|

市场调查报告书

商品编码

1982348

摩托车配件市场:商机、成长要素、产业趋势分析及2026-2035年预测Motorcycle Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

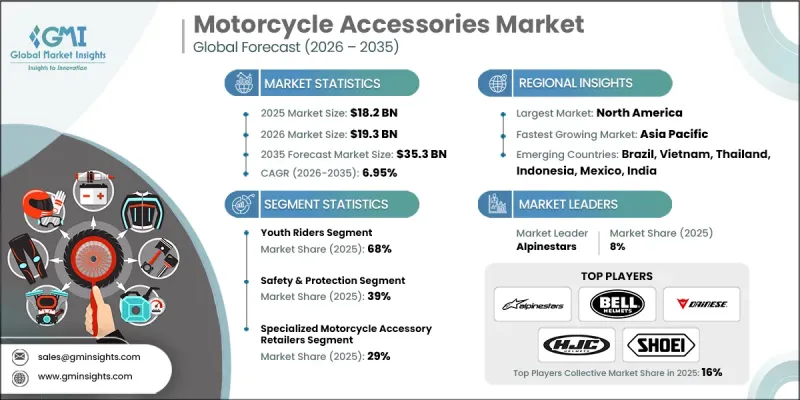

2025 年全球摩托车配件市场价值 182 亿美元,预计到 2035 年将达到 353 亿美元,年复合成长率为 6.95%。

摩托车配件显着提升了不同摩托车类型的骑乘安全性、车辆性能、舒适性和美观性。这些产品直接影响骑乘品质、设备耐用性、个人化客製选项以及尖端技术的整合。製造商正致力于研发高性能安全装备、互联电子设备和高端客製化产品,以满足不断变化的骑乘者需求。随着消费者偏好的演变,各大品牌纷纷引入先进材料、符合人体工学的设计以及整合数位功能,以提升安全性和骑乘效率。全球摩托车保有量的成长、可支配收入的增加以及人们对休閒日益增长的兴趣,都进一步推动了市场需求。个人化文化的盛行,以及长途旅行和探险旅行参与度的提高,持续推动市场的发展。此外,数位化零售通路的拓展扩大了产品供应范围,使骑乘者能够更有效率地比较不同产品的功能、价格和品牌。在持续创新和生活方式主导的需求推动下,摩托车配件正逐渐成为更广泛的强力运动生态系统中不可或缺的一部分。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 182亿美元 |

| 预测金额 | 353亿美元 |

| 复合年增长率 | 6.95% |

该市场涵盖多种产品系列,包括防护头盔、专业骑行服、储物系统、煞车部件、照明系统、性能提升部件、通讯工具和防盗解决方案。原厂配套 (OEM) 产品和售后市场产品均对总销售额贡献显着。技术进步正在推动智慧头盔、无线连接系统、导航设备、先进照明技术和性能提升部件的普及应用。这些创新提升了整体骑乘体验,增强了骑士的感知能力、连接性和运作可靠性。

预计到2025年,年轻骑士群将占据68%的市场份额,并在2026年至2035年间以7.1%的复合年增长率增长。由于年轻骑士积极的骑乘习惯和对创新产品的接受度,他们在摩托车配件消费中占据了很大比例。受数位媒体趋势和社区参与的影响,这群人对个人化和高级功能表现出浓厚的兴趣。可支配收入的成长和对摩托车文化的热情持续推动着这个细分市场的稳定消费。

预计到2025年,安全防护类产品将占据39%的市场份额,复合年增长率达7%。此细分市场涵盖专为最大限度降低受伤风险和提升骑乘者在各种路况下的安全而设计的装备。人们对道路安全标准的日益重视、监管措施的支持以及全球摩托车市场的不断扩张,都在推动对防护配件的需求。

美国摩托车配件市场预计在2026年至2035年间以6.3%的复合年增长率成长。消费者对高端骑乘装备的强劲需求、成熟的摩托车社群以及日益增长的旅行和探险骑行参与度,都将持续推动市场扩张。在美国营运的品牌正透过推出多层防护系统、空气动力学优化头盔以及适用于各种骑乘环境的连网配件,不断提升自身的技术实力。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球摩托车销售和拥有量增加

- 人们越来越关注骑行者的安全和保护。

- 可支配所得和个人消费的增加

- 摩托车旅游和探险骑行的激增

- 电子商务和线上分销管道的成长

- 客製化和个人化趋势

- 产业潜在风险与挑战

- 仿冒品仿冒品

- 奢华配件高成本

- 成熟市场摩托车销量下降

- 复杂的监管和认证要求

- 市场机会

- 电动汽车摩托车配件市场不断扩大

- 智慧互联配件的开发

- 渗透新兴市场

- 订阅式配件服务的成长

- 永续环保产品的创新

- 电动自行车市场发展迅速,需要对车架进行加固。

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 美国 - 摩托车配件安全法规

- 加拿大 - 安全合规框架

- 欧洲

- 德国 - 技术和品质认证标准

- 英国—脱欧后的合规要求

- 法国 - 行动安全认证

- 义大利—工业和交通运输整合标准

- 亚太地区

- 中国—汽车零件製造法规

- 印度 - 产品认证及符合安全标准

- 日本-先进的安全与品管标准

- 澳洲 - 消费者保护和产品品质标准

- 拉丁美洲

- 墨西哥 - 道路安全配件标准

- 阿根廷 - 交通安全法规

- 中东和非洲

- 南非-遵守道路交通安全法规

- 沙乌地阿拉伯 - 出行安全措施

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 感测器技术的发展(摄影机、光达、雷达、超音波)

- 整合感测器融合

- 人工智慧和机器学习在行人侦测的应用

- 新兴技术

- V2X 通讯可提高侦测能力

- 夜间和弱光侦测技术

- 当前技术趋势

- 专利趋势(基于初步调查)

- 投资与资金筹措分析

- 创投创业投资

- 主要企业在研发方面的投资

- 价格分析(基于初步调查)

- 对过去价格趋势的分析

- 按业务类型分類的定价策略

- 贸易数据分析(基于初步调查)

- 进出口量及进口额趋势

- 主要贸易路线及关税的影响

- 人工智慧和生成式人工智慧对市场的影响(基于初步研究)

- 利用人工智慧改造现有经营模式

- GenAI 各细分市场的应用案例与部署蓝图

- 风险、局限性和监管考量

- 使用案例和成功案例

- 案例研究

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

- 生产能力和生产趋势(基于初步调查)

- 按地区和主要生产商分類的设备产能

- 运转率和扩张计划

- 预测假设和情境分析(基于初步研究)

- 基本案例-驱动复合年增长率的关键宏观经济与产业变量

- 看涨情景-向上修正的前提条件与触发条件

- 看跌情景-下调的假设与风险因素

- 敏感度分析-最容易预测的变数。

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲(MEA)

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 主要进展

- 併购

- 伙伴关係和联盟

- 新产品发布

- 业务拓展计划及资金筹措

- 企业级分层基准测试

- 层级分类标准与选择标准

- 按收入、地区和创新能力分類的层级定位矩阵。

第五章 市场估价与预测:依产品划分,2022-2035年

- 安全设备

- 防护装备

- 性能部件

- 加工配件

- 行李箱和储物用品

- 电子配件

- 服饰及相关产品

- 保养和护理产品

- 舒适和便利

第六章 市场估价与预测:依车辆类型划分,2022-2035年

- 巡洋舰

- 运动摩托车

- 标准型/通勤自行车

- 越野/探险摩托车

- Scooter

第七章 市场估算与预测:光达年龄组,2022-2035年

- 年轻骑手

- 成人骑士

- 高级骑士

第八章 市场估算与预测:依销售管道划分,2022-2035年

- 摩托车配件专卖店

- 授权零售商

- 线上/电子商务平台

- 独立零售店

- 超级市场和大卖场

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 安全/防护

- 性能提升

- 舒适和便利

- 风格和外观定制

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 瑞典

- 丹麦

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 以色列

第十一章:公司简介

- 世界公司

- Alpinestars

- Bell Helmets

- Brembo

- Cardo

- Fox Racing

- Garmin

- Givi

- GoPro

- Icon

- Shoei

- 本地球员

- Airhawk

- Arlen Ness

- Corbin

- Dynojet

- Kryptonite

- Nelson-Rigg

- Roland Sands Design(RSD)

- Saddlemen

- Speed and Strength

- 新兴企业和技术基础设施公司

- Xena

The Global Motorcycle Accessories Market was valued at USD 18.2 billion in 2025 and is estimated to grow at a CAGR of 6.95% to reach USD 35.3 billion by 2035.

Motorcycle accessories significantly enhance rider safety, vehicle performance, comfort, and visual appeal across multiple bike categories. These products directly influence riding quality, equipment durability, personalization options, and integration of modern technology. Manufacturers are placing strong emphasis on high-performance safety equipment, connected electronics, and premium customization offerings to align with shifting rider expectations. As consumer preferences evolve, brands are introducing advanced materials, ergonomic designs, and integrated digital features that improve protection and riding efficiency. Expanding global motorcycle ownership, rising disposable income levels, and growing interest in recreational riding are further supporting demand. The market continues to benefit from increasing participation in long-distance touring and adventure-oriented travel, alongside a strong culture of personalization. Additionally, digital retail channels are broadening product access, enabling riders to compare features, pricing, and brands more efficiently. Continuous innovation and lifestyle-driven demand are positioning motorcycle accessories as a critical component of the broader powersports ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $18.2 Billion |

| Forecast Value | $35.3 Billion |

| CAGR | 6.95% |

The market spans a diverse product portfolio, including protective headgear, technical riding apparel, storage systems, braking components, illumination systems, performance upgrades, communication tools, and anti-theft solutions. Both original equipment manufacturer offerings and aftermarket products contribute substantially to overall revenue. Technological progress is driving the adoption of intelligent headgear, wireless connectivity systems, navigation-enabled devices, advanced lighting technologies, and performance-enhancing components. These innovations improve rider awareness, connectivity, and operational reliability while enhancing overall riding functionality.

The youth riders segment accounted for 68% share in 2025 and is forecast to grow at a CAGR of 7.1% between 2026 and 2035. Younger riders represent a significant portion of accessory spending, supported by active riding habits and openness to innovation. This demographic demonstrates a strong interest in personalization and advanced features, often influenced by digital media trends and community engagement. Higher discretionary income and enthusiasm for motorcycling culture continue to drive consistent purchasing within this segment.

The safety and protection category held 39% share in 2025 and is expanding at a CAGR of 7%. This segment includes gear specifically designed to minimize injury risk and improve rider security in various conditions. Increasing awareness regarding road safety standards, supportive regulatory measures, and rising global two-wheeler adoption are reinforcing demand for protective accessories.

United States Motorcycle Accessories Market is projected to grow at a CAGR of 6.3% from 2026 to 2035. Strong consumer demand for premium riding equipment, a well-established motorcycling community, and growing participation in touring and adventure riding continue to support expansion. Brands operating in the U.S. are advancing engineering capabilities by introducing multi-layer protective systems, aerodynamically optimized headgear, and connectivity-enabled accessories suited for diverse riding environments.

Key players operating in the Global Motorcycle Accessories Market include Shoei, Alpinestars, Brembo, Cardo, Givi, Fox Racing, Garmin, Bell Helmets, Icon, and GoPro. These companies compete through innovation in safety engineering, material technology, performance optimization, and digital integration. Companies in the Motorcycle Accessories Market are strengthening their competitive position by investing in advanced protective technologies, lightweight materials, and smart connectivity features. Many brands are expanding premium product lines while maintaining accessible pricing tiers to reach diverse rider segments. Strategic collaborations with motorcycle manufacturers and motorsport communities enhance product credibility and brand visibility. Firms are also leveraging e-commerce growth, direct-to-consumer platforms, and data-driven marketing to increase global reach. Continuous research into aerodynamics, impact resistance, and wearable technology improves product differentiation.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Rider Age

- 2.2.5 Sales Channel

- 2.2.6 Usage

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global motorcycle sales and ownership

- 3.2.1.2 Growing emphasis on rider safety and protection

- 3.2.1.3 Increasing disposable income and consumer spending

- 3.2.1.4 Surge in motorcycle tourism and adventure riding

- 3.2.1.5 Growth of e-commerce and online distribution channels

- 3.2.1.6 Rising trends in customization and personalization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of counterfeit and low-quality products

- 3.2.2.2 High cost of premium accessories

- 3.2.2.3 Declining motorcycle sales in mature markets

- 3.2.2.4 Complex regulatory and certification requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of the electric motorcycle accessories market

- 3.2.3.2 Development of smart and connected accessories

- 3.2.3.3 Penetration into emerging markets

- 3.2.3.4 Growth of subscription-based accessory services

- 3.2.3.5 Innovation in sustainable and eco-friendly products

- 3.2.3.6 Growing e-bike segment requiring reinforced frames.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Motorcycle accessory safety regulations

- 3.4.1.2 Canada - Safety compliance framework

- 3.4.2 Europe

- 3.4.2.1 Germany- Technical and quality certification standards

- 3.4.2.2 UK- Post-Brexit compliance requirements

- 3.4.2.3 France- Mobility safety certification

- 3.4.2.4 Italy- Industrial and mobility integration standards

- 3.4.3 Asia Pacific

- 3.4.3.1 China- Manufacturing and vehicle accessory regulations

- 3.4.3.2 India- Product certification and safety compliance

- 3.4.3.3 Japan- Advanced safety quality control standards

- 3.4.3.4 Australia- Consumer protection and product quality norms

- 3.4.4 LATAM

- 3.4.4.1 Mexico- Road safety accessory standards

- 3.4.4.2 Argentina- Traffic safety regulation

- 3.4.5 MEA

- 3.4.5.1 South Africa- Road safety compliance

- 3.4.5.2 Saudi Arabia- Mobility safety initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Sensor technology evolution (camera, LiDAR, RADAR, ultrasonic)

- 3.7.1.2 Sensor fusion & integration

- 3.7.1.3 AI & machine learning in pedestrian detection

- 3.7.2 Emerging technologies

- 3.7.2.1 V2X communication for enhanced detection

- 3.7.2.2 Nighttime & low-light detection technologies

- 3.7.1 Current technological trends

- 3.8 Patent landscape (Driven by Primary Research)

- 3.8.1 Investment and funding analysis

- 3.8.2 Venture capital investment trends

- 3.8.3 R&D investment by key players

- 3.9 Price analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export volume and value trends

- 3.10.2 Key trade corridors and tariff impact

- 3.11 Impact of AI and generative AI on the market (Driven by Primary Research)

- 3.11.1 AI-driven disruption of existing business models

- 3.11.2 GenAI use cases and adoption roadmap by segment

- 3.11.3 Risks, limitations and regulatory considerations

- 3.12 Use cases & success stories

- 3.13 Case studies

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Capacity & production landscape (Driven by Primary Research)

- 3.15.1 Installed capacity by region & key producer

- 3.15.2 Capacity utilization rates & expansion pipelines

- 3.16 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.16.1 Base Case - key macro & industry variables driving CAGR

- 3.16.2 Bull Scenario - upside assumptions & trigger conditions

- 3.16.3 Bear Scenario - downside assumptions & risk factors

- 3.16.4 Sensitivity Analysis - variables the forecast is most sensitive to

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Company tier benchmarking

- 4.7.1 Tier classification criteria and qualifying thresholds

- 4.7.2 Tier positioning matrix by revenue, geography, and innovation

Chapter 5 Market Estimates & Forecast, By Product, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Safety gear

- 5.3 Protective gear

- 5.4 Performance parts

- 5.5 Customization accessories

- 5.6 Luggage and storage

- 5.7 Electronic accessories

- 5.8 Apparel and merchandise

- 5.9 Maintenance and care products

- 5.10 Comfort and convenience

Chapter 6 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Cruiser

- 6.3 Sports bike

- 6.4 Standard/commuter bike

- 6.5 Off-road/adventure bike

- 6.6 Scooters

Chapter 7 Market Estimates & Forecast, By Rider Age, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Youth Riders

- 7.3 Adult Riders

- 7.4 Senior Riders

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Specialized motorcycle accessory retailers

- 8.3 Authorized dealerships

- 8.4 Online/e-commerce platforms

- 8.5 Independent outlets

- 8.6 Supermarkets & hypermarkets

Chapter 9 Market Estimates & Forecast, By Usage, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Safety & protection

- 9.3 Performance enhancement

- 9.4 Comfort & convenience

- 9.5 Style & aesthetic customization

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.3.9 Denmark

- 10.3.10 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Israel

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Alpinestars

- 11.1.2 Bell Helmets

- 11.1.3 Brembo

- 11.1.4 Cardo

- 11.1.5 Fox Racing

- 11.1.6 Garmin

- 11.1.7 Givi

- 11.1.8 GoPro

- 11.1.9 Icon

- 11.1.10 Shoei

- 11.2 Regional Players

- 11.2.1 Airhawk

- 11.2.2 Arlen Ness

- 11.2.3 Corbin

- 11.2.4 Dynojet

- 11.2.5 Kryptonite

- 11.2.6 Nelson-Rigg

- 11.2.7 Roland Sands Design (RSD)

- 11.2.8 Saddlemen

- 11.2.9 Speed and Strength

- 11.3 Emerging Players & Technology Enablers

- 11.3.1 Xena

2026-2030年全球摩托车骑乘配件市场

2026-2030年全球摩托车骑乘配件市场 摩托车配件市场:依产品类型、销售管道、最终用户和性别划分-2026-2032年全球市场预测摩托车零件及配件市场:按产品类型、摩托车类型、安装类型、销售管道和最终用户划分-2026-2032年全球预测摩托车配件市场按产品类型、车辆类型、应用、分销管道和最终用户划分,全球预测(2026-2032年)

摩托车配件市场:依产品类型、销售管道、最终用户和性别划分-2026-2032年全球市场预测摩托车零件及配件市场:按产品类型、摩托车类型、安装类型、销售管道和最终用户划分-2026-2032年全球预测摩托车配件市场按产品类型、车辆类型、应用、分销管道和最终用户划分,全球预测(2026-2032年) 摩托车顶箱市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

摩托车顶箱市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球机车零件及配件市场全球摩托车配件市场

全球机车零件及配件市场全球摩托车配件市场 2024-2028年全球摩托车配件市场

2024-2028年全球摩托车配件市场 摩托车配件市场规模 - 按产品类型、自行车类型、分销管道和市场类型 - 区域前景、竞争策略和细分市场预测(截至 2033 年)

摩托车配件市场规模 - 按产品类型、自行车类型、分销管道和市场类型 - 区域前景、竞争策略和细分市场预测(截至 2033 年)