|

市场调查报告书

商品编码

1939708

美国汽车服务:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)United States Automotive Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

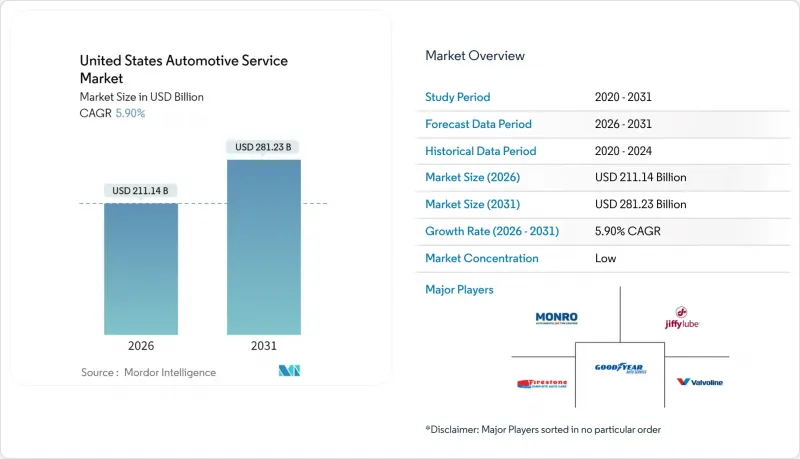

美国汽车服务市场预计到 2026 年价值将达到 2,111.4 亿美元,高于 2025 年的 1993.8 亿美元,预计到 2031 年将达到 2,812.3 亿美元。

预计2026年至2031年年复合成长率(CAGR)为5.9%。

强劲的需求主要源自于美国车辆老化(平均车龄12.6年)、里程回收以及轻型商用车利用率的提高,这些因素共同推动了对汽车服务的需求。加速电气化进程增加了维修的复杂性和单位成本,降低了定期保养的频率,同时也促使服务提供者提昇技师技能并投资高压工具。数位化预约平台、订阅式保养套餐以及「维修权」立法的推出正在重塑竞争格局,而行动按需服务也越来越受到都市区消费者的青睐。这些因素共同推动了美国汽车服务市场的持续收入成长和营运转型。

美国汽车服务市场趋势与洞察

车龄超过12.6年

到2024年,车辆平均车龄将达到12.6年,这将带来结构性利好,其中6-14年车龄的车辆将成为服务市场的主要用户群。新车价格上涨至4.5万美元以上,加上库存短缺,导致车辆使用週期延长,更多车主选择进行必要的保养而非更换。预计2021年至2024年间,混合动力汽车的註册量将成长181%,为未来的电池更换收入奠定基础。在2021年的经济復苏期间,独立维修店获得了约45%的新增服务支出,显示该细分市场的吸引力。高利率强化了消费者对车辆耐用性的关注,即使在经济放缓时期,也能支撑稳定的零件更换需求。

新冠疫情里程恢復

根据美国联邦公路管理局的数据,2024年2月全美公路行驶里程达到2,748亿英里,年增1.4%,已完全恢復到疫情前水准。预计到2050年,长途货车行驶里程将以每年1.1%的速度成长,而单体货车运作预计将以每年1.9%的速度成长,这将进一步增加对商用车辆车队维修的需求。行驶里程的增加加速了老旧车辆的磨损,从而推高了对煞车、轮胎和油液服务的需求。随着疫情后驾驶需求的激增,每周行驶里程趋势已成为衡量维修车间运作的关键指标。每加仑2.85美元的相对稳定的汽油价格支撑了人们的出行,而不断增长的消费者信贷余额也持续将新车购买预算转向售后服务。

电动车的普及将减少定期维护的频率。

电动车所需的机械油和皮带更少,从而减少了定期检查的频率。然而,由于电池和电子系统的复杂性,电动车的平均维修成本比内燃机汽车高出约 50%。与动力传动系统无关的维修工作,例如轮胎和挡风玻璃雨刷,仍将保持强劲势头,但到 2035 年,传统的售后市场可能会萎缩。只有一小部分技术人员接受过完整的电动车培训,这造成了技能缺口,有利于那些能够投资高压安全设备的大型连锁店和经销商集团。虽然到 2024 年,具备电动车维修能力的独立维修店将占据相当大的市场份额,但其中超过一半的维修店缺乏宣传自身专业技术的营销。

细分市场分析

到2025年,乘用车将占美国汽车服务市场的68.74%,该细分市场车辆数量庞大,需要持续维护。随着车辆平均车龄超过12年以及混合动力汽车日益普及,美国乘用车相关的汽车服务市场规模预计将稳定成长。受电子商务和最后一公里配送需求的推动,轻型商用车预计将以8.55%的复合年增长率增长至2031年,这将迫使维修店重新评估其产能规划和零件库存策略。

车队营运商现在会签订预防性维护合同,以最大限度地减少停机时间,并便于预测煞车、轮胎和悬吊零件的订购。特斯拉计划在2024年开设70家新的服务中心,其中许多面积超过10万平方公尺,以满足乘用车和商用车领域日益增长的电动车需求。中型和重型卡车虽然销量较小,但由于严格的运转率要求和联邦安全法规推动了对专业服务的需求,因此仍然是一个盈利的细分市场。

机械维修和保养仍将是美国汽车服务市场的核心,到 2025 年将维持 42.67% 的收入份额。在 ADAS(高级驾驶辅助系统)日益普及的推动下,电气和电子相关工作预计到 2031 年将以 9.02% 的复合年增长率成长。

为了抓住这部分高利润业务,汽车修理厂正在投资扫描工具、校准框架和静态目标。复合材料车身结构使外部和结构维修更加稳定,但也更加复杂。快修连锁店正在拓展业务范围,涉足电池、轮胎和轻型维护等领域,以弥补电动车更长的换油週期,并维持客户到店量。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 平均车龄超过12.6年的老旧车辆数量增加

- 感染疾病后的哩程恢復

- 拓展OEM品牌售后服务计划

- 数位预订系统和客户关係管理平台的兴起

- 订阅维护套餐

- 州级维修权立法进展

- 市场限制

- 由于电动车的普及,常规维护频率降低

- 工程师严重短缺推高了人事费用。

- 因通货膨胀而推迟非必要维修。

- OEM车用资讯系统让客户留在经销商处

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 买方和消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和大型卡车

- 按服务类型

- 机器维修保养

- 外观和结构(车身/油漆/玻璃)

- 电气和电子设备

- 快速保养(机油、润滑油、滤清器)

- 透过装置

- 胎

- 电池

- 座椅和内装部件

- ADAS感测器和摄影机

- 透过服务管道

- 授权OEM经销商

- 独立综合维修店

- 快速润滑和轮胎防滑链

- 行动/按需服务

- 按美国人口普查区域划分

- 东北

- 中西部

- 南部

- 西

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Firestone Complete Auto Care

- Jiffy Lube International Inc.

- Meineke Car Care Centers

- Midas International

- Monro Inc.

- Safelite Group

- Walmart Auto Care Centers

- Pep Boys

- Valvoline Instant Oil Change

- Goodyear Auto Service

- NTB-National Tire & Battery

- Christian Brothers Automotive

- Take 5 Oil Change

- Express Oil Change & Tire Engineers

- Caliber Collision

- Gerber Collision & Glass

- Service King Collision

- Tesla Service Centers

- CarMax Auto Care

- AAA Car Care Centers

第七章 市场机会与未来展望

The United States automotive service market size in 2026 is estimated at USD 211.14 billion, growing from 2025 value of USD 199.38 billion with 2031 projections showing USD 281.23 billion, growing at 5.9% CAGR over 2026-2031.

Robust demand comes from an aging national vehicle fleet that averages 12.6 years, a rebound in vehicle miles traveled, and rising light commercial vehicle utilization that intensifies service requirements. Accelerating electrification lifts repair complexity and ticket values, even lowering routine maintenance frequency, prompting providers to invest in technician upskilling and high-voltage tooling. Digital booking platforms, subscription-based maintenance bundles, and right-to-repair legislation are reshaping competitive strategies, while mobile on-demand services gain traction among urban consumers. Collectively, these forces position the US automotive service market for sustained revenue growth and operational transformation

United States Automotive Service Market Trends and Insights

Aging Vehicle Parc Surpassing 12.6 Years

Average vehicle age reached 12.6 years in 2024, creating a structural tailwind as units between six and fourteen years now form the largest service cohort. High new-vehicle prices above USD 45,000 and constrained inventories have extended ownership cycles, pushing more owners toward essential maintenance rather than replacement. Hybrid registrations swelled 181% from 2021 to 2024, setting the stage for future battery replacement revenue. Independent repair specialists captured nearly 45% of incremental service spend during the 2021 rebound, evidencing the segment's appeal. High interest rates reinforce consumer emphasis on longevity, anchoring steady parts replacement demand even during economic slowdowns.

Post-COVID Rebound in Vehicle Miles Traveled

Federal Highway Administration data show national VMT climbing 1.4% year-over-year to 274.8 billion miles in February 2024, fully matching pre-pandemic baselines. Long-haul truck mileage is projected to expand 1.1% annually through 2050, while single-unit truck activity may grow 1.9% per year, reinforcing commercial fleet maintenance needs. Higher miles intensify wear across an aging vehicle mix, boosting brake, tire, and fluid service demand. As post-pandemic driving surges, weekly mileage trends emerge as a key indicator for workshop activity. Relatively stable gasoline at USD 2.85 per gallon supports sustained travel, and rising consumer credit balances continue to divert budgets from new-car purchases toward aftermarket services.

EV Adoption Lowers Routine Service Intensity

Electric vehicles require fewer mechanical fluids and belts, trimming routine visits, yet each repair averages almost 50% higher than on an internal-combustion model, mainly due to battery and electronic complexity. Powertrain-agnostic work, such as tires and wiper blades, remains resilient, but the conventional aftermarket could contract by 2035. Only some of technicians report substantial EV training, generating a skills gap that favors large chains and dealer groups capable of funding high-voltage safety infrastructure. Independent shops servicing BEVs claimed a significant share in 2024, yet over half lack dedicated marketing to showcase that capability.

Other drivers and restraints analyzed in the detailed report include:

- OEM-Branded After-Sales Program Expansion

- Digital Booking and CRM Platforms Proliferation

- OEM Telematics Locking Customers into Dealerships

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars accounted for 68.74% of the US automotive service market in 2025 as the segment's large installed base demanded consistent maintenance. The US automotive service market size linked to passenger cars is projected to grow steadily as the average age surpasses 12 years and hybrid penetration deepens. Light commercial vehicles, buoyed by e-commerce and last-mile delivery, are set to record the fastest 8.55% CAGR through 2031, reshaping shop capacity planning and parts inventory strategies.

Fleet operators now specify preventative maintenance contracts that minimize downtime, driving predictable parts ordering for brakes, tires, and suspension. Tesla opened seventy new service centers in 2024, many exceeding 100,000 square feet, to cater to rising EV volume across both passenger and commercial segments. Medium and heavy trucks, though smaller in count, remain lucrative due to stringent uptime requirements and federal safety regulations that drive specialized service demand.

Mechanical repair and maintenance retained a 42.67% revenue share in 2025, anchoring the US automotive service market. Electrical and electronics work is forecast to grow at a 9.02% CAGR as ADAS penetration rises by 2031.

Shops invest in scan tools, calibration frames, and static targets to capture this margin-rich business. Due to mixed-material body structures, exterior and structural repairs remain stable yet more complex. Quick-lube chains diversify into battery, tire, and light mechanical jobs to offset longer EV oil-change intervals, preserving customer frequency.

The United States Automotive Services Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Service Type (Mechanical Repair and Maintenance, and More), Equipment Type (Tires, Batteries, and More), Service Channel (OEM Dealerships, Independent General Repair Shops, and More), and by U. S. Census Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Firestone Complete Auto Care

- Jiffy Lube International Inc.

- Meineke Car Care Centers

- Midas International

- Monro Inc.

- Safelite Group

- Walmart Auto Care Centers

- Pep Boys

- Valvoline Instant Oil Change

- Goodyear Auto Service

- NTB - National Tire & Battery

- Christian Brothers Automotive

- Take 5 Oil Change

- Express Oil Change & Tire Engineers

- Caliber Collision

- Gerber Collision & Glass

- Service King Collision

- Tesla Service Centers

- CarMax Auto Care

- AAA Car Care Centers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Vehicle Parc Surpassing 12.6 Years

- 4.2.2 Post-COVID Rebound in Vehicle Miles Travelled

- 4.2.3 OEM-Branded After-Sales Program Expansion

- 4.2.4 Digital Booking and CRM Platforms Proliferation

- 4.2.5 Subscription-Based Maintenance Bundles

- 4.2.6 State-Level Right-To-Repair Legislation Momentum

- 4.3 Market Restraints

- 4.3.1 EV Adoption Lowers Routine Service Intensity

- 4.3.2 Acute Technician Shortage Inflates Labor Costs

- 4.3.3 Inflation-Driven Deferral of Discretionary Repairs

- 4.3.4 OEM Telematics Locking Customers into Dealerships

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium & Heavy Trucks

- 5.2 By Service Type

- 5.2.1 Mechanical Repair & Maintenance

- 5.2.2 Exterior & Structural (Body / Paint / Glass)

- 5.2.3 Electrical & Electronics

- 5.2.4 Quick Services (Oil, Fluids, Filters)

- 5.3 By Equipment Type

- 5.3.1 Tires

- 5.3.2 Batteries

- 5.3.3 Seats & Interiors

- 5.3.4 ADAS Sensors & Cameras

- 5.4 By Service Channel

- 5.4.1 OEM Dealerships

- 5.4.2 Independent General Repair Shops

- 5.4.3 Quick-Lube & Tire Chains

- 5.4.4 Mobile / On-Demand Services

- 5.5 By U.S. Census Region

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Firestone Complete Auto Care

- 6.4.2 Jiffy Lube International Inc.

- 6.4.3 Meineke Car Care Centers

- 6.4.4 Midas International

- 6.4.5 Monro Inc.

- 6.4.6 Safelite Group

- 6.4.7 Walmart Auto Care Centers

- 6.4.8 Pep Boys

- 6.4.9 Valvoline Instant Oil Change

- 6.4.10 Goodyear Auto Service

- 6.4.11 NTB - National Tire & Battery

- 6.4.12 Christian Brothers Automotive

- 6.4.13 Take 5 Oil Change

- 6.4.14 Express Oil Change & Tire Engineers

- 6.4.15 Caliber Collision

- 6.4.16 Gerber Collision & Glass

- 6.4.17 Service King Collision

- 6.4.18 Tesla Service Centers

- 6.4.19 CarMax Auto Care

- 6.4.20 AAA Car Care Centers

7 Market Opportunities & Future Outlook

汽车共乘市场:依预订类型、车辆类型、应用程式和使用者类型划分-2026-2032年全球市场预测

汽车共乘市场:依预订类型、车辆类型、应用程式和使用者类型划分-2026-2032年全球市场预测 2026年全球汽车品质服务市场报告2026年全球汽车服务市场报告2026年全球共乘市场报告汽车即服务市场:2026-2032年全球市场预测(依服务模式、车辆类型、燃料类型及客户类型划分)汽车服务市场:2026-2032年全球市场预测(依服务类型、客户群、价格范围、车辆类型和销售管道)2026年全球认证汽车服务中心市场报告

2026年全球汽车品质服务市场报告2026年全球汽车服务市场报告2026年全球共乘市场报告汽车即服务市场:2026-2032年全球市场预测(依服务模式、车辆类型、燃料类型及客户类型划分)汽车服务市场:2026-2032年全球市场预测(依服务类型、客户群、价格范围、车辆类型和销售管道)2026年全球认证汽车服务中心市场报告 全球汽车品质服务市场:市场规模、份额和趋势分析(按车辆类型、检测类型、应用、最终用途和地区划分),细分市场预测(2026-2033 年)全球捲帘钢製服务门市场按操作方式、材料、门类型、应用、最终用途和分销渠道分類的预测(2026-2032年)

全球汽车品质服务市场:市场规模、份额和趋势分析(按车辆类型、检测类型、应用、最终用途和地区划分),细分市场预测(2026-2033 年)全球捲帘钢製服务门市场按操作方式、材料、门类型、应用、最终用途和分销渠道分類的预测(2026-2032年) 2026 年至 2035 年授权汽车服务中心的市场机会、成长要素、产业趋势分析与预测。

2026 年至 2035 年授权汽车服务中心的市场机会、成长要素、产业趋势分析与预测。