|

市场调查报告书

商品编码

1998795

遥控武器站市场机会、成长要素、产业趋势分析及2026-2035年预测Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

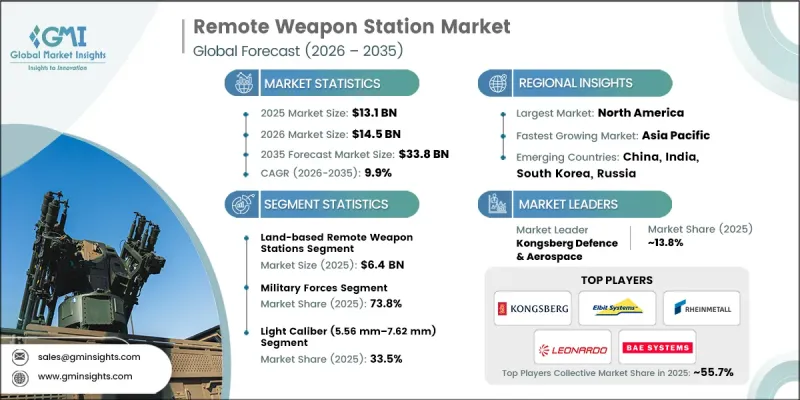

全球遥控武器站市场预计到 2025 年将价值 131 亿美元,以 9.9% 的复合年增长率成长,到 2035 年将达到 338 亿美元。

市场成长的驱动因素包括全球国防现代化预算的增加、非对称威胁场景的扩大以及陆海空平台对部队防护解决方案日益增长的需求。无人和自主平台的部署,以及人工智慧驱动的目标获取和先进感测器融合系统的应用,正在改变作战能力,使现代战场上的反应更加精准迅速。其他驱动因素,包括跨境安全投资、海军和海岸防御现代化以及政府支持国内国防生产的倡议,共同加速了远程武器站在全球范围内的部署。国防费用的增加,加上技术创新和战略采购政策,持续扩大了远程武器站在全球多个军事领域和作战区域的部署。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 131亿美元 |

| 预测金额 | 338亿美元 |

| 复合年增长率 | 9.9% |

该市场深受政府投资的影响,这些投资旨在实现武器系统现代化、提升舰队战备水平,并将遥控武器站(RWS)整合到无人驾驶车辆中。非对称威胁的日益普遍、海军和边防安全采购的扩大以及政府支持的本地製造项目,都显着推动了市场成长。人工智慧驱动的目标捕获和感测器融合技术使操作人员能够更快、更准确地做出决策,从而进一步促进了遥控武器站的应用。

陆基遥控武器站(RWS)市场预计到2025年将达64亿美元。这些系统广泛部署在装甲车、步兵战车和作战卡车上,能够实现持续的战场监视、精确目标定位以及与先进感测器的整合。其作战的多功能性和可靠性使其成为现代军队寻求增强防护和远程打击能力的核心装备。

到2025年,小口径(5.56毫米至7.62毫米)遥控武器站的市占率将达到33.5%。小口径遥控武器站因其精度高、后座力小以及可手动/自动射击而备受青睐。这些系统能够支援都市区和衝突地区的战术行动,同时也保障平民安全。得益于人工智慧驱动的追踪技术和光电感测器的集成,小口径遥控武器站的任务效率显着提升,正成为世界各国军队的理想选择。

预计2025年,北美遥控武器站(RWS)市占率将达33%。该地区的成长主要得益于大规模国防现代化项目、不断增长的国防费用以及对无人系统和部队防护的战略重点。美国国防部对人工智慧驱动的目标获取和感测器融合技术的投入,加上该地区成熟的国防工业基础,正在巩固北美在遥控武器站部署领域的领先地位。边防安全、反恐和联合行动将在2035年前进一步推动市场扩张。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球国防现代化支出增加

- 非对称战争的兴起和对部队保护日益增长的需求。

- 无人系统整合扩展

- 扩大海军在海岸防御中遥控武器站的部署

- 与边防安全和国防安全保障相关的采购

- 产业潜在风险与挑战

- 与传统平台的复杂集成

- 网路安全与电子战的漏洞

- 市场机会

- 人工智慧驱动的自主作战系统

- 无人地面和空中平台中的RWS

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与开发

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴竞争对手和Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依平台类型划分,2022-2035年

- 地面遥控武器站

- 轻型战术车辆

- 防地雷反伏击车和装甲车辆(装甲运兵车+步兵战车+主战坦克)

- 无人地面车辆(UGV)

- 海军遥控武器站

- 小型船隻(巡逻艇、海岸防卫队/边境队)

- 克尔维特

- 大型军舰(巡防舰、驱逐舰、两栖攻击舰)

- 固定/静止设施

- 机载遥控武器站

- 直升机

- 无人驾驶飞行器(UAV)

第六章 市场估价与预测:依武器类型划分,2022-2035年

- 小直径(5.56毫米至7.62毫米)

- 中口径(12.7毫米/.50口径)

- 粗径(14.5毫米至20毫米)

- 火炮(25毫米至40毫米)

第七章 市场估计与预测:依行程类型划分,2022-2035年

- 移动RWS

- 静止RWS

第八章 市场估计与预测:依最高自主等级划分,2022-2035年

- 限手动遥控器

- 半自主

- 自主参与是可能的。

第九章 市场估算与预测:感测器套件配置,2022-2035年

- 基本型(仅限白天拍摄)

- 标准(日间+热感)

- 高级(日间+热感+光达)

- 进阶版(频谱+雷射雷达+自动追踪+人工智慧)

第十章 市场估价与预测:依最终用户划分,2022-2035年

- 军队

- 国防安全保障/边防安全

- 执法机关及国内安全

- 商业和关键基础设施

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 主要企业

- BAE Systems plc

- Rheinmetall AG

- Leonardo SpA

- Thales Group

- Saab AB

- 按地区分類的主要企业

- 北美洲

- General Dynamics Corporation

- 亚太地区

- ASELSAN AS

- Norinco

- ST Engineering

- 欧洲

- FN Herstal

- KNDS Group

- 北美洲

- 特殊玩家/干扰者

- Kongsberg Defence &Aerospace

- Elbit Systems Ltd.

- Electro Optic Systems

- Rafael Advanced Defense Systems

- Pro Optica

The Global Remote Weapon Station Market was valued at USD 13.1 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 33.8 billion in 2035.

Market growth is fueled by rising global defense modernization budgets, expanding asymmetric threat scenarios, and increasing demand for force protection solutions across land, sea, and air platforms. The adoption of unmanned and autonomous platforms, along with AI-enabled targeting and advanced sensor fusion systems, is transforming operational capabilities, enabling more precise and rapid responses on modern battlefields. Additional drivers include cross-border security investments, naval and coastal defense upgrades, and government initiatives supporting indigenous defense production, which together accelerate the deployment of remote weapon stations worldwide. Rising defense expenditures, coupled with technological innovation and strategic procurement policies, continue to strengthen adoption across multiple military domains and operational theaters.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.1 Billion |

| Forecast Value | $33.8 Billion |

| CAGR | 9.9% |

The market is strongly influenced by government investment in modernizing weapons systems, enhancing fleet readiness, and integrating RWS into unmanned vehicles. Rising asymmetric threats, increased naval and border security acquisitions, and government-backed local manufacturing programs are significant contributors to market expansion. AI-driven targeting and sensor fusion technologies allow operators to make faster, more accurate decisions, which further boosts adoption of remote weapon stations.

The land-based remote weapon stations segment reached USD 6.4 billion in 2025. These systems are widely deployed on armored vehicles, infantry fighting vehicles, and combat trucks, offering continuous battlefield surveillance, precise target engagement, and integration with advanced sensors. Their operational versatility and reliability make them a cornerstone for modern armies seeking enhanced protection and remote engagement capabilities.

The light-caliber (5.56 mm-7.62 mm) segment held 33.5% share in 2025. Light-caliber RWS are favored for their precision, minimal recoil, and dual manual and automatic operation. These systems support tactical operations in urban environments and conflict zones while ensuring civilian safety. AI-assisted tracking and electro-optical sensor integration enhance mission efficiency, making light-caliber RWS a preferred choice for militaries worldwide.

North America Remote Weapon Station Market held a 33% share in 2025. Growth in this region is driven by large-scale defense modernization programs, elevated defense spending, and strategic focus on unmanned systems and force protection. Funding from the U.S. Department of Defense for AI-enabled targeting and sensor fusion technologies, combined with the region's mature defense industrial base, strengthens North America's position as a leader in RWS adoption. Border security, counter-terrorism initiatives, and coalition operations further reinforce market expansion through 2035.

Prominent players in the Global Remote Weapon Station Market include Kongsberg Defence & Aerospace, Rheinmetall AG, Rafael Advanced Defense Systems, KNDS Group, BAE Systems plc, FN Herstal, Leonardo S.p.A., Elbit Systems Ltd., ST Engineering, Electro Optic Systems, Pro Optica, Norinco, Thales Group, ASELSAN A.S, General Dynamics Corporation, and Saab AB. Companies in the Global Remote Weapon Station Market are adopting multiple strategies to consolidate their presence and expand market share. These include investing heavily in R&D to develop AI-assisted targeting, sensor fusion, and modular platforms adaptable to multiple vehicles and environments. Strategic partnerships with defense ministries, technology firms, and OEMs help integrate advanced systems into operational fleets. Firms are also focusing on localized production and technology transfer initiatives to meet government requirements and reduce supply chain dependency. Expansion of regional service centers, training programs, and rapid upgrade capabilities ensures operational readiness while enhancing customer engagement.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Platform type trends

- 2.2.2 Weapon type trends

- 2.2.3 Mobility type trends

- 2.2.4 Highest autonomy level trends

- 2.2.5 Sensor suite configuration trends

- 2.2.6 End-user trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense modernization spending

- 3.2.1.2 Increased asymmetric warfare and force-protection needs

- 3.2.1.3 Expansion of unmanned systems integration

- 3.2.1.4 Growing naval RWS deployments for coastal defense

- 3.2.1.5 Border security and homeland security procurements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex integration with legacy platforms

- 3.2.2.2 Cybersecurity and electronic warfare vulnerabilities

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven autonomous engagement systems

- 3.2.3.2 RWS on unmanned ground and aerial platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Land-based remote weapon stations

- 5.2.1 Light tactical vehicles

- 5.2.2 MRAP & armored vehicles (APCs + IFVs + MBTs)

- 5.2.3 Unmanned ground vehicles (UGVs)

- 5.3 Naval remote weapon stations

- 5.3.1 Small naval vessels (patrol boats, coast guard / border patrol)

- 5.3.2 Corvettes

- 5.3.3 Large naval vessels (frigates, destroyers, amphibious assault vessels)

- 5.4 Fixed / stationary installations

- 5.5 Airborne remote weapon stations

- 5.5.1 Helicopters

- 5.5.2 Unmanned aerial vehicles (UAVs)

Chapter 6 Market Estimates and Forecast, By Weapon Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Light caliber (5.56mm - 7.62mm)

- 6.3 Medium caliber (12.7mm / .50 cal)

- 6.4 Heavy caliber (14.5mm - 20mm)

- 6.5 Cannon (25mm - 40mm)

Chapter 7 Market Estimates and Forecast, By Mobility Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Mobile RWS

- 7.3 Stationary RWS

Chapter 8 Market Estimates and Forecast, By Highest Autonomy Level, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Manual remote operation only

- 8.3 Semi-autonomous

- 8.4 Autonomous engagement capable

Chapter 9 Market Estimates and Forecast, By Sensor Suite Configuration, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Basic (day camera only)

- 9.3 Standard (day + thermal)

- 9.4 Advanced (day + thermal + LRF)

- 9.5 Premium (Multi-Spectral + LRF + auto-tracking + AI)

Chapter 10 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 Military forces

- 10.3 Homeland security & border protection

- 10.4 Law enforcement & internal security

- 10.5 Commercial & critical infrastructure

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 BAE Systems plc

- 12.1.2 Rheinmetall AG

- 12.1.3 Leonardo S.p.A

- 12.1.4 Thales Group

- 12.1.5 Saab AB

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 General Dynamics Corporation

- 12.2.2 Asia Pacific

- 12.2.2.1 ASELSAN A.S

- 12.2.2.2 Norinco

- 12.2.2.3 ST Engineering

- 12.2.3 Europe

- 12.2.3.1 FN Herstal

- 12.2.3.2 KNDS Group

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Kongsberg Defence & Aerospace

- 12.3.2 Elbit Systems Ltd.

- 12.3.3 Electro Optic Systems

- 12.3.4 Rafael Advanced Defense Systems

- 12.3.5 Pro Optica

2026年全球海军遥控武器系统(RWS)市场报告2026年全球遥控武器系统市场报告2026年全球遥控武器系统(RWS)市场报告

2026年全球海军遥控武器系统(RWS)市场报告2026年全球遥控武器系统市场报告2026年全球遥控武器系统(RWS)市场报告 海军遥控武器站市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

海军遥控武器站市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 遥控武器系统(RCWS)市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察与预测

遥控武器系统(RCWS)市场规模、份额、成长率及全球产业分析:按类型、应用和地区划分,并提供2026-2034年的洞察与预测 遥控武器系统市场-全球产业规模、份额、趋势、机会、预测:按组件、武器类型、平台、地区和竞争对手划分,2021-2031年

遥控武器系统市场-全球产业规模、份额、趋势、机会、预测:按组件、武器类型、平台、地区和竞争对手划分,2021-2031年 遥控武器站市场规模、份额和成长分析(按平台、应用、组件、武器类型、技术、移动性和地区划分)-2026-2033年产业预测

遥控武器站市场规模、份额和成长分析(按平台、应用、组件、武器类型、技术、移动性和地区划分)-2026-2033年产业预测 RWS(远程武器系统Remote Weapon System的)全球市场的评估:各系统,武器类别,各零件,各地区,机会,预测(2018年~2032年)

RWS(远程武器系统Remote Weapon System的)全球市场的评估:各系统,武器类别,各零件,各地区,机会,预测(2018年~2032年) 2025-2029年全球远程武器系统市场遥控枪系统 (RWS) 市场:2033 年的机会与策略

2025-2029年全球远程武器系统市场遥控枪系统 (RWS) 市场:2033 年的机会与策略