|

市场调查报告书

商品编码

1982297

静脉注射免疫球蛋白市场机会、成长要素、产业趋势分析及2026-2035年预测。Intravenous Immunoglobulin (IVIg) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

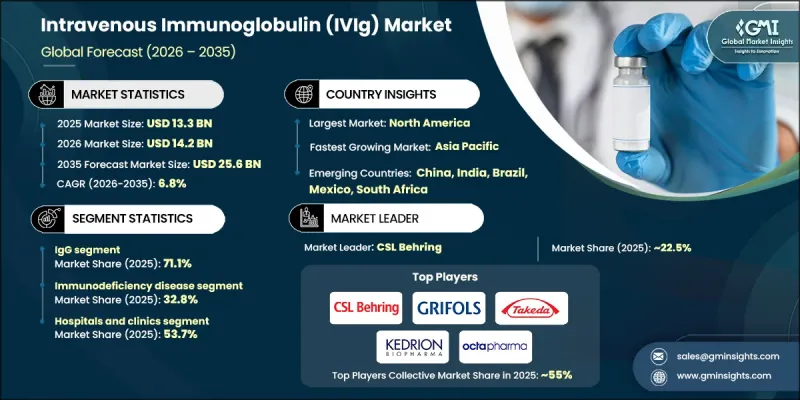

预计到 2025 年,全球静脉注射免疫球蛋白 (IVIg) 市值将达到 133 亿美元,并有望以 6.8% 的复合年增长率增长,到 2035 年达到 256 亿美元。

全球原发性和续发性免疫力缺乏率的不断上升是推动该市场成长的主要因素。静脉注射免疫球蛋白(IVIg)产品是由混合人类血浆製成的无菌浓缩抗体製剂,经由静脉输注给药,以提供被动免疫。它们透过提供现成的抗体来支持免疫系统,这些抗体可以中和有害病原体并调节免疫反应。 IVIg的治疗应用范围正在从原发性免疫力缺乏扩展到自体自体免疫疾病和神经系统疾病,例如慢性脱髓鞘多发性神经炎、Guillain-Barré二氏症候群和重症肌无力。为了满足全球需求,领先的生产商正在迅速扩大血浆采集中心,投资先进的血浆分离设备,并采取区域性血浆筹资策略。随着临床应用的不断增加和供应链的持续投资,静脉注射免疫球蛋白(IVIg)市场正处于强劲的成长轨道上。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 133亿美元 |

| 预测金额 | 256亿美元 |

| 复合年增长率 | 6.8% |

预计到2025年,IgG将占据71.1%的市场份额,这主要得益于其广泛的临床认可和在免疫防御中发挥的关键作用。 IgG是循环系统中最常见的免疫球蛋白,也是治疗原发性和续发性免疫力缺乏疾病的首选药物。其需求涵盖神经科、血液科和内科等多个专科,并有完善的法规和生产标准作为支撑。

预计到2025年,免疫不全症市场将占据32.8%的市场份额,并在2026年至2035年间以6.9%的复合年增长率增长。该市场包括原发性免疫力缺乏、续发性免疫力缺乏缺陷、低丙种球蛋白血症和某些抗体缺陷。由于这些疾病是终身慢性病,需要频繁注射静脉注射免疫球蛋白(IVIg),从而确保了市场需求的持续稳定。

预计到2025年,北美静脉注射免疫球蛋白(IVIg)市占率将达52.5%。这主要得益于该地区先进的医疗基础设施、自体免疫疾病和免疫不全症的高发生率、完善的保险报销体係以及成熟的血浆采集网络。此外,主要企业的存在、持续的临床研究以及创新治疗通讯协定的早期应用,也进一步提升了该地区市场的成熟度。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 免疫不全症盛行率增加

- 老年人口增加

- 血浆采集、分离和纯化技术的不断进步。

- 扩大静脉注射免疫球蛋白在神经系统疾病和自体免疫疾病的临床应用

- 增加免疫球蛋白的医疗保健支出

- 产业潜在风险与挑战

- 静脉注射免疫球蛋白疗法高成本

- 潜在的副作用和过敏反应

- 市场机会

- 重组免疫球蛋白的开发

- 新兴国家需求增加

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 技术进步

- 当前技术趋势

- 新兴技术

- 还款状态

- 未来市场趋势

- 管道分析

- 波特五力分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 合作伙伴关係和合资企业

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- IgG

- IgA

- IgM

- IgD

- IgE

第六章 市场估计与预测:依应用领域划分,2022-2035年

- 免疫不全症

- 原发性免疫力缺乏

- 次发性免疫力缺乏

- 低丙种球蛋白血症

- 特异性抗体缺乏症

- 慢性脱髓鞘多发性神经炎(CIDP)

- 重症肌无力

- 多灶性运动神经病变

- 特发性血小板减少紫斑症(ITP)

- 发炎性肌肉疾病

- Guillain-Barré二氏症候群

- 其他用途

第七章 市场估计与预测:依最终用途划分,2022-2035年

- 医院和诊所

- 门诊手术中心

- 居家医疗设施

- 其他最终用户

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- ADMA Biologics

- Baxter International

- Biotest

- CSL Behring

- China Biologics Products

- Grifols SA

- Intas Pharmaceuticals

- Kedrion Biopharma

- LFB Biotechnologies

- Omrix Biopharmaceuticals(Johnson & Johnson)

- Octapharma AG

- Pfizer

- Shanghai RAAS Blood Products

- Takeda Pharmaceutical Company

The Global Intravenous Immunoglobulin (IVIg) Market was valued at USD 13.3 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 25.6 billion by 2035.

The market is propelled by the rising incidence of both primary and secondary immunodeficiency disorders worldwide. IVIg products are sterile, concentrated antibody formulations derived from pooled human plasma, administered via intravenous infusion to provide passive immunity. They support the immune system by supplying ready-made antibodies that neutralize harmful pathogens and regulate immune responses. The therapeutic applications of IVIg have expanded beyond primary immunodeficiencies, increasingly addressing autoimmune and neurological disorders such as chronic inflammatory demyelinating polyneuropathy, Guillain-Barre syndrome, and myasthenia gravis. To meet global demand, leading manufacturers are rapidly expanding plasma collection centers, investing in advanced plasmapheresis equipment, and adopting regional plasma sourcing strategies. Increasing clinical adoption, combined with steady supply chain investments, is shaping a robust growth trajectory for the Intravenous Immunoglobulin (IVIg) Market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.3 Billion |

| Forecast Value | $25.6 Billion |

| CAGR | 6.8% |

The IgG segment held a 71.1% share in 2025, driven by its broad clinical acceptance and key role in immune defense. IgG is the most prevalent immunoglobulin in circulation, making it the preferred choice for treating both primary and secondary immunodeficiencies. Its demand spans multiple specialties, including neurology, hematology, and internal medicine, reinforced by well-established regulatory and manufacturing standards.

The immunodeficiency disease segment accounted for 32.8% share in 2025 and is expected to grow at a CAGR of 6.9% during 2026-2035. This segment encompasses primary immunodeficiencies, secondary immunodeficiencies, hypogammaglobulinemia, and specific antibody deficiencies. Lifelong and chronic in nature, these conditions require frequent IVIg infusions, ensuring sustained market demand.

North America Intravenous Immunoglobulin (IVIg) Market held 52.5% share in 2025, supported by advanced healthcare infrastructure, high prevalence of autoimmune and immunodeficiency disorders, robust reimbursement systems, and an established plasma collection network. The presence of leading pharmaceutical companies, ongoing clinical research, and early adoption of innovative treatment protocols further strengthen market maturity in the region.

Key players in the Global Intravenous Immunoglobulin (IVIg) Market include Baxter International, CSL Behring, Octapharma AG, Grifols SA, Pfizer, Takeda Pharmaceutical Company, ADMA Biologics, Biotest, China Biologics Products, Omrix Biopharmaceuticals (Johnson & Johnson), LFB Biotechnologies, Kedrion Biopharma, Intas Pharmaceuticals, and Shanghai RAAS Blood Products. To strengthen the Intravenous Immunoglobulin (IVIg) Market position, companies are focusing on expanding plasma collection and fractionation capacities, investing in state-of-the-art plasmapheresis equipment, and developing regional sourcing strategies to ensure a stable supply of raw materials. They are also diversifying their product portfolios to target autoimmune and neurological disorders, while optimizing manufacturing processes to reduce costs and enhance efficiency. Strategic partnerships with hospitals, specialty clinics, and healthcare networks expand distribution channels.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of immunodeficiency disorders

- 3.2.1.2 Increasing geriatric population

- 3.2.1.3 Growing advances in plasma collection, fractionation, and purification technologies

- 3.2.1.4 Rising clinical applications of IVIg in neurological and autoimmune disorders

- 3.2.1.5 Increasing healthcare expenditure for immunoglobulins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of IVIg therapy

- 3.2.2.2 Potential adverse effects and allergic reactions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recombinant immunoglobulins

- 3.2.3.2 Rising demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 IgG

- 5.3 IgA

- 5.4 IgM

- 5.5 IgD

- 5.6 IgE

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Immunodeficiency diseases

- 6.2.1 Primary immunodeficiencies

- 6.2.2 Secondary immunodeficiencies

- 6.2.3 Hypogammaglobulinemia

- 6.2.4 Specific antibody deficiency

- 6.3 Chronic Inflammatory demyelinating polyneuropathy (CIDP)

- 6.4 Myasthenia gravis

- 6.5 Multifocal motor neuropathy

- 6.6 Idiopathic thrombocytopenic purpura (ITP)

- 6.7 Inflammatory myopathies

- 6.8 Guillain-Barre syndrome

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADMA Biologics

- 9.2 Baxter International

- 9.3 Biotest

- 9.4 CSL Behring

- 9.5 China Biologics Products

- 9.6 Grifols SA

- 9.7 Intas Pharmaceuticals

- 9.8 Kedrion Biopharma

- 9.9 LFB Biotechnologies

- 9.10 Omrix Biopharmaceuticals (Johnson & Johnson)

- 9.11 Octapharma AG

- 9.12 Pfizer

- 9.13 Shanghai RAAS Blood Products

- 9.14 Takeda Pharmaceutical Company

免疫球蛋白市场规模、份额、趋势和预测:按产品、应用、给药途径和地区划分,2026-2034年

免疫球蛋白市场规模、份额、趋势和预测:按产品、应用、给药途径和地区划分,2026-2034年 免疫球蛋白市场规模、份额、成长及全球产业分析:按类型和应用划分,区域洞察及2026-2034年预测

免疫球蛋白市场规模、份额、成长及全球产业分析:按类型和应用划分,区域洞察及2026-2034年预测 IgE过敏血液检测市场:依检测类型、技术、应用、最终用户和通路划分-2026-2032年全球预测全球免疫球蛋白市场规模、份额、趋势和成长分析报告(2026-2034年)人类高免疫球蛋白市场按产品类型、给药途径、应用和最终用户划分-2026-2032年全球预测按给药途径、适应症、通路和最终用户分類的高免疫球蛋白产品市场—2026-2032年全球预测特异性IgE血液检测过敏检测市场(按检测类型、过敏原类型、过敏类型、应用和最终用户划分),全球预测,2026-2032年

IgE过敏血液检测市场:依检测类型、技术、应用、最终用户和通路划分-2026-2032年全球预测全球免疫球蛋白市场规模、份额、趋势和成长分析报告(2026-2034年)人类高免疫球蛋白市场按产品类型、给药途径、应用和最终用户划分-2026-2032年全球预测按给药途径、适应症、通路和最终用户分類的高免疫球蛋白产品市场—2026-2032年全球预测特异性IgE血液检测过敏检测市场(按检测类型、过敏原类型、过敏类型、应用和最终用户划分),全球预测,2026-2032年 免疫球蛋白市场规模、份额和成长分析(按产品类型、剂型、给药途径、应用、分销管道和地区划分)-2026-2033年产业预测

免疫球蛋白市场规模、份额和成长分析(按产品类型、剂型、给药途径、应用、分销管道和地区划分)-2026-2033年产业预测 免疫球蛋白市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

免疫球蛋白市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测