|

市场调查报告书

商品编码

1413841

α-烯烃市场:按类型、应用分类 - 2024-2030 年全球预测Alpha Olefins Market by Type (1-Butene, 1-Hexene, 1-Octene), Application (Lubricants, Oil Field Chemicals, Polyolefins Comonomer) - Global Forecast 2024-2030 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

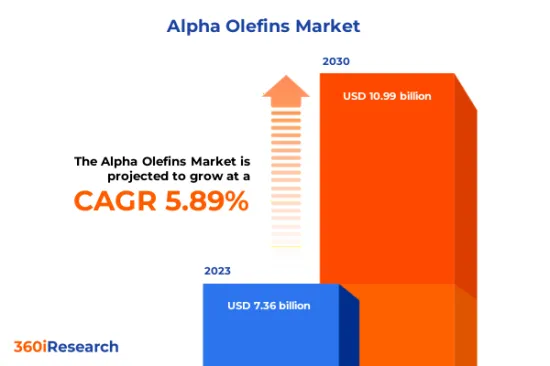

预计2023年α-烯烃市场规模为73.6亿美元,预计2024年将达77.8亿美元,2030年将达到109.9亿美元,复合年增长率为5.89%。

全球α-烯烃市场

| 主要市场统计 | |

|---|---|

| 基准年[2023] | 73.6亿美元 |

| 预测年份 [2024] | 77.8亿美元 |

| 预测年份 [2030] | 109.9亿美元 |

| 复合年增长率(%) | 5.89% |

α-烯烃是一类有机化合物,其特征在于其分子结构中碳原子之间存在双键。这些化学物质源自石化原料,例如乙烯、丙烯和其他烯烃衍生物。聚乙烯因其独特的性能(例如反应性、多功能性和生物分解性)而在各个工业领域中得到广泛应用。包装应用中对聚乙烯的需求不断增长是一个关键驱动因素,因为它具有出色的防潮和气体阻隔性能,同时提供设计选项的弹性。此外,汽车应用中越来越多地采用低黏度合成油润滑油,推动了对高分子量锁状α-烯烃的需求。原油价格波动直接影响LAO生产的原料成本,使得生产者难以维持稳定的价格结构。石化原料价格的波动可能会加剧供应商之间的价格竞争并降低报酬率,从而进一步限制市场成长。加强利用植物油和木质纤维素生物质等可再生原料生产 LAO 的生物方法的研究,为市场成长提供了机会。

区域洞察

在美洲,美国是α-烯烃的主要生产国,因为它是丰富的页岩气供应国。页岩气开采的扩大增加了生产α-烯烃所需原料的可得性。美洲国家的消费者需求是由包装和汽车工业要求的聚乙烯生产等应用所推动的。在欧盟国家,严格的环境法规正在推动使用 α-烯烃生产聚合物的永续解决方案的创新。由于锁状α-烯烃 (LAO) 在高性能聚乙烯产品(主要是汽车和包装行业)中的使用,对线性 α-烯烃 (LAO) 的需求不断增加。研究计划透过资助和促进学术界与工业界之间的合作支持了这一领域的进展。中东拥有丰富的碳氢化合物蕴藏量,对世界α-烯烃生产做出了巨大贡献。该地区拥有许多生产 LAO 的大型石化联合企业。在亚太地区,中国、日本和印度是α-烯烃的主要生产国。由于汽车、建筑和包装行业的扩张,对α-烯烃的需求持续增加。

FPNV定位矩阵

FPNV定位矩阵对于评估α-烯烃市场至关重要。我们检视与业务策略和产品满意度相关的关键指标,以对供应商进行全面评估。这种深入的分析使用户能够根据自己的要求做出明智的决策。根据评估,供应商被分为四个成功程度不同的像限:前沿(F)、探路者(P)、利基(N)和重要(V)。

市场占有率分析

市场占有率分析是一种综合工具,可以对 α 烯烃市场供应商的现状进行深入而详细的研究。全面比较和分析供应商在整体收益、基本客群和其他关键指标方面的贡献,以便更好地了解公司的绩效及其在争夺市场占有率时面临的挑战。此外,该分析还提供了对该行业竞争特征的宝贵考察,包括在研究基准年观察到的累积、分散主导地位和合併特征等因素。这种详细程度的提高使供应商能够做出更明智的决策并制定有效的策略,从而在市场上获得竞争优势。

本报告在以下方面提供了宝贵的见解:

1-市场渗透率:提供有关主要企业所服务的市场的全面资讯。

2-市场开拓:我们深入研究利润丰厚的新兴市场,并分析它们在成熟细分市场中的渗透率。

3- 市场多元化:提供有关新产品发布、开拓地区、最新发展和投资的详细资讯。

4-竞争力评估与资讯:对主要企业的市场占有率、策略、产品、认证、监管状况、专利状况、製造能力等进行全面评估。

5- 产品开发与创新:提供对未来技术、研发活动和突破性产品开发的见解。

本报告解决了以下关键问题:

1-α烯烃市场的市场规模和预测是多少?

在 2-α 烯烃市场预测期间内,有哪些产品、细分市场、应用和领域值得考虑投资?

3-α-烯烃市场的技术趋势和法律规范是什么?

4-α-烯烃市场主要供应商的市场占有率是多少?

进入5-α烯烃市场的适当型态和策略手段是什么?

目录

第一章 前言

第二章调查方法

第三章执行摘要

第四章市场概况

第五章市场洞察

- 市场动态

- 促进因素

- α-烯烃在造纸和纸浆工业的应用不断增加

- 全球页岩气产量增加

- 各行业对合成润滑油的需求不断成长

- 抑制因素

- 原油价格波动

- 机会

- α-烯烃生产不断取得进展

- 生物基α-烯烃的开发

- 任务

- 使用 α 烯烃的严格环境法规

- 促进因素

- 市场区隔分析

- 类型:弹性和电阻率增加了 1-Butene在聚合物生产中的使用

- 应用:扩大 α-烯烃在润滑油生产的使用

- 市场趋势分析

- 高通膨的累积效应

- 波特五力分析

- 价值炼和关键路径分析

- 法律规范

第六章α-烯烃市场:依类型

- 1-Butene

- 1-己烯

- 1-Octene

第七章α-烯烃市场:依应用分类

- 润滑剂

- 油田化学品

- 聚烯烃共聚单体

- 界面活性剂及中间体

- 鞣革油

第八章美洲α-烯烃市场

- 阿根廷

- 巴西

- 加拿大

- 墨西哥

- 美国

第九章亚太地区α-烯烃市场

- 澳洲

- 中国

- 印度

- 印尼

- 日本

- 马来西亚

- 菲律宾

- 新加坡

- 韩国

- 台湾

- 泰国

- 越南

第十章欧洲、中东和非洲α-烯烃市场

- 丹麦

- 埃及

- 芬兰

- 法国

- 德国

- 以色列

- 义大利

- 荷兰

- 奈及利亚

- 挪威

- 波兰

- 卡达

- 俄罗斯

- 沙乌地阿拉伯

- 南非

- 西班牙

- 瑞典

- 瑞士

- 土耳其

- 阿拉伯聯合大公国

- 英国

第十一章竞争形势

- FPNV定位矩阵

- 市场占有率分析:主要企业

- 主要企业竞争情境分析

- 投资、资金筹措

- 奖项/奖励/扩展

第12章竞争产品组合

- 主要公司简介

- Borealis AG

- Chevron Phillips Chemical Company LLC

- Dowpol Chemical International Corp.

- Evonik Industries AG

- Exxon Mobil Corporation

- Idemitsu Kosan Co.,Ltd.

- INEOS AG

- JAM Petrochemical Co.

- Lanxess AG

- LyondellBasell Industries NV

- Mitsubishi Chemical Corporation

- Mitsui Chemicals, Inc.

- PS CHEMICALS

- PJSC Nizhnekamskneftekhim

- Qatar Chemical Company Ltd.

- SABIC

- Sasol Limited

- Shell International BV

- Tokyo Chemical Industry Co.

- TPC Group

- 主要产品系列

第十三章附录

- 讨论指南

- 关于许可证和定价

[193 Pages Report] The Alpha Olefins Market size was estimated at USD 7.36 billion in 2023 and expected to reach USD 7.78 billion in 2024, at a CAGR 5.89% to reach USD 10.99 billion by 2030.

Global Alpha Olefins Market

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2023] | USD 7.36 billion |

| Estimated Year [2024] | USD 7.78 billion |

| Forecast Year [2030] | USD 10.99 billion |

| CAGR (%) | 5.89% |

Alpha Olefins are a class of organic compounds characterized by double bonds between the carbon atoms in their molecular structure. These chemicals are derived from petrochemical feedstocks such as ethylene, propylene, and other olefin derivatives. They are used in numerous applications across various industries due to their unique properties, including reactivity, versatility, and biodegradability. Increasing demand for polyethylene in packaging applications is a significant driver due to its excellent barrier properties against moisture and gasses while offering flexibility in design options. Furthermore, the rising adoption of lubricants based on low-viscosity synthetic oils in automotive applications is driving demand for higher molecular weight linear alpha-olefin. Volatility in crude oil prices has a direct impact on raw material costs for LAO production, making it harder for producers to maintain stable pricing structures. Fluctuating petrochemical feedstock prices may further limit market growth by intensifying price competition among suppliers and reducing profit margins. Ongoing research into bio-based methods of producing alpha olefins from renewable feedstocks such as vegetable oils and lignocellulosic biomass provides an opportunity for market growth.

Regional Insights

In the Americas region, the United States is a key producer of alpha olefins due to its abundant supply of shale gas. The expansion of shale gas extraction has led to greater availability of raw materials for alpha olefins production. Consumer demand in American countries is driven by applications such as polyethylene production for packaging materials and automotive industry requirements. In the EU countries, strict regulations on environmental concerns are driving innovations in sustainable solutions for polymer production using alpha olefins. The demand for linear alpha-olefins (LAOs) is rising due to their use in high-performance polyethylene products, predominantly in the automotive and packaging industries. Research initiatives have supported advancements in this field through funding and fostering collaborations between academia and industry. The Middle East contributes significantly to global alpha olefin production owing to its vast hydrocarbon reserves. The region boasts many large-scale petrochemical complexes that produce LAOs as part of their integrated operations. In the APAC region, China, Japan, and India are the major producers of alpha olefins, driven by its rapidly growing economy and the massive expansion of chemical industries in recent years. The demand for alpha Olefins is increasing consistently due to its expanding automobile, construction, and packaging sectors.

FPNV Positioning Matrix

The FPNV Positioning Matrix is pivotal in evaluating the Alpha Olefins Market. It offers a comprehensive assessment of vendors, examining key metrics related to Business Strategy and Product Satisfaction. This in-depth analysis empowers users to make well-informed decisions aligned with their requirements. Based on the evaluation, the vendors are then categorized into four distinct quadrants representing varying levels of success: Forefront (F), Pathfinder (P), Niche (N), or Vital (V).

Market Share Analysis

The Market Share Analysis is a comprehensive tool that provides an insightful and in-depth examination of the current state of vendors in the Alpha Olefins Market. By meticulously comparing and analyzing vendor contributions in terms of overall revenue, customer base, and other key metrics, we can offer companies a greater understanding of their performance and the challenges they face when competing for market share. Additionally, this analysis provides valuable insights into the competitive nature of the sector, including factors such as accumulation, fragmentation dominance, and amalgamation traits observed over the base year period studied. With this expanded level of detail, vendors can make more informed decisions and devise effective strategies to gain a competitive edge in the market.

Key Company Profiles

The report delves into recent significant developments in the Alpha Olefins Market, highlighting leading vendors and their innovative profiles. These include Borealis AG, Chevron Phillips Chemical Company LLC, Dowpol Chemical International Corp., Evonik Industries AG, Exxon Mobil Corporation, Idemitsu Kosan Co.,Ltd., INEOS AG, JAM Petrochemical Co., Lanxess AG, LyondellBasell Industries N.V., Mitsubishi Chemical Corporation, Mitsui Chemicals, Inc., P. S. CHEMICALS, PJSC Nizhnekamskneftekhim, Qatar Chemical Company Ltd., SABIC, Sasol Limited, Shell International B.V., Tokyo Chemical Industry Co., and TPC Group.

Market Segmentation & Coverage

This research report categorizes the Alpha Olefins Market to forecast the revenues and analyze trends in each of the following sub-markets:

- Type

- 1-Butene

- 1-Hexene

- 1-Octene

- Application

- Lubricants

- Oil Field Chemicals

- Polyolefins Comonomer

- Surfactants & Intermediates

- Tanning Oils

- Region

- Americas

- Argentina

- Brazil

- Canada

- Mexico

- United States

- California

- Florida

- Illinois

- New York

- Ohio

- Pennsylvania

- Texas

- Asia-Pacific

- Australia

- China

- India

- Indonesia

- Japan

- Malaysia

- Philippines

- Singapore

- South Korea

- Taiwan

- Thailand

- Vietnam

- Europe, Middle East & Africa

- Denmark

- Egypt

- Finland

- France

- Germany

- Israel

- Italy

- Netherlands

- Nigeria

- Norway

- Poland

- Qatar

- Russia

- Saudi Arabia

- South Africa

- Spain

- Sweden

- Switzerland

- Turkey

- United Arab Emirates

- United Kingdom

- Americas

The report offers valuable insights on the following aspects:

1. Market Penetration: It presents comprehensive information on the market provided by key players.

2. Market Development: It delves deep into lucrative emerging markets and analyzes the penetration across mature market segments.

3. Market Diversification: It provides detailed information on new product launches, untapped geographic regions, recent developments, and investments.

4. Competitive Assessment & Intelligence: It conducts an exhaustive assessment of market shares, strategies, products, certifications, regulatory approvals, patent landscape, and manufacturing capabilities of the leading players.

5. Product Development & Innovation: It offers intelligent insights on future technologies, R&D activities, and breakthrough product developments.

The report addresses key questions such as:

1. What is the market size and forecast of the Alpha Olefins Market?

2. Which products, segments, applications, and areas should one consider investing in over the forecast period in the Alpha Olefins Market?

3. What are the technology trends and regulatory frameworks in the Alpha Olefins Market?

4. What is the market share of the leading vendors in the Alpha Olefins Market?

5. Which modes and strategic moves are suitable for entering the Alpha Olefins Market?

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Limitations

- 1.7. Assumptions

- 1.8. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Alpha Olefins Market, by Region

5. Market Insights

- 5.1. Market Dynamics

- 5.1.1. Drivers

- 5.1.1.1. Rising application of alpha olefins in the paper & pulp industries

- 5.1.1.2. Increasing production of shale gas across the world

- 5.1.1.3. Growing demand for synthetic lubricants across various industries

- 5.1.2. Restraints

- 5.1.2.1. Fluctuation prices of crude oil

- 5.1.3. Opportunities

- 5.1.3.1. Ongoing advancements in the production of alpha olefins

- 5.1.3.2. Development of bio-based alpha olefins

- 5.1.4. Challenges

- 5.1.4.1. Stringent environmental regulations with the use of alpha olefins

- 5.1.1. Drivers

- 5.2. Market Segmentation Analysis

- 5.2.1. Type: Increasing utilization of 1-butene in the production of polymers due to their flexibility and resistivity

- 5.2.2. Application: Expanding applications of alpha olefin for the lubricants manufacturing

- 5.3. Market Trend Analysis

- 5.4. Cumulative Impact of High Inflation

- 5.5. Porter's Five Forces Analysis

- 5.5.1. Threat of New Entrants

- 5.5.2. Threat of Substitutes

- 5.5.3. Bargaining Power of Customers

- 5.5.4. Bargaining Power of Suppliers

- 5.5.5. Industry Rivalry

- 5.6. Value Chain & Critical Path Analysis

- 5.7. Regulatory Framework

6. Alpha Olefins Market, by Type

- 6.1. Introduction

- 6.2. 1-Butene

- 6.3. 1-Hexene

- 6.4. 1-Octene

7. Alpha Olefins Market, by Application

- 7.1. Introduction

- 7.2. Lubricants

- 7.3. Oil Field Chemicals

- 7.4. Polyolefins Comonomer

- 7.5. Surfactants & Intermediates

- 7.6. Tanning Oils

8. Americas Alpha Olefins Market

- 8.1. Introduction

- 8.2. Argentina

- 8.3. Brazil

- 8.4. Canada

- 8.5. Mexico

- 8.6. United States

9. Asia-Pacific Alpha Olefins Market

- 9.1. Introduction

- 9.2. Australia

- 9.3. China

- 9.4. India

- 9.5. Indonesia

- 9.6. Japan

- 9.7. Malaysia

- 9.8. Philippines

- 9.9. Singapore

- 9.10. South Korea

- 9.11. Taiwan

- 9.12. Thailand

- 9.13. Vietnam

10. Europe, Middle East & Africa Alpha Olefins Market

- 10.1. Introduction

- 10.2. Denmark

- 10.3. Egypt

- 10.4. Finland

- 10.5. France

- 10.6. Germany

- 10.7. Israel

- 10.8. Italy

- 10.9. Netherlands

- 10.10. Nigeria

- 10.11. Norway

- 10.12. Poland

- 10.13. Qatar

- 10.14. Russia

- 10.15. Saudi Arabia

- 10.16. South Africa

- 10.17. Spain

- 10.18. Sweden

- 10.19. Switzerland

- 10.20. Turkey

- 10.21. United Arab Emirates

- 10.22. United Kingdom

11. Competitive Landscape

- 11.1. FPNV Positioning Matrix

- 11.2. Market Share Analysis, By Key Player

- 11.3. Competitive Scenario Analysis, By Key Player

- 11.3.1. Investment & Funding

- 11.3.1.1. ExxonMobil invests USD 2 billion to produce linear alpha olefins

- 11.3.2. Award, Recognition, & Expansion

- 11.3.2.1. Chevron Phillips Chemical completes construction of 1-Hexene unit in Old Ocean

- 11.3.2.2. Shell eyeing expansion of its alpha olefins capabilities in Geismar

- 11.3.1. Investment & Funding

12. Competitive Portfolio

- 12.1. Key Company Profiles

- 12.1.1. Borealis AG

- 12.1.2. Chevron Phillips Chemical Company LLC

- 12.1.3. Dowpol Chemical International Corp.

- 12.1.4. Evonik Industries AG

- 12.1.5. Exxon Mobil Corporation

- 12.1.6. Idemitsu Kosan Co.,Ltd.

- 12.1.7. INEOS AG

- 12.1.8. JAM Petrochemical Co.

- 12.1.9. Lanxess AG

- 12.1.10. LyondellBasell Industries N.V.

- 12.1.11. Mitsubishi Chemical Corporation

- 12.1.12. Mitsui Chemicals, Inc.

- 12.1.13. P. S. CHEMICALS

- 12.1.14. PJSC Nizhnekamskneftekhim

- 12.1.15. Qatar Chemical Company Ltd.

- 12.1.16. SABIC

- 12.1.17. Sasol Limited

- 12.1.18. Shell International B.V.

- 12.1.19. Tokyo Chemical Industry Co.

- 12.1.20. TPC Group

- 12.2. Key Product Portfolio

13. Appendix

- 13.1. Discussion Guide

- 13.2. License & Pricing

LIST OF FIGURES

- FIGURE 1. ALPHA OLEFINS MARKET RESEARCH PROCESS

- FIGURE 2. ALPHA OLEFINS MARKET SIZE, 2023 VS 2030

- FIGURE 3. ALPHA OLEFINS MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 4. ALPHA OLEFINS MARKET SIZE, BY REGION, 2023 VS 2030 (%)

- FIGURE 5. ALPHA OLEFINS MARKET SIZE, BY REGION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 6. ALPHA OLEFINS MARKET DYNAMICS

- FIGURE 7. ALPHA OLEFINS MARKET SIZE, BY TYPE, 2023 VS 2030 (%)

- FIGURE 8. ALPHA OLEFINS MARKET SIZE, BY TYPE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 9. ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2023 VS 2030 (%)

- FIGURE 10. ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 11. AMERICAS ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 12. AMERICAS ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 13. UNITED STATES ALPHA OLEFINS MARKET SIZE, BY STATE, 2023 VS 2030 (%)

- FIGURE 14. UNITED STATES ALPHA OLEFINS MARKET SIZE, BY STATE, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 15. ASIA-PACIFIC ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 16. ASIA-PACIFIC ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 17. EUROPE, MIDDLE EAST & AFRICA ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2030 (%)

- FIGURE 18. EUROPE, MIDDLE EAST & AFRICA ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2023 VS 2024 VS 2030 (USD MILLION)

- FIGURE 19. ALPHA OLEFINS MARKET, FPNV POSITIONING MATRIX, 2023

- FIGURE 20. ALPHA OLEFINS MARKET SHARE, BY KEY PLAYER, 2023

LIST OF TABLES

- TABLE 1. ALPHA OLEFINS MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2023

- TABLE 3. ALPHA OLEFINS MARKET SIZE, 2018-2030 (USD MILLION)

- TABLE 4. GLOBAL ALPHA OLEFINS MARKET SIZE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 5. ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 6. ALPHA OLEFINS MARKET SIZE, BY 1-BUTENE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 7. ALPHA OLEFINS MARKET SIZE, BY 1-HEXENE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 8. ALPHA OLEFINS MARKET SIZE, BY 1-OCTENE, BY REGION, 2018-2030 (USD MILLION)

- TABLE 9. ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 10. ALPHA OLEFINS MARKET SIZE, BY LUBRICANTS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 11. ALPHA OLEFINS MARKET SIZE, BY OIL FIELD CHEMICALS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 12. ALPHA OLEFINS MARKET SIZE, BY POLYOLEFINS COMONOMER, BY REGION, 2018-2030 (USD MILLION)

- TABLE 13. ALPHA OLEFINS MARKET SIZE, BY SURFACTANTS & INTERMEDIATES, BY REGION, 2018-2030 (USD MILLION)

- TABLE 14. ALPHA OLEFINS MARKET SIZE, BY TANNING OILS, BY REGION, 2018-2030 (USD MILLION)

- TABLE 15. AMERICAS ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 16. AMERICAS ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 17. AMERICAS ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 18. ARGENTINA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 19. ARGENTINA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 20. BRAZIL ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 21. BRAZIL ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 22. CANADA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 23. CANADA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 24. MEXICO ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 25. MEXICO ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 26. UNITED STATES ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 27. UNITED STATES ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 28. UNITED STATES ALPHA OLEFINS MARKET SIZE, BY STATE, 2018-2030 (USD MILLION)

- TABLE 29. ASIA-PACIFIC ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 30. ASIA-PACIFIC ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 31. ASIA-PACIFIC ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 32. AUSTRALIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 33. AUSTRALIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 34. CHINA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 35. CHINA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 36. INDIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 37. INDIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 38. INDONESIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 39. INDONESIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 40. JAPAN ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 41. JAPAN ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 42. MALAYSIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 43. MALAYSIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 44. PHILIPPINES ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 45. PHILIPPINES ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 46. SINGAPORE ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 47. SINGAPORE ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 48. SOUTH KOREA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 49. SOUTH KOREA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 50. TAIWAN ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 51. TAIWAN ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 52. THAILAND ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 53. THAILAND ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 54. VIETNAM ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 55. VIETNAM ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 56. EUROPE, MIDDLE EAST & AFRICA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 57. EUROPE, MIDDLE EAST & AFRICA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 58. EUROPE, MIDDLE EAST & AFRICA ALPHA OLEFINS MARKET SIZE, BY COUNTRY, 2018-2030 (USD MILLION)

- TABLE 59. DENMARK ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 60. DENMARK ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 61. EGYPT ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 62. EGYPT ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 63. FINLAND ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 64. FINLAND ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 65. FRANCE ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 66. FRANCE ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 67. GERMANY ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 68. GERMANY ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 69. ISRAEL ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 70. ISRAEL ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 71. ITALY ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 72. ITALY ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 73. NETHERLANDS ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 74. NETHERLANDS ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 75. NIGERIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 76. NIGERIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 77. NORWAY ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 78. NORWAY ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 79. POLAND ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 80. POLAND ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 81. QATAR ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 82. QATAR ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 83. RUSSIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 84. RUSSIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 85. SAUDI ARABIA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 86. SAUDI ARABIA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 87. SOUTH AFRICA ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 88. SOUTH AFRICA ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 89. SPAIN ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 90. SPAIN ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 91. SWEDEN ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 92. SWEDEN ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 93. SWITZERLAND ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 94. SWITZERLAND ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 95. TURKEY ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 96. TURKEY ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 97. UNITED ARAB EMIRATES ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 98. UNITED ARAB EMIRATES ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 99. UNITED KINGDOM ALPHA OLEFINS MARKET SIZE, BY TYPE, 2018-2030 (USD MILLION)

- TABLE 100. UNITED KINGDOM ALPHA OLEFINS MARKET SIZE, BY APPLICATION, 2018-2030 (USD MILLION)

- TABLE 101. ALPHA OLEFINS MARKET, FPNV POSITIONING MATRIX, 2023

- TABLE 102. ALPHA OLEFINS MARKET SHARE, BY KEY PLAYER, 2023

- TABLE 103. ALPHA OLEFINS MARKET LICENSE & PRICING

聚α烯烃全球市场规模、份额和趋势分析报告,按类型、应用和地区分類的展望和预测,2023-2030 年

聚α烯烃全球市场规模、份额和趋势分析报告,按类型、应用和地区分類的展望和预测,2023-2030 年 非晶态α-烯烃共聚物市场 - 全球市场规模、占有率、趋势分析、机会、预测报告,2019-2029

非晶态α-烯烃共聚物市场 - 全球市场规模、占有率、趋势分析、机会、预测报告,2019-2029 1-己烯全球市场分析:工厂产能、生产、运营效率、需求和供应、最终用户行业、销售渠道、区域需求、外贸、公司份额(2015-2035 年)

1-己烯全球市场分析:工厂产能、生产、运营效率、需求和供应、最终用户行业、销售渠道、区域需求、外贸、公司份额(2015-2035 年) APAO(非晶质聚烯烃)的全球市场分析:各厂房生产能力,生产量,运用效率,需求与供给,终端用户产业,销售管道,地区需求,企业占有率(2015年~2035年)

APAO(非晶质聚烯烃)的全球市场分析:各厂房生产能力,生产量,运用效率,需求与供给,终端用户产业,销售管道,地区需求,企业占有率(2015年~2035年) 全球线性 α 烯烃 (LAO) 市场:工厂产能、产量、利用率、需求和供应、最终用户行业、类型、销售渠道、区域需求、公司份额 (2015-2035)

全球线性 α 烯烃 (LAO) 市场:工厂产能、产量、利用率、需求和供应、最终用户行业、类型、销售渠道、区域需求、公司份额 (2015-2035) α-烯烃市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、按应用、地区和竞争细分

α-烯烃市场 - 2018-2028 年全球产业规模、份额、趋势、机会和预测,按类型、按应用、地区和竞争细分 聚α烯烃的全球市场

聚α烯烃的全球市场 2030 年α-烯烃市场预测:按类型、用途和地区分類的全球分析

2030 年α-烯烃市场预测:按类型、用途和地区分類的全球分析 Alpha烯烃的全球市场:各类型,各用途,各地区 - 预测(~2028年)

Alpha烯烃的全球市场:各类型,各用途,各地区 - 预测(~2028年) 聚α烯烃市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测

聚α烯烃市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测