|

市场调查报告书

商品编码

1982349

工业加热器市场机会、成长要素、产业趋势分析及2026-2035年预测Industrial Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

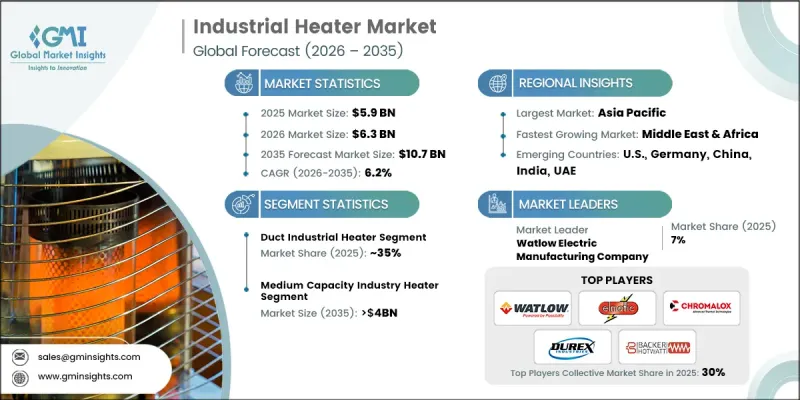

预计到 2025 年,全球工业加热器市场价值将达到 59 亿美元,并预计以 6.2% 的复合年增长率成长,到 2035 年达到 107 亿美元。

市场成长的驱动力来自许多工业应用领域日益增长的需求,在这些领域,精确的温度控制、可靠性和效率至关重要。各产业正越来越多地采用节能环保的加热解决方案,以降低能耗、减少营运成本并满足严格的环保标准。工业加热器旨在为干燥、固化、熔化和热处理等製程中的液体、气体、空气或固体提供可控的热量。技术创新正在催生更智慧、更耐用、更经济高效的加热系统,从而提高製程效率并最大限度地减少停机时间。活性化的工业活动和全球对永续性的关注正在加速高性能加热器的应用,以满足复杂的温度控制需求。在需要在整个製造和製作流程中实现可靠、精确温度控管的行业中,对先进、低排放和数位化控制加热器的需求尤其旺盛。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 59亿美元 |

| 预计金额 | 107亿美元 |

| 复合年增长率 | 6.2% |

预计到2035年,管道加热器市场规模将达到12亿美元。这些加热器能够维持输送液体、气体和黏性物质的管道内的温度稳定性,防止凝固并确保物料顺畅流动。电加热器和浸入式管道加热器因其能源效率高、精度高、可靠性强,在连续工业生产过程中越来越受欢迎。

预计到 2025 年,低容量加热器市场规模将达到 16 亿美元。这些加热器因其结构紧凑、易于安装、能源效率高以及能够在间歇运行期间精确控制温度等优点,受到实验室、小规模製造工厂和设备预热应用的青睐。

预计到2035年,北美工业加热器市场规模将达25亿美元。市场扩张的驱动力主要来自永续和节能型加热系统的普及、智慧控制技术的整合以及製造和加工行业自动化水平的提升。对精准、可靠且环保的加热解决方案的需求持续引领全部区域的市场发展趋势。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 原物料供应及采购分析

- 生产能力评估

- 供应链韧性与风险因素

- 配电网路分析

- 监理情势

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

- 工业加热器成本结构分析

- 价格趋势分析(美元/台币)

- 地区

- 按产能

- 新的成长机会和市场趋势

- 投资前景及未来成长潜力

- 智慧製造和工业4.0的引入

- 环境永续性措施和监管合规性

第四章 竞争情势

- 介绍

- 企业市占率分析:按地区划分

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场规模及预测:依技术划分,2022-2035年

- 电

- 油

- 固态燃料

- 气体

第六章 市场规模与预测:依产能划分,2022-2035年

- 低的

- 中等的

- 高的

第七章 市场规模及预测:依产品划分,2022-2035年

- 管道加热器

- 管道式加热器

- 筒式加热器

- 浸入式加热器

- 循环加热器

第八章 市场规模及预测:依应用领域划分,2022-2035年

- 石油和天然气

- 化学

- 食品/饮料

- 製造业

- 车

- 其他的

第九章 市场规模及预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 义大利

- 法国

- 荷兰

- 西班牙

- 挪威

- 英国

- 瑞典

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 泰国

- 新加坡

- 马来西亚

- 菲律宾

- 越南

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 伊朗

- 伊拉克

- 土耳其

- 南非

- 拉丁美洲

- 巴西

- 智利

- 阿根廷

第十章:公司简介

- Accutherm

- Backer Hotwatt

- Chromalox

- Durex Industries

- Elmec Heaters

- Elmatic

- ExcelHeaters

- Friedr Freek

- Heatcon Sensors

- Heatrex

- Heatco

- Indeeco

- Marathon Heater

- Omega Engineering

- Powrmatic

- Tempco Electric Heater Corporation

- Tutco Heating Solutions Group

- Ulanet

- Warren Electric Heating Technologies

- Watlow Electric Manufacturing Company

- Winterwarm Heating Solutions

- Zoppas Industries

The Global Industrial Heater Market was valued at USD 5.9 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 10.7 billion by 2035.

Growth in the market is driven by rising demand across a wide spectrum of industrial applications, where precise temperature control, reliability, and efficiency are critical. Industries are increasingly adopting energy-efficient and eco-friendly heating solutions to reduce energy consumption, cut operational costs, and meet stringent environmental standards. Industrial heaters are engineered to deliver controlled heat to liquids, gases, air, or solids for processes such as drying, curing, melting, and heat treatment. Technological innovations are enabling smarter, more durable, and cost-effective heating systems that improve process efficiency and minimize downtime. Rising industrial activity and the global focus on sustainability are accelerating the adoption of high-performance heaters capable of meeting complex thermal requirements. Demand for advanced, low-emission, and digitally controlled heaters is particularly strong as industries seek reliable and precise thermal management across manufacturing and processing operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.9 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 6.2% |

The pipe heater segment is expected to reach USD 1.2 billion by 2035. These heaters maintain temperature stability in pipelines transporting liquids, gases, and viscous substances, preventing solidification and ensuring smooth material flow. Electric and immersion-based pipe heaters are increasingly favored for their energy efficiency, precision, and reliability in continuous industrial processes.

The low-capacity heater segment accounted for USD 1.6 billion in 2025. These heaters are preferred in laboratories, smaller manufacturing facilities, and equipment preheating due to their compact design, ease of installation, energy efficiency, and ability to provide precise temperature control for intermittent operations.

North America Industrial Heater Market is projected to reach USD 2.5 billion by 2035. Market expansion is supported by the adoption of sustainable and energy-efficient heating systems, integration of smart controls, and increasing automation across manufacturing and processing sectors. Demand for precise, reliable, and eco-friendly heating solutions continues to shape market trends across the region.

Key companies operating in the Global Industrial Heater Market include Chromalox, Heatrex, Accutherm, Powrmatic, Ulanet, Elmatic, Tutco Heating Solutions Group, Winterwarm Heating Solutions, Tempco Electric Heater Corporation, ExcelHeaters, Backer Hotwatt, Elmec Heaters, Indeeco, Heatrex, Friedr Freek, Omega Engineering, Heatcon Sensors, Heatco, Zoppas Industries, and Marathon Heater. Companies in the Industrial Heater Market are strengthening their presence through technological innovation, product diversification, and strategic partnerships. Key strategies include developing energy-efficient and low-emission heating systems, incorporating smart sensors and digital controls for precise operation, and expanding into emerging industrial markets. Firms are investing in R&D to improve heater durability, reliability, and thermal efficiency while offering customizable solutions for various industrial applications. Collaborations with manufacturing, chemical, and processing companies allow players to provide integrated thermal management solutions, enhance operational performance, and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Market estimates & forecasts parameters

- 1.8 Forecast model

- 1.8.1 Quantified market impact analysis

- 1.8.1.1 Mathematical impact of growth parameters on forecast

- 1.8.1 Quantified market impact analysis

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

- 1.10 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Capacity trends

- 2.1.4 Product trends

- 2.1.5 Application trends

- 2.1.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of industrial heaters

- 3.8 Price trend analysis (USD/Unit)

- 3.8.1 region

- 3.8.2 By capacity

- 3.9 Evolving Growth opportunities & market trends

- 3.10 Investment outlook & future growth potential

- 3.11 Smart manufacturing & industry 4.0 adoption

- 3.12 Environmental sustainability measures & regulatory compliance

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans & funding

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Electric

- 5.3 Oil

- 5.4 Solid

- 5.5 Gas

Chapter 6 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Pipe heater

- 7.3 Duct heater

- 7.4 Cartridge heater

- 7.5 Immersion heater

- 7.6 Circulation heater

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Oil & gas

- 8.3 Chemical

- 8.4 Food & beverage

- 8.5 Manufacturing

- 8.6 Automotive

- 8.7 Others

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Italy

- 9.3.3 France

- 9.3.4 Netherlands

- 9.3.5 Spain

- 9.3.6 Norway

- 9.3.7 UK

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Thailand

- 9.4.7 Singapore

- 9.4.8 Malaysia

- 9.4.9 Philippines

- 9.4.10 Vietnam

- 9.4.11 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Iran

- 9.5.4 Iraq

- 9.5.5 Turkey

- 9.5.6 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Chile

- 9.6.3 Argentina

Chapter 10 Company Profiles

- 10.1 Accutherm

- 10.2 Backer Hotwatt

- 10.3 Chromalox

- 10.4 Durex Industries

- 10.5 Elmec Heaters

- 10.6 Elmatic

- 10.7 ExcelHeaters

- 10.8 Friedr Freek

- 10.9 Heatcon Sensors

- 10.10 Heatrex

- 10.11 Heatco

- 10.12 Indeeco

- 10.13 Marathon Heater

- 10.14 Omega Engineering

- 10.15 Powrmatic

- 10.16 Tempco Electric Heater Corporation

- 10.17 Tutco Heating Solutions Group

- 10.18 Ulanet

- 10.19 Warren Electric Heating Technologies

- 10.20 Watlow Electric Manufacturing Company

- 10.21 Winterwarm Heating Solutions

- 10.22 Zoppas Industries

智慧房间加热器市场:2026-2032年全球市场预测(依产品类型、输出功率、连接方式、应用和销售管道)壁挂式红外线加热器市场:按加热技术、类型、额定功率、销售管道、应用、最终用户划分,全球预测(2026-2032年)

智慧房间加热器市场:2026-2032年全球市场预测(依产品类型、输出功率、连接方式、应用和销售管道)壁挂式红外线加热器市场:按加热技术、类型、额定功率、销售管道、应用、最终用户划分,全球预测(2026-2032年) 2026-2034年全球工业加热器导热油市场规模、份额、趋势及成长分析报告全球单元式加热器市场规模、份额、趋势和成长分析报告(2026-2034年)暖气设备市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

2026-2034年全球工业加热器导热油市场规模、份额、趋势及成长分析报告全球单元式加热器市场规模、份额、趋势和成长分析报告(2026-2034年)暖气设备市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 日本工业加热器市场规模、份额、趋势和预测:按产品、技术、最终用户和地区划分,2026-2034年

日本工业加热器市场规模、份额、趋势和预测:按产品、技术、最终用户和地区划分,2026-2034年 空间加热器市场机会、成长要素、产业趋势分析及2026年至2035年预测

空间加热器市场机会、成长要素、产业趋势分析及2026年至2035年预测 2026-2030年全球空间暖气设备市场ITO透明导电加热器市场:2026-2032年全球预测(按基板、沉积技术、设计类型和应用划分)半导体加热器市场:按产品、额定功率、技术、最终用户、应用和分销管道划分,全球预测(2026-2032年)

2026-2030年全球空间暖气设备市场ITO透明导电加热器市场:2026-2032年全球预测(按基板、沉积技术、设计类型和应用划分)半导体加热器市场:按产品、额定功率、技术、最终用户、应用和分销管道划分,全球预测(2026-2032年)