|

市场调查报告书

商品编码

1998737

汽车牵引马达市场机会、成长要素、产业趋势分析及2026-2035年预测。Automotive Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

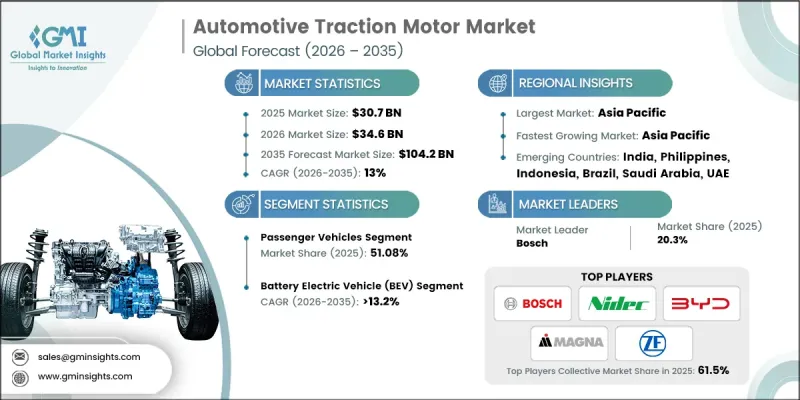

预计到 2025 年,全球汽车牵引马达市场规模将达到 307 亿美元,并预计以 13% 的复合年增长率成长,到 2035 年达到 1,042 亿美元。

汽车产业的快速电气化正在将牵引马达从传动系统的辅助部件转变为决定车辆性能和能源效率的核心部件。随着全球交通运输向电气化转型,牵引马达对于动力输出、优化能源利用以及满足不断变化的环境法规至关重要。这些马达目前已广泛整合到各种电动汽车平臺中,包括纯电动车、混合动力汽车和电动商用车。电动车产量的不断增长、车型阵容的不断扩大以及日益严格的排放气体政策,都推动了对先进马达技术的强劲需求。汽车製造商正致力于提高马达效率、增强扭力输出、减轻系统整体重量并确保稳定的热性能。同时,牵引马达与电力电子和电池系统的集成,也促进了更全面的车辆架构设计。电机材料和结构方面的技术进步也影响市场竞争,製造商不断开发解决方案,以提高能源效率、降低生产成本并提升车辆的长期性能。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 307亿美元 |

| 预测金额 | 1042亿美元 |

| 复合年增长率 | 13% |

预计到2025年,乘用车市占率将达到51.08%,并在2035年之前以12.3%的复合年增长率成长。该细分市场的强劲地位主要得益于全球范围内电动乘用车的加速普及以及涵盖不同价格区间的电动车型供应量的不断扩大。汽车製造商正优先推进各类乘用车的电气化,从而显着增加了现代车辆的驱动马达数量。此外,向专用电动车平台的转型以及豪华乘用车中多马达配置的日益普及,也增加了每辆车使用的马达数量,进一步巩固了乘用车市场的份额。

预计到2025年,电池式电动车(BEV)市占率将达到67.2%,并在2026年至2035年间以13.2%的复合年增长率成长。这种压倒性的市场主导地位主要归功于电池式电动车完全依赖电力驱动系统。与将内燃机与电力动力传动系统结合的混合动力汽车不同,纯电动车完全由电动马达驱动,这直接增加了每辆车对牵引马达的需求。此外,许多高性能电动车采用多马达配置来提高动力输出和车辆控制性能。全球推广零排放出行的努力、电池成本的下降以及充电基础设施的持续扩展,进一步加速了纯电动车的生产和普及,从而增加了对牵引马达技术的需求。

预计到2025年,中国汽车牵引马达市场规模将达104亿美元,市占率高达64.21%。凭藉主导地位以及对汽车电气化的大力支持,中国在区域市场保持着强劲的竞争力。中国已建构起一个涵盖大规模电动车生产、一体化供应链以及强大的电池和电力电子製造能力的综合生态系统。政府旨在推广新能源汽车和扩大电动出行基础设施的各项倡议,持续推动电动乘用车和商务传输解决方案的普及。这些因素共同促成了对高效可靠电力驱动的先进牵引马达系统需求的显着增长。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球电动车产量增加

- 更严格的排放气体和燃油效率法规

- 公共运输和货运车辆电气化进程的快速成长

- 消费者对高性能电动车的需求日益增长

- 增加电动车製造生态系统本地化的投资

- 产业潜在风险与挑战

- 稀土元素材料价格波动

- 初期研发和资本投资需要大量资金。

- 市场机会

- 新兴国家电动车普及率的扩大

- 两轮和三轮车辆电气化进程

- 政府主导的电动公车部署计画增加

- 高端和高性能电动车市场需求激增

- 促进因素

- 成长潜力分析

- 监管指南

- 北美洲

- 美国:电动车税额扣抵、美国环保署排放气体标准和美国能源部电动车效率计划

- 加拿大:加拿大运输部製定了零排放车辆 (ZEV) 强制令和安全标准。

- 欧洲

- 德国:欧盟二氧化碳排放目标与报废车辆指令

- 英国:强制性零排放车辆 (ZEV) 要求和型式法规认证

- 法国:能源转型法与电动车产业战略

- 义大利:与国家能源和气候计画(PNIEC)的一致性

- 亚太地区

- 中国:强制性新能源汽车和双轨政策

- 印度:汽车零件FAME II和PLI计划

- 日本:绿色成长策略与JEVS标准

- 澳洲:国家电动车战略

- 拉丁美洲

- 巴西:Rota 2030计划

- 墨西哥:美墨加协定在地化要求

- 阿根廷:国家永续交通政策

- 中东和非洲

- 阿联酋:2050年实现净零排放策略并扩大电动车基础设施

- 沙乌地阿拉伯:2030愿景与电动车本土化策略

- 南非:绿色交通战略

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析(基于初步研究)

- 价格分析(基于初步调查)

- 对过去价格趋势的分析

- 按业务类型分類的定价策略

- 成本細項分析

- 永续性和环境影响分析

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

- 未来展望与机会

- 贸易统计(基于付费资料库)

- 生产基地

- 消费者群体

- 出口和进口

- 主要贸易走廊及关税的影响

- 美中贸易趋势

- 欧盟内部市场贸易

- 亚太地区的贸易

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- GenAI 各细分市场的应用案例与部署蓝图

- 风险、限制和监管考量

- 投资与资金筹措分析

- 私募股权和创业投资的趋势

- 併购趋势与策略整合

- 政府资助和研发津贴

- 预测假设和情境分析(基于初步研究)

- 基本案例-驱动复合年增长率的关键宏观经济与产业变量

- 乐观情境-宏观经济与产业的顺风

- 悲观情景-宏观经济放缓或产业逆风

第四章 竞争情势

- 介绍

- 企业市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 企业级分层基准测试

- 层级分类标准与选择标准

- 按销售额、地区和创新能力分類的层级定位矩阵。

- 主要进展

- 併购

- 伙伴关係和联盟

- 新产品发布

- 业务拓展计划及资金筹措

第五章 市场估价与预测:依车辆类型划分,2022-2035年

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 摩托车

- 越野车

第六章 市场估算与预测:依电动驱动系统划分,2022-2035年

- 电池式电动车(BEV)

- 混合动力电动车(HEV)

- 插电式混合动力汽车(PHEV)

第七章 市场估计与预测:依动力来源,2022-2035年

- PMSM

- 交流感应马达

- 其他的

第八章 市场估计与预测:依产量划分,2022-2035年

- 小于200千瓦

- 200~400 kW

- 超过400千瓦

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 荷兰

- 比利时

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十章:公司简介

- 世界公司

- Aisin

- BorgWarner

- Bosch

- BYD

- DENSO

- Nidec

- Tesla

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

- 当地公司

- General Motors

- Hitachi Astemo

- Huawei Digital Power

- Hyundai Mobis

- Inovance Automotive

- Jing-Jin Electric

- Magna International

- MAHLE

- Mitsubishi Electric

- Schaeffler Group

- 新兴企业

- Equipmake

- LG Magna e-Powertrain

- Lucid Motors

- Rivian

- YASA(Mercedes-Benz)

The Global Automotive Traction Motor Market was valued at USD 30.7 billion in 2025 and is estimated to grow at a CAGR of 13% to reach USD 104.2 billion by 2035.

The rapid electrification of the automotive industry is transforming the traction motor from a secondary drivetrain element into a central component responsible for vehicle performance and energy efficiency. As global mobility transitions toward electrified transportation, traction motors have become essential for delivering power, optimizing energy usage, and supporting compliance with evolving environmental regulations. These motors are now widely integrated across various electrified vehicle platforms, including fully electric vehicles, hybrid vehicles, and electrified commercial fleets. Rising electric vehicle production, expanding vehicle model offerings, and increasingly strict emission reduction policies are collectively driving strong demand for advanced motor technologies. Automotive manufacturers are focusing on enhancing motor efficiency, improving torque output, reducing overall system weight, and ensuring stable thermal performance. At the same time, the integration of traction motors with power electronics and battery systems is encouraging a more comprehensive approach to vehicle architecture design. Technological advancements in motor materials and configurations are also influencing competition within the market as manufacturers continue to develop solutions that improve energy efficiency, reduce production costs, and enhance long-term vehicle performance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $30.7 Billion |

| Forecast Value | $104.2 Billion |

| CAGR | 13% |

The passenger cars segment accounted for 51.08% share in 2025 and is projected to grow at a CAGR of 12.3% through 2035. The strong position of this segment is primarily supported by the accelerating adoption of electric passenger vehicles worldwide and the increasing availability of electrified models across different price categories. Automotive manufacturers are prioritizing the electrification of various passenger vehicle categories, which has significantly increased the installation of traction motors in modern vehicles. In addition, the transition toward dedicated electric vehicle platforms and the growing adoption of multi-motor configurations in premium passenger vehicles are increasing the number of motors used per vehicle, further strengthening the market share of the passenger car segment.

The battery electric vehicle segment held a 67.2% share in 2025 and is expected to grow at a CAGR of 13.2% between 2026 and 2035. This strong dominance is largely attributed to the complete reliance of battery electric vehicles on electric propulsion systems for mobility. Unlike hybrid vehicles that combine internal combustion engines with electric powertrains, battery electric vehicles operate entirely using electric motors, which directly increases traction motor demand per vehicle. In addition, many high-performance electric vehicles utilize multiple motor configurations to enhance power output and vehicle control. Global initiatives promoting zero-emission mobility, declining battery costs, and the continuous expansion of charging infrastructure are further accelerating the production and adoption of battery electric vehicles, thereby increasing demand for traction motor technologies.

China Automotive Traction Motor Market generated USD 10.4 billion in 2025 and held 64.21% share. The country maintains a strong position in the regional market due to its leadership in global electric vehicle manufacturing and its strong support for vehicle electrification. China has developed a comprehensive ecosystem that includes large-scale electric vehicle production, integrated supply chains, and strong manufacturing capabilities for batteries and power electronics. Government initiatives aimed at promoting new energy vehicles and expanding electric mobility infrastructure continue to encourage the adoption of electrified passenger vehicles and commercial transportation solutions. These factors are contributing to substantial demand for advanced traction motor systems designed to deliver efficient and reliable electric propulsion.

Key companies operating in the Global Automotive Traction Motor Market include Bosch, Denso, ZF Friedrichshafen, Continental, Magna, Valeo, Hitachi, Mitsubishi Electric, Aisin, and General Motors. Companies competing in the Automotive Traction Motor Market are implementing a variety of strategies to strengthen their competitive position and expand global market share. Leading manufacturers are investing heavily in research and development to improve motor efficiency, increase power density, and enhance thermal management capabilities. Many companies are also focusing on developing advanced motor architectures that reduce reliance on expensive raw materials while improving performance and durability. Strategic collaborations with automotive manufacturers and technology partners are helping companies accelerate innovation and integrate traction motors more effectively with electric powertrain systems. Additionally, organizations are expanding manufacturing facilities, strengthening supply chains, and increasing production capacity to meet the rapidly growing demand for electric vehicles. Continuous technological advancement, platform integration, and global expansion remain essential strategies for maintaining competitiveness in the automotive traction motor market.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Electric Drivetrain

- 2.2.4 Motor

- 2.2.5 Power Output

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in global electric vehicle production

- 3.2.1.2 Increase in stringent emission and fuel efficiency regulations

- 3.2.1.3 Surge in electrification of public transport and logistics fleets

- 3.2.1.4 Rise in consumer demand for high-performance EVs

- 3.2.1.5 Increase in investments toward localized EV manufacturing ecosystems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuation in rare-earth material prices

- 3.2.2.2 High initial R&D and capital investment requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in EV adoption across emerging economies

- 3.2.3.2 Rise in electrification of two- and three-wheelers

- 3.2.3.3 Increase in government-backed electric bus deployment programs

- 3.2.3.4 Surge in demand for premium and performance EV segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory guidline

- 3.4.1 North America

- 3.4.1.1 U.S.: EV Tax Credits, EPA Emission Standards & DOE Electric Drive Efficiency Programs

- 3.4.1.2 Canada: Zero-Emission Vehicle (ZEV) Mandate & Transport Canada Safety Standards

- 3.4.2 Europe

- 3.4.2.1 Germany: EU CO Fleet Emission Targets & End-of-Life Vehicle (ELV) Directive

- 3.4.2.2 UK: Zero Emission Vehicle (ZEV) Mandate & Type Approval Regulations

- 3.4.2.3 France: Energy Transition Law & EV Industrial Strategy

- 3.4.2.4 Italy: National Energy & Climate Plan (PNIEC) Alignment

- 3.4.3 Asia Pacific

- 3.4.3.1 China: NEV Mandate & Dual Credit Policy

- 3.4.3.2 India: FAME II & PLI Scheme for Auto Components

- 3.4.3.3 Japan: Green Growth Strategy & JEVS Standards

- 3.4.3.4 Australia: National Electric Vehicle Strategy

- 3.4.4 Latin America

- 3.4.4.1 Brazil: Rota 2030 Program

- 3.4.4.2 Mexico: USMCA Localization Requirements

- 3.4.4.3 Argentina: National Sustainable Mobility Policies

- 3.4.5 MEA

- 3.4.5.1 UAE: Net Zero 2050 Strategy & EV Infrastructure Expansion

- 3.4.5.2 Saudi Arabia: Vision 2030 & EV Localization Strategy

- 3.4.5.3 South Africa: Green Transport Strategy

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis (Driven by Primary Research)

- 3.9 Pricing Analysis (Driven by Primary Research)

- 3.9.1 Historical Price Trend Analysis

- 3.9.2 Pricing Strategy by Player Type

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Trade statistics (Driven by Paid Database)

- 3.13.1 Production hubs

- 3.13.2 Consumption hubs

- 3.13.3 Export and import

- 3.14 Key Trade corridors & tariff impact

- 3.14.1 US-china trade dynamics

- 3.14.2 EU internal market trade

- 3.14.3 Asia-pacific regional trade

- 3.15 Impact of AI & Generative AI on the Market

- 3.15.1 AI-Driven disruption of existing business models

- 3.15.2 GenAI use cases & adoption roadmap by segment

- 3.15.3 Risks, limitations & regulatory considerations

- 3.16 Investment & funding analysis

- 3.16.1 Private equity & venture capital activity

- 3.16.2 M&a trends & strategic consolidations

- 3.16.3 Government funding & R&D grants

- 3.17 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.17.1 Base Case - key macro & industry variables driving CAGR

- 3.17.2 Optimistic Scenarios - Favorable Macro and Industry Tailwinds

- 3.17.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Company Tier Benchmarking

- 4.5.1 Tier Classification Criteria & Qualifying Thresholds

- 4.5.2 Tier Positioning Matrix by Revenue, Geography & Innovation

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Medium Commercial Vehicles (MCV)

- 5.3.3 Heavy Commercial Vehicles (HCV)

- 5.4 Two-wheelers

- 5.5 Off-road vehicles

Chapter 6 Market Estimates & Forecast, By Electric Drivetrain, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicle (BEV)

- 6.3 Hybrid Electric Vehicle (HEV)

- 6.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 7 Market Estimates & Forecast, By Motor, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 PMSM

- 7.3 AC Induction

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 200 KW

- 8.3 200-400 KW

- 8.4 Above 400 KW

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Netherlands

- 9.3.8 Belgium

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Aisin

- 10.1.2 BorgWarner

- 10.1.3 Bosch

- 10.1.4 BYD

- 10.1.5 DENSO

- 10.1.6 Nidec

- 10.1.7 Tesla

- 10.1.8 Valeo

- 10.1.9 Vitesco Technologies

- 10.1.10 ZF Friedrichshafen

- 10.2 Regional Players

- 10.2.1 General Motors

- 10.2.2 Hitachi Astemo

- 10.2.3 Huawei Digital Power

- 10.2.4 Hyundai Mobis

- 10.2.5 Inovance Automotive

- 10.2.6 Jing-Jin Electric

- 10.2.7 Magna International

- 10.2.8 MAHLE

- 10.2.9 Mitsubishi Electric

- 10.2.10 Schaeffler Group

- 10.3 Emerging players

- 10.3.1 Equipmake

- 10.3.2 LG Magna e-Powertrain

- 10.3.3 Lucid Motors

- 10.3.4 Rivian

- 10.3.5 YASA (Mercedes-Benz)

汽车牵引马达市场:2026-2032年全球市场预测(按马达类型、额定功率、车辆类型、速度范围、冷却方式和车辆应用划分)

汽车牵引马达市场:2026-2032年全球市场预测(按马达类型、额定功率、车辆类型、速度范围、冷却方式和车辆应用划分) 汽车牵引力控制系统市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测2026-2034年全球汽车牵引和辅助电池市场规模、份额、趋势和成长分析报告全球汽车牵引马达市场规模、份额、趋势和成长分析报告(2026-2034年)

汽车牵引力控制系统市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察和预测2026-2034年全球汽车牵引和辅助电池市场规模、份额、趋势和成长分析报告全球汽车牵引马达市场规模、份额、趋势和成长分析报告(2026-2034年) 电动车牵引马达市场:依传动类型、设计、额定输出、车辆类型、马达类型、车桥结构、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测

电动车牵引马达市场:依传动类型、设计、额定输出、车辆类型、马达类型、车桥结构、应用、国家及地区划分-产业分析、市场规模、份额及2025年至2032年未来预测 2026年全球电动车牵引马达市场报告新能源汽车牵引马达铁芯市场:按马达类型、额定功率、驱动配置、冷却方式、车辆类型和销售管道,全球预测,2026-2032年汽车牵引马达铁芯市场:按马达类型、电压等级、额定功率、冷却方式和车辆类型划分,全球预测,2026-2032年电动和混合动力汽车牵引马达铁芯市场(按马达技术、功率等级、冷却方式、材料类型、速度范围、相数类型、车辆类型和应用划分),全球预测,2026-2032年电动车牵引马达铁芯市场:按马达类型、推进方式、额定功率、冷却方式和车辆类型划分 - 全球预测(2026-2032 年)

2026年全球电动车牵引马达市场报告新能源汽车牵引马达铁芯市场:按马达类型、额定功率、驱动配置、冷却方式、车辆类型和销售管道,全球预测,2026-2032年汽车牵引马达铁芯市场:按马达类型、电压等级、额定功率、冷却方式和车辆类型划分,全球预测,2026-2032年电动和混合动力汽车牵引马达铁芯市场(按马达技术、功率等级、冷却方式、材料类型、速度范围、相数类型、车辆类型和应用划分),全球预测,2026-2032年电动车牵引马达铁芯市场:按马达类型、推进方式、额定功率、冷却方式和车辆类型划分 - 全球预测(2026-2032 年)