|

市场调查报告书

商品编码

1959563

宠物穿戴装置市场:机会、成长要素、产业趋势分析及2026年至2035年预测Pet Wearables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

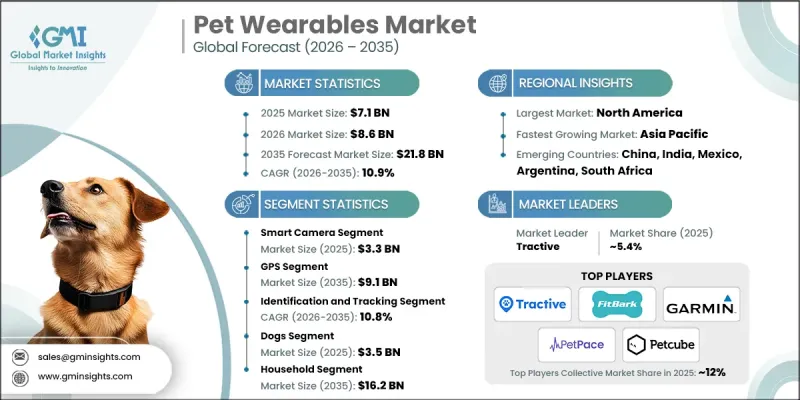

2025 年全球宠物穿戴装置市场价值为 71 亿美元,预计到 2035 年将以 10.9% 的复合年增长率成长至 218 亿美元。

推动市场成长的主要因素包括全球宠物数量的快速成长、家庭收入的提高、宠物健康和保健支出的增加,以及配备先进技术的宠物产品的普及。全球宠物数量超过10亿隻,光在美国、欧洲、巴西和中国等地区,每个家庭就拥有约5亿隻猫狗,为穿戴式装置的普及提供了巨大的潜力。宠物拟人化的趋势也正在推动市场成长,随着饲主越来越将宠物视为家庭成员,家庭在智慧宠物设备上的支出也不断增加。宠物穿戴装置包括GPS项圈、健康监测感测器、射频定位标籤和活动追踪器。这些设备利用GPS、蓝牙、RFID和智慧感测器等技术,提供宠物位置、活动量和生物健康参数的即时资讯。这些设备支援地理围栏、远端监控、行为追踪和健康问题早期检测,显示宠物护理解决方案正朝着更互联和智慧化的方向发展。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 71亿美元 |

| 预测金额 | 218亿美元 |

| 复合年增长率 | 10.9% |

预计到2025年,智慧摄影机市场规模将达到33亿美元。由于人们对远端监控和即时互动的需求日益增长,智慧摄影机的普及率正在不断提高,使饲主即使不在家也能与宠物保持联繫。先进的感测器、物联网连接、视讯串流和Wi-Fi相容性,能够对宠物的活动、安全和行为进行详细监控。人们越来越需要利用科技来确保宠物在饲主不在家时的健康,这推动了该市场的成长,尤其是在家庭安防和宠物监控应用领域。

预计到2025年,犬类市场规模将达35亿美元。由于犬类活动范围广、户外活动频繁,以及对追踪、安全和健康监测的强烈需求,犬类市场占据了最大的市场份额。 GPS项圈、活动追踪器和健康监测穿戴式装置正成为保障犬种(尤其是活跃犬种和工作犬)安全和健康不可或缺的工具。全球犬隻数量的不断增长直接带动了对犬类专用穿戴装置的需求,从而推动了各地区该细分市场的成长。

预计到2035年,北美宠物穿戴装置市场规模将从2025年的39亿美元成长至117亿美元,复合年增长率(CAGR)为10.6%。该地区拥有诸多优势,例如宠物拥有率高、可支配收入高以及能够便捷地获取先进的可穿戴产品。北美宠物饲主对智慧宠物解决方案的认知度很高,加上产品种类繁多、零售生态系统完善,这些因素共同推动了此类产品的普及。主要市场参与者的存在也增强了区域成长,并确保了产品的持续创新和供应。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 宠物饲养量的增加和宠物拟人化

- 人们越来越关注宠物健康和福祉

- 物联网和人工智慧设备的技术进步

- 支持性的数位化环境和法规环境

- 产业潜在风险与挑战

- 技术限制和性能差距

- 先进穿戴装置价格高昂

- 市场机会

- 人工智慧驱动的宠物行为分析和训练解决方案

- 互联兽医生态系的发展

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 科技与创新趋势

- 目前技术

- 新兴技术

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 公司矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 市场估价与预测:依产品划分,2022-2035年

- 智能色彩

- 智慧背心

- 智慧线束

- 智慧型相机

- 其他产品

第六章 市场估计与预测:依技术划分,2022-2035年

- 射频识别设备

- GPS

- 感应器

- Bluetooth

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 医疗诊断和治疗

- 识别和追踪

- 健身监测

- 行为的监控与控制

第八章 市场估算与预测:依动物种类划分,2022-2035年

- 狗

- 猫

- 其他动物

第九章 市场估计与预测:依最终用途划分,2022-2035年

- 家用

- 商业的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- Buddy(Ninja Management)

- Dogtra

- Fi Smart Dog Collar

- Fitbark

- Garmin

- Halo Collar

- KYON

- Loc8tor

- Link My Pet

- Petcube

- Petpace

- PitPat

- SportDOG

- Tractive

- Wagz

The Global Pet Wearables Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 10.9% to reach USD 21.8 billion by 2035.

The market growth is driven by the rapid rise in the global pet population, increasing household incomes, higher spending on pet health and wellness, and the availability of advanced technology-enabled products for pets. With more than one billion pets worldwide, households across regions, including the U.S., Europe, Brazil, and China account for nearly half a billion dogs and cats, reflecting strong potential for wearables adoption. The ongoing trend of pet humanization is also driving growth, as owners increasingly treat pets as integral family members, boosting per-household expenditure on connected pet devices. Pet wearables encompass GPS collars, health monitoring sensors, RF-based locating tags, and activity trackers, which leverage technologies such as GPS, Bluetooth, RFID, and smart sensors to provide real-time insights into location, activity, and biometric health parameters. These devices support geofencing, remote monitoring, behavior tracking, and early detection of health issues, demonstrating a clear shift toward more connected, intelligent pet care solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.1 Billion |

| Forecast Value | $21.8 Billion |

| CAGR | 10.9% |

The smart camera segment reached USD 3.3 billion in 2025. Adoption is rising due to the demand for remote monitoring and real-time interaction, enabling owners to engage with pets even while away. Advanced sensors, IoT connectivity, video streaming, and Wi-Fi compatibility allow detailed monitoring of pet activity, safety, and behavior. The segment benefits from expanding use cases in home security and pet supervision, as owners increasingly seek technology that ensures their pets' well-being in unsupervised environments.

The dogs segment generated USD 3.5 billion in 2025. Dogs represent the largest share due to their higher mobility, frequent outdoor activity, and need for tracking, safety, and health monitoring. GPS-enabled collars, activity trackers, and health monitoring wearables are increasingly essential for ensuring the safety and fitness of dogs, particularly for active or working breeds. The rising global dog population directly correlates with the demand for dog-specific wearable devices, driving segmental growth across regions.

North America Pet Wearables Market was valued at USD 3.9 billion in 2025 and is projected to reach USD 11.7 billion by 2035, growing at a CAGR of 10.6%. The region benefits from high pet ownership, high disposable income, and access to advanced wearable products. Pet owners in North America are highly aware of smart pet solutions, which drives adoption, alongside the availability of multiple device options and a robust retail ecosystem. The presence of leading market players also strengthens regional growth, ensuring continuous innovation and product availability.

Key players in the Global Pet Wearables Market include Buddy (Ninja Management), Dogtra, Fi Smart Dog Collar, Fitbark, Garmin, Halo Collar, KYON, Loc8tor, Link My Pet, Petcube, Petpace, PitPat, SportDOG, Tractive, and Wagz. Companies operating in the pet wearables market are deploying several strategies to strengthen their market position and increase their global presence. These include investing heavily in research and development to enhance device accuracy, battery life, and sensor capabilities. Firms are also expanding their product portfolios with multifunctional devices that combine health tracking, GPS, and activity monitoring. Strategic collaborations with veterinary networks, pet care service providers, and technology integrators help secure brand trust and improve market penetration. Geographic expansion into emerging regions and targeted marketing campaigns enhance adoption rates, while subscription-based models for health monitoring and activity data generate recurring revenue streams.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Technology trends

- 2.2.4 Application trends

- 2.2.5 Animal type trends

- 2.2.6 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet ownership and humanization of pets

- 3.2.1.2 Growing awareness of pet health and wellness

- 3.2.1.3 Technological advancements in IoT- and AI-powered devices

- 3.2.1.4 Supportive digital and regulatory environment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Technical limitations and performance gaps

- 3.2.2.2 Premium pricing of advanced wearables

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven pet behavior and training solutions

- 3.2.3.2 Growth of connected veterinary ecosystems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Smart collar

- 5.3 Smart vest

- 5.4 Smart harness

- 5.5 Smart camera

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 RFID devices

- 6.3 GPS

- 6.4 Sensors

- 6.5 Bluetooth

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Medical diagnosis and treatment

- 7.3 Identification and tracking

- 7.4 Fitness monitoring

- 7.5 Behavior monitoring and control

Chapter 8 Market Estimates and Forecast, By Animal Type, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Other animals

Chapter 9 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 9.1 Key trends

- 9.2 Household

- 9.3 Commercial

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Buddy (Ninja Management)

- 11.2 Dogtra

- 11.3 Fi Smart Dog Collar

- 11.4 Fitbark

- 11.5 Garmin

- 11.6 Halo Collar

- 11.7 KYON

- 11.8 Loc8tor

- 11.9 Link My Pet

- 11.10 Petcube

- 11.11 Petpace

- 11.12 PitPat

- 11.13 SportDOG

- 11.14 Tractive

- 11.15 Wagz

宠物穿戴式装置市场规模、份额、趋势和预测:按产品、技术、应用、最终用户、分销管道和地区划分,2026-2034年

宠物穿戴式装置市场规模、份额、趋势和预测:按产品、技术、应用、最终用户、分销管道和地区划分,2026-2034年 全球宠物穿戴装置市场规模、份额、趋势和成长分析报告(2026-2034年)

全球宠物穿戴装置市场规模、份额、趋势和成长分析报告(2026-2034年) 宠物穿戴式装置市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、技术、最终用途、地区及竞争格局划分,2021-2031年)日本宠物穿戴装置市场报告(按产品、技术、应用、最终用户、配销通路和地区划分,2026-2034年)

宠物穿戴式装置市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、技术、最终用途、地区及竞争格局划分,2021-2031年)日本宠物穿戴装置市场报告(按产品、技术、应用、最终用户、配销通路和地区划分,2026-2034年) 宠物穿戴式装置市场规模、份额及成长分析(按技术、应用和地区划分)-2026-2033年产业预测

宠物穿戴式装置市场规模、份额及成长分析(按技术、应用和地区划分)-2026-2033年产业预测 宠物用穿戴式的全球市场:市场规模·占有率·趋势,产业分析 (各产品·各技术·动物类别·各用途·各地区),未来预测 (2025年~2034年)

宠物用穿戴式的全球市场:市场规模·占有率·趋势,产业分析 (各产品·各技术·动物类别·各用途·各地区),未来预测 (2025年~2034年) 2024-2028年全球宠物穿戴装置市场

2024-2028年全球宠物穿戴装置市场