|

市场调查报告书

商品编码

1959308

AI驱动的工业机器人市场机会、成长要素、产业趋势分析以及2026年至2035年的预测。AI-Powered Industrial Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

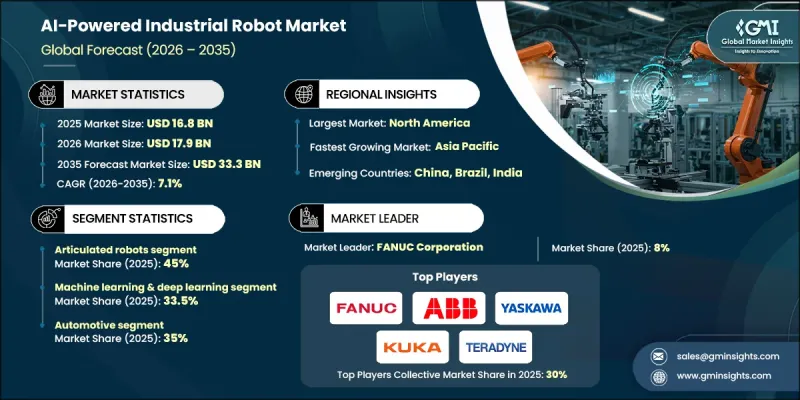

2025 年人工智慧驱动的工业机器人市场价值 168 亿美元,预计到 2035 年将达到 333 亿美元,年复合成长率为 7.1%。

这一成长主要得益于软体定义自动化技术的快速发展以及机器人系统中先进智慧的日益普及。製造商正从传统的固定式自动化转向能够即时学习和优化的自适应、以数据为中心的机器人平台。透过併购实现的市场整合正在加速技术进步,并增强全球部署能力。人工智慧驱动的机器人能够持续分析营运和环境数据,从而提高整个生产环境的效率、柔软性和回应能力。这一转变与全球向客製化、可变生产模式的转变密切相关。对智慧工厂计画的投资增加、已开发市场扩大回流以及多个地区自动化支出的成长,都有助于提高人工智慧驱动的工业机器人的商业性可行性,并增强其长期市场发展势头。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 168亿美元 |

| 预测金额 | 333亿美元 |

| 复合年增长率 | 7.1% |

预计到2025年,关节型机器人将占据45%的市场。该领域的需求主要源自于对高操作精度、多方向柔软性和智慧路径优化的要求。这些系统能够处理复杂的操作任务,同时保持稳定的效能和扩充性,因此持续吸引投资并巩固其强大的市场地位。

预计到2025年,机器学习和深度学习领域将占据33.5%的市场份额,并创造56亿美元的市场规模。随着製造商日益重视自主决策、持续改善和预测系统智能,该领域正引领相关技术的应用。先进的学习演算法使机器人能够适应不断变化的环境,随着时间的推移提高准确性,并支援数据驱动的营运策略。

预计到2025年,北美人工智慧驱动的工业机器人市场规模将达到53亿美元,并在2035年之前以7.3%的复合年增长率成长。美国占该地区市场收入的84%以上,这得益于其强大的製造业能力和旨在增强国内生产韧性的战略倡议。对先进人工智慧软体和自主系统智慧的需求持续推动着全部区域人工智慧技术的应用。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 青年和妇女的参与度提高

- 劳动力短缺和回流

- 生成式人工智慧与大规模语言模式(LLM)的融合

- IT/OT集成

- 产业潜在风险与挑战

- 高阶整合的复杂性

- 资料隐私和网路安全

- 机会

- 机器人即服务 (RaaS)

- 人类通用机器人

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按机器人类型

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估价与预测:依机器人类型划分,2022-2035年

- 关节机器人

- SCARA机器人

- Delta机器人

- 其他的

第六章 市场估计与预测:依技术划分,2022-2035年

- 机器学习和深度学习

- 电脑视觉成像

- 自然语言处理(NLP)

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 组装和物料输送

- 焊接和机械加工

- 包装和托盘堆垛

- 品质检测和视觉系统

- 物流/仓储管理

- 油漆和涂层

- 其他的

第八章 市场估算与预测:依最终使用者划分,2022-2035年

- 车

- 电子电器设备

- 食品/饮料

- 药品和医疗保健

- 消费品

- 物流/仓储业

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- ABB Ltd

- Agility Robotics, Inc.

- Boston Dynamics, Inc.

- FANUC Corporation

- Figure AI, Inc.

- Kawasaki Heavy Industries Ltd.

- Keyence Corporation

- KUKA SE & Co. KGaA

- NVIDIA Corporation

- Omron Corporation

- Standard Bots

- Symbiotic Inc.

- Teradyne, Inc.

- Tesla, Inc.

- Yaskawa Electric Corporation

The AI-Powered Industrial Robot Market was valued at USD 16.8 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 33.3 billion by 2035.

Growth is driven by rapid progress in software-defined automation and the increasing use of advanced intelligence within robotic systems. Manufacturers are shifting away from traditional fixed automation toward adaptive, data-centric robotic platforms capable of real-time learning and optimization. Market consolidation through mergers and acquisitions is accelerating technological advancement and strengthening global deployment capabilities. AI-enabled robots that continuously analyze operational and environmental data enable higher efficiency, flexibility, and responsiveness across production environments. This transition aligns closely with the global shift toward customized, variable-output manufacturing models. Rising investment in smart factory initiatives, growing reshoring efforts in developed markets, and increased automation spending across multiple regions are collectively improving the commercial viability of AI-powered industrial robotics and reinforcing long-term market momentum.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.8 Billion |

| Forecast Value | $33.3 Billion |

| CAGR | 7.1% |

The articulated robots segment held 45% share in 2025. Demand for this segment is supported by requirements for advanced motion precision, multi-directional flexibility, and intelligent path optimization. These systems continue to attract investment due to their ability to handle complex operational tasks while maintaining consistent performance and scalability, reinforcing their strong market position.

The machine learning and deep learning segment held a 33.5% share in 2025 and generated USD 5.6 billion. This segment leads adoption as manufacturers increasingly prioritize autonomous decision-making, continuous improvement, and predictive system intelligence. Advanced learning algorithms enable robots to adapt to changing conditions, improve accuracy over time, and support data-driven operational strategies.

North America AI-Powered Industrial Robot Market reached USD 5.3 billion in 2025 and will grow at a CAGR of 7.3% through 2035. The U.S. accounted for more than 84% of regional revenue, supported by strong manufacturing capabilities and strategic initiatives focused on domestic production resilience. Demand for advanced AI software and autonomous system intelligence continues to support widespread adoption across the region.

Key companies operating in the Global AI-Powered Industrial Robot Market include FANUC Corporation, ABB Ltd, KUKA SE & Co. KGaA, Yaskawa Electric Corporation, Kawasaki Heavy Industries Ltd., NVIDIA Corporation, Omron Corporation, Teradyne, Inc., Boston Dynamics, Inc., Tesla, Inc., Figure AI, Inc., Agility Robotics, Inc., Symbiotic Inc., Standard Bots, and Keyence Corporation. Companies in the AI-powered industrial robot market focus on technological leadership, ecosystem expansion, and strategic collaboration to strengthen their market position. Significant investment is directed toward AI software development, advanced sensing, and real-time analytics to enhance robot intelligence and adaptability. Partnerships and acquisitions are used to broaden capabilities and accelerate innovation cycles. Firms emphasize modular, scalable platforms to support diverse operational needs and faster deployment. Expansion into new geographic markets and localized support networks improves customer reach. Strong focus on reliability, system interoperability, and long-term service offerings helps build trust and sustain competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Robot Type

- 2.2.3 Price

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Participation Among Youth & Women

- 3.2.1.2 Labor shortages & reshoring

- 3.2.1.3 Generative AI & LLM Integration

- 3.2.1.4 IT/OT Convergence

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Integration Complexity

- 3.2.2.2 Data Privacy & Cybersecurity

- 3.2.3 Opportunities

- 3.2.3.1 Robot-as-a-Service (RaaS)

- 3.2.3.2 Humanoid General-Purpose Robots

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Robot type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Robot Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Articulated Robots

- 5.3 SCARA Robots

- 5.4 Delta Robots

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Machine Learning & Deep Learning

- 6.3 Computer Vision & Imaging

- 6.4 Natural Language Processing (NLP)

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Assembly & Material Handling

- 7.3 Welding & Machining

- 7.4 Packaging & Palletizing

- 7.5 Quality Inspection & Vision Systems

- 7.6 Logistics & Warehousing

- 7.7 Painting & Coating

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Electronics & Electrical

- 8.4 Food & Beverage

- 8.5 Pharmaceuticals & Healthcare

- 8.6 Consumer Goods

- 8.7 Logistics & Warehousing

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB Ltd

- 10.2 Agility Robotics, Inc.

- 10.3 Boston Dynamics, Inc.

- 10.4 FANUC Corporation

- 10.5 Figure AI, Inc.

- 10.6 Kawasaki Heavy Industries Ltd.

- 10.7 Keyence Corporation

- 10.8 KUKA SE & Co. KGaA

- 10.9 NVIDIA Corporation

- 10.10 Omron Corporation

- 10.11 Standard Bots

- 10.12 Symbiotic Inc.

- 10.13 Teradyne, Inc.

- 10.14 Tesla, Inc.

- 10.15 Yaskawa Electric Corporation

人工智慧驱动的工业机器人市场预测至2034年——全球产品、机器人类型、部署模式、技术、最终用户和区域分析

人工智慧驱动的工业机器人市场预测至2034年——全球产品、机器人类型、部署模式、技术、最终用户和区域分析 2026年全球表面目视检测市场报告

2026年全球表面目视检测市场报告 表面视觉与检测市场 - 全球产业规模、份额、趋势、机会及预测(按组件、应用、地区和竞争格局划分,2021-2031年)

表面视觉与检测市场 - 全球产业规模、份额、趋势、机会及预测(按组件、应用、地区和竞争格局划分,2021-2031年) 表面视觉与检测市场(按组件、技术、类型、应用、最终用途产业和部署模式)—全球预测 2025-20322032 年人工智慧工业视觉市场预测:按组件、部署模式、技术、应用、最终用户和地区进行的全球分析标籤检测机市场预测(至 2032 年):按产品类型、组件、机器类型、技术、应用、最终用户和地区进行的全球分析

表面视觉与检测市场(按组件、技术、类型、应用、最终用途产业和部署模式)—全球预测 2025-20322032 年人工智慧工业视觉市场预测:按组件、部署模式、技术、应用、最终用户和地区进行的全球分析标籤检测机市场预测(至 2032 年):按产品类型、组件、机器类型、技术、应用、最终用户和地区进行的全球分析 表面视觉与检测设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

表面视觉与检测设备:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 表面视觉检测市场:按组件、类型、应用和地区划分

表面视觉检测市场:按组件、类型、应用和地区划分 表面视觉和检测市场规模、份额、趋势分析报告:按组件、按表麵类型、按系统、按应用、按地区、细分市场预测,2024-2030 年

表面视觉和检测市场规模、份额、趋势分析报告:按组件、按表麵类型、按系统、按应用、按地区、细分市场预测,2024-2030 年