|

市场调查报告书

商品编码

1959564

汽车照明市场机会、成长要素、产业趋势分析及2026年至2035年预测Automotive Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

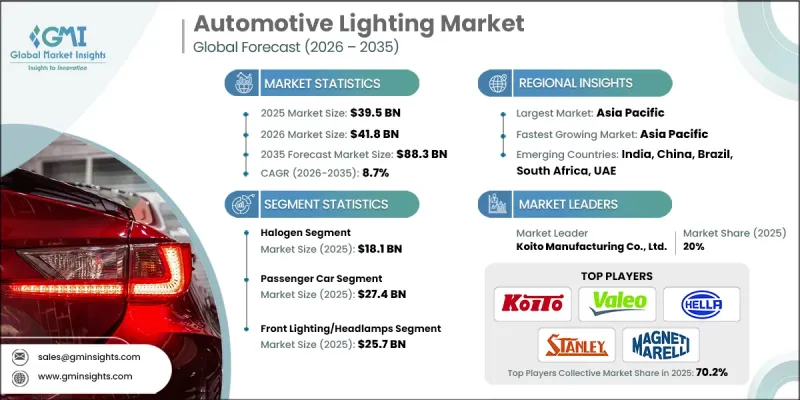

全球汽车照明市场预计到 2025 年价值 395 亿美元,预计到 2035 年将达到 883 亿美元,年复合成长率为 8.7%。

该产业的成长得益于LED和自适应照明系统的日益普及、日益严格的车辆安全标准和排放气体法规、电动车和自动驾驶汽车的日益普及、消费者对节能时尚照明的需求,以及新兴市场汽车製造业的扩张。遵守全球安全标准和能源效率要求正在加速先进照明技术的应用,从而提高驾驶员的视野、减少眩光并提升车辆的整体效率。向电气化和自动驾驶的转型进一步扩大了先进照明解决方案在现代车辆安全、能源管理和美学设计方面的应用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 395亿美元 |

| 预测金额 | 883亿美元 |

| 复合年增长率 | 8.7% |

预计到2025年,卤素灯市场规模将达到181亿美元,其强劲的需求将得益于其低廉的生产成本、简单的製造流程以及与现有车辆电气系统的广泛相容性。在LED和自适应照明系统等高端照明技术尚未普及的入门级和中檔车型中,卤素灯仍然被广泛使用,在不影响基本安全要求的前提下,提供了一种经济高效的解决方案。随着全球汽车数量的成长,卤素灯在售后替换件市场也占据重要地位,预计老旧车辆的改装需求将持续成长。此外,卤素灯泡在各种驾驶条件下都表现出可靠性,且维护需求极低,因此成为车队营运商、商用车公司以及将成本效益放在首位的开发中市场的首选。

预计到2025年,乘用车市场规模将达到274亿美元,主要得益于市场对先进照明技术的强劲需求,例如兼顾安全性和视觉美感的自我调整LED矩阵系统。这些技术能够实现动态光束调节,提升夜间能见度,并减少对向来车的眩光,从而提高驾驶安全评级。此外,乘用车买家越来越重视照明的美观性,将其作为车辆设计和品牌识别的重要组成部分,汽车製造商也正透过独特的照明模式来区分不同车型。主要市场的法规结构(例如强制性日间行车灯、自我调整头灯和能源效率标准)也在加速这些技术的普及应用。

推动要素到2025年,北美汽车照明市场份额将达到18.5%,这主要得益于车辆电气化程度的提高、LED和智慧自适应照明系统的日益普及,以及联邦照明和安全标准的严格执行。该地区先进的汽车製造生态系统、强有力的监管执行以及消费者对高性能、高能源效率照明解决方案的偏好,都为市场扩张提供了支持。先进的头灯系统、矩阵式LED和智慧运输技术正逐渐成为新型乘用车和轻型商用车的标准配置,有助于提高能见度、降低能耗并增强驾驶安全性。此外,随着自动驾驶和智慧出行基础设施的日益普及,北美製造商正大力投资于智慧互联照明解决方案的研发,这些解决方案整合了感测器和物联网技术,能够实现自适应的、与自动驾驶车辆相容的照明功能。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对LED和自适应照明系统的需求不断增长

- 严格的车辆安全标准和排放气体法规

- 电动车和自动驾驶汽车的广泛应用

- 消费者越来越偏好选择时尚节能的照明产品。

- 新兴市场汽车生产的扩张

- 挑战与困难

- 先进照明系统的初始成本很高

- 与车辆电子设备整合的复杂性

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 供应链韧性

- 地缘政治分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 产品系列比较

- 2022-2025 年重大发展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:依产品划分,2022-2035年

- LED

- 卤素

- 氙

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 商用车辆

- 摩托车

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 主要趋势

- 头灯/大灯

- 后部照明

- 室内照明

- 侧灯

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

第九章:公司简介

- 主要企业

- General Electric Company

- Samsung Electronics Co., Ltd.

- Koninklijke Philips NV

- Robert Bosch Gmbh

- 按地区分類的主要企业

- 北美洲

- Continental AG

- Lumax Industries

- Varroc Lighting Solutions

- 欧洲

- HELLA GmbH & Co. KGaA

- OSRAM Gmbh

- Tungsram Group

- Zkw Lichtsysteme Gmbh

- Zizala Lichtsysteme Gmbh

- Magnetti Marelli SpA

- Valeo Visibility Systems

- 亚太地区

- Hyundai Mobis Co., Ltd

- Koito Manufacturing Co.

- Ichikoh Industries, Ltd.

- Seoul Semiconductor

- Stanley Electric Co.Ltd

- 北美洲

- Niche Player/Disruptor

- Namyung Lighting

The Global Automotive Lighting Market was valued at USD 39.5 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 88.3 billion by 2035.

The industry's growth is driven by increasing adoption of LED and adaptive lighting systems, stricter vehicle safety and emissions regulations, rising popularity of electric and autonomous vehicles, consumer demand for energy-efficient and stylish lighting, and expansion of automotive manufacturing in emerging markets. Regulatory compliance with global safety standards and energy-efficiency mandates is encouraging the integration of advanced lighting technologies, enhancing driver visibility, reducing glare, and contributing to overall vehicle efficiency. The shift toward electrification and autonomous driving has further amplified the use of sophisticated lighting solutions as critical components of safety, energy management, and aesthetic design in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $39.5 Billion |

| Forecast Value | $88.3 Billion |

| CAGR | 8.7% |

The halogen segment accounted for USD 18.1 billion in 2025, maintaining strong demand due to its low production costs, straightforward manufacturing processes, and broad compatibility with existing vehicle electrical systems. Halogen lighting continues to be widely used in entry-level and mid-segment vehicles where premium lighting technologies like LEDs or adaptive systems are not yet standard, offering a cost-effective solution without compromising basic safety requirements. Its relevance extends to aftermarket replacements, supported by the growing global vehicle parc, which ensures a consistent demand for retrofitting older vehicles. Additionally, halogen bulbs provide reliability under diverse driving conditions and require minimal maintenance, making them a preferred choice for fleet operators, commercial vehicles, and markets in developing regions where cost efficiency remains a priority.

The passenger car segment reached USD 27.4 billion in 2025, driven by strong demand for advanced lighting features such as adaptive, LED, and matrix systems, which enhance both safety and visual appeal. These technologies provide dynamic beam adjustments, improved nighttime visibility, and glare reduction for oncoming traffic, contributing to higher driving safety ratings. Furthermore, passenger car buyers increasingly consider lighting aesthetics as part of vehicle design and brand identity, pushing automakers to differentiate their models with signature lighting patterns. Regulatory frameworks in major markets, including mandatory daytime running lights, adaptive headlamps, and energy-efficiency standards, further accelerate adoption.

North America Automotive Lighting Market held an 18.5% share in 2025, driven by rising vehicle electrification, widespread adoption of LED and smart adaptive lighting systems, and strict compliance with federal lighting and safety standards. The region's advanced automotive manufacturing ecosystem, strong regulatory enforcement, and consumer preference for high-performance, energy-efficient lighting solutions underpin market expansion. Advanced front lighting systems, matrix LED, and laser-based technologies are becoming standard in new passenger and commercial vehicle models, supporting enhanced visibility, reduced power consumption, and improved driving safety. Additionally, North American manufacturers are investing heavily in R&D for intelligent and connected lighting solutions, integrating sensors and IoT technologies to enable adaptive, autonomous vehicle-ready lighting that aligns with the growing focus on automated driving and smart mobility infrastructure.

Prominent players in the Global Automotive Lighting Market include Continental AG, General Electric Company, HELLA GmbH & Co. KGaA, Hyundai Mobis Co., Ltd, Ichikoh Industries, Ltd., Koito Manufacturing Co., Koninklijke Philips N.V., Lumax Industries, Magnetti Marelli S.p.A, Namyung Lighting, OSRAM GmbH, Robert Bosch GmbH, Samsung Electronics Co., Ltd., Seoul Semiconductor, Stanley Electric Co., Ltd., Tungsram Group, Valeo Visibility Systems, Varroc Lighting Solutions, Zizala Lichtsysteme GmbH, and ZKW Lichtsysteme GmbH. Companies in the Automotive Lighting Market are focusing on strategic initiatives such as expanding R&D for LED and adaptive systems, forming partnerships with OEMs to integrate intelligent lighting technologies, optimizing supply chains for global distribution, investing in sustainable energy-efficient solutions, launching aftermarket programs to capture legacy vehicle demand, and adopting digital and IoT-enabled lighting innovations. Emphasis on design differentiation, regulatory compliance, and modular, scalable solutions helps manufacturers strengthen market presence, improve brand recognition, and secure long-term contracts with automotive producers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Vehicle type trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for LED and adaptive lighting systems

- 3.2.1.2 Stringent vehicle safety and emission regulations

- 3.2.1.3 Increasing adoption of electric and autonomous vehicles

- 3.2.1.4 Growing consumer preference for stylish and energy-efficient lighting

- 3.2.1.5 Expansion of automotive production in emerging markets

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial costs of advanced lighting systems

- 3.2.2.2 Complexity in integration with vehicle electronics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 LED

- 5.3 Halogen

- 5.4 Xenon

Chapter 6 Market Estimates and Forecast, By Vehicle Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Commercial vehicles

- 6.4 Two wheelers

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Front lighting/Headlamps

- 7.3 Rear lighting

- 7.4 Interior lighting

- 7.5 Side lighting

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 General Electric Company

- 9.1.2 Samsung Electronics Co., Ltd.

- 9.1.3 Koninklijke Philips N.V.

- 9.1.4 Robert Bosch Gmbh

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Continental AG

- 9.2.1.2 Lumax Industries

- 9.2.1.3 Varroc Lighting Solutions

- 9.2.2 Europe

- 9.2.2.1 HELLA GmbH & Co. KGaA

- 9.2.2.2 OSRAM Gmbh

- 9.2.2.3 Tungsram Group

- 9.2.2.4 Zkw Lichtsysteme Gmbh

- 9.2.2.5 Zizala Lichtsysteme Gmbh

- 9.2.2.6 Magnetti Marelli S.p.A

- 9.2.2.7 Valeo Visibility Systems

- 9.2.3 Asia Pacific

- 9.2.3.1 Hyundai Mobis Co., Ltd

- 9.2.3.2 Koito Manufacturing Co.

- 9.2.3.3 Ichikoh Industries, Ltd.

- 9.2.3.4 Seoul Semiconductor

- 9.2.3.5 Stanley Electric Co.Ltd

- 9.2.1 North America

- 9.3 Niche Player/Disruptor

- 9.3.1 Namyung Lighting

汽车外饰LED照明市场:依产品类型、安装位置、乘用车及销售管道划分-2026-2032年全球市场预测汽车週边照明市场:依技术、销售管道、车辆类型及应用划分-2026-2032年全球市场预测汽车高位煞车灯市场:按光源、车辆类型、驱动系统和销售管道划分-2026-2032年全球市场预测下一代汽车照明市场:按产品类型、技术、车辆类型、销售管道和应用划分-2026-2032年全球市场预测汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年

汽车外饰LED照明市场:依产品类型、安装位置、乘用车及销售管道划分-2026-2032年全球市场预测汽车週边照明市场:依技术、销售管道、车辆类型及应用划分-2026-2032年全球市场预测汽车高位煞车灯市场:按光源、车辆类型、驱动系统和销售管道划分-2026-2032年全球市场预测下一代汽车照明市场:按产品类型、技术、车辆类型、销售管道和应用划分-2026-2032年全球市场预测汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年 全球汽车照明市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车照明市场规模、份额、趋势和成长分析报告(2026-2034年) 汽车照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告2026年全球汽车发光二极体(LED)灯泡市场报告

2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告2026年全球汽车发光二极体(LED)灯泡市场报告