|

市场调查报告书

商品编码

1959626

2026 年至 2035 年光电感测器市场的机会、成长要素、产业趋势分析与预测。Photoelectric Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

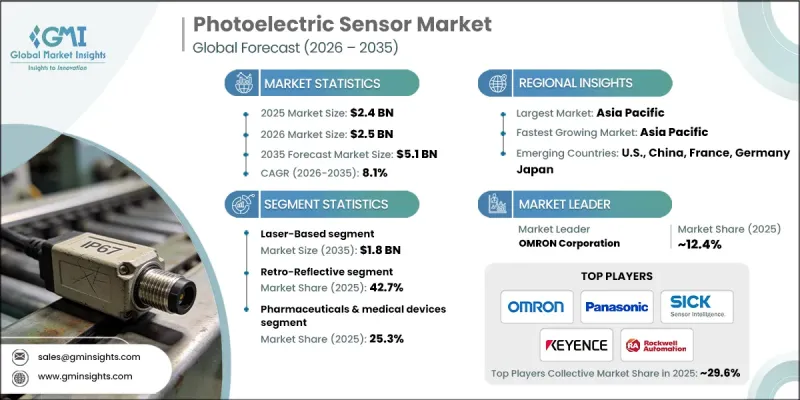

2025 年全球光电感测器市场价值 24 亿美元,预计到 2035 年将达到 51 亿美元,年复合成长率为 8.1%。

该行业的成长得益于各领域流程自动化和智慧製造的普及。企业越来越多地使用光电感测器进行产品检测、计数和检验,从而帮助製造商减少误差并提高生产效率。对自动化物流、电商履约和库存管理日益增长的需求进一步推动了感测器的应用,因为感测器能够实现更快的货物分类、追踪和精准处理。工业4.0和物联网技术的整合正在改变市场格局,在智慧工厂环境中实现即时监控、预测性维护和互联营运。这些互联感测器能够提供可操作的洞察,优化生产流程,并最大限度地减少停机时间,尤其是在汽车、电子和包装行业。此外,小型化趋势正在推动感测器的更广泛应用,因为紧凑且节省空间的感测器适用于PCB组装设备、机器人以及其他空间受限的应用。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 24亿美元 |

| 预测金额 | 51亿美元 |

| 复合年增长率 | 8.1% |

预计到2035年,雷射光电感测器市场规模将达到18亿美元,主要得益于工业环境中对高精度、远距离检测的需求。雷射感测器透过聚焦光斑实现对微小物体的精确检测和定位,在组装和半导体製造等对一致性要求极高的应用中发挥着至关重要的作用。

预计2026年至2035年间,对射式感测器市场将以9.5%的复合年增长率成长。对射式感测器非常适合高精度、远距离侦测需求,并且正在协助智慧工厂和高速包装作业的发展。物联网感测技术和先进光电设计等技术创新正在提升可靠性、精度和系统整合度,推动製造商采用对射式解决方案。

预计到2025年,北美光电感测器市场占有率将达到28.2%。该地区的成长主要得益于製造业、物流和包装行业的快速工业自动化,感测器能够实现精准的物件检测和高效的工作流程。工业物联网(IIoT)、智慧工厂计划以及严格的安全和品质标准的普及,正在加速光电感测器在工业工厂的部署,而现有市场参与者也在不断创新,以满足不断变化的工业需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 工业自动化的广泛应用

- 工业4.0和智慧工厂概念

- 包装和物流行业需求不断增长

- 各领域对高精度感测的需求日益增长

- 人们对能源效率感测器的兴趣日益浓厚

- 产业潜在风险与挑战

- 大量资本支出和营运费用

- 与旧有系统集成

- 市场机会

- 正在经历工业化和自动化的地区

- 智慧建筑应用范围的扩大

- 促进因素

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线广度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 受让人

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 2022-2025 年重大发展

- 併购

- 合作伙伴关係和合资企业

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 光源市场估算与预测(2022-2035年)

- LED底座

- 雷射基座

- 光纤

第六章 市场估算与预测:依光学配置划分,2022-2035年

- 对射式系统

- 反光

- 漫反射型

第七章 市场估计与预测:依检测距离划分,2022-2035年

- 短距离:100毫米或更短

- 中等距离:大于 100 毫米至小于 1000 毫米

- 长距离:大于 1,000 毫米至小于 10,000 毫米

- 超远距离/扩展距离:超过 10,000 毫米

第八章 市场估算与预测:依房屋类型划分,2022-2035年

- 圆柱形

- 矩形/盒形

- 插槽/叉

第九章 市场估计与预测:依最终用户产业划分,2022-2035年

- 工业製造

- 汽车/运输设备

- 食品/饮料加工

- 药品和医疗设备

- 建筑自动化和智慧基础设施

- 电子设备及半导体製造

- 能源、公共产业和基础设施

- 航太/国防

- 其他的

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- OMRON Corporation

- Panasonic Industry Co., Ltd.

- SICK AG

- KEYENCE CORPORATION

- Rockwell Automation

- Balluff Inc

- OPTEX FA CO., LTD.

- Baumer

- Pepperl+Fuchs SE

- TAKEX EUROPE LTD.

- Wenglor

- Schneider Electric

- Banner Engineering Corp.

- Hans Turck GmbH &Co. KG

- Leuze Electronic Pvt. Ltd.

The Global Photoelectric Sensor Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 8.1% to reach USD 5.1 billion by 2035.

The growth of the industry is driven by the widespread adoption of process automation and smart manufacturing across sectors. Companies are increasingly using photoelectric sensors to detect, count, and inspect products, allowing manufacturers to reduce errors and boost production efficiency. Rising demand for automated logistics, e-commerce fulfillment, and inventory management has further propelled adoption, as sensors enable faster sorting, tracking, and precise handling of goods. Integration of Industry 4.0 and IoT technologies is transforming the market, enabling real-time monitoring, predictive maintenance, and connected operations in smart factory environments. These connected sensors provide actionable insights, optimize production workflows, and minimize downtime, particularly in automotive, electronics, and packaging sectors. Additionally, the trend toward miniaturization has made compact, space-efficient sensors suitable for PCB-mounted equipment, robots, and other confined applications, fueling broader adoption.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 8.1% |

The laser-based photoelectric sensor segment is projected to reach USD 1.8 billion by 2035, driven by its demand for high-precision, long-range detection in industrial environments. Laser sensors provide focused light spots for accurate detection of small objects and precise positioning, which is essential for applications requiring consistency, such as assembly lines and semiconductor manufacturing.

The through-beam segment is expected to grow at a CAGR of 9.5% between 2026 and 2035. Through-beam sensors are favored for high-precision, long-distance detection needs, supporting the development of smart factories and high-speed packaging operations. Technological innovations, including IoT-enabled sensing and advanced photoelectric designs, are improving reliability, accuracy, and system integration, prompting manufacturers to adopt through-beam solutions.

North America Photoelectric Sensor Market accounted for a 28.2% share in 2025. The region's growth is supported by rapid industrial automation in manufacturing, logistics, and packaging, where sensors enable precise object detection and streamlined workflows. Adoption of IIoT, smart factory initiatives, and strict safety and quality standards has accelerated implementation in industrial plants, while established market players continue to innovate to meet evolving industrial requirements.

Key players in the Global Photoelectric Sensor Market include Panasonic Industry Co., Ltd., Rockwell Automation, Baumer, Banner Engineering Corp., SICK AG, Hans Turck GmbH & Co. KG, OMRON Corporation, TAKEX EUROPE LTD., OPTEX FA CO., LTD., Wenglor, Leuze electronic Pvt. Ltd., Keyence Corporation, Schneider Electric, Balluff Inc., and Pepperl+Fuchs SE. Companies in the photoelectric sensor market are adopting multiple strategies to strengthen their market presence and maintain a competitive edge. Firms focus on continuous innovation, developing sensors with higher precision, smaller footprints, and enhanced reliability to meet advanced industrial needs. Investments in research and development enable integration of IoT, AI, and predictive maintenance features into sensor solutions. Companies also expand their global footprint through strategic partnerships, mergers, and regional distribution networks. Additionally, they emphasize customer-centric solutions by providing customization, technical support, and training services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 System type trends

- 2.2.2 Deployment model trends

- 2.2.3 End-user industry trends

- 2.2.4 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Widespread adoption of industrial automation

- 3.2.1.2 Industry 4.0 & Smart factory initiatives

- 3.2.1.3 Growing demand in packaging & logistics

- 3.2.1.4 Rising Demand for high precision sensing in sectors

- 3.2.1.5 Growing focus towards energy efficiency sensors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Significant capital and operational expenditure

- 3.2.2.2 Integration challenges with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Growing regions with rising industrialization and automation

- 3.2.3.2 Expanding adoption in smart buildings

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Patent and IP analysis

- 3.10 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors’ landscape

Chapter 5 Market Estimates and Forecast, By Light Source, 2022 - 2035 (USD Billion, Units)

- 5.1 Key trends

- 5.2 LED-Based

- 5.3 Laser-Based

- 5.4 Fiber-Optic

Chapter 6 Market Estimates and Forecast, By Optical Configuration, 2022 - 2035 (USD Billion, Units)

- 6.1 Key trends

- 6.2 Through-Beam

- 6.3 Retro-Reflective

- 6.4 Diffuse

Chapter 7 Market Estimates and Forecast, By Sensing Range, 2022 - 2035 (USD Billion, Units)

- 7.1 Key trends

- 7.2 Short Range: ≤ 100 mm

- 7.3 Medium Range: >100 mm - ≤ 1,000 mm

- 7.4 Long Range: >1,000 mm - ≤ 10,000 mm

- 7.5 Ultra-Long / Extended Range: >10,000 mm

Chapter 8 Market Estimates and Forecast, By Housing Geometry, 2022 - 2035 (USD Billion, Units)

- 8.1 Key trends

- 8.2 Cylindrical

- 8.3 Rectangular / Box

- 8.4 Slot / Fork

Chapter 9 Market Estimates and Forecast, By End-User Industry, 2022 - 2035 (USD Billion, Units)

- 9.1 Key trends

- 9.2 Industrial Manufacturing

- 9.3 Automotive & Transportation

- 9.4 Food & Beverage Processing

- 9.5 Pharmaceuticals & Medical Devices

- 9.6 Building Automation & Smart Infrastructure

- 9.7 Electronics & Semiconductor Manufacturing

- 9.8 Energy, Utilities & Infrastructure

- 9.9 Aerospace & Defense

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 OMRON Corporation

- 11.2 Panasonic Industry Co., Ltd.

- 11.3 SICK AG

- 11.4 KEYENCE CORPORATION

- 11.5 Rockwell Automation

- 11.6 Balluff Inc

- 11.7 OPTEX FA CO., LTD.

- 11.8 Baumer

- 11.9 Pepperl+Fuchs SE

- 11.10 TAKEX EUROPE LTD.

- 11.11 Wenglor

- 11.12 Schneider Electric

- 11.13 Banner Engineering Corp.

- 11.14 Hans Turck GmbH & Co. KG

- 11.15 Leuze Electronic Pvt. Ltd.

四象限检测器市场报告:趋势、预测与竞争分析(至2035年)

四象限检测器市场报告:趋势、预测与竞争分析(至2035年) 光电感测器:全球市场份额和排名、总收入和需求预测(2026-2032年)全球光电感测器市场:依侦测模式、侦测范围、结构、光束光源、安装方式、最终用户、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年)

光电感测器:全球市场份额和排名、总收入和需求预测(2026-2032年)全球光电感测器市场:依侦测模式、侦测范围、结构、光束光源、安装方式、最终用户、国家及地区划分-产业分析、市场规模、份额及预测(2025-2032年) 光电感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、功能、安装类型及最终用户划分

光电感测器市场分析及预测(至2035年):依类型、产品类型、技术、应用、组件、功能、安装类型及最终用户划分 2026年全球光电感测器市场报告

2026年全球光电感测器市场报告 光电感测器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、光束源、产业、地区和竞争格局划分,2021-2031年)

光电感测器市场 - 全球产业规模、份额、趋势、机会及预测(按类型、光束源、产业、地区和竞争格局划分,2021-2031年) 光电感测器市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034)

光电感测器市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2026-2034) 光电感测器市场规模、份额和成长分析(按类型、产品、检测距离、结构、光源、输出、应用和地区划分)-2026-2033年产业预测

光电感测器市场规模、份额和成长分析(按类型、产品、检测距离、结构、光源、输出、应用和地区划分)-2026-2033年产业预测 光电感测器市场:产业趋势及全球预测(至 2035 年)-依检测范围、光源、感测器类型、终端用户、结构、技术、公司规模及主要地区划分

光电感测器市场:产业趋势及全球预测(至 2035 年)-依检测范围、光源、感测器类型、终端用户、结构、技术、公司规模及主要地区划分 全球光电感测器市场:依检测方法、结构、安装方式及光源分類的2032年预测

全球光电感测器市场:依检测方法、结构、安装方式及光源分類的2032年预测