|

市场调查报告书

商品编码

1998847

2026 年至 2035 年医药塑胶瓶的市场机会、成长要素、产业趋势与预测。Pharmaceutical Plastic Bottles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

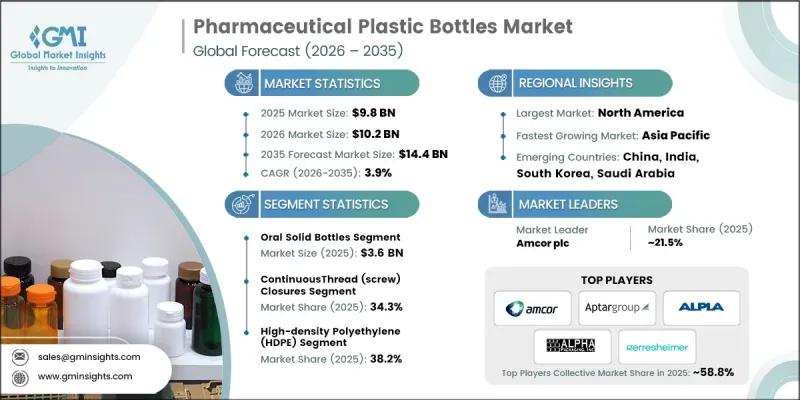

预计到 2025 年,全球药品用塑胶瓶市场价值将达到 98 亿美元,并以 3.9% 的复合年增长率成长,到 2035 年将达到 144 亿美元。

全球学名药产量增加、口服固体製剂需求持续成长以及非处方药(OTC)消费量扩大,是推动市场扩张的主要因素。此外,包装材料从玻璃瓶转向轻质高密度聚苯乙烯(HDPE),以及外包给契约製造组织(CMO)的趋势,也促进了市场需求。儿童安全包装和防篡改包装的监管要求,以及推广可回收和消费后回收(PCR)瓶的可持续发展倡议,进一步推动了市场成长。在北美和亚太地区,受自我治疗、药房网路扩张以及机能性食品市场成长的推动,成药的需求正在不断增长。塑胶瓶具有安全性、防篡改性和轻巧设计等关键优势,这些优势持续支撑着全球零售和药房通路的高周转率和稳定需求。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 98亿美元 |

| 预测金额 | 144亿美元 |

| 复合年增长率 | 3.9% |

预计到2025年,口服固态製剂瓶的市场规模将达到36亿美元。鑑于片剂和胶囊是全球处方量最大的药物之一,尤其是在治疗慢性疾病方面,这些瓶子将继续发挥至关重要的作用。它们具有防潮、适用于大宗包装以及与儿童安全瓶盖相容等优点,使其成为大规模药品生产和分销网络中不可或缺的包装。

预计到2025年,高密度聚苯乙烯(HDPE)市占率将达到38.2%。 HDPE因其优异的防潮性、耐化学性、耐久性和轻质特性而备受青睐,是片剂、胶囊和粉末包装的理想材料。此外,HDPE运输成本低,且符合药品稳定性要求,使其成为北美、欧洲和亚洲等监管市场的理想包装材料。

到2025年,北美医药塑胶瓶市占率将达到39.7%。该地区的成长主要受处方药消费量增加、药品安全法规日益严格以及市场对轻便防碎包装的需求所推动。美国食品药物管理局(FDA)和加拿大卫生署 Canada)的法律规范,例如儿童安全标准和防篡改标准,也推动了对高密度聚乙烯(HDPE)和聚丙烯医药瓶的需求。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 全球学名药产量增加

- 口服固体製剂消耗量增加

- 全球对成药的需求不断增长

- 从玻璃瓶过渡到轻质高密度聚乙烯瓶

- 契约製造组织(CMO)的扩张

- 产业潜在风险与挑战

- 树脂(HDPE、PET、PP)价格波动

- 严格遵守有关萃取物和洗脱液的规定

- 市场机会

- 生物基聚合物在药品包装上的应用

- 具有防伪功能的智慧包装

- 促进因素

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 市场集中度分析

- 主要企业的竞争标竿分析

- 财务绩效比较

- 销售量

- 利润率

- 研究与发展(R&D)

- 产品系列比较

- 产品线宽度

- 科技

- 创新

- 区域扩张比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 业务拓展与投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估价与预测:以瓶型划分,2022-2035年

- 口服固态剂型用瓶

- 口服液体药物瓶

- 眼药水瓶

- 注射剂和注射管瓶

- 鼻喷雾瓶

- 外用/经皮瓶

第六章 市场估算与预测:依材料类型划分,2022-2035年

- 高密度聚苯乙烯(HDPE)

- 低密度聚乙烯(LDPE)

- 聚丙烯(PP)

- 聚对苯二甲酸乙二醇酯(PET)

- 聚对苯二甲酸乙二醇酯(PETG)

- 环烯烃聚合物(COP)和环烯烃共聚物(COC)

第七章 市场估价与预测:依瓶装规格划分,2022-2035年

- 微型瓶(5毫升至20毫升)

- 小瓶装(30毫升至100毫升)

- 中型瓶装(120毫升-300毫升)

- 大容量瓶(500毫升至1000毫升)

- 特大瓶装(超过1000毫升)

第八章 市场估计与预测:依市值类型划分,2022-2035年

- 连续螺帽

- 卡扣式帽

- 分配盖

- 特製帽子

第九章 市场估价与预测:依最终用户划分,2022-2035年

- 製药公司(内部生产)

- 契约製造公司(CMO/CDMO)

- 营养补充品生产商

- 医疗机构

- 药局

第十章 市场估价与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 主要企业

- Gerresheimer AG

- Amcor plc

- AptarGroup, Inc.

- ALPLA Group

- Silgan Holdings Inc.

- Plastipak Holdings, Inc.

- 按地区分類的主要企业

- 北美洲

- Alpha Packaging, Inc.

- COMAR LLC

- Drug Plastics & Glass Company, Inc.

- Pretium Packaging, LLC

- CL Smith Company

- O.Berk Company LLC

- United States Plastic Corporation

- 亚太地区

- Mykron Plus India Pvt. Ltd.

- Zhejiang BI Industrial Co., Ltd.

- Pro-Pac Packaging Ltd

- 欧洲

- Frapak Packaging BV

- Origin Pharma Packaging Ltd

- Weener Plastics Group BV

- Gil Plastic Products Ltd

- 北美洲

The Global Pharmaceutical Plastic Bottles Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 3.9% to reach USD 14.4 billion in 2035.

The market is expanding due to rising global production of generic drugs, continuous growth of oral solid dosage forms, and increasing consumption of over-the-counter (OTC) medicines. The ongoing transition from glass to lightweight high-density polyethylene (HDPE) packaging, coupled with rising outsourcing to contract manufacturing organizations (CMOs), is also driving demand. Regulatory mandates for child-resistant and tamper-evident packaging, along with sustainability initiatives promoting recyclable and PCR-based bottles, are further stimulating growth. North America and Asia-Pacific are experiencing heightened OTC demand driven by self-medication trends, pharmacy network expansion, and growth in the nutraceutical segment. The use of plastic bottles provides key advantages, including safety, tamper evidence, and lightweight design, which continues to support high turnover and consistent demand in retail and pharmacy channels worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $14.4 Billion |

| CAGR | 3.9% |

The oral solid bottles segment reached USD 3.6 billion in 2025. These bottles remain critical as tablets and capsules account for the highest prescription volumes globally, particularly for chronic conditions. They offer moisture protection, bulk packaging efficiency, and compatibility with child-resistant closures, making them essential for large-scale pharmaceutical production and distribution networks.

The high-density polyethylene (HDPE) segment accounted for 38.2% share in 2025. HDPE is preferred for its excellent moisture barrier properties, chemical resistance, durability, and lightweight nature, making it highly suitable for packaging tablets, capsules, and powders. Its cost-effective transport and compliance with pharmaceutical stability requirements make it the material of choice in regulated markets across North America, Europe, and Asia.

North America Pharmaceutical Plastic Bottles Market held 39.7% share in 2025. Growth in this region is supported by rising prescription drug consumption, stricter drug safety regulations, and the shift to lightweight, shatter-resistant packaging. Regulatory oversight from the FDA and Health Canada requires adherence to child-resistant and tamper-evident standards, which drives demand for HDPE and polypropylene pharmaceutical bottles.

Prominent players in the Global Pharmaceutical Plastic Bottles Market include ALPLA Group, Amcor plc, Alpha Packaging, Inc., AptarGroup, Inc., COMAR LLC, Drug Plastics & Glass Company, Inc., C.L. Smith Company, Frapak Packaging B.V., Gerresheimer AG, Gil Plastic Products Ltd, Mykron Plus India Pvt. Ltd., O.Berk Company LLC, Origin Pharma Packaging Ltd, Plastipak Holdings, Inc., Pretium Packaging, LLC, Pro-Pac Packaging Ltd, Silgan Holdings Inc., United States Plastic Corporation, Weener Plastics Group BV, and Zhejiang B.I. Industrial Co., Ltd. Companies in the Global Pharmaceutical Plastic Bottles Market are employing multiple strategies to strengthen their foothold and expand their global presence. These include investing in R&D to develop child-resistant, tamper-evident, and PCR-based packaging solutions that align with sustainability trends. Firms are forming strategic alliances with CMOs and pharmaceutical companies to secure long-term contracts and increase production capacity. Expansion of regional manufacturing facilities ensures faster delivery and cost optimization. Companies are also implementing advanced quality control systems and regulatory compliance protocols to meet international standards, enhancing brand reliability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Bottle type trends

- 2.2.2 Material type trends

- 2.2.3 Bottle capacity trends

- 2.2.4 Closure type trends

- 2.2.5 End-user trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global generic drug production volumes

- 3.2.1.2 Growth in oral solid dosage consumption

- 3.2.1.3 Increasing OTC medicine demand globally

- 3.2.1.4 Shift from glass to lightweight HDPE bottles

- 3.2.1.5 Expansion of contract manufacturing organizations (CMOs)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatile resin prices (HDPE, PET, PP)

- 3.2.2.2 Stringent extractables and leachables compliance

- 3.2.3 Market opportunities

- 3.2.3.1 Bio-based polymer adoption in pharma packaging

- 3.2.3.2 Smart packaging with anti-counterfeit features

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Bottle Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Oral solid bottles

- 5.3 Oral liquid bottles

- 5.4 Ophthalmic bottles

- 5.5 Parenteral/injectable vials

- 5.6 Nasal spray bottles

- 5.7 Topical/dermal bottles

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 High-density polyethylene (HDPE)

- 6.3 Low-density polyethylene (LDPE)

- 6.4 Polypropylene (PP)

- 6.5 Polyethylene terephthalate (PET)

- 6.6 Polyethylene terephthalate glycol (PETG)

- 6.7 Cyclic olefin polymer (COP) & cyclic olefin copolymer (COC)

Chapter 7 Market Estimates and Forecast, By Bottle Capacity, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Micro bottles (5ml - 20ml)

- 7.3 Small bottles (30ml - 100ml)

- 7.4 Medium bottles (120ml - 300ml)

- 7.5 Large bottles (500ml - 1000ml)

- 7.6 Extra-large bottles (>1000ml)

Chapter 8 Market Estimates and Forecast, By Closure Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Continuous thread (screw) closures

- 8.3 Snap-on closures

- 8.4 Dispensing closures

- 8.5 Specialty closures

Chapter 9 Market Estimates and Forecast, By End-User, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Pharmaceutical manufacturers (in-house production)

- 9.3 Contract manufacturing organizations (CMO/CDMO)

- 9.4 Nutraceutical & dietary supplement manufacturers

- 9.5 Healthcare institutions

- 9.6 Compounding pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Gerresheimer AG

- 11.1.2 Amcor plc

- 11.1.3 AptarGroup, Inc.

- 11.1.4 ALPLA Group

- 11.1.5 Silgan Holdings Inc.

- 11.1.6 Plastipak Holdings, Inc.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Alpha Packaging, Inc.

- 11.2.1.2 COMAR LLC

- 11.2.1.3 Drug Plastics & Glass Company, Inc.

- 11.2.1.4 Pretium Packaging, LLC

- 11.2.1.5 C.L. Smith Company

- 11.2.1.6 O.Berk Company LLC

- 11.2.1.7 United States Plastic Corporation

- 11.2.2 Asia Pacific

- 11.2.2.1 Mykron Plus India Pvt. Ltd.

- 11.2.2.2 Zhejiang B.I. Industrial Co., Ltd.

- 11.2.2.3 Pro-Pac Packaging Ltd

- 11.2.3 Europe

- 11.2.3.1 Frapak Packaging B.V.

- 11.2.3.2 Origin Pharma Packaging Ltd

- 11.2.3.3 Weener Plastics Group BV

- 11.2.3.4 Gil Plastic Products Ltd

- 11.2.1 North America