|

市场调查报告书

商品编码

2019033

儿童太阳眼镜市场:商机、成长要素、产业趋势分析及2026-2035年预测Children Sunglasses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

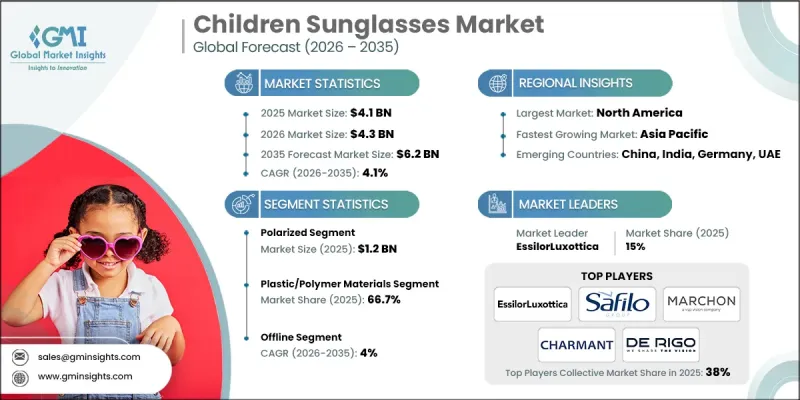

预计到 2025 年,全球儿童太阳眼镜市场价值将达到 41 亿美元,并预计以 4.1% 的复合年增长率成长,到 2035 年达到 62 亿美元。

随着家长对眼部保护意识的不断提高,市场正稳步成长。人们日益关注紫外线对儿童视力的危害,促使儿童从小就配戴防护眼镜产品。此外,可支配收入的增加和生活方式的偏好也推动了对高品质、耐用且美观的儿童专用太阳眼镜的需求。青少年使用电子设备的增加也加剧了人们对视力问题的担忧,进一步强化了对防护解决方案的需求。製造商正积极致力于产品创新以满足消费者的期望,例如推出轻便、抗衝击且符合人体工学设计的太阳眼镜。丰富多样的色彩、款式和设计提升了产品对家长和儿童的吸引力,从而促进了销售成长。此外,数位平台和社群媒体的影响力提高了产品的知名度和可及性,使品牌能够触及更广泛的受众,加速市场成长。

| 市场规模 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 41亿美元 |

| 预测金额 | 62亿美元 |

| 复合年增长率 | 4.1% |

预计到2025年,偏光镜片市场规模将达到12亿美元,并在2026年至2035年间以5.1%的复合年增长率成长。由于家长们越来越意识到偏光镜片能够减少眩光并提升视觉舒适度,因此该细分市场的需求正在不断增长。偏光太阳眼镜适合户外活动,因为它们能够提供清晰的视野并减轻眼睛疲劳。除了镜片技术的不断进步外,专为儿童设计的时尚镜框也进一步推动了该细分市场的扩张。随着消费者对功能性和时尚性的双重重视,偏光太阳眼镜在全球市场的受欢迎程度持续攀升。

预计到2025年,塑胶或聚合物材料眼镜将占据66.7%的市场份额,并在2026年至2035年间以3.8%的复合年增长率成长。这个细分市场非常适合儿童眼镜,充分发挥了聚合物镜框的优势:轻巧、成本绩效且经久耐用。这些材质柔软性好且不易破损,可长期使用。此外,聚合物技术的进步提高了紫外线防护性能,进一步提升了产品的价值。多样化的设计和鲜艳的色彩也增强了产品的吸引力,促使越来越多的家长为孩子寻找舒适、经济实惠且可靠的眼镜产品解决方案。

到2025年,美国儿童太阳眼镜市场占有率将达到76%。该国市场成长的主要驱动力是消费者较高的安全意识、购买力和完善的零售网路。气候和日照时长的区域差异会影响消费者的购买行为。消费者越来越追求兼具防护性和时尚感的高品质产品。此外,先进的分销管道和强大的品牌渗透率也促进了市场的持续扩张。消费者对儿童安全的日益关注以及对长期眼部健康的不断提高,持续推动全美儿童太阳眼镜市场的繁荣发展。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析(基于初步调查)

- 对过去价格趋势的分析(基于初步研究)

- 根据业务类型分類的定价策略(高端/价值/成本加成)(基于初步调查)

- 法律规范

- 紫外线防护标准与安全法规

- 儿童产品安全认证要求(CPSC、EN 1836、AS/NZS 1067)

- 区域标籤和合规要求

- 交易数据分析(基于初步调查)

- 进出口数量和价值趋势(基于初步调查)

- 主要贸易走廊及关税影响(基于初步调查)

- 人工智慧和生成式人工智慧对市场的影响

- 利用人工智慧改造现有经营模式

- GenAI 各细分市场的应用案例与部署蓝图

- 风险、限制和监管考量

- 分销基础设施和通路渗透状况(基于初步调查)

- 按地区和类型(现代零售与传统零售)分類的通路覆盖率(基于初步调查)

- 最后一公里基础设施差异和新分销管道的变化(基于初步研究)

- 波特五力分析

- PESTEL 分析

- 消费行为分析

- 购买模式

- 偏好分析

- 不同地区的消费行为差异

- 电子商务对购买决策的影响

第四章 竞争情势

- 介绍

- 企业市占率分析

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 极化

- 非极化

第六章 市场估算与预测:依框架材料划分,2022-2035年

- 塑胶/聚合物

- 柔软性橡胶

- TR90(热塑性树脂)

- 标准塑胶

- 金属

- 混合材料

第七章 市场估价与预测:依镜片材料划分,2022-2035年

- 聚碳酸酯

- CR-39(烯丙基二甘醇碳酸酯)

- 聚氨酯

- 其他(Trivex、压克力等)

第八章 市场估计与预测:依年龄组别划分,2022-2035年

- 婴儿(0-3岁)

- 学龄前儿童(4-6岁)

- 小学生(7-12岁)

- 青少年(13-17岁)

第九章 市场估计与预测:性别,2022-2035年

- 男生

- 女孩

- 男女通用的

第十章 市场估价与预测:依价格划分,2022-2035年

- 价格低廉(19 美元以下)

- 中价位(20-54美元)

- 高价位(超过 55 美元)

第十一章 市场估计与预测:依应用领域划分,2022-2035年

- 体育和户外活动

- 时尚与生活风格

- 医疗和处方药

第十二章 市场估计与预测:依通路划分,2022-2035年

- 在线的

- 电子商务

- 企业网站

- 离线

- 眼镜专卖店

- 百货公司

- 其他(药局、保健食品店等)

第十三章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十四章:公司简介

- Banz

- Bug+Bean Kids

- Charmant Group

- De Rigo Vision

- EssilorLuxottica

- Julbo

- Marchon Eyewear

- Marcolin Group

- Maui Jim

- Safilo Group

- Smith Optics

- Sun Bum

- Thelios(LVMH)

- Uvex Sports

- Valley Eyewear

The Global Children Sunglasses Market was valued at USD 4.1 billion in 2025 and is estimated to grow at a CAGR of 4.1% to reach USD 6.2 billion by 2035.

The market is gaining steady momentum as awareness among parents regarding eye protection continues to rise. Increasing concerns about the harmful effects of ultraviolet radiation on children's vision are encouraging higher adoption of protective eyewear at an early age. In addition, rising disposable incomes and evolving lifestyle preferences are supporting demand for premium, durable, and aesthetically appealing sunglasses designed specifically for children. The growing use of digital devices among younger populations has also contributed to vision-related concerns, further strengthening the need for protective solutions. Manufacturers are actively focusing on product innovation, introducing lightweight, impact-resistant, and ergonomically designed sunglasses to meet consumer expectations. A wide variety of colors, styles, and designs has improved product appeal among both parents and children, supporting higher sales. Furthermore, digital platforms and social media influence are enhancing product visibility and accessibility, enabling brands to reach a broader audience and accelerate market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 4.1% |

The polarized segment generated USD 1.2 billion in 2025 and is anticipated to grow at a CAGR of 5.1% during 2026-2035. This segment is witnessing increased demand due to growing parental awareness of glare reduction and visual comfort benefits offered by polarized lenses. These sunglasses improve clarity and reduce eye strain, making them suitable for outdoor use. Continuous advancements in lens technology, combined with attractive frame designs tailored for children, are further supporting segment expansion. As consumers prioritize both functionality and style, the adoption of polarized sunglasses continues to strengthen across global markets.

The plastic or polymer materials segment held a 66.7% share in 2025 and is expected to grow at a CAGR of 3.8% from 2026 to 2035. This segment benefits from the lightweight nature, cost-effectiveness, and high durability of polymer-based frames, making them ideal for children's usage. These materials offer flexibility and resistance to breakage, ensuring long-term usability. In addition, advancements in polymer technology have improved UV protection capabilities, further enhancing product value. The availability of diverse designs and vibrant color options also increases product attractiveness, encouraging higher adoption among parents seeking comfortable, affordable, and reliable eyewear solutions for children.

U.S. Children Sunglasses Market accounted for 76% share in 2025. Market growth in the country is supported by strong consumer awareness, high purchasing power, and well-established retail networks. Demand varies across regions due to differences in climate and sunlight exposure, which influences purchasing behavior. Consumers are increasingly inclined toward premium-quality products that offer both protection and style. In addition, the presence of advanced distribution channels and strong brand penetration contributes to sustained market expansion. The focus on child safety, combined with increasing awareness of long-term eye health, continues to drive product adoption across the country.

Key players in the Global Children Sunglasses Market include Banz, Bug + Bean Kids, Charmant Group, De Rigo Vision, EssilorLuxottica, Julbo, Marchon Eyewear, Marcolin Group, Maui Jim, Safilo Group, Smith Optics, Sun Bum, Thelios (LVMH), Uvex Sports, Valley Eyewear. Companies in the children sunglasses market are strengthening their position through continuous product innovation, focusing on lightweight materials, enhanced UV protection, and durable designs. They are expanding their product portfolios with stylish and customizable options to appeal to both children and parents. Strategic collaborations with retailers and e-commerce platforms are improving product accessibility and market reach. Brands are also leveraging digital marketing and social media to increase visibility and consumer engagement. Investments in research and development, along with the introduction of advanced lens technologies, help maintain a competitive advantage. Additionally, companies are focusing on affordability, sustainability, and brand differentiation to build long-term customer loyalty and expand their global footprint.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Type

- 2.2.3 By Frame Material

- 2.2.4 By Lens Material

- 2.2.5 By Age Group

- 2.2.6 By Gender

- 2.2.7 By Price

- 2.2.8 By Application

- 2.2.9 By Distribution Channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (Driven by Primary Research)

- 3.6.1 Historical price trend analysis (Driven by Primary Research)

- 3.6.2 Pricing strategy by player type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.7 Regulatory framework

- 3.7.1 UV protection standards & safety regulations

- 3.7.2 Child product safety certification requirements (CPSC, EN 1836, AS/NZS 1067)

- 3.7.3 Labeling & compliance requirements by region

- 3.8 Trade data analysis (Driven by Primary Research)

- 3.8.1 Import/export volume & value trends (Driven by Primary Research)

- 3.8.2 Key trade corridors & tariff impact (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 AI-driven disruption of existing business models

- 3.9.2 GenAI use cases & adoption roadmap by segment

- 3.9.3 Risks, limitations & regulatory considerations

- 3.10 Distribution infrastructure & channel penetration landscape (Driven by Primary Research)

- 3.10.1 Channel coverage by region & format (Modern vs. Traditional Trade) (Driven by Primary Research)

- 3.10.2 Last-mile infrastructure gaps & emerging channel shifts (Driven by Primary Research)

- 3.11 Porter's five forces analysis

- 3.12 PESTEL analysis

- 3.13 Consumer behavior analysis

- 3.13.1 Purchasing patterns

- 3.13.2 Preference analysis

- 3.13.3 Regional variations in consumer behavior

- 3.13.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Polarized

- 5.3 Non-polarized

Chapter 6 Market Estimates & Forecast, By Frame Material, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Plastic/polymer

- 6.2.1 Flexible rubber

- 6.2.2 TR90 (thermoplastic)

- 6.2.3 Standard plastic

- 6.3 Metal

- 6.4 Hybrid materials

Chapter 7 Market Estimates & Forecast, By Lens Material, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Polycarbonate

- 7.3 CR-39 (allyl diglycol carbonate)

- 7.4 Polyurethane

- 7.5 Others (trivex, acrylic etc.)

Chapter 8 Market Estimates & Forecast, By Age Group, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Toddlers (0-3 years)

- 8.3 Pre-school (4-6 years)

- 8.4 Primary school (7-12 years)

- 8.5 Teenagers (13-17 years)

Chapter 9 Market Estimates & Forecast, By Gender, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Boys

- 9.3 Girls

- 9.4 Unisex

Chapter 10 Market Estimates & Forecast, By Price, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Low (under $19)

- 10.3 Medium ($20-$54)

- 10.4 High ($55 and above)

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 Sports and outdoor activities

- 11.3 Fashion and lifestyle

- 11.4 Medical/prescription

Chapter 12 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 12.1 Key trends

- 12.2 Online

- 12.2.1 E-commerce

- 12.2.2 Company websites

- 12.3 Offline

- 12.3.1 Optical specialty stores

- 12.3.2 Department stores

- 12.3.3 Others (pharmacy and health stores etc.)

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Spain

- 13.3.5 Italy

- 13.3.6 Netherlands

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 Japan

- 13.4.3 India

- 13.4.4 Australia

- 13.4.5 South Korea

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Banz

- 14.2 Bug + Bean Kids

- 14.3 Charmant Group

- 14.4 De Rigo Vision

- 14.5 EssilorLuxottica

- 14.6 Julbo

- 14.7 Marchon Eyewear

- 14.8 Marcolin Group

- 14.9 Maui Jim

- 14.10 Safilo Group

- 14.11 Smith Optics

- 14.12 Sun Bum

- 14.13 Thelios (LVMH)

- 14.14 Uvex Sports

- 14.15 Valley Eyewear

太阳眼镜市场报告:按类型、设计、镜框材料、镜片材料、销售管道、最终用户和地区划分(2026-2034 年)

太阳眼镜市场报告:按类型、设计、镜框材料、镜片材料、销售管道、最终用户和地区划分(2026-2034 年) 紫外线防护眼镜市场:依产品类型、镜片材料、防护等级、通路和最终用户划分-2026-2032年全球预测

紫外线防护眼镜市场:依产品类型、镜片材料、防护等级、通路和最终用户划分-2026-2032年全球预测 全球太阳眼镜市场规模、份额、趋势和成长分析报告(2026-2034年)

全球太阳眼镜市场规模、份额、趋势和成长分析报告(2026-2034年) 全球奢侈太阳眼镜市场-产业规模、份额、趋势、机会与预测:按类型、最终用户、销售管道、地区和竞争格局划分,2021-2031年太阳眼镜市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、销售管道、地区及竞争格局划分,2021-2031年)太阳眼镜袋市场 - 全球产业规模、份额、趋势、机会、预测:按类型、材料、分销管道、地区和竞争格局划分,2021-2031年骑乘太阳眼镜市场-全球产业规模、份额、趋势、机会及预测(按类型、最终用户、分销管道、地区和竞争格局划分,2021-2031年)全球处方太阳眼镜市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)日本太阳眼镜市场报告(按类型、设计、镜框材料、镜片材料、配销通路、最终用户和地区划分,2026-2034年)

全球奢侈太阳眼镜市场-产业规模、份额、趋势、机会与预测:按类型、最终用户、销售管道、地区和竞争格局划分,2021-2031年太阳眼镜市场 - 全球产业规模、份额、趋势、机会及预测(按产品类型、销售管道、地区及竞争格局划分,2021-2031年)太阳眼镜袋市场 - 全球产业规模、份额、趋势、机会、预测:按类型、材料、分销管道、地区和竞争格局划分,2021-2031年骑乘太阳眼镜市场-全球产业规模、份额、趋势、机会及预测(按类型、最终用户、分销管道、地区和竞争格局划分,2021-2031年)全球处方太阳眼镜市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)日本太阳眼镜市场报告(按类型、设计、镜框材料、镜片材料、配销通路、最终用户和地区划分,2026-2034年) 电动变色太阳眼镜:全球市场份额及排名、总收入及需求预测(2025-2031年)

电动变色太阳眼镜:全球市场份额及排名、总收入及需求预测(2025-2031年)