|

市场调查报告书

商品编码

1959637

2026 年至 2035 年授权汽车服务中心的市场机会、成长要素、产业趋势分析与预测。Authorized Car Service Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

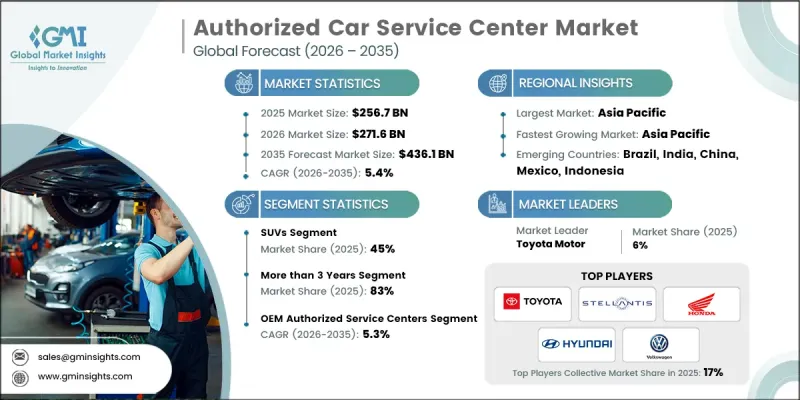

2025 年全球授权汽车服务中心市场价值为 2,567 亿美元,预计到 2035 年将达到 4,361 亿美元,年复合成长率为 5.4%。

授权服务中心在维护车辆安全、性能和耐用性方面发挥着至关重要的作用,它们提供原厂认证的保养、维修和升级服务。该市场涵盖经销商服务中心、多品牌授权研讨会和专业维修连锁机构,所有这些机构都提供有保障的维修、诊断解决方案和原厂配件。随着车辆保有量的增加和使用週期的延长,车辆的复杂性也随之增加,从而推动了对专业服务网络的需求。原厂製造商正日益重视授权服务中心,以提高客户满意度、维持车辆转售价值并确保保固合规性。联网汽车技术和远端资讯处理技术的整合正在加速预测性维护的发展,并促进更频繁、更主动的保养服务。数位化正在重塑整个产业,服务中心采用整合技术平台来简化客户服务、诊断、配件采购和服务管理,从根本上改变了整个产业的流程和投资策略。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 2567亿美元 |

| 预测金额 | 4361亿美元 |

| 复合年增长率 | 5.4% |

预计到2025年,SUV市占率将达到45%,并在2035年之前以5.7%的复合年增长率成长。 SUV因其多功能性、高端定位以及能够提高每次保养收入的复杂系统而备受青睐。维护这些车辆需要特别关注全轮驱动系统、大型煞车系统、复杂的悬吊诊断以及更频繁的轮胎更换。

预计到2025年,OEM认证服务中心市占率将达到57%,并在2035年之前以5.3%的复合年增长率成长。这些服务中心在製造商的独家授权下运营,提供专用诊断工具、保固退款和OEM培训。凭藉品牌信誉、原厂配件供应以及严格遵守製造商指南,它们比独立服务供应商拥有明显的竞争优势。

预计到2025年,中国授权汽车服务中心市场规模将达到414亿美元,并在2035年之前以5.9%的复合年增长率持续成长。这一增长主要得益于区域城市汽车保有量的增长、单车维修保养支出的增加以及豪华车对先进维修保养需求的不断增长。线上预约、行动支付和联网汽车诊断等数位化服务正逐渐成为业界标准。中国主要汽车製造商正透过授权服务中心、行动服务小组和换电站等方式创新服务模式,以提升服务的便利性和效率。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 车辆老化和车辆拥有周期延长

- 车辆日益复杂和技术整合不断进步

- 里程数(VMT)增加

- 严格的排放气体法规和安全标准

- 消费者对官方服务的偏好日益增长

- 扩大车辆保固计划

- 产业潜在风险与挑战

- 高昂的基础设施和设备成本

- 熟练技术人员短缺及训练成本

- 经济不确定性和通货膨胀的影响

- 供应链中断和零件供应情况

- 市场机会

- 电动车服务市场的崛起

- 数位转型和线上服务预订

- 订阅式维护计划

- 在新兴市场拓展业务

- 车队管理服务

- 二手车维修服务的成长

- 促进因素

- 成长潜力分析

- 监管环境

- 北美洲

- 美国联邦政府关于车辆安全标准、排放气体标准和售后服务的法规。

- 加拿大 - 认证维护和电动车服务交付框架

- 欧洲

- 德国及欧盟车辆安全法规及国家服务标准

- 英国—关于脱欧后服务合规性和联网汽车的指导意见

- 法国-车辆检验系统与电动车服务政策

- 义大利——智慧交通系统试点计画和智慧服务法规

- 亚太地区

- 中国 - 工信部(工业和资讯化部)车辆服务义务和标准

- 印度—新兴汽车服务与互联互通法规

- 日本 - ITS 连线与认证服务政策

- 澳洲—技术中立的智慧交通系统政策

- LATAM

- 墨西哥 - NOM车辆安全标准

- 阿根廷 - 国家交通法 24.449

- 中东和非洲

- 南非共和国 - 道路交通法(1996 年)

- 沙乌地阿拉伯—交通运输法律与2030愿景交通运输政策

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 数位服务预订平台

- 人工智慧驱动的诊断系统

- 新兴技术

- 预测性维护技术

- 电动车服务技术与基础设施

- 当前技术趋势

- 专利分析

- 价格分析

- 服务定价模式

- 人事费用趋势

- 零件加价分析

- 竞争性定价策略

- 使用案例和成功案例

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 车辆车队组成与车龄分析

- 全球车辆拥有量统计数据

- 车辆平均年龄趋势

- 对服务需求的影响

- 单位经济效益及服务中心盈利基准分析

- 电动车对传统服务商业模式的影响

- 对标数位化客户旅程与客户体验

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依车辆类型划分,2022-2035年

- 掀背车车

- SUV

- 轿车

第六章 市场估价与预测:依车型年份划分,2022-2035年

- 不到3年

- 3年或以上

第七章 市场估计与预测:依驱动因素划分,2022-2035年

- 内燃机(ICE)

- HEV/PHEV

- 电动车(EV)

第八章 市场估算与预测:依服务业划分,2022-2035年

- 引擎

- 动力传输

- 煞车

- 暂停

- 电

- 身体

- 胎

- 腰带和配件

- 其他的

第九章 市场估算与预测:依服务供应商,2022-2035年

- OEM授权服务中心

- 多品牌服务中心

- 独立维修店

第十章 市场估价与预测:依最终用途划分,2022-2035年

- 个人客户

- 车队营运商

- 企业客户

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十二章:公司简介

- 世界玩家

- 3M

- BMW

- Castrol

- Ford Motor

- General Motors

- Groupe Renault

- Honda Motor

- Hyundai Motor

- Mercedes-Benz

- Mobivia

- Robert Bosch

- Stellantis

- Suzuki Motor

- Toyota Motor

- Volkswagen

- 本地球员

- Automovill Technologies

- Carxpert Garage

- Lansdowne Automobile

- Mahindra First Choice

- Meineke Car Care Centers

- Mobil1 Car Care

- TVS Automobile Solutions

- 新兴企业和技术供应商

- GoMechanic

- Wrench

- YourMechanic

The Global Authorized Car Service Center Market was valued at USD 256.7 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 436.1 billion by 2035.

Authorized service centers play a vital role in maintaining vehicle safety, performance, and longevity by offering OEM-certified maintenance, repairs, and upgrades. The market encompasses dealership service centers, multi-brand authorized workshops, and specialized maintenance chains, all providing warranty-backed repairs, diagnostic solutions, and genuine spare parts. As vehicle fleets grow and ownership cycles lengthen, vehicle complexity rises, driving demand for professional service networks. OEMs are increasingly focusing on authorized service centers to improve customer satisfaction, preserve resale value, and ensure warranty compliance. The integration of connected vehicle technologies and telematics has accelerated predictive maintenance, encouraging more frequent and proactive service visits. Digitalization is reshaping the sector, with service centers adopting integrated technology platforms to streamline customer interactions, diagnostics, parts sourcing, and service management, fundamentally transforming operational workflows and investment strategies across the industry.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $256.7 Billion |

| Forecast Value | $436.1 Billion |

| CAGR | 5.4% |

The SUV segment held a 45% share in 2025 and is expected to grow at a CAGR of 5.7% through 2035. SUVs are favored due to their versatility, premium positioning, and complex systems, which increase per-service revenue. Maintenance for these vehicles involves specialized attention to all-wheel-drive systems, larger brakes, complex suspension diagnostics, and more frequent tire replacements.

The OEM-authorized service centers segment held 57% share in 2025, with a 5.3% CAGR forecast through 2035. These centers operate under exclusive manufacturer authorization, offering proprietary diagnostics, warranty reimbursement, and OEM training. Their brand trust, access to genuine parts, and adherence to manufacturer guidelines give them a clear competitive advantage over independent service providers.

China Authorized Car Service Center Market reached USD 41.4 billion in 2025 and will grow at a CAGR of 5.9% through 2035. Growth is fueled by rising vehicle ownership in lower-tier cities, increasing service expenditure per vehicle, and higher demand for advanced maintenance in premium vehicles. Digital service adoption, including online booking, mobile payment, and connected vehicle diagnostics, is becoming standard. Leading Chinese OEMs are innovating service delivery through authorized centers, mobile units, and battery swap stations, enhancing convenience and efficiency.

Key players in the Global Authorized Car Service Center Market include Toyota Motor, Mercedes-Benz, Ford Motor, Honda Motor, Volkswagen, BMW, Stellantis, Hyundai Motor, Robert Bosch, and General Motors. Companies in the Authorized Car Service Center Market are strengthening their presence through multiple strategies, including expanding geographically into emerging markets, integrating digital platforms for booking, payment, and service tracking, and investing in mobile service solutions. They are forming partnerships with local operators to increase reach, leveraging data analytics to offer predictive maintenance, and improving customer experience with faster turnaround times. OEMs focus on enhancing brand loyalty by providing training, proprietary tools, and genuine parts to maintain service quality, while adopting flexible pricing and subscription-based maintenance plans to attract a broader customer base. Continuous innovation in diagnostics, connected vehicle services, and energy-efficient repairs further reinforces their competitive foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Vehicles Age

- 2.2.4 Propulsion

- 2.2.5 Service

- 2.2.6 Service Providers

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging vehicle fleet and extended ownership cycles

- 3.2.1.2 Rising vehicle complexity and technology integration

- 3.2.1.3 Increasing vehicle miles traveled (VMT)

- 3.2.1.4 Stringent emission and safety standards

- 3.2.1.5 Growing consumer preference for authorized services

- 3.2.1.6 Expansion of vehicle warranty programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High infrastructure and equipment costs

- 3.2.2.2 Skilled technician shortage and training costs

- 3.2.2.3 Economic uncertainties and inflation impact

- 3.2.2.4 Supply chain disruptions and parts availability

- 3.2.3 Market opportunities

- 3.2.3.1 Electric vehicle service market emergence

- 3.2.3.2 Digital transformation and online service booking

- 3.2.3.3 Subscription-based maintenance programs

- 3.2.3.4 Expansion in emerging markets

- 3.2.3.5 Fleet management services

- 3.2.3.6 Used vehicle servicing growth

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal vehicle safety, emissions, and post-repair service regulations

- 3.4.1.2 Canada - Certified maintenance and EV servicing framework

- 3.4.2 Europe

- 3.4.2.1 Germany- EU vehicle safety regulations & national service standards

- 3.4.2.2 UK- Post-Brexit service compliance & connected vehicle guidance

- 3.4.2.3 France- National vehicle inspection & EV servicing policy

- 3.4.2.4 Italy- ITS pilots & smart-service regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT vehicle servicing mandates & standards

- 3.4.3.2 India- Emerging automotive service & connectivity regulations

- 3.4.3.3 Japan- ITS connect & certified service policies

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Digital service booking platforms

- 3.7.1.2 AI-powered diagnostic systems

- 3.7.2 Emerging technologies

- 3.7.2.1 Predictive maintenance technologies

- 3.7.2.2 EV service technologies & infrastructure

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Service pricing models

- 3.9.2 Labor cost trends

- 3.9.3 Parts markup analysis

- 3.9.4 Competitive pricing strategies

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Vehicle fleet demographics & age analysis

- 3.12.1 Global vehicle parc statistics

- 3.12.2 Average vehicle age trends

- 3.12.3 Impact on service demand

- 3.13 Unit Economics & Service Center Profitability Benchmarking

- 3.14 EV Impact on Authorized Service Business Models

- 3.15 Digital Customer Journey & Experience Benchmarking

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hatchbacks

- 5.3 SUVs

- 5.4 Sedan

Chapter 6 Market Estimates & Forecast, By Vehicles Age, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Less than 3 years

- 6.3 More than 3 years

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 HEV/PHEV

- 7.4 EVs

Chapter 8 Market Estimates & Forecast, By Service, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Engine

- 8.3 Transmission

- 8.4 Brakes

- 8.5 Suspension

- 8.6 Electrical

- 8.7 Body

- 8.8 Tire

- 8.9 Belts & accessories

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Service Providers, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 OEM authorized service centers

- 9.3 Multi-brand service centers

- 9.4 Independent garages

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Individual customers

- 10.3 Fleet operators

- 10.4 Corporate customers

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 3M

- 12.1.2 BMW

- 12.1.3 Castrol

- 12.1.4 Ford Motor

- 12.1.5 General Motors

- 12.1.6 Groupe Renault

- 12.1.7 Honda Motor

- 12.1.8 Hyundai Motor

- 12.1.9 Mercedes-Benz

- 12.1.10 Mobivia

- 12.1.11 Robert Bosch

- 12.1.12 Stellantis

- 12.1.13 Suzuki Motor

- 12.1.14 Toyota Motor

- 12.1.15 Volkswagen

- 12.2 Regional Players

- 12.2.1 Automovill Technologies

- 12.2.2 Carxpert Garage

- 12.2.3 Lansdowne Automobile

- 12.2.4 Mahindra First Choice

- 12.2.5 Meineke Car Care Centers

- 12.2.6 Mobil1 Car Care

- 12.2.7 TVS Automobile Solutions

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 GoMechanic

- 12.3.2 Wrench

- 12.3.3 YourMechanic

汽车共乘市场:依预订类型、车辆类型、应用程式和使用者类型划分-2026-2032年全球市场预测

汽车共乘市场:依预订类型、车辆类型、应用程式和使用者类型划分-2026-2032年全球市场预测 2026年全球汽车品质服务市场报告2026年全球汽车服务市场报告2026年全球共乘市场报告汽车即服务市场:2026-2032年全球市场预测(依服务模式、车辆类型、燃料类型及客户类型划分)汽车服务市场:2026-2032年全球市场预测(依服务类型、客户群、价格范围、车辆类型和销售管道)2026年全球认证汽车服务中心市场报告

2026年全球汽车品质服务市场报告2026年全球汽车服务市场报告2026年全球共乘市场报告汽车即服务市场:2026-2032年全球市场预测(依服务模式、车辆类型、燃料类型及客户类型划分)汽车服务市场:2026-2032年全球市场预测(依服务类型、客户群、价格范围、车辆类型和销售管道)2026年全球认证汽车服务中心市场报告 全球汽车品质服务市场:市场规模、份额和趋势分析(按车辆类型、检测类型、应用、最终用途和地区划分),细分市场预测(2026-2033 年)全球捲帘钢製服务门市场按操作方式、材料、门类型、应用、最终用途和分销渠道分類的预测(2026-2032年)

全球汽车品质服务市场:市场规模、份额和趋势分析(按车辆类型、检测类型、应用、最终用途和地区划分),细分市场预测(2026-2033 年)全球捲帘钢製服务门市场按操作方式、材料、门类型、应用、最终用途和分销渠道分類的预测(2026-2032年) 美国汽车服务:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)

美国汽车服务:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)