|

市场调查报告书

商品编码

1982296

汽车煞车皮市场机会、成长要素、产业趋势分析及2026-2035年预测Automotive Brake Pads Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

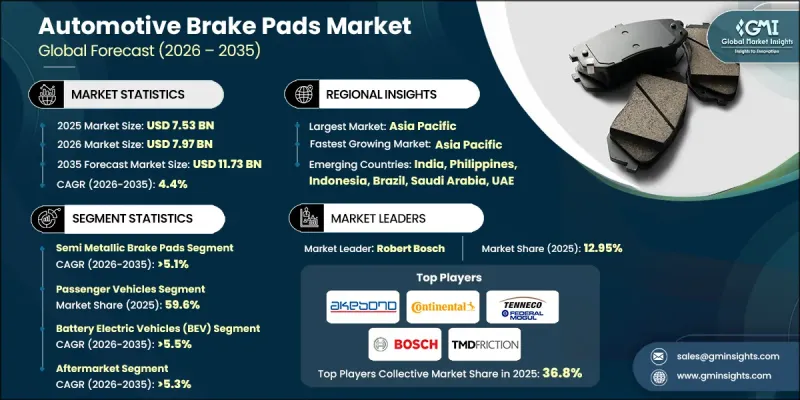

预计到 2025 年,全球汽车煞车皮市场价值将达到 75.3 亿美元,年复合成长率为 4.4%,到 2035 年将达到 117.3 亿美元。

汽车製造技术的不断发展、日益严格的安全标准以及电气化进程的快速推进,正在重新定义煞车皮的角色,使其从单纯的替换零件转变为至关重要的安全和性能部件。如今,煞车皮与乘用车、商用车和电动车的车辆能源效率标准、排放气体目标以及先进的煞车技术紧密相连。全球车辆数量的成长、车辆平均车龄的增加以及车辆使用週期的延长,都推动了售后市场的稳定需求。消费者和车队管理者越来越重视煞车片的耐用性、低噪音、低煞车粉尘排放以及与电子控制煞车系统的兼容性。这种转变反映了一种以生命週期为中心的维护理念,不仅关注初始购买价格,更强调煞车可靠性、安全保障和优化整体拥有成本。同时,摩擦材料工程的进步正在重新定义产品差异化和长期竞争力。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 75.3亿美元 |

| 预计金额 | 117.3亿美元 |

| 复合年增长率 | 4.4% |

摩擦材料的创新不断推动汽车煞车皮产业的变革。半金属、低金属NAO、陶瓷和无铜配方正变得越来越普遍,尤其是在环境法规日益严格的已开发国家。製造商正致力于研发轻量化复合结构、热稳定性化合物和低排放摩擦技术,以在严苛的工况下维持煞车性能,同时满足严格的监管标准。因此,煞车皮的设计不再仅限于普通的消耗品,而是日益成为高性能零件。

预计到2025年,半金属煞车皮片市占率将达到36.4%,并在2035年之前以5.1%的复合年增长率成长。其强大的市场地位得益于卓越的耐用性、高效的散热性能以及在高负载、高速工况下稳定的煞车性能。这些煞车片采用金属成分和摩擦改良剂混合製成,具有可靠的煞车力道和经济性,使其适用于各种在严苛驾驶条件下运行的车辆。

预计到2025年,乘用车市占率将达到59.6%,并在2026年至2035年间以3.9%的复合年增长率成长。全球乘用车市场规模庞大,定期维护保养是其市场主导地位的主要支撑因素。车辆高利用率、都市区拥塞和通勤时间延长加剧了煞车片的磨损,从而支撑了整车製造商和售后市场的需求。新兴市场可支配收入的成长和汽车保有量的增加进一步巩固了其长期成长前景。

中国汽车煞车皮市场占65.52%的全球份额,预计2025年市场规模将达到21亿美元。中国市场的强劲表现得益于庞大的汽车保有量和稳定的汽车生产。城市基础设施的不断完善、中等收入家庭的增加以及货运量的成长,都促使车辆使用频率的提高,进而缩短了煞车片的更换週期。作为世界领先的汽车製造地之一,中国也显着推动了整车厂对摩擦零件的需求。国内製造商受益于完善的供应链网路、具竞争力的生产成本和强大的出口能力,使其在国内和国际市场都占据了稳固的地位。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球汽车保有量增加以及乘用车车队老化加剧了这个问题。

- 有关车辆安全和煞车性能的规定越来越严格。

- 对优质陶瓷和低金属煞车皮的需求不断增长

- 商用车使用量的增加是由物流和电子商务的成长所推动的。

- 产业潜在风险与挑战

- 电动车再生煞车的影响

- 原物料价格波动

- 市场机会

- 电动车专用耐腐蚀煞车皮配方的研发正在不断扩展。

- 对不含铜且符合环保标准的煞车材料的需求激增。

- 新兴国家汽车拥有量增加

- 煞车系统与ADAS和电子控制稳定性控制技术的整合取得了进展。

- 促进因素

- 成长潜力分析

- 北美洲

- 美国:关于无铜煞车皮的法规(加州、华盛顿州)

- 加拿大:煞车摩擦材料环境标准(加拿大运输部)

- 欧洲

- 德国:符合报废车辆指令 (ELV) 和 EcoBrake 标准

- 英国:煞车皮材料环境指南,车辆年检安全标准

- 法国:低排放煞车皮法规(铜和重金属)

- 义大利:符合车辆安全和煞车材料标准(符合PNIEC标准)

- 亚太地区

- 中国:煞车摩擦材料环境标准、重金属法规

- 印度:FAME II 与煞车效率和安全标准的一致性

- 日本:JIS煞车皮标准与环保摩擦材料指南

- 澳洲:符合州级汽车煞车材料安全和环境法规。

- 拉丁美洲

- 巴西:国家汽车安全和煞车材料法规(CONTRAN)

- 墨西哥:汽车摩擦材料环境指南

- 阿根廷:煞车部件安全和环境合规计划

- 中东和非洲

- 阿联酋:车辆安全和煞车材料标准(与ADDM/DEWA标准一致)

- 3.4.5.2. 沙乌地阿拉伯:煞车零件的品质和安全法规(SASO 标准)

- 3.4.5.3. 南非:绿色交通战略与煞车材料环境指南

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 价格分析

- 按地区

- 依材料类型

- 生产统计

- 生产基地

- 消费中心

- 进出口

- 成本細項分析

- 永续性和环境影响分析

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 具有环保意识的倡议

- 碳足迹考量

- 未来展望与机会

- 主要贸易路线及关税的影响

- 美中贸易趋势

- 欧盟内部市场贸易

- 亚太地区的贸易

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- 预测性维护和磨损监测

- 供应链优化

- 品管和缺陷检测

- 按细分市场分類的生成式人工智慧用例和部署蓝图

- 材料设计与模拟(OEM研发)

- 客户服务自动化(售后市场)

- 需求预测与库存管理

- 风险、限制和监管考量

- 资料隐私和安全问题

- 人工智慧模型的可靠性和检验

- 对劳动力和所需技能的影响

- 利用人工智慧改造现有经营模式

- 投资与资金筹措分析

- 私募股权和创业投资的趋势

- 併购趋势与策略整合

- 政府资助和研发津贴

第四章 竞争情势

- 介绍

- 企业市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估计与预测:依材料划分,2022-2035年

- 半金属煞车皮

- 不含石棉的有机(NAO)煞车皮

- 低金属含量NAO煞车皮

- 陶瓷煞车皮

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 轿车/旅行车

- SUV(运动型多用途车)

- 掀背车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 摩托车

第七章 市场估计与预测:依驱动因素划分,2022-2035年

- 内燃机(ICE)

- 混合动力电动车(HEV)

- 电池式电动车(BEV)

第八章 市场估算与预测:依销售管道划分,2022-2035年

- OEM

- 售后市场

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 比利时

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Aisin

- Akebono Brake Industry

- Brembo

- Continental

- Tenneco

- Hitachi Astemo

- Nisshinbo

- Robert Bosch

- TMD Friction

- ZF Friedrichshafen

- 当地公司

- Advics

- Brake Parts(BPI)

- Delphi Technologies

- Fras-le

- Knorr-Bremse

- Miba(Friction)

- MK Kashiyama

- Sangsin Brake

- 新兴企业

- Hardron Motor Parts

- Shandong Aotai Electric

- Shandong Gold Phoenix

- TVS

The Global Automotive Brake Pads Market was valued at USD 7.53 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 11.73 billion by 2035.

The ongoing evolution of vehicle manufacturing, tightening safety mandates, and rapid electrification trends are redefining brake pads from basic replacement parts into essential safety and performance components. Brake pads are now closely aligned with vehicle efficiency standards, emission control targets, and advanced braking technologies across passenger cars, commercial fleets, and electric vehicles. A growing global vehicle fleet, rising average vehicle age, and longer ownership cycles are reinforcing consistent aftermarket demand. Consumers and fleet managers are increasingly prioritizing durability, reduced noise levels, lower brake dust emissions, and compatibility with electronic braking architectures. This shift reflects a lifecycle-focused maintenance approach that emphasizes braking reliability, safety assurance, and optimized total cost of ownership rather than solely initial purchase price. At the same time, advancements in friction material engineering are reshaping product differentiation and long-term competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.53 Billion |

| Forecast Value | $11.73 Billion |

| CAGR | 4.4% |

Innovation in friction materials continues to transform the automotive brake pads industry. Semi-metallic, low-metallic NAO, ceramic, and copper-free formulations are gaining wider adoption as environmental policies become more stringent, particularly across developed economies. Manufacturers are investing in lightweight composite structures, enhanced thermal stability compounds, and low-emission friction technologies to comply with regulatory standards while sustaining braking performance under demanding operating conditions. As a result, brake pads are increasingly engineered as high-performance components rather than standardized wear items.

The semi-metallic brake pads segment held 36.4% share in 2025 and is projected to grow at a CAGR of 5.1% through 2035. Their strong market position is supported by superior durability, efficient heat dissipation, and consistent braking output under high-load and high-speed environments. These pads, manufactured using blended metallic content combined with friction modifiers, deliver reliable stopping power and cost efficiency, making them suitable across a broad range of vehicle categories operating in intensive driving conditions.

The passenger vehicles segment accounted for 59.6% share in 2025 and is expected to grow at a CAGR of 3.9% between 2026 and 2035. The dominance of this segment is driven by the scale of global passenger car ownership and recurring replacement cycles linked to routine maintenance. High vehicle utilization rates, urban traffic congestion, and extended commuting distances contribute to accelerated brake wear, sustaining both OEM and aftermarket demand. Growing disposable incomes and expanding vehicle ownership across emerging economies are further strengthening long-term growth prospects.

China Automotive Brake Pads Market held 65.52% share, generating USD 2.1 billion in 2025. The country's strong performance is supported by its extensive vehicle base and consistent automotive production output. Expanding urban infrastructure, rising middle-income households, and increasing freight movement are elevating vehicle usage intensity, which shortens brake replacement intervals. As a leading global automotive manufacturing center, China also drives substantial OEM demand for friction components. Domestic producers benefit from integrated supply networks, competitive production costs, and robust export capabilities, enabling strong participation in both domestic and international markets.

Key companies operating in the Global Automotive Brake Pads Market include Brembo, Robert Bosch, Akebono Brake Industry, ZF Friedrichshafen, Continental, Tenneco, Hitachi Astemo, TMD Friction, Delphi Technologies, and Knorr-Bremse. Companies in the automotive brake pads market are reinforcing their competitive position through material innovation, strategic OEM partnerships, and global distribution expansion. Manufacturers are investing in advanced friction formulations, lightweight designs, and environmentally compliant compounds to meet evolving emission and safety standards. Strengthening long-term supply agreements with automakers ensures stable revenue streams and early integration into new vehicle platforms. Many players are expanding aftermarket networks to capture recurring replacement demand while enhancing brand visibility. Capacity expansion in high-growth regions improves cost efficiency and supply responsiveness.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material Type

- 2.2.3 Vehicle

- 2.2.4 Sales Channel

- 2.2.5 Propulsion

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global vehicle parc and aging passenger car fleet

- 3.2.1.2 Surge in stringent vehicle safety and braking performance regulations

- 3.2.1.3 Increase in demand for premium ceramic and low-metallic brake pads

- 3.2.1.4 Rise in commercial vehicle utilization driven by logistics and e-commerce expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Impact of Regenerative Braking in EVs

- 3.2.2.2 Raw Material Price Volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in development of EV-specific and corrosion-resistant brake pad formulations

- 3.2.3.2 Surge in demand for copper-free and environmentally compliant brake materials

- 3.2.3.3 Increase in vehicle ownership across emerging economies

- 3.2.3.4 Rise in integration of brake systems with ADAS and electronic stability technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 North America

- 3.3.1.1 U.S.: Copper-Free Brake Pad Regulations (California, Washington)

- 3.3.1.2 Canada: Brake Friction Material Environmental Standards (Transport Canada)

- 3.3.2 Europe

- 3.3.2.1 Germany: End-of-Life Vehicle (ELV) Directive Compliance, EcoBrake Standards

- 3.3.2.2 UK: Brake Pad Material Environmental Guidelines, MOT Vehicle Safety Standards

- 3.3.2.3 France: Low Emission Brake Pad Regulations (Copper and Heavy Metals)

- 3.3.2.4 Italy: Vehicle Safety & Brake Material Compliance (PNIEC Alignment)

- 3.3.3 Asia Pacific

- 3.3.3.1 China: Brake Friction Material Environmental Standards, Heavy Metal Restrictions

- 3.3.3.2 India: FAME II Alignment with Brake Efficiency & Safety Standards

- 3.3.3.3 Japan: JIS Brake Pad Standards & Eco-Friendly Friction Material Guidelines

- 3.3.3.4 Australia: State-Level Vehicle Brake Material Safety & Environmental Compliance

- 3.3.4 Latin America

- 3.3.4.1 Brazil: National Vehicle Safety & Brake Material Regulations (CONTRAN)

- 3.3.4.2 Mexico: Environmental Guidelines for Friction Materials in Vehicles

- 3.3.4.3 Argentina: Brake Component Safety & Environmental Compliance Programs

- 3.3.5 MEA

- 3.3.5.1 UAE: Vehicle Safety and Brake Material Standards (ADDM/DEWA Alignment)

- 3.3.5.2 3.4.5.2. Saudi Arabia: Brake Component Quality and Safety Regulations (SASO Standards)

- 3.3.5.3 3.4.5.3. South Africa: Green Transport Strategy and Brake Material Environmental Guidelines

- 3.3.1 North America

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Pricing Analysis

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Key Trade corridors & tariff impact

- 3.13.1 US-china trade dynamics

- 3.13.2 EU internal market trade

- 3.13.3 Asia-pacific regional trade

- 3.14 Impact of AI & Generative AI on the Market

- 3.14.1 AI-driven disruption of existing business models

- 3.14.1.1 Predictive maintenance & wear monitoring

- 3.14.1.2 Supply chain optimization

- 3.14.1.3 Quality control & defect detection

- 3.14.2 GenAI use cases & adoption roadmap by segment

- 3.14.2.1 Material design & simulation (OEM R&D)

- 3.14.2.2 Customer service automation (aftermarket)

- 3.14.2.3 Demand forecasting & inventory management

- 3.14.3 Risks, limitations & regulatory considerations

- 3.14.3.1 Data privacy & security concerns

- 3.14.3.2 AI model reliability & validation

- 3.14.3.3 Workforce impact & skill requirements

- 3.14.1 AI-driven disruption of existing business models

- 3.15 Investment & funding analysis

- 3.15.1 Private equity & venture capital activity

- 3.15.2 M&A trends & strategic consolidations

- 3.15.3 Government funding & R&D grants

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Semi-Metallic Brake Pads

- 5.3 Non-Asbestos Organic (NAO) Brake Pads

- 5.4 Low-Metallic NAO Brake Pads

- 5.5 Ceramic Brake Pads

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 Sedan/Wagon

- 6.2.2 SUV (Sport Utility Vehicle)

- 6.2.3 Hatchback

- 6.3 Commercial Vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Medium Commercial Vehicles (MCV)

- 6.3.3 Heavy Commercial Vehicles (HCV)

- 6.4 Two-Wheeler

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Hybrid Electric Vehicles (HEV)

- 7.4 Battery Electric Vehicles (BEV)

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aisin

- 10.1.2 Akebono Brake Industry

- 10.1.3 Brembo

- 10.1.4 Continental

- 10.1.5 Tenneco

- 10.1.6 Hitachi Astemo

- 10.1.7 Nisshinbo

- 10.1.8 Robert Bosch

- 10.1.9 TMD Friction

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 Advics

- 10.2.2 Brake Parts (BPI)

- 10.2.3 Delphi Technologies

- 10.2.4 Fras-le

- 10.2.5 Knorr-Bremse

- 10.2.6 Miba (Friction)

- 10.2.7 MK Kashiyama

- 10.2.8 Sangsin Brake

- 10.3 Emerging players

- 10.3.1 Hardron Motor Parts

- 10.3.2 Shandong Aotai Electric

- 10.3.3 Shandong Gold Phoenix

- 10.3.4 TVS

2026年全球汽车煞车皮市场报告

2026年全球汽车煞车皮市场报告 电动汽车煞车皮市场:2026-2032年全球市场预测(依煞车皮类型、摩擦材料类型、车辆类型、应用和销售管道)煞车皮市场:按煞车皮类型、材质、车辆类型和销售管道-2026-2032年全球预测烧结石墨船市场:依最终用途、材料等级、形状、製造流程、温度范围、船体尺寸划分,全球预测(2026-2032年)

电动汽车煞车皮市场:2026-2032年全球市场预测(依煞车皮类型、摩擦材料类型、车辆类型、应用和销售管道)煞车皮市场:按煞车皮类型、材质、车辆类型和销售管道-2026-2032年全球预测烧结石墨船市场:依最终用途、材料等级、形状、製造流程、温度范围、船体尺寸划分,全球预测(2026-2032年) 汽车煞车皮市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年

汽车煞车皮市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年 汽车煞车皮:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球煞车皮市场规模、份额、趋势和成长分析报告(2026-2034年)烧结煞车皮全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车煞车皮:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球煞车皮市场规模、份额、趋势和成长分析报告(2026-2034年)烧结煞车皮全球市场规模、份额、趋势和成长分析报告(2026-2034) 烧结煞车皮市场-全球产业规模、份额、趋势、机会和预测:按材料成分、车辆类型、分销管道、地区和竞争格局划分,2021-2031年

烧结煞车皮市场-全球产业规模、份额、趋势、机会和预测:按材料成分、车辆类型、分销管道、地区和竞争格局划分,2021-2031年 2026-2030年全球汽车煞车皮市场

2026-2030年全球汽车煞车皮市场