|

市场调查报告书

商品编码

1939087

汽车照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

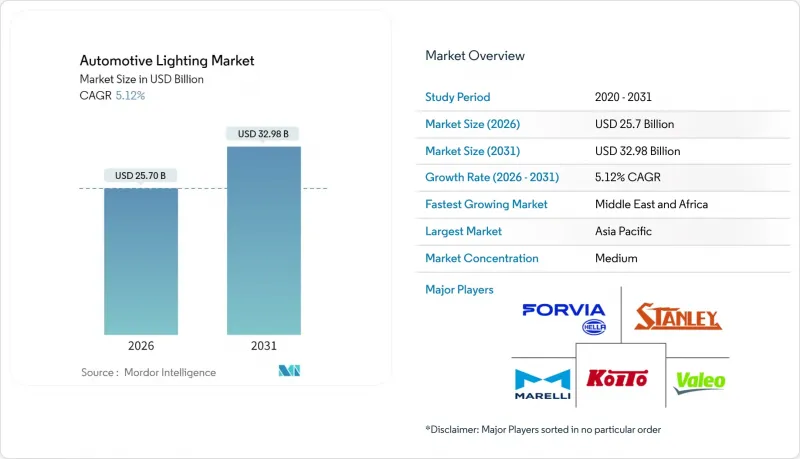

据估计,到 2026 年,汽车照明市场价值将达到 257 亿美元,高于 2025 年的 244.5 亿美元,预计到 2031 年将达到 329.8 亿美元。

预计2026年至2031年年复合成长率(CAGR)为5.12%。

市场成长主要与全球范围内不断加强的节能政策、LED的快速普及以及对更智慧、更个人化照明模组日益增长的需求密切相关。汽车製造商正持续从电力消耗量的卤素灯解决方案过渡到高度整合的LED、OLED和雷射平台,这些平台能够降低功率负载并实现更丰富的功能。电动车产量的扩张使得每一瓦节能都显得尤为重要,而自我调整远光灯在关键地区的核准也加速了高端功能的普及。在供应方面,照明专家和半导体供应商之间的策略联盟正在缩短开发週期,并为支援ADAS(高级驾驶辅助系统)通讯的数位光投影技术拓展机会。儘管亚太地区仍然是製造地,但随着政策制定者协调安全标准并发展充电基础设施,预计中东和非洲地区的销售成长速度将最快。

全球汽车照明市场趋势与洞察

强制性LED推广

为实现减碳目标,政策制定者正在逐步淘汰高能耗灯具,并在所有车型领域推广使用LED灯。欧洲车队的估算显示,全面采用LED灯每年可节省1.48兆瓦时。美国于2024年修订了FMVSS 108号联邦机动车辆安全标准,使自我调整远光灯合法化,并进一步推动LED头灯的普及。联合国第148号法规协调了核准代码,有助于下一代设备的全球型式认证。

智慧驾驶座和环境体验的需求

内装模组如今融合了数千个RGB LED灯,打造出以健康为中心的座舱环境,并与资讯娱乐系统互动。梅赛德斯-宾士数位照明系统拥有超过200万像素,可投射道路标誌,增强驾驶者的视野。实验室研究证实,先进的校准技术提升了直接照明导光板的色彩精准度和均匀性,消除了高阶仪表板上的光斑现象。

先进模组的初始成本较高

AudiQ5等高阶车型采用的数位OLED尾灯由18个可独立控制的灯段组成,这推高了物料清单(BOM)和模具成本。串联堆迭式OLED原型灯已实现77%的外部量子效率和46,000小时的使用寿命,但製造工艺的复杂性限制了其量产。 MicroLED替代OLED可以使头灯组件的功率降低30瓦,重量减轻1公斤,但前期投资成本仍然很高。

细分市场分析

乘用车领域引领汽车照明市场,预计2025年将占总营收的68.92%。同时,摩托车领域预计将以7.15%的复合年增长率实现最快成长。随着电动Scooter优先采用低功率LED以确保电池寿命,摩托车汽车照明市场规模预计将进一步扩大。 Fiem Industries已公布超过80个摩托车LED计划,计划在三年内投入生产。轻型商用车车队依靠自我调整头灯来提升密集都市区「最后一公里」的安全性。虽然中型和重型卡车的升级改造进展缓慢,但强制性的反光胶带和行车灯要求维持了持续的改装需求。

采用多感测器融合技术的自适应LED头灯将于2025年率先应用于多款国产轿车,并逐步推广至摩托车车型,以消除路边照明盲区。虽然高端乘用车已采用数位光投射技术和独特的日间行车灯模式来强化品牌形象,但车队营运商更注重耐用性和每流明成本。在预测期内,小型LED和无散热器光学元件将使先前仅限于高阶车型的自适应驾驶辅助系统(ADB)功能得以应用于低成本Scooter。

到2025年,外部模组将占汽车照明市场78.02%的份额,而内装解决方案正以7.88%的复合年增长率紧随其后。可寻址RGB阵列部署在车顶和脚部空间,以与空调和资讯娱乐功能协调工作。研究表明,协调的色温有助于减轻驾驶员夜间驾驶的疲劳。

车头灯仍然是技术试验场:联邦机动车辆安全标准 (FMVSS) 的更新允许使用自适应远光灯,使 LED 灯能够动态地阻挡对向来车的眩光。豪华 SUV 中的 OLED 尾灯能够在复杂的形状上实现均匀的亮度,这是单一 LED 灯无法实现的。反映 ADAS 警告的车内灯条现在已整合到 L3 级自动驾驶系统中,使车内氛围与外部灯光行为协调一致。

区域分析

亚太地区将引领汽车照明市场,预计2025年将占全球收入的32.22%,巩固其作为全球汽车製造商生产基地的地位。中国一级供应商目前正出口符合联合国第148号规则的自适应LED模组,为消费者提供了传统日本和欧洲製造商以外的更多选择。广东省一家领先的主要企业表示,智慧照明合约将占其2024年收入的41.5%。 Apan公司正在改进其多感测器头灯融合技术,而印度摩托车市场的蓬勃发展也正在加速通勤摩托车对LED的需求。

预计中东和非洲地区将以6.88%的复合年增长率实现最快增长,海湾国家正在建造电动车充电走廊并实施符合欧盟眩光标准的国家安全标准。沙乌地阿拉伯的目标是到2025年销售超过500万辆轻型汽车,而阿联酋的目标是到2050年实现50%的电动车普及率。这两项政策都在推动对节能灯具的需求。各国政府也正在推广光生物安全审核,要求原始设备製造商在产品进入市场前检验其蓝光含量。

受节能指令和豪华车日益普及的推动,欧洲和北美预计将分别成长4.65%和5.35%。欧盟二氧化碳排放标准奖励那些成功降低电力负荷的汽车製造商,这使得LED成为易于采用的选择。随着FMVSS自适应光束的核准,美国市场活动日益活跃,国内卡车平台计划在2026年生产週期内进行数位化照明昇级。南美洲的复合年增长率将达到6.55%,因为区域组装采用通用平台架构,将照明模组与全球标准集成,从而降低单位成本并简化售后市场认证。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 强制安装LED灯

- 对智慧驾驶座和环境体验的需求

- 电动车能源效率要求

- 用于ADAS/V2X的数位光投影技术

- OTA支持照明个性化

- 安全和能见度规定

- 市场限制

- 先进模组的初始成本较高

- 半导体和原物料价格波动

- 更严格的眩光/光生物学安全限制

- 对报废产品回收的法律责任

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和大型商用车辆

- 摩托车

- 透过使用

- 外部的

- 头灯

- 尾灯

- 日间行车灯(DRL)

- 雾灯

- 内部的

- 室内照明/足部照明

- 屋顶/穹顶

- 外部的

- 透过技术

- 卤素

- 氙气灯/HID灯

- LED

- 雷射

- 有机发光二极体

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Koito Manufacturing Co. Ltd

- Stanley Electric Co. Ltd

- Valeo SE

- Forvia-HELLA GmbH & Co. KGaA

- Marelli Holdings Co. Ltd

- Tungsram Group

- Hyundai Mobis Co.

- Lumax Industries Ltd

- ams-OSRAM AG

- ZKW Group GmbH

- SL Corporation

- Nichia Corporation

- Continental AG

- DENSO Corporation

- Lear Corporation

- Bosch Mobility Lighting Modules

- LG Innotek Co.

- Panasonic Automotive Lighting

- Seoul Semiconductor Co.

第七章 市场机会与未来展望

Automotive lighting market size in 2026 is estimated at USD 25.7 billion, growing from 2025 value of USD 24.45 billion with 2031 projections showing USD 32.98 billion, growing at 5.12% CAGR over 2026-2031.

The market's growth is primarily linked to stricter global energy-efficiency policies, rapid LED penetration, and rising demand for smarter, personalization-ready lighting modules. Automakers continue to shift away from power-hungry halogen solutions toward highly integrated LED, OLED, and laser platforms that deliver lower electrical loads and richer functionality. Intensifying electric-vehicle production magnifies the importance of every watt saved, while adaptive driving beam approvals in key regions accelerate premium feature uptake. On the supply side, strategic partnerships between lighting specialists and semiconductor suppliers are shortening development cycles and unlocking digital-light projection opportunities that support advanced driver-assistance systems (ADAS) communication. Asia-Pacific remains the manufacturing hub, yet the Middle East and Africa promise the fastest volume gains as policymakers harmonize safety rules and build charging infrastructure.

Global Automotive Lighting Market Trends and Insights

LED-penetration mandates

Policymakers are phasing out energy-intensive lamps to meet CO2-reduction targets, pushing LEDs into every vehicle segment. European fleet calculations show potential savings of 1.48 TWh per year when full LED deployment is achieved. The United States amended FMVSS 108 in 2024, legalising adaptive driving beams and further incentivising LED headlamp adoption. UN Regulation 148 unifies approval codes, easing global homologation for next-generation devices.

Smart-cockpit and ambient-experience demand

Interior modules now blend thousands of RGB LEDs to create wellness-centric cabins that synchronise with infotainment cues. Mercedes-Benz DIGITAL LIGHT packs over 2 million pixels and projects road symbols to augment driver awareness. Laboratory studies confirm that advanced calibration improves colour accuracy and uniformity in direct-lit guides, removing hotspot artefacts in premium dashboards.

High upfront cost of advanced modules

Digital OLED tail-lamps in luxury models such as the Audi Q5 use 18 individually addressable segments that raise BOM and tooling costs. Tandem-stack OLED prototypes achieve 77% external quantum efficiency at 46,000-hour lifetimes, yet manufacturing complexity limits mass-market migration. Micro-LED replacements can shave 30 W and 1 kg from a headlamp assembly, but capital equipment costs remain significant.

Other drivers and restraints analyzed in the detailed report include:

- EV energy-efficiency requirements

- Digital-light projection for ADAS/V2X

- Semiconductor and raw-material volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The passenger cars segment dominated the Automotive Lighting Market with a 68.92% Share in 2025 revenues. Meanwhile, Two-wheelers are expected to register the fastest 7.15% CAGR. The automotive lighting market size within Two-wheelers will climb as e-scooters prioritize low-draw LEDs to preserve battery autonomy. Fiem Industries disclosed more than 80 active LED projects for bikes scheduled to hit assembly lines within three years. Light commercial fleets lean on adaptive headlamps to increase last-mile safety in dense urban corridors. Medium and heavy trucks upgrade more slowly, but mandatory conspicuity tape and running-light laws still feed a steady retrofit pipeline.

Adaptive LED headlamps using multi-sensor fusion debuted on several 2025 domestic Chinese sedans and cascaded to motorcycle variants to counter bend-lighting blind spots. Passenger-car premium trims already bake in digital-light projection and signature DRL patterns to reinforce brand identity, whereas fleet operators concentrate on durability and cost per lumen. Over the forecast horizon, small-format LEDs and heatsink-free optics will let low-cost scooters adopt ADB features previously limited to luxury cars.

Exterior modules segment dominated the Automotive Lighting Market with a 78.02% share in global revenues in 2025, but Interior solutions are set to outpace with an 7.88% CAGR. Roof and foot-well zones now host addressable RGB arrays that coordinate with climate controls and infotainment events. Studies confirm that harmonized color temperature can cut driver fatigue during night-time commutes.

Headlamps remain technology testbeds: FMVSS updates permit adaptive driving beams, letting LEDs dynamically mask glare for oncoming traffic. OLED tail lights in premium SUVs deliver uniform luminance across complex shapes, which is impossible with discrete LEDs. Interior light bars that mirror ADAS warnings are now bundled with Level-3 autonomy packages, linking ambient cues to external lamp behavior.

The Automotive Lighting Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Exterior (Headlamps, Taillights, Fog Lamps, and More) and Interior (Ambient/Footwell and Roof/Dome)), Technology (Halogen, Xenon / HID, LED, Laser and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific dominated the Automotive Lighting Market and holds 32.22% of 2025 revenues, cementing its role as a production center for global carmakers. Chinese tier-one suppliers now export adaptive LED modules compliant with UN Regulation 148, widening market options beyond traditional Japanese and European incumbents. Local champions in Guangdong reported that smart-lighting contracts accounted for 41.5% of 2024 revenue. Apan refines multi-sensor headlamp fusion, while India's two-wheeler boom accelerates LED demand across commuter bikes.

The Middle East and Africa are expected to log the fastest 6.88% CAGR as Gulf states build EV charging corridors and roll out national safety codes that mirror EU glare thresholds. Saudi Arabia targets more than 5 million light-vehicle sales by 2025, and the UAE aims for 50% EV penetration by 2050, both policies fuelling the need for energy-efficient lamps. Governments also pursue photobiological safety audits, prompting OEMs to validate blue-light ratios before market entry.

Europe and North America are expected to expand at 4.65% and 5.35%, respectively, sustained by energy-conservation directives and premium-vehicle density. EU CO2 standards reward automakers who cut electrical loads, positioning LEDs as low-hanging fruit. The United States sees heightened activity after FMVSS adaptive-beam approval, with domestic truck platforms planning digital-light updates in 2026 production cycles. South America advances at 6.55% CAGR as regional assemblers adopt consolidated platform architectures that integrate global-spec lighting modules, reducing cost per unit and easing aftermarket certification.

- Koito Manufacturing Co. Ltd

- Stanley Electric Co. Ltd

- Valeo SE

- Forvia-HELLA GmbH & Co. KGaA

- Marelli Holdings Co. Ltd

- Tungsram Group

- Hyundai Mobis Co.

- Lumax Industries Ltd

- ams-OSRAM AG

- ZKW Group GmbH

- SL Corporation

- Nichia Corporation

- Continental AG

- DENSO Corporation

- Lear Corporation

- Bosch Mobility Lighting Modules

- LG Innotek Co.

- Panasonic Automotive Lighting

- Seoul Semiconductor Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 LED-penetration mandates

- 4.2.2 Smart-cockpit & ambient-experience demand

- 4.2.3 EV energy-efficiency requirements

- 4.2.4 Digital-light projection for ADAS/V2X

- 4.2.5 OTA-enabled lighting personalisation

- 4.2.6 Safety-visibility regulations

- 4.3 Market Restraints

- 4.3.1 High upfront cost of advanced modules

- 4.3.2 Semiconductor & raw-material volatility

- 4.3.3 Stricter glare/photobiological safety caps

- 4.3.4 End-of-life recycling liabilities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium & Heavy Commercial Vehicles

- 5.1.4 Two-Wheelers

- 5.2 By Application

- 5.2.1 Exterior

- 5.2.1.1 Headlamps

- 5.2.1.2 Taillights

- 5.2.1.3 Daytime Running Lights (DRLs)

- 5.2.1.4 Fog Lamps

- 5.2.2 Interior

- 5.2.2.1 Ambient / Footwell

- 5.2.2.2 Roof / Dome

- 5.2.1 Exterior

- 5.3 By Technology

- 5.3.1 Halogen

- 5.3.2 Xenon / HID

- 5.3.3 LED

- 5.3.4 Laser

- 5.3.5 OLED

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Koito Manufacturing Co. Ltd

- 6.4.2 Stanley Electric Co. Ltd

- 6.4.3 Valeo SE

- 6.4.4 Forvia-HELLA GmbH & Co. KGaA

- 6.4.5 Marelli Holdings Co. Ltd

- 6.4.6 Tungsram Group

- 6.4.7 Hyundai Mobis Co.

- 6.4.8 Lumax Industries Ltd

- 6.4.9 ams-OSRAM AG

- 6.4.10 ZKW Group GmbH

- 6.4.11 SL Corporation

- 6.4.12 Nichia Corporation

- 6.4.13 Continental AG

- 6.4.14 DENSO Corporation

- 6.4.15 Lear Corporation

- 6.4.16 Bosch Mobility Lighting Modules

- 6.4.17 LG Innotek Co.

- 6.4.18 Panasonic Automotive Lighting

- 6.4.19 Seoul Semiconductor Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车外饰LED照明市场:依产品类型、安装位置、乘用车及销售管道划分-2026-2032年全球市场预测汽车週边照明市场:依技术、销售管道、车辆类型及应用划分-2026-2032年全球市场预测汽车高位煞车灯市场:按光源、车辆类型、驱动系统和销售管道划分-2026-2032年全球市场预测下一代汽车照明市场:按产品类型、技术、车辆类型、销售管道和应用划分-2026-2032年全球市场预测汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年

汽车外饰LED照明市场:依产品类型、安装位置、乘用车及销售管道划分-2026-2032年全球市场预测汽车週边照明市场:依技术、销售管道、车辆类型及应用划分-2026-2032年全球市场预测汽车高位煞车灯市场:按光源、车辆类型、驱动系统和销售管道划分-2026-2032年全球市场预测下一代汽车照明市场:按产品类型、技术、车辆类型、销售管道和应用划分-2026-2032年全球市场预测汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年 全球汽车照明市场规模、份额、趋势和成长分析报告(2026-2034年)

全球汽车照明市场规模、份额、趋势和成长分析报告(2026-2034年) 汽车照明市场机会、成长要素、产业趋势分析及2026年至2035年预测汽车照明市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

汽车照明市场机会、成长要素、产业趋势分析及2026年至2035年预测汽车照明市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告

2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告