|

市场调查报告书

商品编码

1959329

电动重型卡车市场机会、成长要素、产业趋势分析及2026年至2035年预测Electric Heavy Duty Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球电动重型卡车市场价值 169.7 亿美元,预计到 2035 年将达到 1,529.5 亿美元,年复合成长率为 22.2%。

货运脱碳趋势日益增强,正在重塑车辆营运、车辆设计和部署策略。电动重型卡车(e-HDT)正成为永续物流的核心,尤其是在城市配送、港口营运和区域间运输领域。这些卡车有助于减少柴油排放、降低燃油价格波动,并减轻商业业者面临的监管压力。与轻型电动车不同,e-HDT 专为负载容量和长循环运作而设计,因此电池寿命、充电速度和全生命週期成本是其部署的关键因素。现代 e-HDT 采用专用设计,而非柴油车型的改装,配备高能量电池系统、扭矩优化电桥、先进的电力电子设备、温度控管解决方案和车辆控制软体。车队管理人员越来越倾向于根据路线适用性、负载容量和续航里程效率、基础设施可用性以及长期营运成本来评估车辆,而不是只专注于初始购买成本。公共和私人投资的加速成长正在推动全球物流和工业领域的大规模部署。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 169.7亿美元 |

| 预测金额 | 1529.5亿美元 |

| 复合年增长率 | 22.2% |

预计到2025年,7级卡车市占率将达到63%,并在2035年之前以21.8%的复合年增长率成长。 7级卡车的总吨位从26,001英镑到33,000英镑不等,是区域货运、都市区配送和高运转率商业运营的理想选择。可预测的路线、频繁的停靠以及与仓库枢纽充电系统的兼容性,使营运商能够优化电池使用,减少充电造成的停机时间,并有效控制营运成本。

预计到2025年,电池式电动车(BEV)市场份额将达到65.4%,并在2035年之前以22.6%的复合年增长率成长。纯电动汽车凭藉其零排放、卓越的能源效率以及对都市区和区域交通运营的适用性,引领市场。先进的电池技术、再生煞车和能量管理系统确保了性能稳定、维护成本低、使用寿命长,使纯电动车成为寻求永续且经济高效解决方案的车队营运商的理想选择。

预计到2025年,中国电动重型卡车市场将占显着份额。这一增长主要得益于政府强有力的政策支持、排放目标、都市化以及零排放车辆的强制推广。在地化的产能、高性价比的高容量电池以及扩充性的电动驱动系统正在加速物流、工业和区域运输领域的应用。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 加强政府对零排放商用车的监管

- 物流和工业车辆营运商对电动卡车的采用率迅速提高

- 柴油卡车的燃料成本波动和总营运费用不断增加

- 电池能量密度和充电技术的快速发展

- 产业潜在风险与挑战

- 车辆和基础设施部署的初始成本较高

- 长途货运充电设施短缺

- 市场机会

- 车队即服务和租赁模式的采用率不断提高

- 港口、矿业和工业运作中的快速电气化

- 增加兆瓦级和超快速充电解决方案的部署

- 数位车辆管理平台的整合正在迅速发展。

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国环保署(EPA)柴油排放减少法案(DERA)

- 美国能源局车辆技术局项目

- 美国环保署清洁轨道计划

- 加州先进清洁卡车法规(ACT)

- 欧洲

- 欧盟二氧化碳排放标准与清洁卡车指令

- 德国联邦零排放轨道计划

- 英国引进超低排放车辆(ULEV)车队的支援措施

- 法国对重型车辆脱碳的支持

- 亚太地区

- 中国:新能源公车(NEB)的推广与采购政策

- 日本:公共交通脱碳绿色成长策略

- 韩国:公共运输环保车辆蓝图

- 新加坡:绿色公共交通计画(GPTP)

- 拉丁美洲

- 巴西零排放卡车采购

- 墨西哥的清洁交通与车辆现代化政策

- 智利国家零排放轨道战略

- 中东和非洲

- 阿拉伯联合大公国(阿联酋)永续交通政策

- 沙乌地阿拉伯「2030愿景」:货运电气化

- 南非绿色货运策略

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 未来前景与机会

- 成本細項分析

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 舰队过渡和部署模型

- 充电基础设施和电网相容性评估

- 电池劣化、保固和二次利用经济学

- 未来前景与机会

第四章 竞争情势

- 介绍

- 企业市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依车辆类型划分,2022-2035年

- 七年级

- 八年级

第六章 市场估计与预测:依驱动因素划分,2022-2035年

- 电池式电动车(BEV)

- 混合动力电动车(HEV)

- 插电式混合动力车(PHEV)

第七章 市场估计与预测:依范围划分,2022-2035年

- 短期预测

- 中距离

- 长期预测

第八章 市场估算与预测:依电池容量划分,2022-2035年

- 小于300度

- 300-500千瓦时

- 500度或以上

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 物流/配送

- 建造

- 废弃物管理

- 其他的

第十章 市场估计与预测:以毛重计算,2022-2035年

- 不到6吨

- 6-14吨

- 超过14吨

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- BYD

- Daimler Truck

- Ford

- GM

- Komatsu

- Nikola

- PACCAR

- Tesla

- Traton

- Volvo

- 本地球员

- Designwerk

- E-Force One

- Orange EV

- Terberg

- Xos

- 新兴企业

- Bollinger Motors

- Edison Motors

- Hyliion

- Lion Electric

- Mitsubishi

- Renault Trucks

- Rivian

- Rizon

- SEA Electric

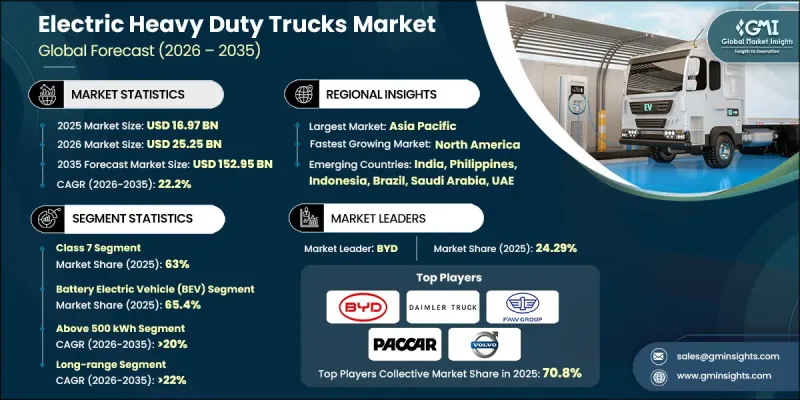

The Global Electric Heavy Duty Trucks Market was valued at USD 16.97 billion in 2025 and is estimated to grow at a CAGR of 22.2% to reach USD 152.95 billion by 2035.

The increasing drive toward decarbonizing freight transportation is reshaping fleet operations, vehicle design, and deployment strategies. Electric heavy-duty trucks (e-HDTs) are becoming central to sustainable logistics, particularly for urban distribution, port operations, and regional haul applications. These trucks mitigate diesel emissions, fuel price volatility, and regulatory pressures on commercial operators. Unlike lighter EVs, e-HDTs are designed for heavy payloads and long duty cycles, making battery longevity, charging speed, and total lifecycle cost crucial for adoption. Modern e-HDTs are purpose-built rather than conversions from diesel models, featuring high-energy battery systems, torque-optimized electric axles, advanced power electronics, thermal management solutions, and vehicle control software. Fleet managers increasingly assess vehicles based on route compatibility, payload-range efficiency, infrastructure readiness, and long-term operating expenses rather than upfront purchase cost. Accelerated public and private investment is supporting large-scale deployment across logistics and industrial sectors worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.97 Billion |

| Forecast Value | $152.95 Billion |

| CAGR | 22.2% |

The Class 7 segment held 63% share in 2025 and is expected to grow at a CAGR of 21.8% through 2035. Class 7 trucks, with gross vehicle weight ratings of 26,001 to 33,000 pounds, are well-suited for regional freight, urban delivery, and high-utilization commercial operations. Their predictable routes, frequent stops, and compatibility with depot- and hub-based charging allow operators to optimize battery use, reduce charging downtime, and manage operational costs efficiently.

The battery electric vehicle (BEV) segment accounted for 65.4% share in 2025 and is projected to grow at a CAGR of 22.6% through 2035. BEVs dominate due to zero tailpipe emissions, superior energy efficiency, and suitability for both urban and regional haul operations. Advanced battery technologies, regenerative braking, and energy management systems ensure consistent performance, low maintenance, and long service life, making BEVs the preferred choice for fleet operators pursuing sustainable and cost-effective solutions.

China Electric Heavy Duty Trucks Market held a significant share in 2025. Expansion is driven by strong government policies, emission reduction targets, urbanization, and zero-emission fleet mandates. Local manufacturing capabilities, cost-efficient high-capacity batteries, and scalable electric drivetrains accelerate adoption across logistics, industrial, and regional applications.

Key players in the Global Electric Heavy Duty Trucks Market include BYD, Daimler Truck, Ford, GM, Komatsu, Nikola, PACCAR, Tesla, Traton, and Volvo. Companies in the Electric Heavy Duty Trucks Market are strengthening their presence by developing purpose-built platforms optimized for high payloads, long routes, and depot charging networks. Strategic partnerships with battery manufacturers, fleet operators, and infrastructure providers enable faster scaling and enhanced charging coverage. Investment in R&D focuses on improving energy density, thermal management, power electronics, and regenerative braking systems. Manufacturers are adopting modular vehicle architectures, expanding global production facilities, and leveraging government incentives for clean transportation. They are also deploying pilot fleets and digital fleet management tools to demonstrate performance, reduce operational risk, and accelerate customer adoption.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle Class

- 2.2.3 Propulsion

- 2.2.4 Range

- 2.2.5 Battery Capacity

- 2.2.6 Application

- 2.2.7 GVWR

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in government mandates for zero-emission commercial vehicles

- 3.2.1.2 Surge in adoption of electric trucks by logistics and industrial fleet operators

- 3.2.1.3 Rise in fuel cost volatility and total operating expenses of diesel trucks

- 3.2.1.4 Surge in advancements in battery energy density and charging technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost associated with vehicle and infrastructure deployment

- 3.2.2.2 Limited charging availability for long-haul freight operations

- 3.2.3 Market opportunities

- 3.2.3.1 Increase in adoption of fleet-as-a-service and leasing models

- 3.2.3.2 Surge in electrification of ports, mining, and industrial operations

- 3.2.3.3 Rise in deployment of megawatt and ultra-fast charging solutions

- 3.2.3.4 Surge in integration of digital fleet management platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. EPA Diesel Emissions Reduction Act (DERA)

- 3.4.1.2 U.S. DOE Vehicle Technologies Office Programs

- 3.4.1.3 EPA Clean Truck Program

- 3.4.1.4 California Advanced Clean Trucks (ACT) Regulation.

- 3.4.2 Europe

- 3.4.2.1 EU CO2 Emission Standards & Clean Truck Directive

- 3.4.2.2 Germany Federal Zero-Emission Truck Program

- 3.4.2.3 United Kingdom ULEV Fleet Incentives

- 3.4.2.4 France Heavy Vehicle Decarbonization Support

- 3.4.3 Asia Pacific

- 3.4.3.1 China: New Energy Bus (NEB) Promotion & Procurement Policies

- 3.4.3.2 Japan: Green Growth Strategy for Decarbonized Public Transport

- 3.4.3.3 South Korea: Eco-Friendly Vehicle Roadmap for Public Transport

- 3.4.3.4 Singapore: Green Public Transport Programme (GPTP)

- 3.4.4 Latin America

- 3.4.4.1 Brazil Zero-Emission Truck Procurement

- 3.4.4.2 Mexico Clean Transport & Fleet Modernization Policies

- 3.4.4.3 Chile National Zero-Emission Truck Strategy

- 3.4.5 MEA

- 3.4.5.1 UAE Sustainable Transport Policy

- 3.4.5.2 Saudi Arabia Vision 2030 Freight Electrification

- 3.4.5.3 South Africa Green Freight Strategy

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Future outlook & opportunities

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Fleet Transition & Deployment Models

- 3.14 Charging Infrastructure & Grid Readiness Assessment

- 3.15 Battery Degradation, Warranty & Second-Life Economics

- 3.16 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Class 7

- 5.3 Class 8

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicle (BEV)

- 6.3 Hybrid Electric Vehicle (HEV)

- 6.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 7 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Short Range

- 7.3 Medium Range

- 7.4 Long Range

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Below 300 kWh

- 8.3 300-500 kWh

- 8.4 Above 500 kWh

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Logistics & Delivery

- 9.3 Construction

- 9.4 Waste Management

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By GVWR, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 Below 6 tons

- 10.3 6 - 14 tons

- 10.4 Above 14 tons

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Belgium

- 11.3.8 Netherlands

- 11.3.9 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Indonesia

- 11.4.8 Singapore

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 BYD

- 12.1.2 Daimler Truck

- 12.1.3 Ford

- 12.1.4 GM

- 12.1.5 Komatsu

- 12.1.6 Nikola

- 12.1.7 PACCAR

- 12.1.8 Tesla

- 12.1.9 Traton

- 12.1.10 Volvo

- 12.2 Regional Players

- 12.2.1 Designwerk

- 12.2.2 E-Force One

- 12.2.3 Orange EV

- 12.2.4 Terberg

- 12.2.5 Xos

- 12.3 Emerging Players

- 12.3.1 Bollinger Motors

- 12.3.2 Edison Motors

- 12.3.3 Hyliion

- 12.3.4 Lion Electric

- 12.3.5 Mitsubishi

- 12.3.6 Renault Trucks

- 12.3.7 Rivian

- 12.3.8 Rizon

- 12.3.9 SEA Electric

卡车起重机底盘市场:按类型、负载能力、操作模式、应用和最终用户产业划分-2026-2032年全球预测

卡车起重机底盘市场:按类型、负载能力、操作模式、应用和最终用户产业划分-2026-2032年全球预测 电动卡车市场规模、份额、趋势和预测:按车辆类型、功率、续航里程、应用和地区划分,2026-2034年

电动卡车市场规模、份额、趋势和预测:按车辆类型、功率、续航里程、应用和地区划分,2026-2034年 全球电动卡车底盘市场规模、份额、趋势和成长分析报告(2026-2034)全球电动堆高机市场规模、份额、趋势和成长分析报告(2026-2034)全球货车市场规模、份额、趋势和成长分析报告(2026-2034年)

全球电动卡车底盘市场规模、份额、趋势和成长分析报告(2026-2034)全球电动堆高机市场规模、份额、趋势和成长分析报告(2026-2034)全球货车市场规模、份额、趋势和成长分析报告(2026-2034年) 电动卡车市场 - 全球产业规模、份额、趋势、机会及预测(按动力类型、类型、最终用户、地区和竞争格局划分,2021-2031年)纯电动卡车底盘市场(按车辆等级、车架材料、驾驶室类型、应用和最终用户产业划分)-全球预测(2026-2032年)纯电动压缩式垃圾车市场(按车辆类型、载重能力、驱动轴、充电方式、应用和最终用户划分),全球预测,2026-2032年货车底盘市场(按底盘类型、车轴配置、材料、动力系统、车辆类型和最终用途划分),全球预测,2026-2032年

电动卡车市场 - 全球产业规模、份额、趋势、机会及预测(按动力类型、类型、最终用户、地区和竞争格局划分,2021-2031年)纯电动卡车底盘市场(按车辆等级、车架材料、驾驶室类型、应用和最终用户产业划分)-全球预测(2026-2032年)纯电动压缩式垃圾车市场(按车辆类型、载重能力、驱动轴、充电方式、应用和最终用户划分),全球预测,2026-2032年货车底盘市场(按底盘类型、车轴配置、材料、动力系统、车辆类型和最终用途划分),全球预测,2026-2032年 欧洲电动卡车市场-份额分析、产业趋势与统计、成长预测(2026-2031)

欧洲电动卡车市场-份额分析、产业趋势与统计、成长预测(2026-2031)