|

市场调查报告书

商品编码

1829984

全球疫苗市场按适应症、技术、类型、给药途径、最终用户和地区划分—预测至 2030 年Vaccines Market by Technology (Conjugate, Recombinant, Inactivated, Live Attenuated, Viral Vector, mRNA), Type (Monovalent, Multivalent), Disease (Pneumococcal, Flu, Hepatitis, MMR, RSV), Route of Administration (IM, SC, Oral)-Global Forecast to 2030 |

||||||

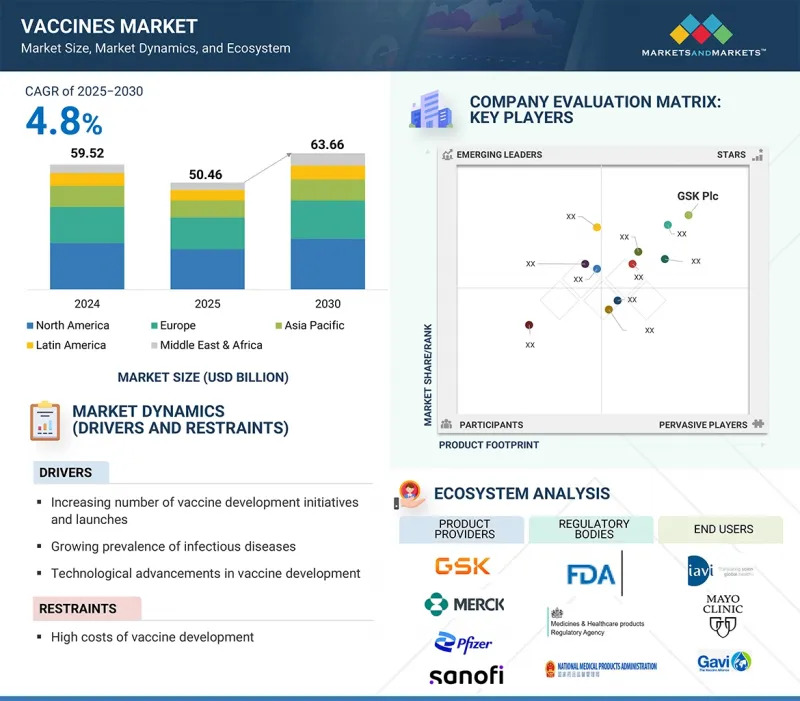

疫苗市场预计将从 2025 年的 504.6 亿美元成长到 2030 年的 636.6 亿美元,预测期内的复合年增长率为 4.8%。

| 调查范围 | |

|---|---|

| 调查年份 | 2024-2030 |

| 基准年 | 2024 |

| 预测期 | 2025-2030 |

| 对价单位 | 金额(十亿美元) |

| 部分 | 按适应症、技术、类型、给药途径、最终用户和地区 |

| 目标区域 | 北美、欧洲、亚太地区、拉丁美洲、中东和非洲 |

传染病发病率高、疫苗技术创新、政府对疫苗开发的支持和大量资金、疫苗接种倡议的增加以及对创新产品的投资和推出的高度重视等因素正在推动疫苗的增长。

2024 年,根据适应症,肺炎链球菌疫苗将占据疫苗市场的最大份额。

依适应症,疫苗市场分为联合疫苗、HPV、脑膜炎球菌疾病、带状疱疹、轮状病毒、MMR、肺炎球菌疾病、流感、水痘、肝炎、DTP、脊髓灰质炎和其他适应症。 2022 年,肺炎链球菌疫苗占据了疫苗市场的最大份额。这背后的几个关键因素包括全球肺炎链球菌感染发病率上升、政府对疫苗接种计划的资助增加以及公众对肺炎、脑膜炎和血液感染等肺炎球菌併发症相关的严重健康风险的认识不断提高。此外,下一代肺炎球菌疫苗的持续开发和创新,例如最近核准的20 价和 21 价结合疫苗,正在扩大疫苗接种选择,并进一步促进市场成长和公共卫生成果。

2024年,多效价疫苗领域将占据疫苗类型中最大的份额。

疫苗市场按类型细分为单价疫苗和多效价疫苗。 2024年,多效价疫苗占据了疫苗市场的最大份额。此优点归因于多效价疫苗单剂即可预防多种疾病。这减少了所需的注射次数,简化了疫苗接种流程,提高了患者的依从性,并减少了后勤方面的挑战。此外,需要广泛免疫的疾病(例如呼吸道感染疾病和某些癌症)的日益普及也推动了对此类疫苗的需求。技术进步和对多效价疫苗高效生产的投资不断增加进一步推动了这一趋势,因为多价疫苗能够实现大规模快速生产。政府和医疗机构,尤其是在医疗保健资源有限的地区,更青睐多效价疫苗,因为简化的疫苗接种程序可以提高覆盖率并改善公共卫生结果。

到2024年,亚太地区将成为疫苗市场成长最快的地区。

疫苗市场分为北美、欧洲、亚太、拉丁美洲以及中东和非洲。预计亚太地区在预测期内将实现显着的复合年增长率。这一增长得益于公众健康意识的提高、国家疫苗接种计划的扩大以及政府对医疗基础设施投资的增加。这些努力得到了官民合作关係关係、旨在提高疫苗公平性的国际合作以及实现先进疫苗开发和更低成本生产的技术进步的支持。此外,该地区,尤其是中国和印度等国家,人口不断增长,使其成为现有疫苗和新兴疫苗的巨大目标市场。这些因素凸显了亚太地区在疫苗产业市场的领导地位。

本报告研究了全球疫苗市场,按适应症、技术、类型、给药途径、最终用户和区域趋势进行细分,并提供了参与市场的公司概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章 市场概况

- 介绍

- 市场动态

第六章 产业趋势

- 影响客户业务的趋势/中断

- 定价分析

- 技术分析

- 价值链分析

- 管道分析

- 生态系分析

- 监管分析

- 贸易分析

- 波特五力分析

- 专利分析

- 2025-2026年主要会议和活动

- 主要相关人员和采购标准

- 投资金筹措场景

- 人工智慧/生成式人工智慧对疫苗市场的影响

- 2025年美国关税将如何影响疫苗市场

- 疫苗采购数据

- 疫苗製造过程

第七章疫苗市场(按适应症)

- 介绍

- 肺炎链球菌感染

- 流感

- 联合疫苗

- HPV

- 病菌感染

- 带状疱疹

- 轮状病毒

- MMR

- 水痘

- 肝炎

- DTP

- 脊髓灰质炎

- RSV

- COVID-19

- 其他的

第八章疫苗市场(按技术)

- 介绍

- 疫苗市场(不包括 COVID-19 疫苗),依技术分类

- COVID-19疫苗市场(按技术)

第九章 疫苗市场(不包括新冠疫苗),依类型

- 介绍

- 多效价疫苗

- 单价疫苗

第十章 疫苗市场(不包括新冠疫苗)依接种途径

- 介绍

- 肌肉注射和皮下注射

- 口服

- 其他的

第 11 章疫苗市场(不包括 COVID-19 疫苗),以最终用户划分

- 介绍

- 成人疫苗

- 儿童疫苗

第十二章 疫苗市场(不包括新冠疫苗),依地区

- 介绍

- 北美洲

- 北美宏观经济展望

- 美国

- 加拿大

- 欧洲

- 欧洲宏观经济展望

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他的

- 亚太地区

- 亚太宏观经济展望

- 中国

- 日本

- 印度

- 韩国

- 其他的

- 拉丁美洲

- 拉丁美洲宏观经济展望

- 巴西

- 墨西哥

- 其他的

- 中东

- 感染疾病爆发推动市场

- 中东宏观经济展望

- 非洲

- 已开发国家提供资金和补贴来刺激市场

- 非洲宏观经济展望

第十三章竞争格局

- 介绍

- 主要参与企业的策略/优势

- 2020-2024年收益分析

- 2024年市占率分析

- 公司估值矩阵:2024 年关键参与企业

- 公司估值矩阵:Start-Ups/中小企业,2024 年

- 估值和财务指标

- 品牌/产品比较

- 竞争场景

第十四章:公司简介

- 主要参与企业

- GSK PLC

- MERCK & CO., INC.

- PFIZER INC.

- SANOFI

- CSL

- EMERGENT

- JOHNSON & JOHNSON SERVICES, INC.

- ASTRAZENECA

- SERUM INSTITUTE OF INDIA PVT., LTD.

- BAVARIAN NORDIC

- MITSUBISHI TANABE PHARMA CORPORATION

- DAIICHI SANKYO COMPANY, LIMITED

- PANACEA BIOTEC

- BIOLOGICAL E LIMITED

- BHARAT BIOTECH

- NOVAVAX

- INOVIO PHARMACEUTICALS

- 其他公司

- SINOVAC

- INCEPTA PHARMACEUTICALS LTD.

- VALNEVA SE

- VBI VACCINE INC.

- BIO FARMA

- MICROGEN

- ZHI FEI BIOLOGICAL

- INDIAN IMMUNOLOGICALS LIMITED

第十五章 附录

The vaccines market is expected to reach 63.66 billion USD in 2030, up from 50.46 billion USD in 2025, growing at a CAGR of 4.8% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Type, Disease Indication, Route of Administration, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. |

Factors such as the high incidence of contagious diseases, innovation in vaccine technology, government support and substantial funding for vaccine development, increasing vaccination initiatives, and a strong focus on investing in and launching innovative products are driving this growth vaccines.

In 2024, by disease indication, the pneumococcal segment accounted for the largest share of the vaccines market.

Based on disease indication, the vaccines market is segmented into combination vaccines, HPV, meningococcal disease, herpes zoster, rotavirus, MMR, pneumococcal disease, influenza, varicella, hepatitis, DTP, polio, and other disease indications. In 2022, the pneumococcal segment held the largest share of the vaccines market. This is due to several key factors: a rising incidence of pneumococcal infections worldwide; increased government funding for vaccination programs; and heightened public awareness of the serious health risks associated with pneumococcal-related complications such as pneumonia, meningitis, and bloodstream infections. Additionally, ongoing innovation and the development of next-generation pneumococcal vaccines, such as the recently approved 20-valent and 21-valent conjugate vaccines, are expanding immunization options, further boosting market growth and public health benefits outcomes.

In 2024, by type, the multivalent vaccines segment accounted for the largest share of the vaccines market.

The vaccines market is divided into monovalent vaccines and multivalent vaccines, based on type. In 2024, the multivalent vaccines segment held the largest portion of the Vaccines market. This dominance comes from the ability of multivalent vaccines to provide protection against multiple diseases with a single dose-simplifying immunization by reducing the number of injections needed, which increases patient compliance and decreases logistical challenges. Additionally, the growing prevalence of diseases that require broad-spectrum immunity, such as respiratory infections and certain cancers, has increased demand for these vaccines. Further supporting this trend are technological advances and increased investment in efficient manufacturing of multivalent vaccines, enabling larger and faster production. Governments and healthcare providers in regions with limited healthcare access particularly favor them because simplified vaccination schedules improve coverage and boost public health outcomes.

In 2024, the Asia Pacific was the fastest growing region in the Vaccines market.

The vaccines market region is divided into North America, Europe, the Asia Pacific, Latin America, the Middle East & Africa. The Asia Pacific region is expected to grow at a significant CAGR during the forecast period. This increase is driven by greater public health awareness, expanding national immunization programs, and increased government investment in healthcare infrastructure. Supporting these efforts are public-private partnerships, international collaborations aimed at improving vaccine equity, and technological advancements that enable advanced vaccine development and more affordable production. Additionally, the region's large and growing populations, especially in countries such as China and India, present a substantial target market for both established and new vaccines. These factors highlight the Asia Pacific's leadership in the vaccine industry market.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Tier 1-25%, Tier 2-35%, and Tier 3- 40%

- By Designation: C-level Executives - 55%, Directors- 20%, and Others- 25%

- By Region: North America -35%, Europe - 25%, Asia Pacific -20%, Latin America -10%, the Middle East & Africa- 10%

GSK plc (UK), Merck & Co., Inc. (US), Pfizer, Inc. (US), Sanofi (France), CSL (Australia), Emergent (US), Johnson & Johnson Services Inc. (US), AstraZeneca (UK), Serum Institute of India Pvt. Ltd. (India), Bavarian Nordic (Denmark), Mitsubishi Tanabe Pharma Corporation (Japan), Daiichi Sankyo Company, Limited (Japan), Panacea Biotec (India), Biological E. Limited (India), Bharat Biotech (India), Novavax (US), Inovio Pharmaceuticals (US), Sinovac (China), Incepta Pharmaceuticals (Bangladesh), Valneva SE (France), VBI Vaccines Inc. (US), Bio Farma (Indonesia), FSUE NPO Microgen (Russia), Zhi fei Biological (China), Indian Immunologicals Ltd (India) are some of the key companies offering Vaccines.

Research Coverage

This research report categorizes the Vaccines market by technology (conjugate vaccine, recombinant vaccine, inactivated & subunit vaccine, live attenuated vaccine, toxoid vaccine, viral vector vaccine, mRNA vaccine, and other vaccines), type (monovalent vaccines, multivalent vaccines), indication (pneumococcal disease, influenza, combination vaccine, HPV, meningococcal disease, herpes zoster, rotavirus, MMR, varicella, hepatitis, DTP, polio, RSA, other disease indications), route of administration (intramuscular & subcutaneous, oral, other routes), end user (pediatric vaccines, adult vaccines), and by region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). The scope of the report provides detailed information on major factors such as drivers, challenges, opportunities, and restraints that influence the growth of the vaccines market. A comprehensive analysis of key industry players has been conducted to offer insights into their business overview, product portfolios, and key strategies, including collaborations, partnerships, expansions, agreements, acquisitions, and recent developments related to the vaccines market. Competitive analysis of top players and upcoming startups within the vaccines market ecosystem is included in this report. The report also details primary factors like drivers, restraints, challenges, and opportunities shaping the market growth, along with an in-depth review of key industry players' solutions, products, recent product launches, mergers, acquisitions, and emerging market trends ecosystem.

Key Benefits of Buying the Report

This report offers a comprehensive overview of the Vaccines market. It aims to assess the size and future growth opportunities of the market across various segments, such as technology, type, indication, route of administration, end user, and region. The report also features an in-depth competitive analysis of the major market players, including their company profiles, recent developments, and key market strategies.

The report provides insights into the following pointers:

Analysis of key drivers (strong emphasis on investment and launch of novel vaccines, rising prevalence of infectious disease, expanding immunization programs, advancements in vaccine technology and robust government support & funding for the development of vaccines), restraints (High development cost, patent expiry ), opportunities (Increased focus on therapeutic vaccines, robust & strong pipeline) and challenges (Stringent regulatory processes, vaccine supply shortage, frequent product recall)

- Product Development/Innovation: Detailed insights on newly launched Products, and technological assessment of the Vaccines market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the Vaccines market across varied regions.

- Market Diversification: Exhaustive information about new, untapped geographies, recent developments, and investments in the Vaccines market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as GSK plc (UK), Merck & Co., Inc. (US), Pfizer, Inc. (US), Sanofi (France), CSL (Australia), Emergent (US), Johnson & Johnson Services Inc. (US), AstraZeneca (UK), Serum Institute of India Pvt. Ltd. (India), Bavarian Nordic (Denmark), Mitsubishi Tanabe Pharma Corporation (Japan), Daiichi Sankyo Company, Limited (Japan), Panacea Biotec (India), Biological E. Limited (India), Bharat Biotech (India), Novavax (US), Inovio Pharmaceuticals (US), Sinovac (China), Incepta Pharmaceuticals (Bangladesh), Valneva SE (France), VBI Vaccines Inc. (US), Bio Farma (Indonesia), FSUE NPO Microgen (Russia), Zhi fei Biological (China), Indian Immunologicals Ltd (India), among others, in the vaccines market. The report also helps stakeholders understand the trends of the vaccines market and provides information on key market drivers, restraints, challenges, and opportunities. A detailed analysis of the key industry players has been conducted to offer insights into their key strategies, product launches and approvals, pipeline developments, acquisitions, partnerships, collaborations, recent activities, investments, and funding activities, brand and product comparisons, vendor evaluations, and financial metrics of the vaccines sector market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key sources of secondary data

- 2.1.1.2 Key objectives of secondary research

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primaries

- 2.1.2.2 Key objectives of primary research

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 GLOBAL MARKET SIZE ESTIMATION, 2024

- 2.2.1.1 Company revenue analysis (bottom-up approach)

- 2.2.1.2 MarketsandMarkets repository analysis

- 2.2.1.3 Secondary analysis

- 2.2.1.4 Bottom-up approach (disease indication-based analysis)

- 2.2.1.5 Primary research

- 2.2.1.5.1 Insights from primary sources

- 2.2.2 SEGMENTAL MARKET SIZE ESTIMATION (TOP-DOWN APPROACH)

- 2.2.1 GLOBAL MARKET SIZE ESTIMATION, 2024

- 2.3 MARKET GROWTH RATE PROJECTIONS

- 2.4 DATA TRIANGULATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ANALYSIS

3 EXECUTIVE SUMMARY

- 3.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 3.2 STRATEGIC IMPERATIVES FOR STAKEHOLDERS IN VACCINES MARKET

- 3.3 DISRUPTIVE TRENDS SHAPING VACCINES MARKET

- 3.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

4 PREMIUM INSIGHTS

- 4.1 GLOBAL VACCINES MARKET SNAPSHOT

- 4.2 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE AND COUNTRY, 2024

- 4.3 VACCINES MARKET (EXCLUDING COVID-19 VACCINES): GEOGRAPHIC GROWTH OPPORTUNITIES

- 4.4 UNMET NEEDS & WHITE SPACES

- 4.5 STRATEGIC ANALYSIS OF GROWTH OPPORTUNITIES

- 4.6 EMERGING BUSINESS MODELS & ECOSYSTEM SHIFTS

- 4.7 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.8 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Focus on vaccine development and launches

- 5.2.1.2 Rising prevalence of infectious diseases

- 5.2.1.3 Increasing immunization programs

- 5.2.1.4 Advancements in vaccine technology

- 5.2.1.5 Government support and funding for vaccine development

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of vaccine development

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising focus on therapeutic vaccines

- 5.2.3.2 Extensive R&D for vaccines and increased investments in clinical trials

- 5.2.4 CHALLENGES

- 5.2.4.1 Stringent regulatory processes

- 5.2.4.2 Product recalls

- 5.2.1 DRIVERS

6 INDUSTRY TRENDS

- 6.1 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 6.2 PRICING ANALYSIS

- 6.2.1 AVERAGE SELLING PRICE TREND OF VACCINES, BY KEY PLAYER, 2023-2025

- 6.2.2 AVERAGE SELLING PRICE TREND OF VACCINES, BY DISEASE INDICATION, 2023-2025

- 6.2.3 AVERAGE SELLING PRICE TREND OF VACCINES, BY REGION, 2021-2023

- 6.3 TECHNOLOGY ANALYSIS

- 6.3.1 KEY TECHNOLOGIES

- 6.3.1.1 Recombinant technology

- 6.3.1.2 Conjugation technology

- 6.3.1.3 Viral vector technology

- 6.3.2 COMPLEMENTARY TECHNOLOGIES

- 6.3.2.1 Encapsulation & delivery technology

- 6.3.2.2 Automation & control

- 6.3.2.3 AI & machine learning for vaccine design

- 6.3.3 ADJACENT TECHNOLOGIES

- 6.3.3.1 Single-use technology

- 6.3.3.2 Cell line development

- 6.3.1 KEY TECHNOLOGIES

- 6.4 VALUE CHAIN ANALYSIS

- 6.5 PIPELINE ANALYSIS

- 6.5.1 VACCINES MARKET: CLINICAL TRIALS, BY PHASE

- 6.5.2 VACCINES MARKET: CLINICAL TRIALS, BY DISEASE INDICATION

- 6.5.3 VACCINES MARKET: PHASE 2/3 CLINICAL TRIALS, BY COMPANY

- 6.6 ECOSYSTEM ANALYSIS

- 6.6.1 VACCINES MARKET: ROLE IN ECOSYSTEM

- 6.7 REGULATORY ANALYSIS

- 6.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.7.2 REGULATORY FRAMEWORK

- 6.7.2.1 North America

- 6.7.2.2 Europe

- 6.7.2.3 Asia Pacific

- 6.7.2.4 Latin America

- 6.7.2.5 Middle East & Africa

- 6.7.3 REGULATORY CHALLENGES IN VACCINES MARKET

- 6.8 TRADE ANALYSIS

- 6.8.1 IMPORT DATA (HS CODE 300220)

- 6.8.2 EXPORT DATA (HS CODE 300220)

- 6.9 PORTER'S FIVE FORCES ANALYSIS

- 6.9.1 THREAT OF NEW ENTRANTS

- 6.9.2 THREAT OF SUBSTITUTES

- 6.9.3 BARGAINING POWER OF SUPPLIERS

- 6.9.4 BARGAINING POWER OF BUYERS

- 6.9.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.10 PATENT ANALYSIS

- 6.10.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR VACCINE PATENTS, 2014-2024

- 6.11 KEY CONFERENCES & EVENTS, 2025-2026

- 6.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 6.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.12.2 KEY BUYING CRITERIA

- 6.13 INVESTMENT & FUNDING SCENARIO

- 6.14 IMPACT OF AI/GENERATIVE AI ON VACCINES MARKET

- 6.14.1 INTRODUCTION

- 6.14.2 MARKET POTENTIAL OF AI IN VACCINES MARKET

- 6.14.3 AI USE CASES

- 6.14.4 KEY COMPANIES IMPLEMENTING AI

- 6.14.5 FUTURE OF GENERATIVE AI IN VACCINES ECOSYSTEM

- 6.15 IMPACT OF 2025 US TARIFFS ON VACCINES MARKET

- 6.15.1 INTRODUCTION

- 6.15.2 KEY TARIFF RATES

- 6.15.3 PRICE IMPACT ANALYSIS

- 6.15.4 IMPACT ON COUNTRY/REGION

- 6.15.4.1 US

- 6.15.4.2 Europe

- 6.15.4.3 Asia Pacific

- 6.15.5 IMPACT ON END-USE INDUSTRIES

- 6.15.5.1 Public health & government bodies

- 6.15.5.2 Healthcare providers & institutions

- 6.16 VACCINE PROCUREMENT DATA

- 6.16.1 NUMBER OF VACCINES DELIVERED BY UNICEF, 2023-2025

- 6.16.2 WHO: VACCINE PURCHASE DATABASE, 2021-2023

- 6.17 VACCINE MANUFACTURING PROCESS

- 6.17.1 OVERVIEW

- 6.17.1.1 R&D and process development

- 6.17.1.2 Upstream production (antigen generation)

- 6.17.1.3 Downstream processing

- 6.17.1.4 Formulation & fill-finish

- 6.17.1.5 Quality control & regulatory release

- 6.17.1.6 Packaging, cold chain, and distribution

- 6.17.2 MANUFACTURING MODELS & CAPACITY DYNAMICS

- 6.17.1 OVERVIEW

7 VACCINES MARKET, BY DISEASE INDICATION

- 7.1 INTRODUCTION

- 7.2 PNEUMOCOCCAL DISEASE

- 7.2.1 INCREASING INCIDENCE OF PNEUMONIA IN CHILDREN TO DRIVE MARKET

- 7.3 INFLUENZA

- 7.3.1 RISING NEED FOR IMMUNIZATION AGAINST VIRAL INFECTIONS TO DRIVE MARKET

- 7.4 COMBINATION VACCINES

- 7.4.1 GROWING DEMAND FOR ALL-IN-ONE VACCINES TO DRIVE MARKET GROWTH

- 7.5 HPV

- 7.5.1 RISING FOCUS ON CERVICAL CANCER PREVENTION TO DRIVE HPV VACCINE UPTAKE

- 7.6 MENINGOCOCCAL DISEASE

- 7.6.1 INCREASING INITIATIVES BY GOVERNMENT AND NON-GOVERNMENT ORGANIZATIONS TO SUPPORT MARKET GROWTH

- 7.7 HERPES ZOSTER

- 7.7.1 RISING AGING POPULATION TO DRIVE DEMAND FOR HERPES ZOSTER VACCINES

- 7.8 ROTAVIRUS

- 7.8.1 RISING INFANT IMMUNIZATION PROGRAMS TO DRIVE ROTAVIRUS VACCINE MARKET GROWTH

- 7.9 MMR

- 7.9.1 RISING INCIDENCE OF MEASLES, MUMPS, AND RUBELLA TO BOOST DEMAND

- 7.10 VARICELLA

- 7.10.1 INCREASING PROMOTION OF IMMUNIZATION PROGRAMS TO SUPPORT MARKET GROWTH

- 7.11 HEPATITIS

- 7.11.1 LOW SOCIO-ECONOMIC STANDARDS OF LIVING AND HIGH CONTAMINATION IN DRINKING WATER TO DRIVE MARKET

- 7.12 DTP

- 7.12.1 STRONG INTEGRATION INTO NATIONAL IMMUNIZATION PROGRAMS TO SUSTAIN DTP VACCINE DEMAND

- 7.13 POLIO

- 7.13.1 INCREASING GOVERNMENT INITIATIVES AND IMMUNIZATION PROGRAMS TO DRIVE MARKET

- 7.14 RSV

- 7.14.1 STRONG PRODUCT PIPELINE AND NEW PRODUCT LAUNCHES TO PROPEL MARKET GROWTH

- 7.15 COVID-19

- 7.15.1 DECLINING DEMAND DUE TO HIGH POPULATION COVERAGE AND REDUCED SEVERITY OF VARIANTS TO SLOW DOWN MARKET GROWTH

- 7.16 OTHER DISEASE INDICATIONS

8 VACCINES MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY

- 8.2.1 CONJUGATE VACCINES

- 8.2.1.1 Increasing public-private partnerships to drive market growth

- 8.2.2 RECOMBINANT VACCINES

- 8.2.2.1 Low post-vaccination reactions and reduced need for booster doses to drive market

- 8.2.3 INACTIVATED & SUBUNIT VACCINES

- 8.2.3.1 Ease of storage and transportation to support growth

- 8.2.4 LIVE ATTENUATED VACCINES

- 8.2.4.1 High cost of storage and limited financial resources of distributors to restrain market

- 8.2.5 TOXOID VACCINES

- 8.2.5.1 Rising prevalence of bacterial infections among infants and children to drive market

- 8.2.6 OTHER VACCINES

- 8.2.1 CONJUGATE VACCINES

- 8.3 COVID-19 VACCINES MARKET, BY TECHNOLOGY

- 8.3.1 MRNA VACCINES

- 8.3.1.1 Increasing focus on mRNA vaccine development to drive market

- 8.3.2 VIRAL VECTOR VACCINES

- 8.3.2.1 Rising investment in vaccine development to drive market

- 8.3.3 OTHER COVID-19 VACCINES

- 8.3.1 MRNA VACCINES

9 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE

- 9.1 INTRODUCTION

- 9.2 MULTIVALENT VACCINES

- 9.2.1 INCREASED NEED FOR IMMUNIZATION AND COST-EFFECTIVENESS TO DRIVE MARKET

- 9.3 MONOVALENT VACCINES

- 9.3.1 RISING R&D INVESTMENTS AND PREVALENCE OF INFECTIOUS DISEASES TO SUPPORT MARKET GROWTH

10 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION

- 10.1 INTRODUCTION

- 10.2 INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION

- 10.2.1 EASE OF ABSORPTION AND BETTER IMMUNE RESPONSE TO DRIVE ADOPTION

- 10.3 ORAL ADMINISTRATION

- 10.3.1 REDUCED RISK OF BLOOD-TRANSMITTED INFECTIONS TO DRIVE ADOPTION

- 10.4 OTHER ROUTES OF ADMINISTRATION

11 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER

- 11.1 INTRODUCTION

- 11.2 ADULT VACCINES

- 11.2.1 ADULT VACCINES TO COMMAND LARGER MARKET SHARE DURING FORECAST PERIOD

- 11.3 PEDIATRIC VACCINES

- 11.3.1 SUPPORT FROM GOVERNMENT AND NON-GOVERNMENT BODIES TO DRIVE MARKET

12 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 12.2.2 US

- 12.2.2.1 US to dominate North American market during forecast period

- 12.2.3 CANADA

- 12.2.3.1 High incidence of infectious diseases to drive market growth

- 12.3 EUROPE

- 12.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 12.3.2 GERMANY

- 12.3.2.1 Significant R&D investments and growing biotechnology industry to drive market

- 12.3.3 UK

- 12.3.3.1 Launch of new products and increased funding by government and non-government organizations to drive market

- 12.3.4 FRANCE

- 12.3.4.1 Favorable government initiatives for mass immunization to drive market

- 12.3.5 ITALY

- 12.3.5.1 Higher investments by companies for increased production capacities to drive market

- 12.3.6 SPAIN

- 12.3.6.1 Rising investments in vaccine development by private organizations to drive market

- 12.3.7 REST OF EUROPE

- 12.4 ASIA PACIFIC

- 12.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 12.4.2 CHINA

- 12.4.2.1 China to hold largest share of APAC vaccines market

- 12.4.3 JAPAN

- 12.4.3.1 Favorable government initiatives to support market growth

- 12.4.4 INDIA

- 12.4.4.1 Increasing government initiatives and development of new and improved vaccines to drive market

- 12.4.5 SOUTH KOREA

- 12.4.5.1 Strong government strategies for improved vaccine hubs to drive market

- 12.4.6 REST OF ASIA PACIFIC

- 12.5 LATIN AMERICA

- 12.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 12.5.2 BRAZIL

- 12.5.2.1 Rising focus on immunization programs to drive market

- 12.5.3 MEXICO

- 12.5.3.1 Trained workforce and ethnically varied population base for clinical trials to propel market growth

- 12.5.4 REST OF LATIN AMERICA

- 12.6 MIDDLE EAST

- 12.6.1 INCREASING PREVALENCE OF INFECTIOUS DISEASES TO DRIVE MARKET

- 12.6.2 MACROECONOMIC OUTLOOK FOR MIDDLE EAST

- 12.7 AFRICA

- 12.7.1 AVAILABILITY OF FUNDS AND GRANTS FROM DEVELOPED ECONOMIES TO DRIVE MARKET

- 12.7.2 MACROECONOMIC OUTLOOK FOR AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 13.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN VACCINES MARKET

- 13.3 REVENUE ANALYSIS, 2020-2024

- 13.4 MARKET SHARE ANALYSIS, 2024

- 13.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- 13.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 13.5.5.1 Company footprint

- 13.5.5.2 Region footprint

- 13.5.5.3 Technology footprint

- 13.5.5.4 Type footprint

- 13.5.5.5 Route of administration footprint

- 13.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.6.1 PROGRESSIVE COMPANIES

- 13.6.2 RESPONSIVE COMPANIES

- 13.6.3 DYNAMIC COMPANIES

- 13.6.4 STARTING BLOCKS

- 13.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES

- 13.6.5.1 Detailed list of key startups/SMEs

- 13.6.5.2 Competitive benchmarking of key startups/SMEs

- 13.7 COMPANY VALUATION & FINANCIAL METRICS

- 13.7.1 FINANCIAL METRICS

- 13.7.2 COMPANY VALUATION

- 13.8 BRAND/PRODUCT COMPARISON

- 13.8.1 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES & APPROVALS

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 GSK PLC

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches & approvals

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses & competitive threats

- 14.1.2 MERCK & CO., INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product approvals

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses & competitive threats

- 14.1.3 PFIZER INC.

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product approvals

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM view

- 14.1.3.4.1 Key strengths

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses & competitive threats

- 14.1.4 SANOFI

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product approvals

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.3.4 Other developments

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses & competitive threats

- 14.1.5 CSL

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product approvals

- 14.1.5.3.2 Deals

- 14.1.5.3.3 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses & competitive threats

- 14.1.6 EMERGENT

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product approvals

- 14.1.6.3.2 Other developments

- 14.1.7 JOHNSON & JOHNSON SERVICES, INC.

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Deals

- 14.1.8 ASTRAZENECA

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.3.2 Expansions

- 14.1.8.3.3 Other developments

- 14.1.9 SERUM INSTITUTE OF INDIA PVT., LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches & approvals

- 14.1.9.3.2 Deals

- 14.1.9.3.3 Expansions

- 14.1.10 BAVARIAN NORDIC

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product approvals

- 14.1.10.3.2 Deals

- 14.1.10.3.3 Other developments

- 14.1.11 MITSUBISHI TANABE PHARMA CORPORATION

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches & approvals

- 14.1.11.3.2 Deals

- 14.1.12 DAIICHI SANKYO COMPANY, LIMITED

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Deals

- 14.1.13 PANACEA BIOTEC

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Deals

- 14.1.14 BIOLOGICAL E LIMITED

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product approvals

- 14.1.14.3.2 Deals

- 14.1.14.3.3 Other developments

- 14.1.15 BHARAT BIOTECH

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Product launches & approvals

- 14.1.15.3.2 Deals

- 14.1.16 NOVAVAX

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Product approvals

- 14.1.17 INOVIO PHARMACEUTICALS

- 14.1.17.1 Business overview

- 14.1.17.2 Products offered

- 14.1.17.3 Recent developments

- 14.1.17.3.1 Other developments

- 14.1.1 GSK PLC

- 14.2 OTHER PLAYERS

- 14.2.1 SINOVAC

- 14.2.2 INCEPTA PHARMACEUTICALS LTD.

- 14.2.3 VALNEVA SE

- 14.2.4 VBI VACCINE INC.

- 14.2.5 BIO FARMA

- 14.2.6 MICROGEN

- 14.2.7 ZHI FEI BIOLOGICAL

- 14.2.8 INDIAN IMMUNOLOGICALS LIMITED

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS

List of Tables

- TABLE 1 VACCINES MARKET: INCLUSIONS & EXCLUSIONS

- TABLE 2 IMPACT ANALYSIS OF SUPPLY-SIDE AND DEMAND-SIDE FACTORS

- TABLE 3 VACCINES MARKET: RISK ASSESSMENT ANALYSIS

- TABLE 4 VACCINES MARKET: STRATEGIC ANALYSIS OF GROWTH OPPORTUNITIES

- TABLE 5 VACCINES MARKET: EMERGING BUSINESS MODELS & TARGET SEGMENTS

- TABLE 6 VACCINES MARKET: IMPACT ANALYSIS

- TABLE 7 NIH FUNDING FOR VACCINE RESEARCH, 2020-2024 (USD MILLION)

- TABLE 8 MAJOR COST DRIVERS AND IMPACT ON COST OF GOODS SOLD (COGS)

- TABLE 9 NOTABLE CANCER VACCINES IN CLINICAL TRIALS

- TABLE 10 AVERAGE SELLING PRICE TREND OF PEDIATRIC VACCINES, BY KEY PLAYER, 2023-2025 (USD)

- TABLE 11 AVERAGE SELLING PRICE TREND OF ADULT VACCINES, BY KEY PLAYER, 2023-2025 (USD)

- TABLE 12 AVERAGE SELLING PRICE TREND OF VACCINES, BY REGION, 2021-2023 (USD)

- TABLE 13 VACCINE PIPELINE PRODUCTS UNDER PHASE 3 CLINICAL TRIALS FOR RSV

- TABLE 14 VACCINE PIPELINE PRODUCTS UNDER PHASE 3 CLINICAL TRIALS FOR PNEUMOCOCCAL DISEASE

- TABLE 15 VACCINE PIPELINE PRODUCTS UNDER PHASE 3 CLINICAL TRIALS FOR INFLUENZA

- TABLE 16 KEY PIPELINE VACCINES: GSK PLC

- TABLE 17 KEY PIPELINE VACCINES: MERCK & CO., INC.

- TABLE 18 KEY PIPELINE VACCINES: PFIZER INC.

- TABLE 19 KEY PIPELINE VACCINES: SANOFI S.A.

- TABLE 20 VACCINES MARKET: ROLE IN ECOSYSTEM

- TABLE 21 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 22 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 23 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 24 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 25 MIDDLE EAST: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 26 AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 27 IMPORT VALUE FOR HS CODE 300220, 2020-2024 (USD THOUSAND)

- TABLE 28 IMPORT VOLUME FOR HS CODE 300220, 2020-2024 (TONS)

- TABLE 29 EXPORT VALUE FOR HS CODE 300220, 2020-2024 (USD THOUSAND)

- TABLE 30 EXPORT VOLUME FOR HS CODE 300220, 2020-2024 (TONS)

- TABLE 31 VACCINES MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 32 VACCINES MARKET: INDICATIVE LIST OF PATENTS, 2025

- TABLE 33 VACCINES MARKET: LIST OF CONFERENCES & EVENTS, 2025-2026

- TABLE 34 BUYING CRITERIA FOR VACCINES, BY END USER

- TABLE 35 KEY COMPANIES IMPLEMENTING AI

- TABLE 36 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 37 NUMBER OF VACCINES DELIVERED BY UNICEF, 2023-2025

- TABLE 38 WHO VACCINE PURCHASE DATABASE, BY PROCUREMENT MECHANISM, 2021-2023

- TABLE 39 WHO VACCINE PURCHASE DATABASE, BY MANUFACTURER, 2021-2023

- TABLE 40 WHO VACCINE PURCHASE DATABASE, BY INDICATION, 2021-2023

- TABLE 41 WHO VACCINE PURCHASE DATABASE, BY REGION, 2021-2023

- TABLE 42 VACCINE PRODUCTION CAPACITY, BY KEY PLAYER, 2024

- TABLE 43 VACCINES MARKET, BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 44 LIST OF COMMERCIALLY AVAILABLE PNEUMOCOCCAL DISEASE VACCINES

- TABLE 45 PNEUMOCOCCAL DISEASE VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 46 NORTH AMERICA: PNEUMOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 47 EUROPE: PNEUMOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 48 ASIA PACIFIC: PNEUMOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 49 LATIN AMERICA: PNEUMOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 50 LIST OF COMMERCIALLY AVAILABLE INFLUENZA VACCINES

- TABLE 51 INFLUENZA VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 52 NORTH AMERICA: INFLUENZA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 53 EUROPE: INFLUENZA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 54 ASIA PACIFIC: INFLUENZA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 55 LATIN AMERICA: INFLUENZA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 56 LIST OF COMMERCIALLY AVAILABLE COMBINATION VACCINES

- TABLE 57 COMBINATION VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 58 NORTH AMERICA: COMBINATION VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 59 EUROPE: COMBINATION VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 60 ASIA PACIFIC: COMBINATION VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 61 LATIN AMERICA: COMBINATION VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 62 LIST OF COMMERCIALLY AVAILABLE HPV VACCINES

- TABLE 63 HPV VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 64 NORTH AMERICA: HPV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 65 EUROPE: HPV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 66 ASIA PACIFIC: HPV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 67 LATIN AMERICA: HPV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 68 LIST OF COMMERCIALLY AVAILABLE MENINGOCOCCAL DISEASE VACCINES

- TABLE 69 MENINGOCOCCAL DISEASE VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 70 NORTH AMERICA: MENINGOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 71 EUROPE: MENINGOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 72 ASIA PACIFIC: MENINGOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 73 LATIN AMERICA: MENINGOCOCCAL DISEASE VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 74 LIST OF COMMERCIALLY AVAILABLE HERPES ZOSTER VACCINES

- TABLE 75 HERPES ZOSTER VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 76 NORTH AMERICA: HERPES ZOSTER VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 77 EUROPE: HERPES ZOSTER VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 78 ASIA PACIFIC: HERPES ZOSTER VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 79 LATIN AMERICA: HERPES ZOSTER VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 80 LIST OF COMMERCIALLY AVAILABLE ROTAVIRUS VACCINES

- TABLE 81 ROTAVIRUS VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 82 NORTH AMERICA: ROTAVIRUS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 83 EUROPE: ROTAVIRUS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 84 ASIA PACIFIC: ROTAVIRUS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 85 LATIN AMERICA: ROTAVIRUS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 86 TOP 10 COUNTRIES WITH MEASLES OUTBREAKS, JANUARY 2025-JULY 2025

- TABLE 87 LIST OF COMMERCIALLY AVAILABLE MMR VACCINES

- TABLE 88 MMR VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: MMR VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 90 EUROPE: MMR VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 91 ASIA PACIFIC: MMR VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 92 LATIN AMERICA: MMR VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 93 LIST OF COMMERCIALLY AVAILABLE VARICELLA VACCINES

- TABLE 94 VARICELLA VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 95 NORTH AMERICA: VARICELLA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 96 EUROPE: VARICELLA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 97 ASIA PACIFIC: VARICELLA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 98 LATIN AMERICA: VARICELLA VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 99 LIST OF COMMERCIALLY AVAILABLE HEPATITIS VACCINES

- TABLE 100 HEPATITIS VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 101 NORTH AMERICA: HEPATITIS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 102 EUROPE: HEPATITIS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 103 ASIA PACIFIC: HEPATITIS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 104 LATIN AMERICA: HEPATITIS VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 105 LIST OF COMMERCIALLY AVAILABLE DTP VACCINES

- TABLE 106 DTP VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 107 NORTH AMERICA: DTP VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 108 EUROPE: DTP VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 109 ASIA PACIFIC: DTP VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 110 LATIN AMERICA: DTP VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 111 POLIO VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 112 NORTH AMERICA: POLIO VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 113 EUROPE: POLIO VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 114 ASIA PACIFIC: POLIO VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 115 LATIN AMERICA: POLIO VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 116 RSV VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 117 NORTH AMERICA: RSV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 118 EUROPE: RSV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 119 ASIA PACIFIC: RSV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 120 LATIN AMERICA: RSV VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 121 COVID-19 VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 122 NORTH AMERICA: COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 123 EUROPE: COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 124 ASIA PACIFIC: COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 125 LATIN AMERICA: COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 126 LIST OF COMMERCIALLY AVAILABLE VACCINES FOR OTHER DISEASE INDICATIONS

- TABLE 127 VACCINES MARKET FOR OTHER DISEASE INDICATIONS, BY REGION, 2023-2030 (USD MILLION)

- TABLE 128 NORTH AMERICA: VACCINES MARKET FOR OTHER DISEASE INDICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 129 EUROPE: VACCINES MARKET FOR OTHER DISEASE INDICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 130 ASIA PACIFIC: VACCINES MARKET FOR OTHER DISEASE INDICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 131 LATIN AMERICA: VACCINES MARKET FOR OTHER DISEASE INDICATIONS, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 132 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 133 CONJUGATE VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 134 NORTH AMERICA: CONJUGATE VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 135 EUROPE: CONJUGATE VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 136 ASIA PACIFIC: CONJUGATE VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 137 LATIN AMERICA: CONJUGATE VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 138 EXAMPLES OF RECOMBINANT VACCINES

- TABLE 139 RECOMBINANT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 140 NORTH AMERICA: RECOMBINANT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 141 EUROPE: RECOMBINANT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 142 ASIA PACIFIC: RECOMBINANT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 143 LATIN AMERICA: RECOMBINANT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 144 EXAMPLES OF INACTIVATED & SUBUNIT VACCINES

- TABLE 145 INACTIVATED & SUBUNIT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 146 NORTH AMERICA: INACTIVATED & SUBUNIT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 147 EUROPE: INACTIVATED & SUBUNIT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 148 ASIA PACIFIC: INACTIVATED & SUBUNIT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 149 LATIN AMERICA: INACTIVATED & SUBUNIT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 150 EXAMPLES OF LIVE ATTENUATED VACCINES

- TABLE 151 LIVE ATTENUATED VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 152 NORTH AMERICA: LIVE ATTENUATED VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 153 EUROPE: LIVE ATTENUATED VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 154 ASIA PACIFIC: LIVE ATTENUATED VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 155 LATIN AMERICA: LIVE ATTENUATED VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 156 EXAMPLES OF TOXOID VACCINES

- TABLE 157 TOXOID VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 158 NORTH AMERICA: TOXOID VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 159 EUROPE: TOXOID VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 160 ASIA PACIFIC: TOXOID VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 161 LATIN AMERICA: TOXOID VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 162 OTHER VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 163 NORTH AMERICA: OTHER VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 164 EUROPE: OTHER VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 165 ASIA PACIFIC: OTHER VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 166 LATIN AMERICA: OTHER VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 167 COVID-19 VACCINES MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 168 MRNA COVID-19 VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 169 NORTH AMERICA: MRNA COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 170 EUROPE: MRNA COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 171 ASIA PACIFIC: MRNA COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 172 LATIN AMERICA: MRNA COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 173 VIRAL VECTOR COVID-19 VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 174 NORTH AMERICA: VIRAL VECTOR COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 175 EUROPE: VIRAL VECTOR COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 176 ASIA PACIFIC: VIRAL VECTOR COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 177 LATIN AMERICA: VIRAL VECTOR COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 178 OTHER COVID-19 VACCINES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 179 NORTH AMERICA: OTHER COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 180 EUROPE: OTHER COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 181 ASIA PACIFIC: OTHER COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 182 LATIN AMERICA: OTHER COVID-19 VACCINES MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 183 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 184 EXAMPLES OF MULTIVALENT VACCINES

- TABLE 185 MULTIVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 186 NORTH AMERICA: MULTIVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 187 EUROPE: MULTIVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 188 ASIA PACIFIC: MULTIVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 189 LATIN AMERICA: MULTIVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 190 EXAMPLES OF MONOVALENT VACCINES

- TABLE 191 MONOVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 192 NORTH AMERICA: MONOVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 193 EUROPE: MONOVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 194 ASIA PACIFIC: MONOVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 195 LATIN AMERICA: MONOVALENT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 196 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 197 ADVANTAGES AND DISADVANTAGES OF INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION

- TABLE 198 VACCINES MARKET FOR INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 199 NORTH AMERICA: VACCINES MARKET FOR INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 200 EUROPE: VACCINES MARKET FOR INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 201 ASIA PACIFIC: VACCINES MARKET FOR INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 202 LATIN AMERICA: VACCINES MARKET FOR INTRAMUSCULAR & SUBCUTANEOUS ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 203 VACCINES MARKET FOR ORAL ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 204 NORTH AMERICA: VACCINES MARKET FOR ORAL ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 205 EUROPE: VACCINES MARKET FOR ORAL ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 206 ASIA PACIFIC: VACCINES MARKET FOR ORAL ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 207 LATIN AMERICA: VACCINES MARKET FOR ORAL ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 208 VACCINES MARKET FOR OTHER ROUTES OF ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 209 NORTH AMERICA: VACCINES MARKET FOR OTHER ROUTES OF ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 210 EUROPE: VACCINES MARKET FOR OTHER ROUTES OF ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 211 ASIA PACIFIC: VACCINES MARKET FOR OTHER ROUTES OF ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 212 LATIN AMERICA: VACCINES MARKET FOR OTHER ROUTES OF ADMINISTRATION (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 213 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 214 ADULT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 215 NORTH AMERICA: ADULT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 216 EUROPE: ADULT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 217 ASIA PACIFIC: ADULT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 218 LATIN AMERICA: ADULT VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 219 PEDIATRIC VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 220 NORTH AMERICA: PEDIATRIC VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 221 EUROPE: PEDIATRIC VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 222 ASIA PACIFIC: PEDIATRIC VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 223 LATIN AMERICA: PEDIATRIC VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 224 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY REGION, 2023-2030 (USD MILLION)

- TABLE 225 NORTH AMERICA: KEY MACROINDICATORS

- TABLE 226 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 227 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 228 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 229 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 230 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 231 NORTH AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 232 US: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 233 US: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 234 US: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 235 US: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 236 US: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 237 CANADA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 238 CANADA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 239 CANADA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 240 CANADA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 241 CANADA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 242 EUROPE: KEY MACROINDICATORS

- TABLE 243 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 244 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 245 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 246 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 247 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 248 EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 249 GERMANY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 250 GERMANY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 251 GERMANY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 252 GERMANY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 253 GERMANY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 254 UK: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 255 UK: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 256 UK: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 257 UK: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 258 UK: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 259 FRANCE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 260 FRANCE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 261 FRANCE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 262 FRANCE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 263 FRANCE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 264 ITALY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 265 ITALY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 266 ITALY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 267 ITALY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 268 ITALY: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 269 SPAIN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 270 SPAIN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 271 SPAIN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 272 SPAIN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 273 SPAIN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 274 REST OF EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 275 REST OF EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 276 REST OF EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 277 REST OF EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 278 REST OF EUROPE: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 279 ASIA PACIFIC: KEY MACROINDICATORS

- TABLE 280 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 281 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 282 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 283 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 284 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 285 ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 286 CHINA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 287 CHINA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 288 CHINA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 289 CHINA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 290 CHINA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 291 JAPAN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 292 JAPAN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 293 JAPAN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 294 JAPAN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 295 JAPAN: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 296 INDIA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 297 INDIA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 298 INDIA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 299 INDIA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 300 INDIA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 301 SOUTH KOREA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 302 SOUTH KOREA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 303 SOUTH KOREA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 304 SOUTH KOREA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 305 SOUTH KOREA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 306 REST OF ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 307 REST OF ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 308 REST OF ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 309 REST OF ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 310 REST OF ASIA PACIFIC: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 311 LATIN AMERICA: KEY MACROINDICATORS

- TABLE 312 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY COUNTRY, 2023-2030 (USD MILLION)

- TABLE 313 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 314 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 315 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 316 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 317 LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 318 BRAZIL: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 319 BRAZIL: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 320 BRAZIL: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 321 BRAZIL: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 322 BRAZIL: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 323 MEXICO: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 324 MEXICO: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 325 MEXICO: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 326 MEXICO: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 327 MEXICO: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 328 REST OF LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 329 REST OF LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 330 REST OF LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 331 REST OF LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 332 REST OF LATIN AMERICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 333 MIDDLE EAST: KEY MACROINDICATORS

- TABLE 334 MIDDLE EAST: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 335 MIDDLE EAST: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 336 MIDDLE EAST: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 337 MIDDLE EAST: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 338 MIDDLE EAST: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 339 AFRICA: KEY MACROINDICATORS

- TABLE 340 AFRICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 341 AFRICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2023-2030 (USD MILLION)

- TABLE 342 AFRICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY DISEASE INDICATION, 2023-2030 (USD MILLION)

- TABLE 343 AFRICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2023-2030 (USD MILLION)

- TABLE 344 AFRICA: VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2023-2030 (USD MILLION)

- TABLE 345 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN VACCINES MARKET, JANUARY 2022-AUGUST 2025

- TABLE 346 VACCINES MARKET: DEGREE OF COMPETITION

- TABLE 347 VACCINES MARKET: REGION FOOTPRINT

- TABLE 348 VACCINES MARKET: TECHNOLOGY FOOTPRINT

- TABLE 349 VACCINES MARKET: TYPE FOOTPRINT

- TABLE 350 VACCINES MARKET: ROUTE OF ADMINISTRATION FOOTPRINT

- TABLE 351 VACCINES MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 352 VACCINES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 353 VACCINES MARKET: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 354 VACCINES MARKET: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 355 VACCINES MARKET: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 356 GSK PLC: COMPANY OVERVIEW

- TABLE 357 GSK PLC: PRODUCTS OFFERED

- TABLE 358 GSK PLC: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 359 GSK PLC: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 360 GSK PLC: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 361 MERCK & CO., INC.: COMPANY OVERVIEW

- TABLE 362 MERCK & CO., INC.: PRODUCTS OFFERED

- TABLE 363 MERCK & CO., INC.: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 364 MERCK & CO., INC.: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 365 MERCK & CO., INC.: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 366 PFIZER INC.: COMPANY OVERVIEW

- TABLE 367 PFIZER INC.: PRODUCTS OFFERED

- TABLE 368 PFIZER INC.: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 369 PFIZER INC.: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 370 SANOFI: COMPANY OVERVIEW

- TABLE 371 SANOFI: PRODUCTS OFFERED

- TABLE 372 SANOFI: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 373 SANOFI: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 374 SANOFI: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 375 SANOFI: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 376 CSL: COMPANY OVERVIEW

- TABLE 377 CSL: PRODUCTS OFFERED

- TABLE 378 CSL: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 379 CSL: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 380 CSL: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 381 EMERGENT: COMPANY OVERVIEW

- TABLE 382 EMERGENT: PRODUCTS OFFERED

- TABLE 383 EMERGENT: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 384 EMERGENT: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 385 JOHNSON & JOHNSON SERVICES INC.: COMPANY OVERVIEW

- TABLE 386 JOHNSON & JOHNSON SERVICES INC.: PRODUCTS OFFERED

- TABLE 387 JOHNSON & JOHNSON SERVICES INC.: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 388 ASTRAZENECA: COMPANY OVERVIEW

- TABLE 389 ASTRAZENECA: PRODUCTS OFFERED

- TABLE 390 ASTRAZENECA: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 391 ASTRAZENECA: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 392 ASTRAZENECA: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 393 SERUM INSTITUTE OF INDIA PVT., LTD.: COMPANY OVERVIEW

- TABLE 394 SERUM INSTITUTE OF INDIA PVT., LTD.: PRODUCTS OFFERED (SUPPLIED OVERSEAS)

- TABLE 395 SERUM INSTITUTE OF INDIA PVT., LTD.: PRODUCTS OFFERED (SUPPLIED IN INDIA)

- TABLE 396 SERUM INSTITUTE OF INDIA PVT., LTD.: PRODUCTS LAUNCHES & APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 397 SERUM INSTITUTE OF INDIA PVT., LTD.: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 398 SERUM INSTITUTE OF INDIA PVT., LTD.: EXPANSIONS, JANUARY 2022-AUGUST 2025

- TABLE 399 BAVARIAN NORDIC: COMPANY OVERVIEW

- TABLE 400 BAVARIAN NORDIC: PRODUCTS OFFERED

- TABLE 401 BAVARIAN NORDIC: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 402 BAVARIAN NORDIC: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 403 BAVARIAN NORDIC: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 404 MITSUBISHI TANABE PHARMA CORPORATION: COMPANY OVERVIEW

- TABLE 405 MITSUBISHI TANABE PHARMA CORPORATION: PRODUCTS OFFERED

- TABLE 406 MITSUBISHI TANABE PHARMA CORPORATION: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 407 MITSUBISHI TANABE PHARMA CORPORATION: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 408 DAIICHI SANKYO COMPANY, LIMITED: COMPANY OVERVIEW

- TABLE 409 DAIICHI SANKYO COMPANY, LIMITED: PRODUCTS OFFERED

- TABLE 410 DAIICHI SANKYO COMPANY, LIMITED: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 411 PANACEA BIOTEC: COMPANY OVERVIEW

- TABLE 412 PANACEA BIOTEC: PRODUCTS OFFERED

- TABLE 413 PANACEA BIOTEC: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 414 BIOLOGICAL E LIMITED: COMPANY OVERVIEW

- TABLE 415 BIOLOGICAL E LIMITED: PRODUCTS OFFERED (INDIAN MARKET)

- TABLE 416 BIOLOGICAL E LIMITED: PRODUCTS OFFERED (INTERNATIONAL MARKET)

- TABLE 417 BIOLOGICAL E LIMITED: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 418 BIOLOGICAL E LIMITED: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 419 BIOLOGICAL E LIMITED: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 420 BHARAT BIOTECH: COMPANY OVERVIEW

- TABLE 421 BHARAT BIOTECH: PRODUCTS OFFERED

- TABLE 422 BHARAT BIOTECH: PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 423 BHARAT BIOTECH: DEALS, JANUARY 2022-AUGUST 2025

- TABLE 424 NOVAVAX: COMPANY OVERVIEW

- TABLE 425 NOVAVAX: PRODUCTS OFFERED

- TABLE 426 NOVAVAX: PRODUCT APPROVALS, JANUARY 2022-AUGUST 2025

- TABLE 427 INOVIO PHARMACEUTICALS: COMPANY OVERVIEW

- TABLE 428 INOVIO PHARMACEUTICALS: PRODUCTS OFFERED

- TABLE 429 INOVIO PHARMACEUTICALS: OTHER DEVELOPMENTS, JANUARY 2022-AUGUST 2025

- TABLE 430 SINOVAC: COMPANY OVERVIEW

- TABLE 431 INCEPTA PHARMACEUTICALS LTD.: COMPANY OVERVIEW

- TABLE 432 VALNEVA SE: COMPANY OVERVIEW

- TABLE 433 VBI VACCINE INC.: COMPANY OVERVIEW

- TABLE 434 BIO FARMA: COMPANY OVERVIEW

- TABLE 435 MICROGEN: COMPANY OVERVIEW

- TABLE 436 ZHI FEI BIOLOGICAL: COMPANY OVERVIEW

- TABLE 437 INDIAN IMMUNOLOGICALS LIMITED: COMPANY OVERVIEW

List of Figures

- FIGURE 1 VACCINES MARKET SEGMENTATION & REGIONAL SCOPE

- FIGURE 2 VACCINES MARKET: RESEARCH DESIGN

- FIGURE 3 VACCINES MARKET: BREAKDOWN OF PRIMARIES (SUPPLY- AND DEMAND-SIDE PARTICIPANTS)

- FIGURE 4 VACCINES MARKET SIZE ESTIMATION (SUPPLY-SIDE ANALYSIS), 2024

- FIGURE 5 GLOBAL MARKET SIZE ESTIMATION: COMPANY REVENUE ANALYSIS (BOTTOM-UP APPROACH), 2024

- FIGURE 6 ILLUSTRATIVE EXAMPLE OF PFIZER INC.: REVENUE SHARE ANALYSIS, 2024

- FIGURE 7 ILLUSTRATIVE EXAMPLE OF INFLUENZA VACCINES: COMPANY REVENUE ANALYSIS (BOTTOM-UP APPROACH), 2024

- FIGURE 8 VACCINES MARKET: MARKET SIZE VALIDATION FROM PRIMARY SOURCES

- FIGURE 9 SEGMENTAL MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 10 VACCINES MARKET: CAGR PROJECTION (2025-2030)

- FIGURE 11 VACCINES MARKET: GROWTH ANALYSIS OF MARKET DYNAMICS

- FIGURE 12 DATA TRIANGULATION METHODOLOGY

- FIGURE 13 VACCINES MARKET, BY DISEASE INDICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TECHNOLOGY, 2025 VS. 2030 (USD MILLION)

- FIGURE 15 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY ROUTE OF ADMINISTRATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 17 VACCINES MARKET (EXCLUDING COVID-19 VACCINES), BY END USER, 2025 VS. 2030 (USD MILLION)

- FIGURE 18 REGIONAL SNAPSHOT OF VACCINES MARKET (EXCLUDING COVID-19 VACCINES)

- FIGURE 19 FOCUS ON VACCINE DEVELOPMENT & LAUNCHES TO PROPEL MARKET GROWTH

- FIGURE 20 US AND MULTIVALENT VACCINES SEGMENT COMMANDED LARGEST MARKET SHARES IN 2024

- FIGURE 21 CHINA TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 22 VACCINES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 23 US: NOVEL INFLUENZA A VIRUS CASES, BY SEASON (2010-2011 TO 2023-2024 SEASON)

- FIGURE 24 MANUFACTURING-RELATED PARAMETERS INCLUDED IN COST MODEL

- FIGURE 25 US: ESTIMATED NUMBER OF NEW CANCER CASES AND DEATHS BY SITE, 2025

- FIGURE 26 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 27 AVERAGE SELLING PRICE TREND OF VACCINES, BY DISEASE INDICATION, 2023-2025 (USD)

- FIGURE 28 VALUE CHAIN ANALYSIS: RAW MATERIAL AND MANUFACTURING PHASES TO CONTRIBUTE MAXIMUM VALUE

- FIGURE 29 VACCINES MARKET: CLINICAL TRIALS, BY PHASE

- FIGURE 30 VACCINES MARKET: CLINICAL TRIALS, BY DISEASE INDICATION

- FIGURE 31 VACCINES MARKET: ECOSYSTEM MARKET MAP

- FIGURE 32 VACCINES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 33 TOP APPLICANTS/OWNERS (COMPANIES) FOR VACCINES PATENTS, 2014-2024

- FIGURE 34 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF VACCINES

- FIGURE 35 KEY BUYING CRITERIA FOR END USERS

- FIGURE 36 BIOPHARMA MERGER & ACQUISITION (M&A) ACTIVITIES: INVESTMENT & FUNDING SCENARIO, 2020-2024

- FIGURE 37 VACCINES DEAL ACTIVITIES: INVESTMENT & FUNDING SCENARIO, 2017-2023

- FIGURE 38 AI USE CASES

- FIGURE 39 NORTH AMERICA: VACCINES MARKET SNAPSHOT (EXCLUDING COVID-19 VACCINES)

- FIGURE 40 ASIA PACIFIC: VACCINES MARKET SNAPSHOT (EXCLUDING COVID-19 VACCINES)

- FIGURE 41 REVENUE ANALYSIS OF KEY PLAYERS IN VACCINES MARKET, 2020-2024 (USD BILLION)

- FIGURE 42 MARKET SHARE ANALYSIS OF KEY PLAYERS IN VACCINES MARKET (2024)

- FIGURE 43 VACCINES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 44 VACCINES MARKET: COMPANY FOOTPRINT

- FIGURE 45 VACCINES MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 46 EV/EBITDA OF KEY VENDORS

- FIGURE 47 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 48 VACCINES MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 49 GSK PLC: COMPANY SNAPSHOT (2024)

- FIGURE 50 MERCK & CO., INC.: COMPANY SNAPSHOT (2024)

- FIGURE 51 PFIZER INC.: COMPANY SNAPSHOT (2024)

- FIGURE 52 SANOFI: COMPANY SNAPSHOT (2024)

- FIGURE 53 CSL: COMPANY SNAPSHOT (2024)

- FIGURE 54 EMERGENT: COMPANY SNAPSHOT (2024)

- FIGURE 55 JOHNSON & JOHNSON SERVICES INC.: COMPANY SNAPSHOT (2024)

- FIGURE 56 ASTRAZENECA: COMPANY SNAPSHOT (2024)

- FIGURE 57 BAVARIAN NORDIC: COMPANY SNAPSHOT (2024)

- FIGURE 58 DAIICHI SANKYO COMPANY, LIMITED: COMPANY SNAPSHOT (2024)

- FIGURE 59 PANACEA BIOTEC: COMPANY SNAPSHOT (2024)

- FIGURE 60 NOVAVAX: COMPANY SNAPSHOT (2024)

- FIGURE 61 INOVIO PHARMACEUTICALS: COMPANY SNAPSHOT (2024)

猴痘疫苗和治疗药物全球市场规模、份额、趋势和成长分析报告(2026-2034年)

猴痘疫苗和治疗药物全球市场规模、份额、趋势和成长分析报告(2026-2034年) 传染性鼻炎疫苗市场规模、份额和成长分析:按疫苗类型、给药途径、应用领域、最终用户、分销管道、地区和行业预测,2026-2033年

传染性鼻炎疫苗市场规模、份额和成长分析:按疫苗类型、给药途径、应用领域、最终用户、分销管道、地区和行业预测,2026-2033年 疫苗市场分析及预测(至2035年):类型、产品、技术、应用、最终使用者、流程、给药方式、材料类型及设备

疫苗市场分析及预测(至2035年):类型、产品、技术、应用、最终使用者、流程、给药方式、材料类型及设备 疫苗市场规模、份额和趋势分析报告:按适应症、类型、给药途径、年龄层、分销管道、地区和细分市场预测(2026-2033 年)

疫苗市场规模、份额和趋势分析报告:按适应症、类型、给药途径、年龄层、分销管道、地区和细分市场预测(2026-2033 年) 疫苗管瓶监测器市场 - 全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)全球重组疫苗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量、未来预测(2026-2034)

疫苗管瓶监测器市场 - 全球产业规模、份额、趋势、机会及按类型、应用、地区和竞争格局分類的预测(2021-2031年)全球重组疫苗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量、未来预测(2026-2034) 人用联合疫苗市场按产品类型、年龄层、联合类型、通路和地区划分全球疫苗市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的考量、未来预测(2026-2034)

人用联合疫苗市场按产品类型、年龄层、联合类型、通路和地区划分全球疫苗市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的考量、未来预测(2026-2034) 疫苗市场规模、份额和成长分析(按类型、给药途径、年龄层和地区划分)-2026-2033年产业预测

疫苗市场规模、份额和成长分析(按类型、给药途径、年龄层和地区划分)-2026-2033年产业预测 重组疫苗市场规模、份额及成长分析(按类型、疾病、最终用户、通路及地区划分)-2026-2033年产业预测

重组疫苗市场规模、份额及成长分析(按类型、疾病、最终用户、通路及地区划分)-2026-2033年产业预测