|

市场调查报告书

商品编码

1940788

汽车煞车皮:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Brake Pad - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

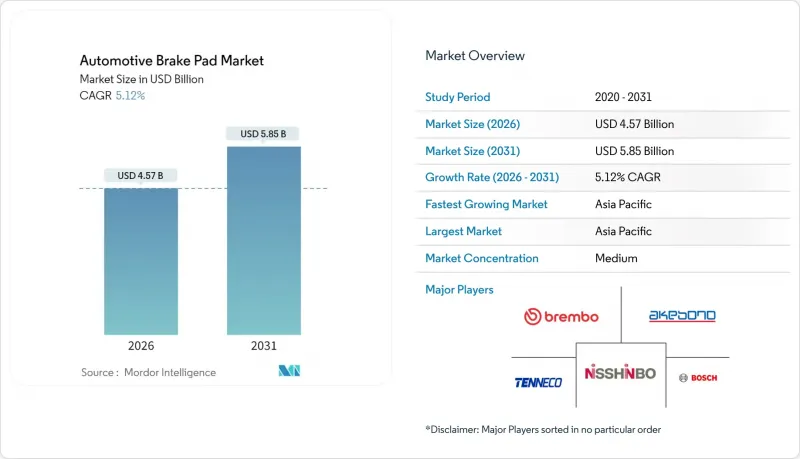

汽车煞车皮市场预计将从 2025 年的 43.5 亿美元成长到 2026 年的 45.7 亿美元,预计到 2031 年将达到 58.5 亿美元,2026 年至 2031 年的复合年增长率为 5.12%。

这项稳定扩张得益于日益严格的全球排放气体法规、电动车数量的成长以及摩擦材料科学的进步,这些进步在不影响煞车安全性的前提下减少了颗粒物排放。亚太地区强大的製造业基础、取代零件管道向电子商务的转型以及客户对低噪音陶瓷复合材料的需求,都在推动该行业的进一步成长。同时,钢材和酚醛树脂供应链的不稳定性正在挤压利润空间,促使製造商投资于流程自动化和人工智慧驱动的配方工具。随着高端品牌将磨损感测器和软体整合到煞车片中,并将预测性维护服务建立在新的收入来源之上,竞争压力也不断加剧。

全球汽车煞车皮市场趋势与洞察

更严格的安全法规(欧7、国7)

欧盟7排放标准将把煞车颗粒物排放限制在7毫克/公里以内,并强制规定自2025年起,煞车片中铜的含量低于0.5%(重量比),这将使传统的酚醛-铜混合煞车片被淘汰。中国也正在製定与欧盟标准相符的法规,旨在为全球两大汽车市场建立统一的合规标准。率先获得无铜认证的製造商将获得明显的销售优势,而未能获得认证的製造商则将面临高成本高昂的配方变更和生产线停产。这些法规正在加速陶瓷和无机(NAO)材料的应用,迫使原始设备製造商(OEM)在全球平台上实现摩擦片的标准化。美国的先例,例如加州于2025年生效的“更佳煞车规则”,显示州级措施如何迅速波及整个国家供应链。

无铜低排放焊盘材料的快速普及

原始设备製造商 (OEM) 和一级供应商正将无铜化合物定位为性能提升手段,而非仅仅作为合规工具。 Brembo 的水泥基复合材料「眼镜蛇计划」获得了 ECE-R90 认证,同时消除了甲醛并减少了 20% 的颗粒物排放。陶瓷纤维和改性酚醛树脂的结合,可实现更安静的煞车和更清洁的轮毂,这对于无法像传统汽车那样被引擎噪音掩盖的电动车车主来说尤其重要。生产转型导致特殊酰胺纤维和玻璃纤维供应短缺,进而引发了选择性现货定价和供应商审核的加强。模具改造(高温压平机和更高的混合精度)需要数百万美元的资本投资,但对于需要更高价格煞车片的高阶车型而言,这些投资可以迅速收回成本。

再生煞车可降低更换频率

纯电动轿车车主享有一项显着优势:煞车皮更换频率远低于传统车辆。由于能量回收煞车系统,电动轿车车主在首次更换煞车皮前通常行驶里程是传统车辆的两倍以上,凸显了该系统的高效性和低磨损性。较短的保养週期会降低每辆车的售后市场收入;然而,特殊的耐腐蚀涂层会增加每组煞车片的单价。车队营运商会延长服务合约并推迟批量采购,这给供应商的订单前景带来了不确定性。销售量下滑将首先影响区域分销商,迫使他们整合业务或将业务转向其他易耗件,例如轮胎和挡风玻璃雨刷。

细分市场分析

到2025年,半金属煞车片将占据汽车煞车皮市场最大份额,达到46.34%。铁粉和铜粉因其在高速煞车过程中高效的散热性能而继续受到青睐。同时,受铜粉禁用法规和消费者对低粉尘轮毂需求的推动,陶瓷复合材料预计到2031年将以5.68%的复合年增长率成长。这种成长在价格弹性较高的豪华SUV和高性能轿车领域尤其显着。

陶瓷煞车片的广泛应用仍面临诸多障碍:原料成本高、需要专用窑炉、需要供应商有限的细粒氧化铝粉末。然而,像 Brembo 这样的製造商已经证明,无铜陶瓷煞车片能够保持良好的抗热衰减性能,使其应用范围超越了小众跑车领域。在拉丁美洲和非洲,由于初始价格高于耐用性,无石棉有机煞车片仍应用于低成本车辆。在所有车型类别中,半金属煞车片对于重型卡车仍然至关重要,因为目前还没有任何陶瓷混合物能够在不大幅改进煞车碟盘的情况下达到其热性能。

到2025年,前轮煞车片总成将占汽车煞车皮市场规模的65.10%,这反映了车辆前轴承受的物理载重不断增加的趋势。电子煞车力道分配系统和先进的稳定性控制系统将更多的煞车力道传递至后轴,导致后轮煞车片损耗率更高。预计到2031年,这将推动后轮煞车片细分市场的复合年增长率达到5.98%。汽车製造商正在为后轮煞车系统配备更先进的卡钳,以支援弯道行驶时的软体控制扭力向量分配。

在混合动力汽车和电动车车型中,工程师们越来越多地在后轮上安装再生製动电机,以便在电池电量低时选择性地启动后轮液压煞车。此变更会影响后煞车片的耐热性能,因此需要采用耐腐蚀涂层以延长煞车间隔。售后维修店也相应地调整了库存比例,订购的后煞车片数量比过去十年都要多,以避免维修延误。

区域分析

预计到2025年,亚太地区将占据全球汽车煞车皮市场47.80%的份额,并在2031年之前以5.75%的复合年增长率持续成长。这主要得益于中国、印度和东南亚国协不断扩大汽车生产规模并培育供应商群。中国从欧盟6标准过渡到欧7标准,需要采用无铜生产方式,这给国内煞车片製造商带来了挑战和机会。印度摩托车产业的蓬勃发展推动了拥有一体化铸造和复合材料生产设施的本土蓝筹企业的成长,降低了对进口的依赖。日本和韩国企业正在推进陶瓷和酰胺纤维技术的尖端发展,并将其专业知识输出到区域子公司。

在北美,车辆平均车龄较长,成熟的替换市场支撑着稳定的售后市场收入。加州和华盛顿州的铜禁令促使供应商早期进行投资,如今这些投资已在全国获得回报。随着墨西哥扩大汽车组装线,美墨加协定(USMCA)鼓励区域采购的关税规则意味着大量零件在地采购。加拿大和美国北部各州严酷的冬季气候促进了对耐腐蚀背板和耐盐蚀分层的特殊低温黏合剂的需求。

欧洲在监管方面处于领先地位,其製定的欧7标准确地立了限制颗粒物排放的全球标准。德国豪华品牌在陶瓷材料的应用方面处于领先地位,而义大利和西班牙的供应商则在摩托车和高性能汽车领域表现出色。儘管外汇波动和能源价格飙升推高了生产成本,但欧盟的团结弥补了跨境监管的复杂性,使得零件能够从波兰自由流通到葡萄牙。由于劳动力成本低廉且拥有符合欧盟标准的品管体系,东欧工厂正越来越多地赢得新的煞车皮合约。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 更严格的安全法规(例如欧7、国7)

- 快速采用无铜低排放焊盘材料

- 售后市场电子商务在煞车零件领域的渗透率

- 电动车的NVH和腐蚀设计要求

- 人工智慧驱动的垫片配方优化和虚拟测试

- 对嵌入式煞车片磨损和状态感测器的需求日益增长

- 市场限制

- 因热裂纹失效导致产品召回的风险

- 原料(钢材、树脂)价格波动所导致的价格压力

- 再生煞车可降低更换频率

- 无铜原料的供应链能力有限

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额)

- 依材料类型

- 半金属

- 非石棉有机物 (NAO)

- 低金属NAO

- 陶瓷製品

- 按位置

- 正面

- 后部

- 按销售管道

- 汽车製造商(OEM)

- 售后市场

- 按车辆类型

- 搭乘用车

- 轻型商用车(LCV)

- 重型商用车(HCV)

- 摩托车

- 依推进类型

- 内燃机车辆

- 油电混合车

- 电池式电动车

- 地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 卡达

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Brembo NV

- Robert Bosch GmbH

- Tenneco Inc.(Ferodo)

- ZF Friedrichshafen AG(TRW)

- Akebono Brake Industry Co.

- Continental AG

- ITT Inc.(ITT Motion Technologies)

- Nisshinbo Holdings Inc.

- Fras-le SA

- ADVICS Co., Ltd.

- Federal-Mogul Holdings LLC

- EBC Brakes

- Sangsin Brake

- Carlisle Brake & Friction

- Gold Phoenix Brake Tech.

- Mando Corporation

- Garrett Motion Inc.

- Belmont Rubber Pvt. Ltd.

第七章 市场机会与未来展望

The automotive brake pad market is expected to grow from USD 4.35 billion in 2025 to USD 4.57 billion in 2026 and is forecast to reach USD 5.85 billion by 2031 at 5.12% CAGR over 2026-2031.

This steady expansion is anchored in stricter global emission rules, growing electrified-vehicle volumes, and advances in friction-material science that lower particulate output without sacrificing braking safety. Asia-Pacific's manufacturing depth, the shift to e-commerce in the replacement parts channel, and customer demand for low-noise ceramic compounds add further momentum. At the same time, supply-chain volatility in steel and phenolic resins squeezes margins, prompting makers to invest in process automation and AI-driven formulation tools. Competitive pressure rises as premium brands embed wear sensors and software into pads, underpinning predictive-maintenance services that create new revenue streams.

Global Automotive Brake Pad Market Trends and Insights

Surging Safety-Regulation Stringency (Euro 7, China 7)

Euro 7 rules cap brake particulate emissions at 7 mg/km from 2025 and force copper content below 0.5% by weight, making legacy phenolic-copper blends obsolete . China is drafting parallel limits that mirror the EU threshold, creating a unified compliance bar across the two largest vehicle markets. Makers that completed copper-free validation early now enjoy a clear sales edge, whereas late movers face costly reformulation and line downtime. The rule set accelerates ceramic and NAO adoption, pushing OEMs to standardize friction packs across global platforms. U.S. precedents such as California's "Better Brake Rule," in force since 2025, underscore how state-level action can quickly spread to nationwide supply chains.

Rapid Copper-Free and Low-Emission Pad Material Adoption

OEMs and tier-one suppliers now treat copper-free compounds as performance upgrades, not compliance tools. Brembo's cement-matrix "Project Cobra" won ECE-R90 approval while eliminating formaldehyde and cutting fine particulates by 20% . Ceramic fibers paired with modified phenolic alternatives enable quieter stops and cleaner wheels, which are prized by EV owners whose cabins lack engine masking noise. Production transitions have strained sourcing of specialized aramid and glass fibers, leading to selective spot pricing and tighter supplier audits. Tooling changes-higher-temperature presses and finer mixing tolerances-require multi-million-dollar capex, but the payback arrives quickly in premium models that command higher pad prices.

Regenerative Braking Reducing Replacement Frequency

Drivers of battery electric sedans enjoy a notable advantage: they replace their brake pads far less frequently than those in conventional vehicles. Thanks to regenerative braking systems, electric sedan drivers can typically go over twice the distance before their first brake pad change, underscoring the system's efficiency and reduced wear. Fewer service intervals shrink aftermarket revenue per vehicle, although each pad set sells at a higher unit price due to specialized corrosion coatings. Fleet operators extend service contracts longer, deferring large-lot pad purchases, which softens order visibility for suppliers. Volume declines hit regional distributors first, forcing consolidation or shifts into other wear parts such as tires and wiper blades.

Other drivers and restraints analyzed in the detailed report include:

- Electrified-Vehicle NVH and Corrosion Design Requirements

- Aftermarket E-Commerce Penetration in Brake Parts

- Product-Recall Risk from Thermal-Cracking Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Semi-metallic pads generated the most significant slice with 46.34% of the automotive brake pad market size in 2025. They remain popular because iron and copper shavings dissipate heat efficiently during repeated high-speed stops. Ceramic compounds, however, are advancing at a 5.68% CAGR through 2031 thanks to copper bans and consumer demand for low-dust wheels. This growth is most visible in premium SUVs and performance sedans with higher price elasticity.

Ceramic uptake faces hurdles: higher raw-material costs, different curing ovens, and the need for fine-grained alumina powders that only a few suppliers provide. Nonetheless, makers like Brembo demonstrated that copper-free ceramics can retain fade resistance, expanding potential beyond niche sports cars. Non-asbestos organic pads continue to serve budget cars in Latin America and Africa, where upfront price trumps longevity. Across all groups, semi-metallic will remain vital for heavy-duty trucks because no ceramic blend yet matches its thermal capacity without significant rotor upgrades.

Front assemblies held 65.10% of the automotive brake pad market size in 2025, reflecting physics-driven front-axle loading. Electronic brake-force distribution and advanced stability programs now redirect more stopping energy to the rear axle, elevating rear-pad wear rates and pushing that subsegment's 5.98% CAGR through 2031. Automakers equip rear brakes with more sophisticated calipers to support software-controlled torque vectoring in curves.

In hybrid and EV models, engineers often mount regenerative motors on rear wheels, selectively using rear hydraulic brakes when batteries are near complete. This switch changes heat profiles, requiring corrosion-resistant coatings on rear pads, which now sit idle longer between stops. Aftermarket workshops adjust stocking ratios accordingly, ordering higher rear-pad volumes than in the past decade to avoid service delays.

The Automotive Brake Pad Market Report is Segmented by Material Type (Semi-Metallic, Non-Asbestos Organic, Low-Metallic NAO, and Ceramic), Position (Front and Rear), Sales Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, and More), Propulsion Type (ICE, Hybrid, and Battery Electric), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the automotive brake pad market with a 47.80% share in 2025, growing at a CAGR of 5.75% through 2031, as China, India, and ASEAN nations scaled vehicle output and nurtured dense supplier clusters. China's transition from Euro 6 to Euro 7 standards compels rapid copper-free conversions, creating challenges and opportunities for domestic pad makers. India's two-wheeler boom channels growth to local champions integrating foundries and compound kitchens under one roof, reducing import reliance. Japanese and Korean firms push the frontier of ceramic and aramid fiber technology, exporting recipes to regional affiliates.

North America shows a mature replacement landscape where high vehicle age supports stable aftermarket revenue. State-level copper bans in California and Washington forced early supplier investments that now pay dividends nationwide. Mexico's expanding vehicle assembly lines source a significant volume of parts locally, thanks to USMCA tariff rules that favor regional content. Severe winters in Canada and northern states nurture demand for corrosion-proof back-plates and special low-temperature binders that resist salt-induced delamination.

Europe acts as a regulatory pacesetter, with Euro 7 setting the global template for particulate limits. Premium German marques pull ceramic adoption upward, while Italian and Spanish suppliers excel in motorcycle and performance sectors. Currency swings and energy-price shocks elevate production costs, yet EU cohesion offsets cross-border rule complexity, letting parts flow freely from Poland to Portugal. Eastern European plants increasingly win new pad contracts due to lower labor costs and EU-compliant quality regimes.

- Brembo N.V.

- Robert Bosch GmbH

- Tenneco Inc. (Ferodo)

- ZF Friedrichshafen AG (TRW)

- Akebono Brake Industry Co.

- Continental AG

- ITT Inc. (ITT Motion Technologies)

- Nisshinbo Holdings Inc.

- Fras-le SA

- ADVICS Co., Ltd.

- Federal-Mogul Holdings LLC

- EBC Brakes

- Sangsin Brake

- Carlisle Brake & Friction

- Gold Phoenix Brake Tech.

- Mando Corporation

- Garrett Motion Inc.

- Belmont Rubber Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Safety-Regulation Stringency (E.G., Euro 7, China 7)

- 4.2.2 Rapid Copper-Free and Low-Emission Pad Material Adoption

- 4.2.3 Aftermarket E-Commerce Penetration In Brake Parts

- 4.2.4 Electrified-Vehicle NVH and Corrosion Design Requirements

- 4.2.5 AI-Driven Pad-Formulation Optimization and Test Virtualization

- 4.2.6 Growing Demand for Embedded Pad-Wear/Condition Sensors

- 4.3 Market Restraints

- 4.3.1 Product-Recall Risk from Thermal-Cracking Failures

- 4.3.2 Price Pressure from Raw Materials (Steel, Resin) Volatility

- 4.3.3 Regenerative Braking Reducing Replacement Frequency

- 4.3.4 Limited Copper-Free Raw-Material Supply Chain Capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Material Type

- 5.1.1 Semi-metallic

- 5.1.2 Non-asbestos Organic (NAO)

- 5.1.3 Low-metallic NAO

- 5.1.4 Ceramic

- 5.2 By Position

- 5.2.1 Front

- 5.2.2 Rear

- 5.3 By Sales Channel

- 5.3.1 Original Equipment Manufacturers (OEM)

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles (LCV)

- 5.4.3 Heavy Commercial Vehicles (HCV)

- 5.4.4 Two-Wheelers

- 5.5 By Propulsion Type

- 5.5.1 Internal-Combustion Engine Vehicles

- 5.5.2 Hybrid Electric Vehicles

- 5.5.3 Battery-Electric Vehicles

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Qatar

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Brembo N.V.

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Tenneco Inc. (Ferodo)

- 6.4.4 ZF Friedrichshafen AG (TRW)

- 6.4.5 Akebono Brake Industry Co.

- 6.4.6 Continental AG

- 6.4.7 ITT Inc. (ITT Motion Technologies)

- 6.4.8 Nisshinbo Holdings Inc.

- 6.4.9 Fras-le SA

- 6.4.10 ADVICS Co., Ltd.

- 6.4.11 Federal-Mogul Holdings LLC

- 6.4.12 EBC Brakes

- 6.4.13 Sangsin Brake

- 6.4.14 Carlisle Brake & Friction

- 6.4.15 Gold Phoenix Brake Tech.

- 6.4.16 Mando Corporation

- 6.4.17 Garrett Motion Inc.

- 6.4.18 Belmont Rubber Pvt. Ltd.

7 Market Opportunities and Future Outlook

2026年全球汽车煞车皮市场报告

2026年全球汽车煞车皮市场报告 电动汽车煞车皮市场:2026-2032年全球市场预测(依煞车皮类型、摩擦材料类型、车辆类型、应用和销售管道)煞车皮市场:按煞车皮类型、材质、车辆类型和销售管道-2026-2032年全球预测烧结石墨船市场:依最终用途、材料等级、形状、製造流程、温度范围、船体尺寸划分,全球预测(2026-2032年)

电动汽车煞车皮市场:2026-2032年全球市场预测(依煞车皮类型、摩擦材料类型、车辆类型、应用和销售管道)煞车皮市场:按煞车皮类型、材质、车辆类型和销售管道-2026-2032年全球预测烧结石墨船市场:依最终用途、材料等级、形状、製造流程、温度范围、船体尺寸划分,全球预测(2026-2032年) 汽车煞车皮市场机会、成长要素、产业趋势分析及2026-2035年预测

汽车煞车皮市场机会、成长要素、产业趋势分析及2026-2035年预测 汽车煞车皮市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年全球煞车皮市场规模、份额、趋势和成长分析报告(2026-2034年)烧结煞车皮全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车煞车皮市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,预测2026-2034年全球煞车皮市场规模、份额、趋势和成长分析报告(2026-2034年)烧结煞车皮全球市场规模、份额、趋势和成长分析报告(2026-2034) 烧结煞车皮市场-全球产业规模、份额、趋势、机会和预测:按材料成分、车辆类型、分销管道、地区和竞争格局划分,2021-2031年

烧结煞车皮市场-全球产业规模、份额、趋势、机会和预测:按材料成分、车辆类型、分销管道、地区和竞争格局划分,2021-2031年 2026-2030年全球汽车煞车皮市场

2026-2030年全球汽车煞车皮市场