|

市场调查报告书

商品编码

1998849

毛毡纤维市场机会、成长要素、产业趋势分析及2026-2035年预测Tackifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

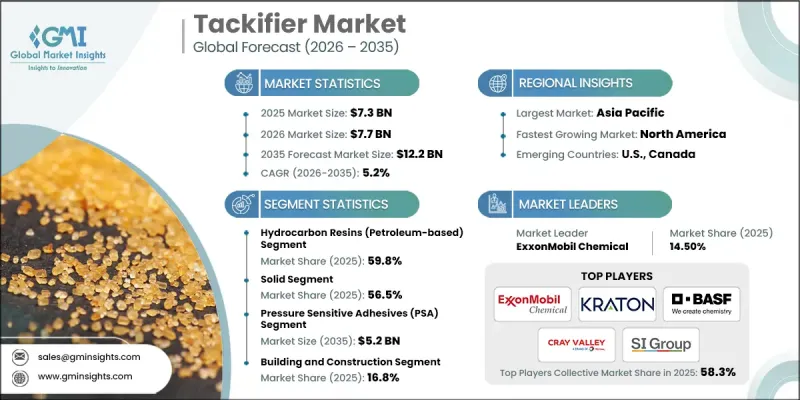

预计到 2025 年,全球黏性纤维市场价值将达到 73 亿美元,并有望以 5.2% 的复合年增长率成长,到 2035 年达到 122 亿美元。

黏性纤维市场的成长主要得益于多个工业领域对黏合技术的需求不断增长,这些领域依赖黏合技术来提升产品性能和耐久性。黏性纤维在提升各种黏合剂配方(贯穿整个製造环境)的黏合强度、柔软性和长期稳定性方面发挥着至关重要的作用。在终端用户领域中,包装产业占据最大的消费份额,其次是建筑施工、汽车製造、不织布以及木工和家具製造。随着人们对环境永续性和法规遵循的日益关注,製造商正在开发能够减少排放并提升环境性能的树脂。随着环境法规日趋严格,为了满足不断变化的标准,业界正越来越多地采用低挥发性有机化合物(VOC)和生物基黏性材料。从区域来看,亚太地区凭藉其完善的製造基础设施、强大的工业生产能力以及对研发活动的持续投入,占据了全球最大的销售份额。同时,欧洲黏性纤维市场正透过开发环保高性能树脂技术而蓬勃发展。北美市场成长最快,这主要得益于工业活动的扩张、城市发展的推进以及包装和不织布用黏合剂产品消费量的成长。拉丁美洲和中东及非洲在全球市场中所占份额相对较小,但预计这两个地区在预测期内都将保持稳定温和的成长。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 73亿美元 |

| 预计金额 | 122亿美元 |

| 复合年增长率 | 5.2% |

预计到2025年,松香树脂市场规模将达到27亿美元,仍将是黏合剂配方中最重要的天然树脂类别之一。松香基材料因其优异的黏合性能和对众多工业应用的适应性而被广泛应用。多种加工技术已被应用于改善这些材料的性能,包括透过化学改质来增强其稳定性和抗氧化性。此外,还开发了多种衍生配方,以提高其与各种聚合物系统和黏合剂组合物的相容性,使製造商能够在广泛的工业领域中获得更佳的黏合性能和配方柔软性。

预计到2025年,固体黏性纤维的市占率将达到56.5%,并在2026年至2035年间以4.9%的复合年增长率成长。固体黏性纤维因其在储存和处理过程中具有高稳定性,并在整个黏合剂生产过程中保持性能稳定,而备受青睐。其物理特性使製造商能够更有效地控制热处理过程中的黏度和软化特性。因此,这些材料广泛应用于需要可靠黏合强度和可预测加工性能的黏合剂系统中。其耐久性和与工业生产方法的兼容性持续推动其在多个製造领域的广泛应用。

预计到2025年,北美黏性纤维市场规模将达到18亿美元。该地区强大的工业基础设施以及主要化工企业持续的研发投入,正推动着产业的创新发展。各公司日益专注于开发特殊树脂技术,例如氢化树脂和高性能混炼技术,旨在提升产品的稳定性和耐久性。然而,该地区市场仍易受价格波动的影响,尤其是树脂生产中使用的石油衍生原料的价格波动。原材料成本的波动会影响製造成本,并最终影响全部区域的市场动态。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 对压敏黏着剂(PSA)的需求增加

- 包装和电子商务行业的成长

- 建筑业和汽车业的扩张

- 产业潜在风险与挑战

- 原油和原料价格波动

- 严格的环境法规和挥发性有机化合物(VOC)法规

- 替代黏合技术的可用性

- 市场机会

- 对生物基和永续树脂的需求日益增长

- 亚太地区的快速工业化

- 氢化树脂和特殊树脂的最新进展

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依化学类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 考虑碳足迹

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依化学性质划分,2022-2035年

- 烃类树脂(石油基)

- C5脂肪族树脂

- C9芳香树脂

- C5/C9混合脂肪族/芳香族树脂

- DCPD(二环戊二烯)树脂

- 氢化烃类树脂

- 松香树脂(天然)

- 松香酸

- 松香酯

- 萜烯树脂

- 聚萜烯树脂

- 氢化萜烯树脂

- 苯乙烯改质萜烯树脂

- 萜烯酚树脂

第六章 市场估计与预测:依类型划分,2022-2035年

- 固体的

- 液体

- 树脂分散体

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 压敏黏着剂(PSA)

- 黏合剂(HMA)

- 组装黏合剂

- 装订黏合剂

- 鞋类、皮革和橡胶黏合剂

- 其他的

第八章 市场估算与预测:依最终使用者划分,2022-2035年

- 包装

- 建筑/施工

- 车

- 不织布

- 木工和家具

- 鞋类

- 其他的

第九章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Arakawa Chemical Industries Ltd.

- BASF SE

- Cray Valley

- DRT(Derives Resiniques et Terpeniques)

- Eastman Chemical Company

- ExxonMobil Chemical

- Foreverest Resources Ltd.

- Kolon Industries Inc.

- Kraton Corporation

- Lawter Inc.

- Neville Chemical Company

- Resin Solutions LLC

- SI Group Inc.

- Yasuhara Chemical Co. Ltd.

- ZEON Corporation

The Global Tackifier Market was valued at USD 7.3 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 12.2 billion by 2035.

Growth in the tackifier market is driven by rising demand from multiple industrial sectors that rely on adhesive technologies to enhance product performance and durability. Tackifiers play an important role in improving adhesion strength, flexibility, and long-term stability within various adhesive formulations used across manufacturing environments. Among end-use sectors, packaging represents the largest share of consumption, followed by building and construction, automotive production, non-woven materials, and woodworking or furniture manufacturing. Increasing focus on environmental sustainability and regulatory compliance is encouraging manufacturers to develop resins with reduced emissions and improved ecological profiles. As environmental regulations become stricter, industries are increasingly adopting low-VOC and bio-based tackifying materials to meet evolving standards. Regionally, Asia Pacific generates the largest share of global revenue due to its extensive manufacturing infrastructure, strong industrial production capacity, and continuous investment in research and development activities. Meanwhile, the European tackifier market is advancing through the development of environmentally responsible high-performance resin technologies. North America is witnessing the fastest growth, supported by expanding industrial activities, increasing urban development, and rising consumption of adhesive products used in packaging and non-woven materials. Although Latin America and the Middle East & Africa represent comparatively smaller portions of the global market, both regions are anticipated to demonstrate consistent and gradual growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.3 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.2% |

The rosin resins segment generated USD 2.7 billion in 2025 and remains one of the most important natural resin categories used in adhesive formulations. Rosin-based materials are widely utilized due to their effective bonding properties and adaptability in numerous industrial applications. Several processing techniques are applied to improve the performance characteristics of these materials, including chemical modifications that enhance stability and resistance to oxidation. In addition, various derivative formulations are developed to improve compatibility with different polymer systems and adhesive compositions, allowing manufacturers to achieve improved bonding performance and formulation flexibility across multiple industries.

The solid tackifier segment accounted for 56.5% share in 2025 and is projected to grow at a CAGR of 4.9% between 2026 and 2035. Solid-form tackifiers remain widely preferred because they offer greater stability during storage and handling while maintaining consistent performance during adhesive production. Their physical properties allow manufacturers to control viscosity levels and softening characteristics more effectively during thermal processing. As a result, these materials are commonly incorporated into hot-melt adhesive systems that require dependable bonding strength and predictable processing behavior. Their durability and compatibility with industrial production methods continue to support widespread adoption across multiple manufacturing sectors.

North America Tackifier Market generated USD 1.8 billion in 2025. Strong industrial infrastructure and consistent investment in research and development by major chemical manufacturers support ongoing innovation within the region. Companies are increasingly focusing on developing specialized resin technologies, including hydrogenated and advanced performance formulations designed to improve product stability and durability. However, the regional market remains sensitive to fluctuations in raw material pricing, particularly those associated with petroleum-derived inputs used in resin production. Variability in feedstock costs can influence manufacturing expenses and ultimately affect market dynamics across the region.

Major companies operating in the Global Tackifier Market include BASF SE, Eastman Chemical Company, ExxonMobil Chemical, Kraton Corporation, SI Group Inc., Kolon Industries Inc., ZEON Corporation, Arakawa Chemical Industries Ltd., Yasuhara Chemical Co. Ltd., Lawter Inc., Neville Chemical Company, DRT (Derives Resiniques et Terpeniques), Cray Valley, Foreverest Resources Ltd., and Resin Solutions LLC. Companies competing in the Tackifier Market are strengthening their market presence through continuous innovation, strategic partnerships, and capacity expansion initiatives. Many manufacturers are investing in research and development to create advanced tackifying resins that offer improved bonding performance while meeting evolving environmental standards. The development of bio-based and low-VOC resin technologies has become a key strategic priority as industries shift toward sustainable production practices. Firms are also expanding production facilities and strengthening supply chain networks to support growing global demand for adhesive materials. Strategic collaborations with adhesive manufacturers enable companies to develop customized resin solutions tailored to specific industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemistry Type

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End User

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Demand for Pressure Sensitive Adhesives (PSA)

- 3.2.1.2 Growth in Packaging & E-commerce Industries

- 3.2.1.3 Expansion of Construction & Automotive Sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in Crude Oil & Raw Material Prices

- 3.2.2.2 Stringent Environmental & VOC Regulations

- 3.2.2.3 Availability of Alternative Adhesive Technologies

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing Demand for Bio-Based & Sustainable Resins

- 3.2.3.2 Rapid Industrialization in Asia Pacific

- 3.2.3.3 Advancements in Hydrogenated & Specialty Resins

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By chemistry type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Chemistry Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hydrocarbon Resins (Petroleum-Based)

- 5.2.1 C5 Aliphatic Resins

- 5.2.2 C9 Aromatic Resins

- 5.2.3 C5/C9 Mixed Aliphatic/Aromatic Resins

- 5.2.4 DCPD (Dicyclopentadiene) Resins

- 5.2.5 Hydrogenated Hydrocarbon Resins

- 5.3 Rosin Resins (Natural)

- 5.3.1 Rosin Acids

- 5.3.2 Rosin Esters

- 5.4 Terpene Resins

- 5.4.1 Polyterpene Resins

- 5.4.2 Hydrogenated Terpene Resins

- 5.4.3 Styrenated Terpene Resins

- 5.4.4 Terpene Phenolic Resins

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Liquid

- 6.4 Resin Dispersion

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Pressure Sensitive Adhesives (PSA)

- 7.3 Hot Melt Adhesives (HMA)

- 7.4 Assembly Adhesives

- 7.5 Bookbinding Adhesives

- 7.6 Footwear, Leather & Rubber Adhesives

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Packaging

- 8.3 Building & Construction

- 8.4 Automotive

- 8.5 Non-Wovens

- 8.6 Woodworking & Furniture

- 8.7 Footwear

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arakawa Chemical Industries Ltd.

- 10.2 BASF SE

- 10.3 Cray Valley

- 10.4 DRT (Derives Resiniques et Terpeniques)

- 10.5 Eastman Chemical Company

- 10.6 ExxonMobil Chemical

- 10.7 Foreverest Resources Ltd.

- 10.8 Kolon Industries Inc.

- 10.9 Kraton Corporation

- 10.10 Lawter Inc.

- 10.11 Neville Chemical Company

- 10.12 Resin Solutions LLC

- 10.13 SI Group Inc.

- 10.14 Yasuhara Chemical Co. Ltd.

- 10.15 ZEON Corporation

全球增稠剂市场规模、份额、趋势和成长分析报告(2026-2034年)

全球增稠剂市场规模、份额、趋势和成长分析报告(2026-2034年) PTOP橡胶增粘剂市场按类型、形态、等级和应用划分,全球预测(2026-2032年)生物基 Tacklyzer 市场按原料来源、产品类型、应用、终端用户产业和分销管道划分,全球预测(2026-2032 年)增黏剂市场 - 全球预测 2025-2030

PTOP橡胶增粘剂市场按类型、形态、等级和应用划分,全球预测(2026-2032年)生物基 Tacklyzer 市场按原料来源、产品类型、应用、终端用户产业和分销管道划分,全球预测(2026-2032 年)增黏剂市场 - 全球预测 2025-2030 增黏剂市场-全球产业规模、份额、趋势、机会与预测,依产品、形式、应用、地区及竞争细分,2020-2030 年预测

增黏剂市场-全球产业规模、份额、趋势、机会与预测,依产品、形式、应用、地区及竞争细分,2020-2030 年预测 增稠剂:市占率分析、产业趋势、统计、成长预测(2025-2030)

增稠剂:市占率分析、产业趋势、统计、成长预测(2025-2030) 增黏剂市场报告:2031 年趋势、预测与竞争分析

增黏剂市场报告:2031 年趋势、预测与竞争分析 增粘剂市场规模、份额、趋势分析报告:按产品、形式、应用、地区、细分市场预测,2024-2030

增粘剂市场规模、份额、趋势分析报告:按产品、形式、应用、地区、细分市场预测,2024-2030