|

市场调查报告书

商品编码

1959316

生物基增塑剂市场机会、成长要素、产业趋势分析及2026年至2035年预测。Biobased Plasticizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

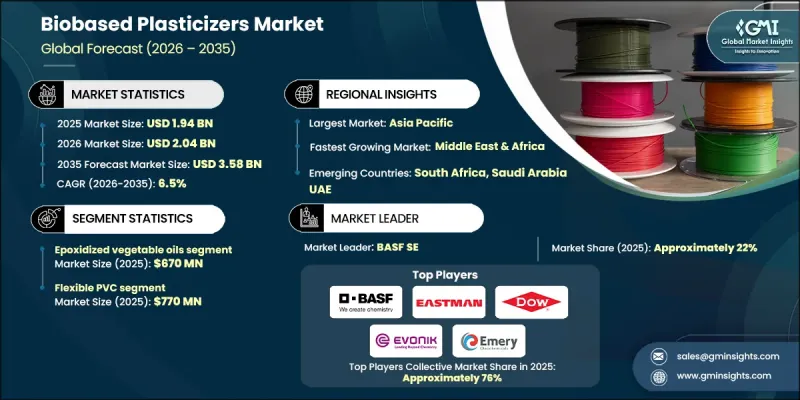

2025 年全球生物基增塑剂市场价值为 19.4 亿美元,预计到 2035 年将达到 35.8 亿美元,年复合成长率为 6.5%。

随着各产业加速向可再生和永续材料解决方案转型,市场正稳步发展。日益增强的环保意识以及对传统石油基增塑剂对生态系统影响的担忧,正推动着以可再生原材料生产的生物基替代品的过渡。这些材料与企业的永续性目标和循环经济框架高度契合,因此在製造业和消费品行业备受关注。随着企业优先考虑材料的长期安全性、合规性和环境责任,各价值链的需求都在不断增强。对绿色化学的持续投资、加工效率的提高以及可再生添加剂在工业应用中的广泛应用,都进一步支撑了市场前景。在已开发市场和新兴市场不断发展的材料标准和以永续性发展为导向的筹资策略的支持下,市场成长结构合理,并持续受到合规性的主导。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 19.4亿美元 |

| 预测金额 | 35.8亿美元 |

| 复合年增长率 | 6.5% |

监管压力在市场扩张中持续发挥重要作用。出于对健康和环境的担忧,世界各国政府和监管机构正在加强对传统塑化剂的监管。这项政策转变迫使製造商使用无毒的生物基替代品重新设计产品,而合规性直接促进了产品采用率的提高和长期稳定的市场需求。

预计到2025年,环氧化植物油市场规模将达到6.7亿美元,并在2026年至2035年间以6.2%的复合年增长率成长。产品层面的成长主要得益于性能要求与生物基配方之间日益增强的契合度。製造商正积极推广使用植物油基、柠檬酸基、蓖麻油基和琥珀酸基增塑剂,转向供应稳定、功能可靠的可再生原料,从而推动整个行业的需求成长。

预计到2025年,柔软性PVC市场销售额将达到7.7亿美元,市占率为39.7%,并将在2035年之前以6.3%的复合年增长率成长。该市场是生物基增塑剂最大的消费领域,其成长主要受永续性标准提高和监管要求不断变化的影响。随着製造商将符合监管要求且环保的增塑剂解决方案整合到柔软性材料生产中,应用主导需求持续成长。

预计到2025年,北美生物基增塑剂市场规模将达到3.5亿美元,并在整个预测期内保持稳定成长。区域需求主要由逐步但稳定的推广应用所驱动,并着重于各工业部门对永续性的整合。美国透过提高监管意识和对适应性强、柔软性的材料的需求,为市场成长做出了贡献;而墨西哥则透过扩大生产能力和发展出口导向产品,为市场成长提供了支持。该地区的市场发展以创新为主导,并与循环材料策略相契合,从而实现了谨慎且注重适应性的扩张。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 环氧植物油

- 环氧大豆油(ESBO/ESO)

- 环氧亚麻仁油

- 其他环氧化植物油

- 柠檬酸酯

- 柠檬酸三丁酯(TBC)

- 乙酰柠檬酸三丁酯 (ATBC)

- 其他柠檬酸酯

- 蓖麻油基增塑剂

- 琥珀酸酯类增塑剂

- 己二酸和癸二酸

- 甘油基增塑剂

- 甘油/丙三醇

- 醋酸甘油酯

- 聚合物基生物增塑剂

- 其他的

第六章 市场估算与预测:依等级划分,2022-2035年

- 食品级

- 医用级

- 工业级

- 技术级

- 其他的

第七章 市场估计与预测:依生物基含量划分,2022-2035年

- 100% 生物基

- 部分生物基(生物基含量超过50%)

- 部分生物基(生物基含量低于50%)

第八章 市场估计与预测:依应用领域划分,2022-2035年

- 柔性聚氯乙烯树脂

- 包装材料

- 食品/饮料包装

- 消费品包装

- 可堆肥和可生物降解的包装

- 电线电缆

- 地板材料、屋顶和墙壁材料

- 汽车/运输设备

- 内装和仪表板贴膜

- 引擎室部件

- 密封件和垫圈

- 油漆、黏合剂和密封剂

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Avient Corporation

- BASF SE

- Dow Chemical Company

- Eastman Chemical Company

- Emery Oleochemicals

- Evonik Industries AG

- Jungbunzlauer Suisse AG

- LANXESS AG

- Matrica SpA

- OXEA GmbH

- Valtris Specialty Chemicals

- Zhejiang Jiaao Enprotech

The Global Biobased Plasticizers Market was valued at USD 1.94 billion in 2025 and is estimated to grow at a CAGR of 6.5% to reach USD 3.58 billion by 2035.

The market is progressing steadily as industries increasingly transition toward renewable and sustainable material solutions. Rising environmental awareness and growing concern over the ecological impact of conventional petroleum-based plasticizers are accelerating the shift toward bio-derived alternatives produced from renewable feedstocks. These materials align closely with corporate sustainability targets and circular economy frameworks, making them attractive across manufacturing and consumer-facing industries. Demand is strengthening throughout multiple value chains as companies prioritize long-term material safety, regulatory compliance, and environmental responsibility. The market outlook is further supported by consistent investments in green chemistry, improved processing efficiency, and broader acceptance of renewable additives across industrial applications. Growth remains structured and compliance-driven, supported by evolving material standards and sustainability-focused procurement strategies across developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.94 Billion |

| Forecast Value | $3.58 Billion |

| CAGR | 6.5% |

Regulatory pressure continues to play a significant role in market expansion. Governments and oversight bodies across global regions are tightening restrictions on conventional plasticizers due to health and environmental concerns. These policy shifts are compelling manufacturers to reformulate products using non-toxic biobased alternatives, directly translating regulatory compliance into higher adoption levels and stable long-term demand.

The epoxidized vegetable oils segment reached USD 0.67 billion in 2025 and is projected to grow at a CAGR of 6.2% from 2026 to 2035. Product-level growth is driven by increasing alignment between performance requirements and biobased formulations. Manufacturers are advancing the use of vegetable oil-based, citrate-based, castor oil-derived, and succinic acid-derived plasticizers as part of a broader move toward renewable inputs with consistent availability and reliable functionality, strengthening demand across industrial segments.

The flexible PVC segment generated USD 0.77 billion in 2025 and held a share of 39.7%, with an anticipated CAGR of 6.3% through 2035. This segment represents the largest area of consumption for biobased plasticizers, supported by rising sustainability standards and evolving regulatory expectations. Application-driven demand continues to expand as manufacturers integrate compliant and environmentally aligned plasticizer solutions into flexible material production.

North America Biobased Plasticizers Market generated USD 0.35 billion in 2025 and is expected to experience steady growth over the forecast timeline. Regional demand is supported by gradual but consistent adoption across industrial sectors, emphasizing sustainability integration. The United States contributes through higher regulatory awareness and demand for compliant flexible materials, while Mexico supports growth through expanding manufacturing capacity and export-oriented production. Market development in the region remains innovation-led and aligned with circular material strategies, resulting in measured and compliance-focused expansion.

Key participants in the Global Biobased Plasticizers Market include Dow Chemical, BASF SE, Emery Oleochemicals, Evonik Industries, Eastman Chemical, and other established manufacturers. Companies operating in the biobased plasticizers market are reinforcing their competitive position through product innovation, capacity expansion, and strategic sourcing of renewable raw materials. Many players are investing in advanced formulation technologies to improve performance consistency while maintaining sustainability credentials. Long-term supply agreements and backward integration into bio-based feedstocks are helping stabilize input costs and ensure supply reliability. Firms are also strengthening partnerships with downstream manufacturers to co-develop application-specific solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Grade

- 2.2.4 Bio-Based Content

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxidized Vegetable Oils

- 5.2.1 Epoxidized Soybean Oil (ESBO/ESO)

- 5.2.2 Epoxidized Linseed Oil

- 5.2.3 Other Epoxidized Vegetable Oils

- 5.3 Citrate Esters

- 5.3.1 Tributyl Citrate (TBC)

- 5.3.2 Acetyl Tributyl Citrate (ATBC)

- 5.3.3 Other Citrate Esters

- 5.4 Castor Oil-Based Plasticizers

- 5.5 Succinic Acid-Based Plasticizers

- 5.6 Adipates & Sebacates

- 5.7 Glycerol-Based Plasticizers

- 5.7.1 Glycerin/Glycerol

- 5.7.2 Glycerin Acetate

- 5.8 Polymeric Bio-Based Plasticizers

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Grade, 2022 - 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Food Grade

- 6.3 Medical Grade

- 6.4 Industrial Grade

- 6.5 Technical Grade

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Bio-Based Content, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 100% Bio-Based

- 7.3 Partially Bio-Based (>50% Bio-Based Content)

- 7.4 Partially Bio-Based (<50% Bio-Based Content)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Flexible PVC

- 8.3 Packaging Materials

- 8.3.1 Food & Beverage Packaging

- 8.3.2 Consumer Goods Packaging

- 8.3.3 Compostable & Biodegradable Packaging

- 8.4 Wire & Cables

- 8.5 Flooring, Roofing & Wall Coverings

- 8.6 Automotive & Transportation

- 8.6.1 Interior Trim & Dashboard Films

- 8.6.2 Under-Hood Components

- 8.6.3 Seals & Gaskets

- 8.7 Coatings, Adhesives & Sealants

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Avient Corporation

- 10.2 BASF SE

- 10.3 Dow Chemical Company

- 10.4 Eastman Chemical Company

- 10.5 Emery Oleochemicals

- 10.6 Evonik Industries AG

- 10.7 Jungbunzlauer Suisse AG

- 10.8 LANXESS AG

- 10.9 Matrica S.p.A.

- 10.10 OXEA GmbH

- 10.11 Valtris Specialty Chemicals

- 10.12 Zhejiang Jiaao Enprotech

PLA塑胶市场按形态、等级、製造流程、应用和最终用途产业划分-2026-2032年全球预测有机甜菜根粉市场按类型、包装形式、消费者年龄层、应用和分销管道划分-全球预测(2026-2032 年)生物基大宗化学品市场(依化学品类型、原料生物质、生产製程及最终用途产业划分)-2026-2032年全球预测

PLA塑胶市场按形态、等级、製造流程、应用和最终用途产业划分-2026-2032年全球预测有机甜菜根粉市场按类型、包装形式、消费者年龄层、应用和分销管道划分-全球预测(2026-2032 年)生物基大宗化学品市场(依化学品类型、原料生物质、生产製程及最终用途产业划分)-2026-2032年全球预测 生物基平台化学品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)生物基平台化学品市场(按应用、最终用途产业、原料、产品类型和製程技术)-2025-2032 年全球预测

生物基平台化学品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)生物基平台化学品市场(按应用、最终用途产业、原料、产品类型和製程技术)-2025-2032 年全球预测 生物基平台化学品市场-全球产业规模、份额、趋势、机会和预测(按产品、地区和竞争细分,2020-2030 年)

生物基平台化学品市场-全球产业规模、份额、趋势、机会和预测(按产品、地区和竞争细分,2020-2030 年) 2025-2033年生物基平台化学品市场报告(依化学品、原料、最终用途产业及地区)

2025-2033年生物基平台化学品市场报告(依化学品、原料、最终用途产业及地区) 生物为基础平台用化学品的全球市场,规模,占有率,趋势,产业分析报告:各产品,各应用领域,各地区 - 市场预测,2025年~2034年

生物为基础平台用化学品的全球市场,规模,占有率,趋势,产业分析报告:各产品,各应用领域,各地区 - 市场预测,2025年~2034年 生物基平台化学品市场规模、份额和趋势分析报告:2025-2033 年产品、地区和细分市场预测

生物基平台化学品市场规模、份额和趋势分析报告:2025-2033 年产品、地区和细分市场预测 生物基平台化学品市场规模、份额及成长分析(按来源、类型、产品、最终用途和地区)-2025-2032 年产业预测

生物基平台化学品市场规模、份额及成长分析(按来源、类型、产品、最终用途和地区)-2025-2032 年产业预测