|

市场调查报告书

商品编码

2019100

食用油及脂肪市场机会、成长要素、产业趋势分析及2026-2035年预测。Edible Oils and Fats Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

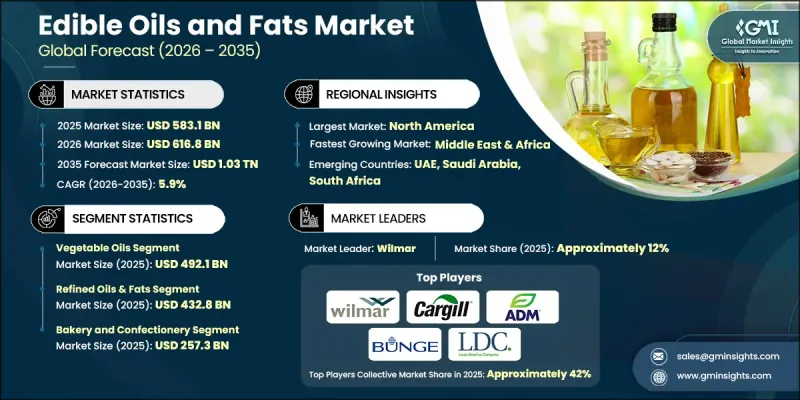

预计到 2025 年,全球食用油和脂肪市场价值将达到 5,831 亿美元,并以 5.9% 的复合年增长率增长,到 2035 年将达到 1.03 兆美元。

食用油脂,包括大豆油、橄榄油和棕榈油等植物来源,以及黄油和猪油等动物来源油脂,在烹饪、烘焙和食品生产中发挥至关重要的作用。它们赋予食物风味、口感和营养价值,是加工食品、零食、糖果甜点和其他烹饪应用的主要原料。消费者对富含不饱和脂肪酸的健康油脂(如橄榄油、葵花籽油和芥花籽油)的偏好日益增长,推动了市场扩张,而棕榈油的价格优势和用途广泛也支撑着市场需求。素食和植物来源饮食的日益普及,正推动人们从动物油脂转向植物油脂。此外,消费者对有机、非基因改造和永续来源产品的日益关注,也促使生产商采用环保的生产方式,以满足不断变化的消费者需求,并拓展全球市场机会。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 5831亿美元 |

| 预测金额 | 1.03兆美元 |

| 复合年增长率 | 5.9% |

预计到2025年,植物油市场规模将达到4,921亿美元,并在2026年至2035年间以10.1%的复合年增长率成长。消费者对植物来源产品、洁净标示产品以及更健康烹饪方式的需求不断增长,是推动该市场成长的主要动力。植物油在加工食品、烘焙产品、糖果甜点以及餐饮服务业的广泛应用,也促进了其市场的稳定成长。消费者对强化植物油和冷压植物油的日益青睐,也为零售和商用通路的长期成长奠定了基础。

预计到2025年,精炼油脂市场规模将达到4,328亿美元,并在2035年之前以6.1%的复合年增长率成长。其品质稳定、保质期长、用途广泛,适用于多种烹饪方式,因此在家庭和食品行业中广泛应用。精炼过程提高了油脂的纯度,标准化了其风味特征,满足了消费者对安全、可靠、高品质且适合日常使用的油脂的需求。

预计到2025年,北美食用油和脂肪市场规模将达到1,964亿美元,主要受加工食品、烘焙产品和速食食品需求的推动。消费者越来越倾向选择低反式脂肪、植物来源和洁净标示的产品,这促使生产商更加重视研发更健康的配方并拓展零售通路。

目录

第一章:调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监理情势

- 波特五力分析

- PESTEL 分析

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利趋势

- 贸易统计

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续倡议

- 减少废弃物策略

- 生产中的能源效率

- 环保意识的倡议

- 关于碳足迹的考量

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依类型划分,2022-2035年

- 植物油

- 棕榈油

- 大豆油

- 菜籽油

- 芥末油

- 椰子油

- 动物脂肪和油脂

- 脂

- 猪油

- 酥油

- 其他的

第六章 市场估算与预测:依加工方式划分,2022-2035年

- 初榨油/冷压

- 精炼油脂

- 加工油脂

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 麵包糖果甜点

- 小吃

- 肉品

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- ACH食品公司

- ADM

- Bunge

- Cargill

- Fuji Oil

- GrainCorp

- IOI Corporation

- Louis Dreyfus Company

- Nisshin Oillio

- Wilmar

The Global Edible Oils and Fats Market was valued at USD 583.1 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 1.03 trillion by 2035.

Edible oils and fats, derived from both plant sources such as soybean, olive, and palm oils, and animal sources like butter and lard, play a vital role in cooking, baking, and food manufacturing. They contribute flavor, texture, and nutritional benefits while serving as key ingredients across processed foods, snacks, confectionery, and other culinary applications. Rising consumer preference for healthier oils high in unsaturated fats, such as olive, sunflower, and canola, is driving market expansion, while affordability and versatility sustain demand for palm oil. The popularity of vegan and plant-based diets is encouraging the shift from animal fats to plant oils. Additionally, growing interest in organic, non-GMO, and sustainably sourced products is prompting manufacturers to adopt eco-friendly production practices, catering to evolving consumer priorities and expanding global market opportunities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $583.1 Billion |

| Forecast Value | $1.03 Trillion |

| CAGR | 5.9% |

The vegetable oils segment was valued at USD 492.1 billion in 2025 and is expected to grow at a CAGR of 10.1% during 2026-2035. Rising demand for plant-based options, clean-label products, and healthier cooking alternatives is driving the growth of this segment. Its widespread application in packaged foods, bakery products, confectionery products, and foodservice operations ensures steady adoption. Fortified and cold-pressed products are increasingly favored by consumers, sustaining long-term growth in retail and commercial channels.

The refined oils and fats segment accounted for USD 432.8 billion in 2025 and is anticipated to grow at a CAGR of 6.1% through 2035. Its consistent quality, extended shelf life, and adaptability across cooking methods make it popular among households and the food industry. Refining processes enhance purity and standardize flavor profiles, meeting consumer demand for safe, reliable, and high-quality oils suitable for daily use.

North America Edible Oils and Fats Market generated USD 196.4 billion in 2025, driven by demand from processed foods, baked goods, and convenience meals. Consumers are increasingly seeking low-trans-fat, plant-based, and clean-label products, prompting manufacturers to focus on healthier formulations and diversified retail distribution.

Key players in the Global Edible Oils and Fats Market include ADM, Fuji Oil, Wilmar, ACH Food Companies, Louis Dreyfus Company, GrainCorp, Bunge, Cargill, IOI Corporation, Nisshin Oillio, among others. Companies in the Edible Oils and Fats Market are pursuing strategies such as expanding production capacity, investing in advanced extraction and refining technologies, and enhancing supply chain efficiency to strengthen market presence. Product diversification, including plant-based, cold-pressed, and fortified oils, allows firms to target health-conscious and premium consumer segments. Sustainability initiatives, such as eco-friendly sourcing and reduced carbon footprint practices, are increasingly prioritized. Strategic partnerships with food manufacturers and retailers secure long-term distribution channels, while research and development focus on improving oil quality, flavor consistency, and shelf life to meet evolving consumer expectations. These approaches help companies maintain competitiveness and drive market growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Processing Type

- 2.2.4 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022- 2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Vegetable oils

- 5.2.1 Palm oil

- 5.2.2 Soybean oil

- 5.2.3 Rapeseed oil

- 5.2.4 Mustard oil

- 5.2.5 Coconut oil

- 5.3 Animal fats

- 5.3.1 Tallow

- 5.3.2 Lard

- 5.3.3 Ghee

- 5.3.4 Others

Chapter 6 Market Estimates and Forecast, By Processing Type, 2022- 2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Virgin/Cold-Pressed Oils

- 6.3 Refined Oils & Fats

- 6.4 Modified Fats

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery and Confectionery

- 7.3 Snacks

- 7.4 Meat products

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 ACH Food Companies

- 9.2 ADM

- 9.3 Bunge

- 9.4 Cargill

- 9.5 Fuji Oil

- 9.6 GrainCorp

- 9.7 IOI Corporation

- 9.8 Louis Dreyfus Company

- 9.9 Nisshin Oillio

- 9.10 Wilmar