|

市场调查报告书

商品编码

1982299

工业突波保护设备市场:商机、成长要素、产业趋势分析及2026-2035年预测Industrial Surge Protection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

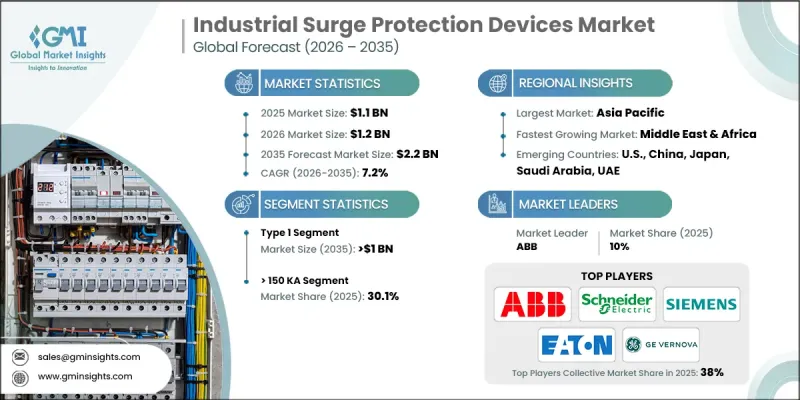

全球工业突波保护设备市场预计到 2025 年将达到 11 亿美元,并以 7.2% 的复合年增长率成长,到 2035 年达到 22 亿美元。

随着工业环境对复杂电子系统的依赖日益加深,对可靠突波保护解决方案的需求也显着成长。电网波动和天气因素导致的停电频率不断增加,加速了各行各业对突波保护产品的应用。同时,更严格的电气安全法规以及对IEC和UL突波保护标准的强制性要求也推动了市场需求。随着工业运作日益数位化,以及高度敏感的电力基础设施的部署,保护关键设备免受电压异常的影响已成为营运的首要任务。在工业设施中,最大限度地减少停机时间、防止资产损坏以及确保员工安全变得越来越重要。同时,电力基础设施的现代化以及向更互联的工业生态系统的转型,也为产业发展创造了有利的环境。此外,市场正朝着融合突波抑制、智慧监控和综合能源管理功能的先进整合解决方案发展,这进一步增强了产业的长期发展前景。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 11亿美元 |

| 预计金额 | 22亿美元 |

| 复合年增长率 | 7.2% |

工业突波保护装置在保护电气系统免受雷击、开关操作和电压突变引起的瞬态过电压损害方面发挥着至关重要的作用。这些系统透过将过电压从敏感元件转移开来,从而减少设备故障、运作中断和安全风险。在电力可靠性至关重要的工业环境中,突波保护对于保护马达、变压器和自动化控制系统等高价值资产至关重要。智慧电网基础设施的快速扩展和人们对电力弹性的日益重视预计将加速市场成长。製造商正越来越多地提供整合即时诊断和系统监控功能以及突波保护的多功能设备,以提高运作透明度。

预计2035年,I型工业突波保护器市场规模将达10亿美元。对保护重型工业设备免受高能量突波的需求日益增长,正在重塑市场竞争格局。这些设备广泛部署在服务入口点,以保护关键基础设施,并降低代价高昂的停机时间和安全隐患的发生机率。工业自动化技术的进步和工业IoT框架的扩展,正推动这些产品在各类设施中的广泛应用。

到2025年,额定电流超过150kA的设备将占据30.1%的市场。随着企业将严重电力故障的韧性放在首位,高容量突波保护设备正日益受到关注。企业越来越意识到预防突波相关损害的经济效益,因此增加对高额定保护系统的投资,以提高长期可靠性和业务连续性。

预计2025年,美国工业突波保护市场规模将达1.578亿美元。法规结构的不断完善和对运行安全标准的日益重视正在推动行业扩张。持续的基础设施升级、先进技术的广泛应用以及高灵敏度电子设备的日益普及是关键的成长要素。老化的电网和因天气原因导致的频繁停电进一步凸显了在整体工业应用中对可靠的突波保护系统的需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 生产能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 监理情势

- 成长潜力分析

- 价格趋势分析(美元/单位)

- 按地区

- 按产能

- 波特的分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 工业突波保护装置的成本结构分析

- 新机会与趋势

- 数位化和物联网集成

- 未开发市场和应用领域的成长

- 投资分析及未来展望

第四章 竞争情势

- 介绍

- 企业市占率分析:按地区划分

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场规模及预测:依产品划分,2022-2035年

- 硬布线

- 外挂

- 电源线

- 电源控制设备

第六章 市场规模及预测:依技术划分,2022-2035年

- 1型

- 类型 2

- 3型

第七章 市场规模及预测:依额定电流计算,2022-2035年

- 50千安或以下

- 超过 50 千安至 100 千安

- >100 kA~150 kA

- >150 kA

第八章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 西班牙

- 荷兰

- 奥地利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 马来西亚

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 南非

- 奈及利亚

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 秘鲁

- 阿根廷

第九章:公司简介

- ABB

- Belkin

- CAPE Electric

- CG Power and Industrial Solutions

- CITEL

- DEHN

- Eaton

- Emerson Electric

- GE Vernova

- Havells

- Hubbell

- Legrand

- Leviton Manufacturing

- Maxivolt

- Mersen

- nVent

- Phoenix Contact

- Prosurge

- Raycap

- Rockwell Automation

- Saltek

- Schneider Electric

- Siemens

- Socomec

- Weidmuller Electronics

The Global Industrial Surge Protection Devices Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 2.2 billion by 2035.

Growing dependence on advanced electronic systems across industrial environments is significantly increasing the need for reliable surge protection solutions. Rising incidents of grid fluctuations and weather-driven power disturbances are accelerating product adoption across multiple sectors. At the same time, stricter electrical safety mandates and compulsory compliance with IEC and UL surge protection standards are reinforcing demand. As industries continue to digitize operations and deploy sensitive electrical infrastructure, safeguarding mission-critical equipment from voltage irregularities has become a top operational priority. Industrial facilities are placing greater emphasis on minimizing downtime, preventing asset damage, and ensuring workforce safety. In parallel, modernization of power infrastructure and the transition toward more connected industrial ecosystems are creating favorable growth conditions. The market is also witnessing a shift toward advanced, integrated solutions that combine surge suppression with intelligent monitoring and broader energy management capabilities, further strengthening long-term industry prospects.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 7.2% |

Industrial surge protection devices play a crucial role in shielding electrical systems from transient overvoltage caused by lightning events, switching operations, and sudden power fluctuations. These systems function by diverting excess voltage away from sensitive components, reducing the risk of equipment failure, operational disruption, and safety hazards. In industrial settings where electrical reliability is essential, surge protection is vital to preserving high-value assets, including motors, transformers, and automated control systems. The rapid expansion of smart grid infrastructure and heightened awareness of electrical resilience are expected to accelerate market growth. Manufacturers are increasingly offering multifunctional devices that integrate surge protection with real-time diagnostics and system monitoring to enhance operational transparency.

The Type 1 industrial surge protection devices segment is forecast to reach USD 1 billion by 2035. Increasing demand to protect heavy-duty industrial equipment from high-energy surges is reshaping the competitive landscape. These devices are widely deployed at service entrances to secure critical infrastructure and reduce the likelihood of costly shutdowns or safety concerns. Growing industrial automation and the expansion of industrial IoT frameworks are contributing to stronger product penetration across diverse facilities.

The devices rated above 150 kA accounted for 30.1% share in 2025. High-capacity surge protection units are gaining traction as organizations prioritize resilience against severe electrical disturbances. Businesses are increasingly recognizing the financial advantages of preventing surge-related damage, prompting investment in higher-rated protection systems that enhance long-term reliability and operational continuity.

U.S. Industrial Surge Protection Devices Market reached USD 157.8 million in 2025. Strengthening regulatory frameworks and heightened focus on operational safety standards are reinforcing industry expansion. Ongoing infrastructure upgrades, wider adoption of advanced technologies, and increased deployment of sensitive electronic equipment are major growth drivers. Aging electrical networks and recurring weather-related power disruptions further underscore the necessity of robust surge protection systems across industrial applications.

Prominent companies operating in the Global Industrial Surge Protection Devices Market include Schneider Electric, ABB, Siemens, Eaton, Legrand, Phoenix Contact, Emerson Electric, Rockwell Automation, GE Vernova, Hubbell, Belkin, Raycap, Socomec, Mersen, Havells, Weidmuller Electronics, Prosurge, DEHN, CG Power and Industrial Solutions, CAPE Electric, Saltek, nVent, Leviton Manufacturing, CITEL, and Maxivolt. Companies in the industrial surge protection devices market are reinforcing their market foothold through continuous product innovation, regulatory alignment, and strategic collaborations. Manufacturers are investing in advanced surge suppression technologies, higher discharge capacity systems, and smart monitoring features to differentiate their portfolios. Expanding global distribution networks and strengthening partnerships with industrial contractors enhance market reach and customer engagement. Many players are focusing on certification compliance and adherence to evolving electrical safety standards to build credibility and trust. Localization of production facilities and supply chain optimization helps reduce lead times and operational costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates and forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Product trends

- 2.1.3 Technology trends

- 2.1.4 Power rating trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Regulatory landscape

- 3.4 Growth potential analysis

- 3.5 Price trend analysis (USD/Unit)

- 3.5.1 By region

- 3.5.2 By capacity

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

- 3.7.1 Political factors

- 3.7.2 Economic factors

- 3.7.3 Social factors

- 3.7.4 Technological factors

- 3.7.5 Legal factors

- 3.7.6 Environmental factors

- 3.8 Cost structure analysis of industrial surge protection devices

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Growth in untapped markets & applications

- 3.10 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Hard-wired

- 5.3 Plug-in

- 5.4 Line cord

- 5.5 Power control devices

Chapter 6 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Type 1

- 6.3 Type 2

- 6.4 Type 3

Chapter 7 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 ≤ 50 kA

- 7.3 > 50 kA to 100 kA

- 7.4 > 100 kA to 150 kA

- 7.5 > 150 kA

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 New Zealand

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Kuwait

- 8.5.8 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Belkin

- 9.3 CAPE Electric

- 9.4 CG Power and Industrial Solutions

- 9.5 CITEL

- 9.6 DEHN

- 9.7 Eaton

- 9.8 Emerson Electric

- 9.9 GE Vernova

- 9.10 Havells

- 9.11 Hubbell

- 9.12 Legrand

- 9.13 Leviton Manufacturing

- 9.14 Maxivolt

- 9.15 Mersen

- 9.16 nVent

- 9.17 Phoenix Contact

- 9.18 Prosurge

- 9.19 Raycap

- 9.20 Rockwell Automation

- 9.21 Saltek

- 9.22 Schneider Electric

- 9.23 Siemens

- 9.24 Socomec

- 9.25 Weidmuller Electronics

2026年全球瞬态保护装置市场报告

2026年全球瞬态保护装置市场报告 突波保护设备的全球市场(2025年):终端用户,用途,竞争企业:分析与预测

突波保护设备的全球市场(2025年):终端用户,用途,竞争企业:分析与预测 突波保护零组件的全球市场(2025年)- 终端用户,用途,竞争企业

突波保护零组件的全球市场(2025年)- 终端用户,用途,竞争企业 快速充电突波保护插座市场:依产品类型、通路、最终用途和应用划分-全球预测,2026-2032年

快速充电突波保护插座市场:依产品类型、通路、最终用途和应用划分-全球预测,2026-2032年 突波保护设备市场规模、份额、趋势和预测:按产品、类型、额定功率、最终用户和地区划分,2026-2034 年2026年全球突波保护设备市场报告

突波保护设备市场规模、份额、趋势和预测:按产品、类型、额定功率、最终用户和地区划分,2026-2034 年2026年全球突波保护设备市场报告 临时防护装置市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年突波保护器市场-全球产业规模、份额、趋势、机会与预测:按类型、功率范围、组件、最终用途、地区和竞争格局划分,2021-2031年

临时防护装置市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年突波保护器市场-全球产业规模、份额、趋势、机会与预测:按类型、功率范围、组件、最终用途、地区和竞争格局划分,2021-2031年 突波保护器市场机会、成长要素、产业趋势分析及2026年至2035年预测按类型、安装方式、相位、最终用途和分销管道突波的浪涌抑制器市场 - 全球预测 2026-2032

突波保护器市场机会、成长要素、产业趋势分析及2026年至2035年预测按类型、安装方式、相位、最终用途和分销管道突波的浪涌抑制器市场 - 全球预测 2026-2032