|

市场调查报告书

商品编码

1959625

分析 2026 年至 2035 年电力分配业务市场的机会、成长要素、产业趋势和预测。Electric Distribution Utility Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

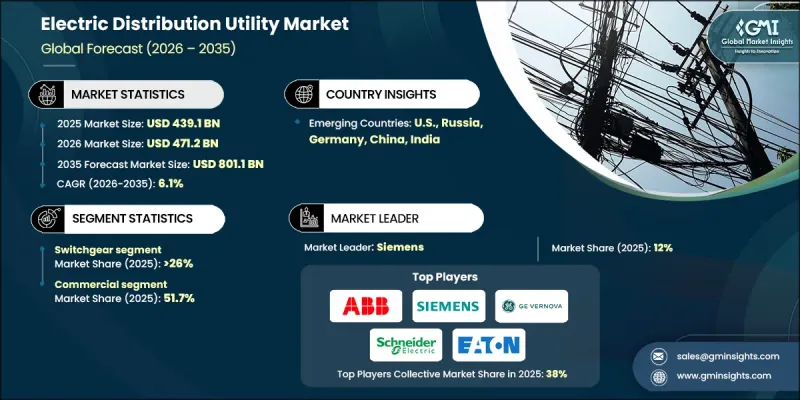

2025年全球电力分配市场价值为4,391亿美元,预计2035年将达到8,011亿美元,年复合成长率为6.1%。

这一成长主要得益于配电网路现代化改造的资本投入增加,这些改造包括数位化、自动化和即时系统视觉化。公共产业正在加强网路建设,以提高营运效率、服务可靠性,并在整个配电资产范围内实现数据驱动的规划。交通、住宅、商业和工业领域的电气化率不断提高,对配电层面的负载需求也随之增加;同时,都市区和半都市区的持续基础设施建设也推动了电力消耗量的成长。电力公司正透过加强和扩大网路来应对这项挑战,以适应更高的容量并确保稳定的电力供应。气候变迁和老旧电气元件的更换需求进一步加速了对容错和自动化输配电技术的投资。这些努力旨在透过升级先进的保护系统、智慧配电设备和电缆解决方案,提高输配电网的稳定性,减少停电时间,并提升服务品质。透过数位化向灵活智慧的配电基础设施的广泛转型,仍然是推动市场发展的核心动力。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 4391亿美元 |

| 预测金额 | 8011亿美元 |

| 复合年增长率 | 6.1% |

预计到2025年,开关设备市占率将达到26%,并在2035年之前以7%的复合年增长率成长。推动市场需求成长的主要因素是先进电网解决方案的普及,这些方案能够提升发电、配电和用电各环节的效率。已开发国家和新兴国家对老旧基础设施的大规模维修以及配电网路的持续扩张,进一步巩固了开关设备部署的前景。

预计2035年,工业终端用户领域将以6%的复合年增长率成长。对高可靠性和高品质电力需求不断增长的工业设施的扩张,推动了配电基础设施需求的成长。有利的政府政策、先进製造流程的日益普及以及对客製化变电站和馈线系统投资的增加,都对市场动态产生了积极影响。

预计2035年,欧洲电力分配市场规模将达到1,620亿美元。输电网现代化、可再生能源併网以及对长期脱碳目标的重视,正推动配电基础设施的大量投资。电网扩容、智慧电网技术的应用以及先进工业能力的提升,也持续增强该地区的成长前景。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 影响价值链的关键因素

- 中断

- 监管环境

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新机会和趋势

- 利用物联网技术实现数位转型

- 进入新兴市场

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 企业市占率分析:按地区划分

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 重要合作伙伴关係和合作

- 主要併购活动

- 产品创新和新产品发布

- 市场扩大策略

- 竞争性标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 市场规模及预测:依组件划分,2022-2035年

- 配电变电站

- 配电变压器

- 开关设备

- 电力线和电线杆

- AMI智能电錶

- 其他的

第六章 市场规模与预测:依最终用途划分,2022-2035年

- 住宅

- 商业的

- 工业的

第七章 市场规模及预测:依电压等级划分,2022-2035年

- 低电压

- 中压

- 围栏内

- 外部的

第八章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- ABB

- ACWA Power

- China Yangtze Power

- Coil Innovation

- Duke Energy

- Eaton

- Enel

- Engie

- Fuji Electric

- GE Vernova

- Hitachi Energy

- Iberdrola

- Kansai Electric Power

- Lucy Group

- Mitsubishi Electric Corporation

- National Grid

- Orecco Electric

- Schneider Electric

- SGC

- Siemens

- Siemens Energy

- Southern Company

The Global Electric Distribution Utility Market was valued at USD 439.1 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 801.1 billion by 2035.

Growth is supported by increasing capital allocation toward modernizing distribution networks through digitalization, automation, and real-time system visibility. Utilities are strengthening their networks to improve operational efficiency, service reliability, and data-driven planning across distribution assets. Rising electrification across transportation, residential, commercial, and industrial applications is placing higher load requirements at the distribution level, while ongoing infrastructure development across urban and semi-urban regions continues to elevate electricity consumption. Utilities are responding by reinforcing and expanding networks to handle higher capacity requirements and ensure stable power delivery. Changing climate patterns and the need to replace aging electrical components are further accelerating investment in resilient and automated grid technologies. These efforts focus on improving grid stability, reducing outage duration, and enhancing service quality through advanced protection systems, intelligent distribution equipment, and upgraded cabling solutions. The broader transition toward digitally enabled, flexible, and intelligent distribution infrastructure remains a central growth driver for the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $439.1 Billion |

| Forecast Value | $801.1 Billion |

| CAGR | 6.1% |

The switchgear segment held 26% share in 2025 and is expected to grow at a CAGR of 7% through 2035. Demand is driven by widespread adoption of advanced grid solutions that enhance efficiency across power generation, distribution, and consumption. Large-scale refurbishment of aging infrastructure and continuous expansion of distribution networks across developed and emerging economies are further strengthening the outlook for switchgear deployment.

The industrial end-use segment is projected to grow at a CAGR of 6% by 2035. Expansion of industrial facilities requiring high reliability and power quality is supporting increased demand for distribution infrastructure. Favorable government policies, rising adoption of advanced manufacturing practices, and growing investment in tailored substations and feeder systems are positively influencing market dynamics.

Europe Electric Distribution Utility Market is expected to reach USD 162 billion by 2035. Strong focus on grid modernization, renewable energy integration, and long-term decarbonization goals is driving significant investment in distribution infrastructure. Network expansion, adoption of intelligent grid technologies, and development of advanced industrial capacity continue to strengthen regional growth prospects.

Key companies operating in the Global Electric Distribution Utility Market include Siemens, Schneider Electric, ABB, Hitachi Energy, GE Vernova, Mitsubishi Electric Corporation, Eaton, Enel, Iberdrola, Engie, National Grid, Duke Energy, Southern Company, Siemens Energy, Fuji Electric, Kansai Electric Power, China Yangtze Power, ACWA Power, Lucy Group, Orecco Electric, Coil Innovation, and SGC. Companies in the Electric Distribution Utility Market are reinforcing their market position through large-scale investment in digital grid technologies and infrastructure modernization. Utilities and technology providers focus on automation, advanced analytics, and intelligent equipment to improve reliability and operational efficiency. Strategic partnerships with technology firms help accelerate the deployment of smart distribution solutions. Firms are expanding grid capacity and upgrading legacy assets to support rising electricity demand and the integration of decentralized energy sources. Emphasis on resilience planning, predictive maintenance, and cybersecurity strengthens long-term network performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Component trends

- 2.4 End use trends

- 2.5 Voltage trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digital transformation with IoT technologies

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035, (USD Million)

- 5.1 Key trends

- 5.2 Distribution substations

- 5.3 Distribution transformers

- 5.4 Switchgear

- 5.5 Distribution lines and poles

- 5.6 AMI smart meters

- 5.7 Others

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035, (USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Voltage, 2022 - 2035, (USD Million)

- 7.1 Key trends

- 7.2 Low voltage

- 7.3 Medium voltage

- 7.3.1 Behind the fence

- 7.3.2 Outside the fence

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035, (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Egypt

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 ACWA Power

- 9.3 China Yangtze Power

- 9.4 Coil Innovation

- 9.5 Duke Energy

- 9.6 Eaton

- 9.7 Enel

- 9.8 Engie

- 9.9 Fuji Electric

- 9.10 GE Vernova

- 9.11 Hitachi Energy

- 9.12 Iberdrola

- 9.13 Kansai Electric Power

- 9.14 Lucy Group

- 9.15 Mitsubishi Electric Corporation

- 9.16 National Grid

- 9.17 Orecco Electric

- 9.18 Schneider Electric

- 9.19 SGC

- 9.20 Siemens

- 9.21 Siemens Energy

- 9.22 Southern Company

电动商用车市场:2026-2032年全球市场预测(依推进系统、应用、车辆类型及最终用户产业划分)

电动商用车市场:2026-2032年全球市场预测(依推进系统、应用、车辆类型及最终用户产业划分) 2026年全球电动多用途车辆市场报告

2026年全球电动多用途车辆市场报告 电动多用途车辆市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球电动多用途车辆市场规模、份额、趋势和成长分析报告(2026-2034年)

电动多用途车辆市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球电动多用途车辆市场规模、份额、趋势和成长分析报告(2026-2034年) 电动多用途车辆市场规模、份额和成长分析(按车辆类型、电池类型、驱动系统、应用、乘客容量、推进方式和地区划分)-2026-2033年产业预测

电动多用途车辆市场规模、份额和成长分析(按车辆类型、电池类型、驱动系统、应用、乘客容量、推进方式和地区划分)-2026-2033年产业预测 电动多用途车市场-全球产业规模、份额、趋势、机会和预测(按车型、电池、应用、地区和竞争细分,2020-2030 年)

电动多用途车市场-全球产业规模、份额、趋势、机会和预测(按车型、电池、应用、地区和竞争细分,2020-2030 年) 全球电动多用途车市场全球配电公司市场

全球电动多用途车市场全球配电公司市场 电动车市场规模、份额和趋势分析报告:按车辆类型、电池类型、驱动类型、推进类型、乘客容量、应用、地区和细分市场预测,2025-2030 年

电动车市场规模、份额和趋势分析报告:按车辆类型、电池类型、驱动类型、推进类型、乘客容量、应用、地区和细分市场预测,2025-2030 年 2032 年电动多用途车市场预测:按车辆类型、推进类型、电池类型、驱动类型、负载容量、每次充电行驶里程、应用、最终用户和地区进行的全球分析

2032 年电动多用途车市场预测:按车辆类型、推进类型、电池类型、驱动类型、负载容量、每次充电行驶里程、应用、最终用户和地区进行的全球分析