|

市场调查报告书

商品编码

1959557

电子安防市场机会、成长要素、产业趋势分析及2026年至2035年预测Electronic Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

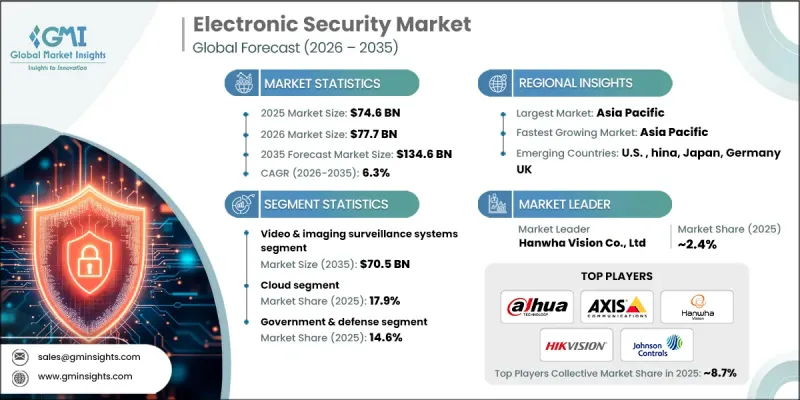

2025 年全球电子安防市场价值为 746 亿美元,预计到 2035 年将达到 1,346 亿美元,年复合成长率为 6.3%。

全球安全情势日益严峻、技术持续创新以及跨行业监管要求日益严格,共同推动了市场扩张。智慧城市计画的不断普及,以及人们对家庭和企业远端监控功能的日益关注,进一步刺激了市场需求。硬体成本的降低和云端平台的兴起,使得企业能够开发扩充性的整合式安防系统,以满足不断变化的需求。电子安防涵盖了旨在保护人员、财产和资产的解决方案,这些方案利用视讯监控、门禁控制、入侵检测系统、生物识别和高级监控软体等设备。人工智慧和机器学习的融合是关键趋势,使系统能够侦测异常情况、预测威胁并自动回应。这些进步正促使企业、政府和住宅用户越来越多地利用智慧互联的安防解决方案,以提高安全性和营运效率。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 746亿美元 |

| 预测金额 | 1346亿美元 |

| 复合年增长率 | 6.3% |

预计到2025年,门禁系统市场规模将达到188亿美元,并在2035年之前维持7.1%的复合年增长率。该行业正朝着生物识别和非接触式解决方案转型,例如指纹识别、脸部认证辨识和虹膜辨识,从而提升安全性并增强用户便利性。行动认证日益普及,用户可以透过智慧型手机进行远端存取。同时,物联网和云端集成为商业设施、医疗机构和关键基础设施提供了集中管理、即时监控和警报功能。

预计到2025年,云端安全解决方案的市占率将达到17.9%,显示基于云端的安全平台正被迅速采用。这些系统具有扩充性、远端系统管理,并降低了硬体需求,使企业能够安全地储存视讯资料、利用人工智慧分析,并透过单一介面监控多个位置。与行动和物联网技术的进一步整合增强了柔软性,使云端平台成为企业、智慧城市和住宅用户的理想选择。

预计到2025年,北美电子安防市占率将达到26.9%。该地区的成长主要得益于住宅、商业和公共部门的广泛应用,尤其是与云端平台、人工智慧分析和先进存取管理技术的整合。公共倡议充分利用监控和自动化监控,而个人用户也越来越多地采用具备远端存取和即时警报功能的连网安防系统。政府计画也持续加强基础设施建设,作为更广泛的安全和犯罪预防策略的一部分。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 犯罪率上升,公共安全问题令人担忧

- 行动应用与DIY智慧家庭安防的融合。

- 对远端监控和云端安全的需求

- 商业和工业设施的扩建

- 无线和行动技术的不断进步

- 产业潜在风险与挑战

- 较高的初始实施和整合成本

- 对资料隐私和监控法规的担忧

- 市场机会

- 老旧公共基础设施的安全现代化

- 医疗机构电子安防的扩展

- 促进因素

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估计与预测:依系统类型划分,2022-2035年

- 影像监控系统

- 门禁系统

- 入侵侦测和周界安全系统

- 整合生命安全系统

- 其他的

第六章 市场估算与预测:依部署模式划分,2022-2035年

- 现场

- 基于云端的

- 杂交种

第七章 市场估计与预测:依最终用户产业划分,2022-2035年

- 政府/国防

- 适用于商业和企业用途

- 零售与消费空间

- 饭店和娱乐

- 工业和製造业

- 住宅住宅相关

- 卫生保健

- 教育

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Axis Communications AB

- Hanwha Vision Co., Ltd.

- Bosch Security Systems

- Honeywell International Inc.

- Johnson Controls International

- Motorola Solutions, Inc.

- ASSA ABLOY

- Allegion plc

- Dormakaba Holding AG

- Siemens

- HID Global

- Avigilon

- FLIR Systems

- Genetec Inc.

- Panasonic

- Hanwha

The Global Electronic Security Market was valued at USD 74.6 billion in 2025 and is estimated to grow at a CAGR of 6.3% to reach USD 134.6 billion by 2035.

The market expansion is driven by increasing global security concerns, continuous technological innovation, and stricter regulatory requirements across industries. Growing adoption of smart city initiatives, coupled with rising awareness of remote monitoring capabilities for homes and businesses, is further fueling demand. The declining cost of hardware, alongside the emergence of cloud-based platforms, enables companies to develop scalable, integrated security systems to meet evolving needs. Electronic security encompasses solutions designed to protect people, property, and assets using devices such as video surveillance, access control, intrusion detection systems, biometrics, and advanced monitoring software. Integration of AI and machine learning is a key trend, allowing systems to detect anomalies, predict threats, and respond automatically. With these advancements, businesses, governments, and residential users are increasingly leveraging intelligent and connected security solutions to enhance safety and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $74.6 Billion |

| Forecast Value | $134.6 Billion |

| CAGR | 6.3% |

The access control systems segment reached USD 18.8 billion in 2025 and is expected to grow at a CAGR of 7.1% through 2035. The segment is shifting toward biometric and contactless solutions, including fingerprint, facial, and iris recognition, improving security and user convenience. Mobile credentialing is gaining traction, allowing remote access through smartphones, while IoT and cloud integration provide centralized control, real-time monitoring, and alerts across commercial, healthcare, and critical infrastructure facilities.

The cloud segment accounted for 17.9% share in 2025, reflecting strong adoption of cloud-based security platforms. These systems offer scalability, remote management, and reduced hardware requirements, enabling organizations to securely store video data, utilize AI analytics, and monitor multiple locations from a single interface. Mobile and IoT integration further enhances flexibility, making cloud platforms attractive for businesses, smart cities, and residential users.

North America Electronic Security Market captured 26.9% share in 2025. Growth in the region is fueled by widespread deployment across residential, commercial, and public sectors, including integration with cloud platforms, AI analytics, and advanced access management technologies. Public safety initiatives leverage surveillance and automated monitoring, while private users increasingly adopt connected security systems with remote access and real-time alerts. Government programs continue to strengthen infrastructure as part of broader safety and crime prevention strategies.

Leading players in the Global Electronic Security Market include Axis Communications, Allegion, Dahua Technology, Honeywell Security, Johnson Controls Security, Milestone Systems, ASSA ABLOY, Bosch Security Product Biz, Hikvision Digital Technology Co., Ltd., Resideo Security, Siemens SI Security, Secom, Hanwha Vision, TKH Group, and Motorola Solutions Video & Access. Companies in the electronic security market are strengthening their position through investment in AI-driven analytics, IoT integration, and cloud-based monitoring platforms. Many are expanding product portfolios to include biometric and mobile access solutions to meet rising demand for secure, contactless access. Strategic partnerships with smart city initiatives, government agencies, and commercial enterprises enable early adoption and long-term contracts. Emphasis on cybersecurity, product reliability, and real-time monitoring capabilities enhances customer trust.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Deployment model trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising crime and public safety concerns

- 3.2.1.2 Convergence of mobile applications and DIY smart home security

- 3.2.1.3 Demand for remote monitoring and cloud security

- 3.2.1.4 Expansion of commercial and industrial facilities

- 3.2.1.5 Growing advancement in wireless and mobile technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial installation and integration costs

- 3.2.2.2 Data privacy and surveillance regulation concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Security modernization in aging public infrastructure

- 3.2.3.2 Expansion of electronic security in healthcare facilities

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By System Type, 2022 - 2035 (USD Mn)

- 5.1 Key trends

- 5.2 Video & Imaging Surveillance Systems

- 5.3 Access Control Systems

- 5.4 Intrusion & Perimeter Detection Systems

- 5.5 Life-Safety Integration Systems

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Deployment Model, 2022 - 2035 (USD Mn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-Based

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Mn)

- 7.1 Key trends

- 7.2 Government & Defense

- 7.3 Commercial & Corporate

- 7.4 Retail & Consumer Spaces

- 7.5 Hospitality & Entertainment

- 7.6 Industrial & Manufacturing

- 7.7 Residential & Housing

- 7.8 Healthcare

- 7.9 Education

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Hikvision Digital Technology Co., Ltd.

- 9.2 Dahua Technology Co., Ltd.

- 9.3 Axis Communications AB

- 9.4 Hanwha Vision Co., Ltd.

- 9.5 Bosch Security Systems

- 9.6 Honeywell International Inc.

- 9.7 Johnson Controls International

- 9.8 Motorola Solutions, Inc.

- 9.9 ASSA ABLOY

- 9.10 Allegion plc

- 9.11 Dormakaba Holding AG

- 9.12 Siemens

- 9.13 HID Global

- 9.14 Avigilon

- 9.15 FLIR Systems

- 9.16 Genetec Inc.

- 9.17 Panasonic

- 9.18 Hanwha

电子安防系统市场:依系统类型、技术、服务类型及最终用户划分-2026-2032年全球市场预测

电子安防系统市场:依系统类型、技术、服务类型及最终用户划分-2026-2032年全球市场预测 2026年东西方威胁侦测设备全球市场报告

2026年东西方威胁侦测设备全球市场报告 威胁侦测设备市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终使用者、功能及安装类型划分

威胁侦测设备市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终使用者、功能及安装类型划分 威胁侦测设备市场机会、成长要素、产业趋势分析及2026年至2035年预测。监狱邮件侦测与安全系统市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终使用者、功能及安装类型划分2026年全球携带式工作站市场报告2026年全球安防机器人指挥显示市场报告2026年全球电子安防市场报告

威胁侦测设备市场机会、成长要素、产业趋势分析及2026年至2035年预测。监狱邮件侦测与安全系统市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终使用者、功能及安装类型划分2026年全球携带式工作站市场报告2026年全球安防机器人指挥显示市场报告2026年全球电子安防市场报告 电子安防市场-全球产业规模、份额、趋势、机会及预测(依产品类型、终端用户产业、地区及竞争格局划分,2020-2030 年预测)

电子安防市场-全球产业规模、份额、趋势、机会及预测(依产品类型、终端用户产业、地区及竞争格局划分,2020-2030 年预测) 电子安全系统市场:2025-2030 年预测

电子安全系统市场:2025-2030 年预测