 区域建筑

- 混合架构

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车

- 中型商用车

- 大型商用车辆

第七章 市场估计与预测:依驱动因素划分,2022-2035年

- 内燃机车

- 电动车和混合动力汽车

- 电池式电动车(BEV)

- 插电式混合动力车(PHEV)

- 燃料电池电动车(FCEV)

第八章 市场估算与预测:依自动驾驶等级划分,2022-2035年

- 一级

- 二级

- 3级

- 4级和5级

第九章 市场估算与预测:依通讯协定,2022-2035年

- 基于 CAN/LIN 的系统

- 以乙太网路为基础的系统

第十章 市场估价与预测:依电压划分,2022-2035年

- 12V系统

- 48V系统

第十一章 市场估计与预测:依应用领域划分,2022-2035年

- ADAS领域

- 动力传动系统/电动车续航里程

- 身体与舒适类别

- 驾驶座/资讯娱乐区域

- 安全场

- 底盘和运动场

第十二章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 捷克共和国

- 比利时

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十三章:公司简介

- 世界公司

- Robert Bosch

- Continental

- Aptiv

- NXP Semiconductors

- Infineon

- Valeo

- STMicroelectronics

- Texas Instruments

- Visteon

- Harman

- Panasonic

- NVIDIA

- Qualcomm

- onsemi

- 区域玩家

- HiRain

- SemiDrive

- Sonatus

- ETAS

- Elektrobit

- Lear

- Magna

- Marelli

- DENSO

- 新兴企业

- TTTech

- GuardKnox

- Ambarella

- Aurora Labs

- Rivian

- AUMOVIO

- Molex

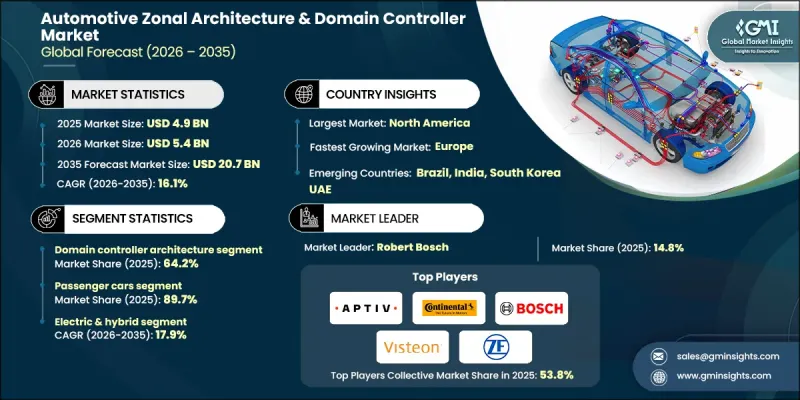

The Global Automotive Zonal Architecture & Domain Controller Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 16.1% to reach USD 20.7 billion by 2035.

Market growth is driven by a fundamental shift in how vehicle electronics are designed and integrated. Automakers are moving away from highly fragmented electronic systems toward more centralized and software-focused architectures. Traditional vehicle designs relied on many independent electronic control units connected through extensive wiring networks, which increased vehicle weight, production complexity, and manufacturing costs. Zonal architecture restructures this approach by organizing electronics based on physical vehicle zones and connecting them through high-speed data networks, significantly reducing wiring requirements. This streamlined structure improves energy efficiency, simplifies assembly processes, and supports the transition toward software-defined vehicles where functionality can be updated digitally. Advanced communication protocols enable faster data handling from sensors and onboard systems, while improved power distribution helps optimize vehicle performance, particularly in electrified platforms. Together, these benefits are accelerating adoption across the global automotive industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 16.1% |

The domain controller architecture segment held 64.2% share, generating USD 3.2 billion in 2025. Automakers are favoring centralized computing systems because they consolidate multiple vehicle functions into fewer, high-performance units. By integrating areas such as driver assistance, infotainment, and body electronics into unified controllers, manufacturers reduce system complexity and wiring density. This approach also enhances scalability and makes it easier to deploy advanced software capabilities compared to legacy vehicle electronics designs.

The passenger cars segment accounted for 89.7% share in 2025 and is expected to reach USD 18.1 billion by 2035. Adoption is higher in this segment due to the growing concentration of advanced digital features and connected technologies. High production volumes and consumer demand for innovation make passenger vehicles the primary platform for introducing zonal and centralized electronic systems, enabling more efficient management of complex vehicle functions.

U.S. Automotive Zonal Architecture & Domain Controller Market reached USD 1.4 billion in 2025. The regional market is being shaped by strong momentum toward software-defined vehicle platforms, with manufacturers emphasizing centralized electronic architectures to support remote software updates and faster feature deployment. This shift is reinforcing demand for domain controller solutions across electric and next-generation vehicles.

Key companies operating in the Global Automotive Zonal Architecture & Domain Controller Market include Robert Bosch, Aptiv, Continental, ZF, Visteon, Valeo, NXP, Infineon, Qualcomm, and Onsemi. Companies in the automotive zonal architecture and domain controller market are strengthening their market position through heavy investment in advanced semiconductor development and centralized computing platforms. Strategic partnerships with automakers and software providers are helping accelerate the integration of scalable electronic architectures. Many players are expanding research efforts focused on high-speed networking, power management, and cybersecurity to support software-defined vehicles. Portfolio diversification, regional expansion, and early involvement in next-generation vehicle programs are also key priorities.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Architecture

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Autonomy level

- 2.2.6 Communication Protocol

- 2.2.7 Voltage

- 2.2.8 Application

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification

- 3.2.1.2 Increasing software-defined vehicle adoption

- 3.2.1.3 Growing demand for advanced driver assistance systems (ADAS)

- 3.2.1.4 Expansion of over-the-air (OTA) update capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity and functional safety challenges

- 3.2.2.2 High development and integration complexity

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of electric and hybrid vehicle platforms

- 3.2.3.2 Advancements in automotive ethernet technologies

- 3.2.3.3 Expansion of Software-Centric Automotive Ecosystems

- 3.2.3.4 Emerging opportunities in autonomous commercial vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 California Air Resources Board (CARB)

- 3.4.1.4 Transport Canada

- 3.4.2 Europe

- 3.4.2.1 European Commission

- 3.4.2.2 UNECE World Forum for Harmonization of Vehicle Regulations

- 3.4.2.3 Vehicle Certification Agency

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT), China

- 3.4.3.2 Japan Automobile Standards Internationalization Center

- 3.4.3.3 Automotive Industry Standards (AIS)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian Association of Automotive Vehicle Manufacturers (ANFAVEA)

- 3.4.4.2 INMETRO

- 3.4.4.3 National Road Safety Commission

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standards Organization

- 3.4.5.2 South African Bureau of Standards

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Architecture & system design

- 3.11.1 Domain controller architecture fundamentals

- 3.11.2 Zonal architecture design principles

- 3.11.3 Hybrid architecture implementation strategies

- 3.11.4 Centralized vs decentralized computing models

- 3.11.5 High-performance computing (HPC) integration

- 3.12 Vehicle server architecture

- 3.12.1 Zonal gateway design and placement

- 3.12.2 Software Defined Vehicle (SDV) Strategy

- 3.12.3 Service-oriented architecture (SOA) implementation

- 3.12.4 Middleware platforms and standards

- 3.13 Zonal architecture in autonomous vehicles

- 3.13.1 ADAS domain integration in zonal systems

- 3.13.2 Sensor fusion architecture for autonomy

- 3.13.3 Real-time data processing requirements

- 3.13.4 Redundancy and fail-operational systems

- 3.13.5 Centralized perception and decision making

- 3.14 Case studies

- 3.15 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Architecture, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Domain controller architecture

- 5.3 Zonal architecture

- 5.4 Hybrid architecture

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Internal Combustion Engine (ICE) vehicles

- 7.3 Electric & hybrid vehicles

- 7.3.1 Battery Electric Vehicles (BEV)

- 7.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 7.3.3 Fuel Cell Electric Vehicles (FCEV)

Chapter 8 Market Estimates & Forecast, By Autonomy level, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Level 1

- 8.3 Level 2

- 8.4 Level 3

- 8.5 Level 4 & Level 5

Chapter 9 Market Estimates & Forecast, By Communication protocol, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 CAN / LIN-based system

- 9.3 Ethernet-based system

Chapter 10 Market Estimates & Forecast, By Voltage, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 12V system

- 10.3 48V system

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 ADAS domain

- 11.3 Powertrain / EV power domain

- 11.4 Body & comfort domain

- 11.5 Cockpit / infotainment domain

- 11.6 Safety domain

- 11.7 Chassis & motion domain

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 US

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Czech Republic

- 12.3.7 Belgium

- 12.3.8 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Singapore

- 12.4.7 Malaysia

- 12.4.8 Indonesia

- 12.4.9 Vietnam

- 12.4.10 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global players

- 13.1.1 Robert Bosch

- 13.1.2 Continental

- 13.1.3 Aptiv

- 13.1.4 NXP Semiconductors

- 13.1.5 Infineon

- 13.1.6 Valeo

- 13.1.7 STMicroelectronics

- 13.1.8 Texas Instruments

- 13.1.9 Visteon

- 13.1.10 Harman

- 13.1.11 Panasonic

- 13.1.12 NVIDIA

- 13.1.13 Qualcomm

- 13.1.14 onsemi

- 13.2 Regional players

- 13.2.1 HiRain

- 13.2.2 SemiDrive

- 13.2.3 Sonatus

- 13.2.4 ETAS

- 13.2.5 Elektrobit

- 13.2.6 Lear

- 13.2.7 Magna

- 13.2.8 Marelli

- 13.2.9 DENSO

- 13.3 Emerging players

- 13.3.1 TTTech

- 13.3.2 GuardKnox

- 13.3.3 Ambarella

- 13.3.4 Aurora Labs

- 13.3.5 Rivian

- 13.3.6 AUMOVIO

- 13.3.7 Molex

电子控制管理市场:2026-2032年全球市场预测(依产品类型、技术、安装类型、应用及最终用户产业划分)汽车电控系统市场:2026-2032年全球市场预测(依车辆类型、动力系统、自动驾驶等级、电子架构、应用与销售管道)硬体在环 (HIL) 模拟市场:按类型、组件、测试类型、应用和最终用户划分-2026-2032 年全球市场预测

电子控制管理市场:2026-2032年全球市场预测(依产品类型、技术、安装类型、应用及最终用户产业划分)汽车电控系统市场:2026-2032年全球市场预测(依车辆类型、动力系统、自动驾驶等级、电子架构、应用与销售管道)硬体在环 (HIL) 模拟市场:按类型、组件、测试类型、应用和最终用户划分-2026-2032 年全球市场预测 2026年全球汽车ECU市场报告2026年全球汽车智慧驾驶座系统晶片(SoC)市场报告汽车电子控制系统高度感测器市场:依产品类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球市场预测球栅阵列封装市场:依封装类型、基板材料、间距、I/O数量、互连结构及最终用途产业划分-2026年至2032年全球预测全球空气弹簧压缩机ECU市场(按车辆类型、ECU类型、应用和分销管道划分)预测(2026-2032年)

2026年全球汽车ECU市场报告2026年全球汽车智慧驾驶座系统晶片(SoC)市场报告汽车电子控制系统高度感测器市场:依产品类型、技术、车辆类型、应用和销售管道划分-2026-2032年全球市场预测球栅阵列封装市场:依封装类型、基板材料、间距、I/O数量、互连结构及最终用途产业划分-2026年至2032年全球预测全球空气弹簧压缩机ECU市场(按车辆类型、ECU类型、应用和分销管道划分)预测(2026-2032年) 汽车电控系统市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车电控系统市场机会、成长要素、产业趋势分析及2026年至2035年预测 全球汽车电控系统(ECU)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车电控系统(ECU)市场规模、份额、趋势和成长分析报告(2026-2034年)