|

市场调查报告书

商品编码

1859661

全球应用现代化服务市场(至 2031 年)依服务类型(云端应用程式迁移、应用程式平台重构、后现代化)及应用类型(传统应用程式、云端託管应用程式、云端原生应用程式)划分Application Modernization Services Market by Service Type (Cloud Application Migration, Application Re-Platforming, Post Modernization), Application Type (Legacy, Cloud-hosted, Cloud-native) - Global Forecast to 2031 |

||||||

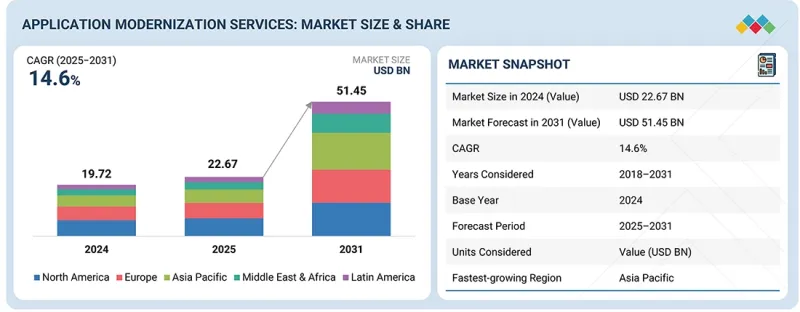

应用现代化服务市场预计将从 2025 年的 226.7 亿美元成长到 2031 年的 514.5 亿美元,复合年增长率为 14.6%。

| 调查范围 | |

|---|---|

| 调查年度 | 2018-2031 |

| 基准年 | 2024 |

| 预测期 | 2025-2031 |

| 单元 | 金额(美元) |

| 部分 | 服务类型、应用类型、产业、地区 |

| 目标区域 | 北美洲、欧洲、亚太地区、中东和非洲、拉丁美洲 |

应用现代化服务市场正因多种因素而蓬勃发展。在科技快速发展的时代,企业必须更新过时的应用软体才能保持竞争力并提高效率。通常情况下,随着企业业务规模、网路和覆盖范围的扩张,现有的旧有系统已无法满足当前的业务需求。这主要是由于规模限制、缺乏灵活性以及难以与新技术整合等原因造成的。

云端技术的日益普及是另一项关键成长要素,许多企业转向云端服务供应商以实现营运可扩展性和成本效益。这种数位转型正迫使企业对其应用程式进行改造,因为它们必须能够与人工智慧 (AI)、机器学习 (ML) 和物联网 (IoT) 等新兴技术无缝整合。

此外,随着对资料安全和合规性的日益重视,企业正积极迁移到新版本的应用程序,以满足不断变化的网路安全监管要求。同时,提升应用程式效能和使用者体验也是推动现代化趋势的重要因素。企业不断寻求改善客户与其数位化互动的方式。另一个关键驱动因素是提高敏捷性和产品上市速度,同时降低营运成本。应用程式现代化能够实现新功能和服务的快速部署。综上所述,这些因素共同推动了对应用程式现代化服务的需求,因为企业希望根据策略目标和营运效率重组其技术基础设施。

“预计在预测期内,云端原生应用领域将呈现最高的成长率。”

由于其在可扩展性、灵活性和效率方面的高成长潜力,预计该细分市场在预测期内将实现最高成长率。旧有应用程式通常以独立单元的形式交付,并依赖伺服器和资料中心等实体基础架构。相较之下,云端原生应用程式围绕着云端构建,并采用微服务、容器化启动和调度管理系统等先进的架构设计。这使得企业能够灵活应对业务环境的变化,根据需要扩展资源,并最大限度地降低不必要的营运成本。此外,云端基础方案的广泛应用和云端技术的成熟正在推动对云端原生应用程式的需求。这些解决方案克服了市场挑战,能够提供更快、更高品质的结果和优化的使用者体验。透过业务流程数位化来提高效率的持续努力也是一项关键的技术趋势。这促使人们开发出满足现代云端基础需求的高效能、响应迅速的系统解决方案,加速了向云端原生应用程式的转型,并推动了该细分市场的快速成长。

预计亚太地区在预测期内将实现最高的成长率。

推动这一成长的因素之一是该地区持续的数位转型。云端运算和其他新兴技术的日益普及,以及对营运效率的追求,都在推动成长。中国和印度等国的IT支出和数位化活动不断增加,从而带动了对现代化老旧管理系统和实施新技术服务的需求。全球技术供应商的进入和本土企业的崛起也活性化了市场竞争,加速了成长。此外,收入水准的提高和人口结构的变化(人口结构日益趋向技术化)也是推动该地区对高性能、大容量应用现代化服务需求的关键因素。

本报告调查了全球应用现代化服务市场,并提供了市场概况、影响市场成长的各种因素分析、技术和专利趋势、法律制度、案例研究、市场规模趋势和预测、按各个细分市场、地区/主要国家/地区进行的详细分析、竞争格局以及主要企业的概况。

目录

第一章 引言

第二章调查方法

第三章执行摘要

第四章重要考察

第五章 市场概览与产业趋势

- 市场动态

- 司机

- 抑制因素

- 机会

- 任务

- 应用现代化服务的演变

- 应用现代化服务:生态系分析

- 案例研究分析

- 供应链分析

- 监管状态

- 定价分析

- 波特五力分析

- 技术分析

- 专利分析

- 影响您业务的趋势/颠覆性因素

- 主要相关利益者和采购标准

- 2025-2026 年重要会议与活动

- 应用现代化服务市场技术蓝图

- 应用现代化服务市场的最佳实践

- 当前和新兴的经营模式经营模式

- 投资和资金筹措方案

- 生成式人工智慧对应用现代化服务市场的影响

- 2025年美国关税的影响概述

- 主要关税税率

- 价格影响分析

- 对国家的影响

- 产业

- 应用现代化的7个“R”

6. 按服务类型分類的应用现代化服务市场

- 市场驱动因素

- 应用组合评估

- 云端应用迁移

- 应用程式平台迁移

- 应用整合

- UI/UX现代化

- 晶粒服务

7. 按应用类型分類的应用现代化服务市场

- 市场驱动因素

- 旧有应用程式

- 云端託管应用程式

- 云端原生应用

8. 按垂直产业分類的应用现代化服务市场

- 市场驱动因素

- BFSI

- 资讯科技/资讯科技服务

- 医疗保健与生命科学

- 製造业

- 通讯

- 运输/物流

- 媒体与娱乐

- 零售与电子商务

- 政府

- 其他的

9. 按地区分類的应用现代化服务市场

- 北美洲

- 宏观经济展望

- 美国

- 加拿大

- 欧洲

- 宏观经济展望

- 英国

- 德国

- 法国

- 义大利

- 其他的

- 亚太地区

- 宏观经济展望

- 中国

- 日本

- 印度

- 其他的

- 中东和非洲

- 宏观经济展望

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 非洲

- 其他的

- 拉丁美洲

- 宏观经济展望

- 巴西

- 墨西哥

- 其他的

第十章 竞争格局

- 主要参与企业的策略/优势

- 市占率分析

- 收入分析

- 品牌/产品对比

- 估值和财务指标

- 公司评估矩阵:主要企业

- 公司估值矩阵:Start-Ups/中小企业

- 竞争场景

第十一章 公司简介

- 主要企业

- IBM

- MICROSOFT

- HCL TECHNOLOGIES

- ACCENTURE

- AWS

- ATOS

- CAPGEMINI

- ORACLE

- COGNIZANT

- TCS

- INNOVA SOLUTIONS

- EPAM SYSTEMS

- ASPIRE SYSTEMS

- NTT DATA

- DELL TECHNOLOGIES

- DXC TECHNOLOGY

- LTIMINDTREE

- INFOSYS

- WIPRO

- ROCKET SOFTWARE, INC.

- FUJITSU

- HEXAWARE TECHNOLOGIES

- VIRTUSA

- MONGODB

- SCIENCESOFT

- SIMFORM

- UTTHUNGA

- RISHABH SOFTWARE

- Start-Ups/中小企业

- SOFTURA

- CLOUDHEDGE TECHNOLOGIES PVT. LTD.

- D3V TECHNOLOGY

- BAYSHORE INTELLIGENCE SOLUTIONS

- OPINOV8

- ICREON

- SYMPHONY SOLUTIONS

- CLEVEROAD

- TECHAHEAD

- GEOMOTIV

- SOFT SUAVE

- PALMDIGITALZ

- AVERISOURCE

- VERITIS

第十二章:邻近及相关市场

第十三章附录

The Application modernization services market was estimated to be USD 22.67 billion in 2025 and is expected to reach USD 51.45 billion by 2031 at a compound annual growth rate (CAGR) of 14.6%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2031 |

| Base Year | 2024 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD) Million/Billion |

| Segments | By Service Type, Application Type, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

There are a few factors owing to which the application modernization services market is experiencing growth. In the era of rapid technological advancements, a business cannot afford to overlook the need to update its outdated applications in order to stay competitive and improve its efficiency. Often, when a business has grown sufficiently in scope, coverage, and network, the legacy systems in place can hardly meet current business demands because they are constrained by scale, flexibility, and integration with new-age technologies.

The increased use of cloud technology is another key driver, with many organizations aiming to utilize cloud providers due to the scalability and cost-effectiveness of their operations. As a result of this digital evolution, companies have been compelled to undergo application transformation, as it is essential that such applications integrate seamlessly with advanced technologies such as Artificial Intelligence, machine learning, and the Internet of Things.

Moreover, with the increasing focus on securing data and compliance, organizations are also actively migrating their deployments to newer versions of applications developed to meet the changing needs of regulations aimed at addressing cybersecurity issues. Additionally, better performance of applications and improving user experience with such applications are other reasons for enhanced modernization trends, since every business strives to improve how its customers interact with the business digitally. The need to reduce operating costs while increasing agility and speed to market is also a major factor, as application modernization enables the rollout of new features and services in a shorter period. Overall, these are the reasons for the high demand for services related to application modernization, as organizations seek to redesign their technological frameworks in response to their strategic objectives and operational effectiveness.

"The healthcare & life sciences vertical is expected to have the second-largest market size during the forecast period."

The healthcare sector is expected to capture a significant share of the application modernization services market, second only to the telecom industry, during the forecast period. This growth is driven by the rising demand for advanced digital solutions. The sector is undergoing a major transformation fueled by the increasing adoption of electronic health records, telemedicine, and AI-driven diagnostics. To support these advancements, healthcare providers require more efficient IT systems that enhance operational efficiency, improve patient care, and ensure compliance with regulatory standards. Additionally, the growing demand for cloud-based solutions that offer both security and scalability, along with seamless integration of new technologies into existing systems, continues to accelerate growth in this space.

"The cloud-native applications segment will witness the highest growth rate during the forecast period."

In the application modernization services, owing to their vast potential for growth in aspects such as scalability, flexibility, and efficiency over and above the others, cloud-native applications are projected to have a greater increase within the forecasted period. On the other hand, while legacy applications offer services as a single unit and often rely on underlying physical structures, such as servers and data centers, cloud-native applications are cloud-centric and are constructed using enhanced architectural designs, including those of microservices, containerized booting, and scheduling management systems. This allows players in the industry to adapt to changes in the business environment, increase resources when needed, and minimize unnecessary operational costs. Additionally, the increased use of cloud-based solutions and the maturation of cloud technologies are driving the need for cloud-native applications, as such solutions have overcome market challenges to deliver faster, better results, and an optimized user experience. The most important technological trend has also been the continuous and sustained drive towards digitalizing businesses' processes for improved efficiency, which therefore means the development of able and responsive system solutions to the modern need for cloud based solutions will make transition to the more use of cloud-native applications faster hence this explains the expected higher growth rate of such applications in the application modernization services market.

"Asia Pacific to register the highest growth rate during the forecast period."

The application modernization services market in the forecast period is expected to grow at a higher pace in the Asia-Pacific region, driven by several underlying factors. One of the reasons is the digital transformation of the region, which has been facilitated by the growing adoption of cloud computing and other emerging technologies, as well as the pursuit of efficiency in business operations. There is an increase in IT spending and digital activities in countries like China and India, creating a need for services to modernize aging management systems and incorporate new technologies. The growth of the sector is also enhanced by the efforts of global technology providers and the influx of local enterprises, which are enhancing competition. The increasing affluence of the population, along with the trend towards a more technologically inclined population, is another major factor driving the need for sophisticated and high-capacity application modernization services within the region.

Breakdown of primaries

The study offers insights from a range of industry experts, including solution vendors and Tier 1 companies. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 62%, Tier 2 - 23%, and Tier 3 - 15%

- By Designation: C-level -50%, D-level - 30%, and Others - 20%

- By Region: North America - 38%, Europe - 15%, Asia Pacific - 35%, Middle East & Africa - 7%, and Latin America - 5%.

The major players in the Application modernization services market include Oracle (US), IBM (US), Microsoft (US), AWS (US), HCL Technologies (India), Accenture (Ireland), ATOS (France), Capgemini (France), Cognizant (US), TCS (India), Aspire Systems (India), NTT Data Group Corporation (Japan), Infosys (India), Dell Technologies (US), Innova Solutions (US), EPAM Systems (US), DXC Technology (US), MongoDB (US), LTIMindtree (India), Wipro (India), Rocket Software (US), Fujitsu (Japan), Hexaware Technologies (India), Virtusa (US), Softura (US), CloudHedge (US), D3V Technology (US), Bayshore Intelligence (US), Opinov8 (UK), Icreon (US), Symphony Solutions (Netherlands), Cleveroad (Ukraine), Soft Suave (India), TechAhead (US), Geomotiv (US), PalmDigitalz (India), AveriSource (US), ScienceSoft (US), Simform (US), Utthunga (India), Rishabh Software (India), and Veritis (US). These players have adopted various growth strategies, including partnerships, agreements, collaborations, product launches, enhancements, and acquisitions, to expand their footprint in the application modernization services market.

Research Coverage

The market study covers the size of the application modernization services market across various segments. It aims to estimate the market size and growth potential across different segments, including service types, application types, verticals, and regions. The service type includes application portfolio assessment, cloud application migration, application re-platforming, application integration, UI/UX modernization, and post-modernization. Further, the application types include legacy applications, cloud-hosted applications, and cloud-native applications. The verticals include BFSI, healthcare & life sciences, telecom, IT & ITeS, retail & e-commerce, government, energy & utilities, transportation & logistics, media & entertainment, and manufacturing. The regional analysis of the Application modernization services market covers North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America. The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of the global Application Modernization Services market's revenue numbers and subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. Moreover, the report will provide stakeholders with insights into the market's pulse, as well as information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. Analysis of key drivers (rising digital transformation initiatives, demand for flexibility and scalability through cloud computing, rapid technological advancements), restraints (high costs and complexity, legacy system dependencies), opportunities (emerging markets and SMEs, evolution of open standards for software development), and challenges (vendor lock-in and platform dependencies, managing technical debt) influencing the growth of the application modernization services market.

2. Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the application modernization services market.

3. Market Development: Comprehensive information about lucrative markets - the report analyses the application modernization services market across various regions.

4. Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the application modernization services market.

5. Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as Oracle (US), IBM (US), Microsoft (US), AWS (US), HCL Technologies (India), Accenture (Ireland), ATOS SE (France), Capgemini (France), Cognizant (US), Tata Consultancy Services (India), Aspire Systems (India), NTT Data Group Corporation (Japan), Infosys (India), Dell Technologies (US), Innova Solutions (US), EPAM Systems (US), DXC Technology (US), MongoDB (US), LTIMindtree (India), Wipro (India), Rocket Software (US), Fujitsu (Japan), Hexaware Technologies (India), Virtusa (US), Softura (US), CloudHedge (US), D3V Technology (US), Bayshore Intelligence (US), Opinov8 (UK), Icreon (US), Symphony Solutions (Netherlands), Cleveroad (Ukraine), Soft Suave (India), TechAhead (US), Geomotiv (US), PalmDigitalz (India), AveriSource (US), ScienceSoft (US), Simform (US), Utthunga (India), Rishabh Software (India), and Veritis (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 Breakdown of primary profiles

- 2.1.2.3 Key insights from industry experts

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 TOP-DOWN APPROACH

- 2.2.2 BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 LIMITATIONS AND RISK ASSESSMENT

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR KEY PLAYERS IN APPLICATION MODERNIZATION SERVICES MARKET

- 4.2 APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE

- 4.3 APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE

- 4.4 APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL

- 4.5 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE AND APPLICATION TYPE

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rise in digital transformation initiatives

- 5.2.1.2 Demand for flexibility and scalability through cloud computing

- 5.2.1.3 Rapid technological advancements

- 5.2.1.4 Shift toward modernization by cloud-native technologies

- 5.2.1.5 Stringent regulatory compliance and security

- 5.2.2 RESTRAINTS

- 5.2.2.1 High costs and complexity

- 5.2.2.2 Legacy system dependencies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Proliferation of Kubernetes and containerization

- 5.2.3.2 Evolution of open standards for software development

- 5.2.3.3 Emerging markets and SMEs

- 5.2.3.4 Existence of large number of legacy applications

- 5.2.4 CHALLENGES

- 5.2.4.1 Vendor lock-in and platform dependencies

- 5.2.4.2 Managing technical debt

- 5.2.1 DRIVERS

- 5.3 EVOLUTION OF APPLICATION MODERNIZATION SERVICES

- 5.4 APPLICATION MODERNIZATION SERVICES: ECOSYSTEM ANALYSIS

- 5.5 CASE STUDY ANALYSIS

- 5.5.1 AIRBNB MODERNIZED RUBY ON RAILS MONOLITH USING KUBERNETES TO REDUCE TECH DEBT

- 5.5.2 MODERNIZATION OF ATRUVIA AG'S BANKING APPLICATION

- 5.5.3 LEGACY SYSTEMS' MODERNIZATION FOR BIOPHARMA BY HCL ON AWS

- 5.5.4 APPLICATION MODERNIZATION FOR LEADING MEDICAL LABORATORY RESULTING IN BETTER ROI

- 5.5.5 UNIPER ENERGY'S UK TRADING SOLUTIONS MODERNIZED BY INFOSYS

- 5.6 SUPPLY CHAIN ANALYSIS

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.7.2 REGULATIONS

- 5.7.2.1 North America

- 5.7.2.1.1 US

- 5.7.2.1.2 Canada

- 5.7.2.2 Europe

- 5.7.2.2.1 UK

- 5.7.2.2.2 Germany

- 5.7.2.3 Asia Pacific

- 5.7.2.3.1 South Korea

- 5.7.2.3.2 China

- 5.7.2.3.3 Japan

- 5.7.2.3.4 India

- 5.7.2.4 Middle East & Africa

- 5.7.2.4.1 UAE

- 5.7.2.4.2 KSA

- 5.7.2.5 Latin America

- 5.7.2.5.1 Brazil

- 5.7.2.5.2 Mexico

- 5.7.2.1 North America

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SERVICE TYPE, 2024

- 5.8.2 INDICATIVE PRICING ANALYSIS, BY SERVICE FEATURE, 2024

- 5.9 PORTER'S FIVE FORCES ANALYSIS

- 5.9.1 THREAT OF NEW ENTRANTS

- 5.9.2 THREAT OF SUBSTITUTES

- 5.9.3 BARGAINING POWER OF BUYERS

- 5.9.4 BARGAINING POWER OF SUPPLIERS

- 5.9.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 Cloud platforms

- 5.10.1.2 Containerization

- 5.10.1.3 DevOps tools and CI/CD pipelines

- 5.10.1.4 Microservices architecture

- 5.10.1.5 API management platforms

- 5.10.1.6 Low-code/No-code platforms

- 5.10.2 ADJACENT TECHNOLOGIES

- 5.10.2.1 Edge computing

- 5.10.2.2 5G and next-generation networks

- 5.10.2.3 Blockchain

- 5.10.2.4 Quantum computing

- 5.10.2.5 Augmented reality (AR) and virtual reality (VR)

- 5.10.3 COMPLEMENTARY TECHNOLOGIES

- 5.10.3.1 AI/ML integration

- 5.10.3.2 Robotic process automation (RPA)

- 5.10.3.3 Identity and access management (IAM)

- 5.10.3.4 Data lakes and data warehousing

- 5.10.3.5 Enterprise service bus (ESB)

- 5.10.1 KEY TECHNOLOGIES

- 5.11 PATENT ANALYSIS

- 5.12 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.13.2 BUYING CRITERIA

- 5.14 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.15 TECHNOLOGY ROADMAP FOR APPLICATION MODERNIZATION SERVICES MARKET

- 5.15.1 SHORT-TERM ROADMAP (2026-2027)

- 5.15.2 MID-TERM ROADMAP (2028-2029)

- 5.15.3 LONG-TERM ROADMAP (2030-2031)

- 5.16 BEST PRACTICES IN APPLICATION MODERNIZATION SERVICES MARKET

- 5.16.1 CONDUCT THOROUGH ASSESSMENT

- 5.16.2 DEFINE CLEAR GOALS AND OBJECTIVES

- 5.16.3 DEVELOP MODERNIZATION ROADMAP

- 5.16.4 CHOOSE RIGHT MODERNIZATION APPROACH

- 5.16.5 PRIORITIZE APPLICATIONS FOR MODERNIZATION

- 5.16.6 OPTIMIZE FOR CLOUD

- 5.16.7 ENSURE CONTINUOUS MONITORING AND OPTIMIZATION

- 5.16.8 ENGAGE STAKEHOLDERS THROUGHOUT PROCESS

- 5.17 CURRENT AND EMERGING BUSINESS MODELS

- 5.17.1 PLATFORM-AS-A-SERVICE (PAAS)

- 5.17.2 CONSULTATIVE SERVICES MODEL

- 5.17.3 OUTCOME-BASED MODELS

- 5.17.4 OPEN-SOURCE MODEL

- 5.17.5 CO-DEVELOPMENT MODEL

- 5.17.6 AUTOMATED MODELS

- 5.18 INVESTMENT AND FUNDING SCENARIO

- 5.19 IMPACT OF GENERATIVE AI ON APPLICATION MODERNIZATION SERVICES MARKET

- 5.19.1 IMPACT OF AI/GENERATIVE AI ON APPLICATION MODERNIZATION SERVICES

- 5.19.2 USE CASES OF GENERATIVE AI IN APPLICATION MODERNIZATION SERVICES

- 5.19.3 BEST PRACTICES

- 5.19.3.1 BFSI Industry

- 5.19.3.2 IT & ITeS Industry

- 5.19.3.3 Telecom Industry

- 5.19.4 CASE STUDIES OF GENERATIVE AI IMPLEMENTATION

- 5.19.4.1 Modernizing a mission critical banking app

- 5.19.4.2 Cloud-first ERP renewal for a manufacturer

- 5.19.4.3 Zero-downtime auction platform scale-out

- 5.19.5 CLIENT READINESS AND IMPACT ASSESSMENT

- 5.19.5.1 Client A: Global retail bank

- 5.19.5.2 Client B: Industrial manufacturer

- 5.19.5.3 Client C: Digital marketplace

- 5.20 IMPACT OF 2025 US TARIFF - OVERVIEW

- 5.20.1 INTRODUCTION

- 5.21 KEY TARIFF RATES

- 5.22 PRICE IMPACT ANALYSIS

- 5.23 IMPACT ON COUNTRY/REGION

- 5.23.1 NORTH AMERICA

- 5.23.2 EUROPE

- 5.23.3 APAC

- 5.24 INDUSTRIES

- 5.25 7 'R'S OF APPLICATION MODERNIZATION

- 5.25.1 REHOST

- 5.25.2 RE-PLATFORM

- 5.25.3 REFACTOR

- 5.25.4 REVISE

- 5.25.5 REBUILD

- 5.25.6 REPLACE

- 5.25.7 RETIRE

6 APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE

- 6.1 INTRODUCTION

- 6.1.1 SERVICE TYPE: MARKET DRIVERS

- 6.1.2 APPLICATION PORTFOLIO ASSESSMENT

- 6.1.2.1 Need for strategic evaluation to streamline modernization paths to drive initial adoption of portfolio assessments

- 6.1.3 CLOUD APPLICATION MIGRATION

- 6.1.3.1 Rapid adoption of cloud infrastructure to support these services as businesses seek scalability and cost-efficiency

- 6.1.4 APPLICATION RE-PLATFORMING

- 6.1.4.1 Demand for performance optimization without complete rewrites

- 6.1.5 APPLICATION INTEGRATION

- 6.1.5.1 Increase in complexity of hybrid environments to drive need for seamless application integration across cloud and legacy systems

- 6.1.6 UI/UX MODERNIZATION

- 6.1.6.1 Growth in emphasis on user-centric digital experiences to sustain demand for UI/UX modernization

- 6.1.7 POST-MODERNIZATION SERVICES

- 6.1.7.1 Ongoing need for support in maintaining modernized applications to ensure steady, albeit slower, growth of post-modernization services

7 APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE

- 7.1 INTRODUCTION

- 7.1.1 APPLICATION TYPE: MARKET DRIVERS

- 7.1.2 LEGACY APPLICATIONS

- 7.1.2.1 Need to reduce operational costs of legacy applications and integrate with modern technologies

- 7.1.3 CLOUD-HOSTED APPLICATIONS

- 7.1.3.1 Growth in demand for scalable and cost-efficient IT infrastructure to fuel adoption of cloud-hosted application modernization

- 7.1.4 CLOUD-NATIVE APPLICATIONS

- 7.1.4.1 Push for innovation, scalability, and speed in digital transformation to drive rapid adoption of cloud-native applications

8 APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL

- 8.1 INTRODUCTION

- 8.1.1 VERTICAL: MARKET DRIVERS

- 8.2 BFSI

- 8.2.1 NEED FOR SECURE, SCALABLE, AND EFFICIENT FINANCIAL SERVICES

- 8.2.2 BFSI: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.2.2.1 Core banking system modernization

- 8.2.2.2 Claims processing overhaul

- 8.2.2.3 Digital customer portals

- 8.2.2.4 Real-time risk management

- 8.2.2.5 Payment gateway integration

- 8.3 IT & ITES

- 8.3.1 NEED FOR AGILE SERVICE DELIVERY AND TECHNOLOGICAL INTEGRATION

- 8.3.2 IT & ITES: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.3.2.1 ERP cloud migration

- 8.3.2.2 Unified IT management systems

- 8.3.2.3 Customer support systems modernization

- 8.3.2.4 Cloud-native software optimization

- 8.3.2.5 Hybrid cloud management systems

- 8.4 HEALTHCARE & LIFE SCIENCES

- 8.4.1 NEED FOR IMPROVED PATIENT CARE, DIGITAL HEALTH SOLUTIONS, AND EFFICIENT DATA MANAGEMENT

- 8.4.2 HEALTHCARE & LIFE SCIENCES: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.4.2.1 EHR cloud migration

- 8.4.2.2 Pharmaceutical research modernization

- 8.4.2.3 Health insurance claims

- 8.4.2.4 Telemedicine platforms

- 8.4.2.5 Medical device connectivity

- 8.5 MANUFACTURING

- 8.5.1 DRIVE TOWARD SMART FACTORIES AND REAL-TIME SUPPLY CHAIN OPTIMIZATION

- 8.5.2 MANUFACTURING: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.5.2.1 Smart factory implementations

- 8.5.2.2 Predictive maintenance solutions

- 8.5.2.3 Integrated supply chain management

- 8.5.2.4 Quality control enhancements

- 8.5.2.5 Collaborative robotics integration

- 8.6 TELECOM

- 8.6.1 RAPID GROWTH OF 5G NETWORKS AND DEMAND FOR ENHANCED SERVICE DELIVERY

- 8.6.2 TELECOM: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.6.2.1 5G network management modernization

- 8.6.2.2 Cloud-based CRM systems

- 8.6.2.3 Billing system integration

- 8.6.2.4 Network automation

- 8.6.2.5 Self-service portal modernization

- 8.7 TRANSPORTATION & LOGISTICS

- 8.7.1 DEMAND FOR REAL-TIME VISIBILITY AND OPERATIONAL EFFICIENCY

- 8.7.2 TRANSPORTATION & LOGISTICS: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.7.2.1 Cloud-based fleet management systems

- 8.7.2.2 Integrated warehouse management

- 8.7.2.3 Enhanced shipping portals

- 8.7.2.4 Visibility and responsiveness improvements

- 8.7.2.5 Predictive analytics for demand forecasting

- 8.8 MEDIA & ENTERTAINMENT

- 8.8.1 NEED FOR INNOVATIVE CONTENT DELIVERY AND PERSONALIZED VIEWER EXPERIENCES

- 8.8.2 MEDIA & ENTERTAINMENT: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.8.2.1 Cloud-based content delivery networks

- 8.8.2.2 Personalized user experiences

- 8.8.2.3 Digital asset management systems

- 8.8.2.4 Enhanced audience analytics

- 8.8.2.5 Integrated marketing solutions

- 8.9 RETAIL & E-COMMERCE

- 8.9.1 ADOPTION OF PERSONALIZED CUSTOMER EXPERIENCES AND STREAMLINED OPERATIONS

- 8.9.2 RETAIL & E-COMMERCE: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.9.2.1 Cloud-based inventory management

- 8.9.2.2 Customer loyalty program modernization

- 8.9.2.3 POS and e-commerce integration

- 8.9.2.4 Demand forecasting modernization

- 8.9.2.5 Scalable e-commerce platforms

- 8.10 GOVERNMENT

- 8.10.1 NEED FOR ENHANCED CITIZEN ENGAGEMENT AND EFFICIENT SERVICE DELIVERY

- 8.10.2 GOVERNMENT: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.10.2.1 Citizen services cloud migration

- 8.10.2.2 Document management system overhaul

- 8.10.2.3 Inter-agency communication integration

- 8.10.2.4 User-friendly public service apps

- 8.10.2.5 Disaster recovery planning

- 8.11 OTHER VERTICALS

- 8.11.1 OTHER VERTICALS: APPLICATION MODERNIZATION SERVICE USE CASES

- 8.11.1.1 Cloud-based booking systems

- 8.11.1.2 Personalized travel recommendations

- 8.11.1.3 Cloud-based student information systems

- 8.11.1.4 Interactive virtual classrooms

- 8.11.1.5 Adaptive learning platforms

- 8.11.1 OTHER VERTICALS: APPLICATION MODERNIZATION SERVICE USE CASES

9 APPLICATION MODERNIZATION SERVICES MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 9.2.2 US

- 9.2.2.1 Rise in prevalence of AI advancements, automation, and next-gen network technologies

- 9.2.3 CANADA

- 9.2.3.1 Government-backed digital initiatives and cloud adoption to fuel modernization across public and private sectors

- 9.3 EUROPE

- 9.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 9.3.2 UK

- 9.3.2.1 Stringent regulations support adoption of application modernization services in UK

- 9.3.3 GERMANY

- 9.3.3.1 Strong focus on Industry 4.0 and smart manufacturing, and need for advanced networking solutions

- 9.3.4 FRANCE

- 9.3.4.1 Increased demand for digital services and automation to boost modernization across sectors

- 9.3.5 ITALY

- 9.3.5.1 Transformation of legacy infrastructure, particularly in finance and telecom

- 9.3.6 REST OF EUROPE

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 9.4.2 CHINA

- 9.4.2.1 Significant investments by key players and need for rapid development and adoption of new technologies

- 9.4.3 JAPAN

- 9.4.3.1 Increase in adoption of advanced technologies and integration with AI and automation

- 9.4.4 INDIA

- 9.4.4.1 Growing focus on cloud and network connectivity powered by AI technology

- 9.4.5 REST OF ASIA PACIFIC

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 9.5.2 UAE

- 9.5.2.1 Economic Vision 2030's focus on digital transformation to key driver for modernization in public and private sectors

- 9.5.3 KSA

- 9.5.3.1 Saudi's need for digital transformation driven by Vision 2030 agenda

- 9.5.4 AFRICA

- 9.5.4.1 Growing need for digital infrastructure and modernized telecom and financial systems

- 9.5.5 REST OF MIDDLE EAST & AFRICA

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 9.6.2 BRAZIL

- 9.6.2.1 Ongoing investments in telecom infrastructure and modernization projects

- 9.6.3 MEXICO

- 9.6.3.1 Shift toward cloud modernization in public and financial sectors

- 9.6.4 REST OF LATIN AMERICA

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 10.3 MARKET SHARE ANALYSIS

- 10.3.1 MARKET RANKING ANALYSIS

- 10.4 REVENUE ANALYSIS, 2020-2024

- 10.5 BRAND/PRODUCT COMPARISON

- 10.6 COMPANY VALUATION AND FINANCIAL METRICS

- 10.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 10.7.1 STARS

- 10.7.2 EMERGING LEADERS

- 10.7.3 PERVASIVE PLAYERS

- 10.7.4 PARTICIPANTS

- 10.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 10.7.5.1 Company footprint

- 10.7.5.2 Service type footprint

- 10.7.5.3 Application type footprint

- 10.7.5.4 Vertical footprint

- 10.7.5.5 Regional footprint

- 10.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 10.8.1 PROGRESSIVE COMPANIES

- 10.8.2 RESPONSIVE COMPANIES

- 10.8.3 DYNAMIC COMPANIES

- 10.8.4 STARTING BLOCKS

- 10.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.8.5.1 Key startups/SMEs

- 10.8.5.2 Competitive benchmarking of key startups/SMEs

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES

- 10.9.2 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 IBM

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Solutions/Services offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Product launches

- 11.1.1.3.2 Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses and competitive threats

- 11.1.2 MICROSOFT

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Solutions/Services offered

- 11.1.2.3 Recent developments

- 11.1.2.3.1 Product launches

- 11.1.2.3.2 Deals

- 11.1.2.4 MnM view

- 11.1.2.4.1 Key strengths

- 11.1.2.4.2 Strategic choices

- 11.1.2.4.3 Weaknesses and competitive threats

- 11.1.3 HCL TECHNOLOGIES

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Solutions/Services offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Product launches

- 11.1.3.3.2 Deals

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses and competitive threats

- 11.1.4 ACCENTURE

- 11.1.4.1 Business overview

- 11.1.4.2 Platforms/Solutions/Services offered

- 11.1.4.3 Recent developments

- 11.1.4.3.1 Deals

- 11.1.4.4 MnM view

- 11.1.4.4.1 Key strengths

- 11.1.4.4.2 Strategic choices

- 11.1.4.4.3 Weaknesses and competitive threats

- 11.1.5 AWS

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Solutions/Services offered

- 11.1.5.3 Recent developments

- 11.1.5.3.1 Deals

- 11.1.5.4 MnM view

- 11.1.5.4.1 Right to win

- 11.1.5.4.2 Strategic choices

- 11.1.5.4.3 Weaknesses and competitive threats

- 11.1.6 ATOS

- 11.1.6.1 Business overview

- 11.1.6.2 Platforms/Solutions/Services offered

- 11.1.6.3 Recent developments

- 11.1.6.3.1 Product launches

- 11.1.6.3.2 Deals

- 11.1.6.4 MnM view

- 11.1.6.4.1 Key strengths

- 11.1.6.4.2 Strategic choices

- 11.1.6.4.3 Weaknesses and competitive threats

- 11.1.7 CAPGEMINI

- 11.1.7.1 Business overview

- 11.1.7.2 Platforms/Solutions/Services offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Product launches

- 11.1.7.3.2 Deals

- 11.1.7.4 MnM view

- 11.1.7.4.1 Key strengths

- 11.1.7.4.2 Strategic choices

- 11.1.7.4.3 Weaknesses and competitive threats

- 11.1.8 ORACLE

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Solutions/Services offered

- 11.1.8.3 Recent developments

- 11.1.8.3.1 Product launches

- 11.1.8.3.2 Deals

- 11.1.8.4 MnM view

- 11.1.8.4.1 Key strengths

- 11.1.8.4.2 Strategic choices

- 11.1.8.4.3 Weaknesses and competitive threats

- 11.1.9 COGNIZANT

- 11.1.9.1 Business overview

- 11.1.9.2 Platforms/Solutions/Services offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Deals

- 11.1.10 TCS

- 11.1.10.1 Business overview

- 11.1.10.2 Platforms/Solutions/Services offered

- 11.1.10.3 Recent developments

- 11.1.10.3.1 Product launches

- 11.1.10.3.2 Deals

- 11.1.11 INNOVA SOLUTIONS

- 11.1.12 EPAM SYSTEMS

- 11.1.13 ASPIRE SYSTEMS

- 11.1.14 NTT DATA

- 11.1.15 DELL TECHNOLOGIES

- 11.1.16 DXC TECHNOLOGY

- 11.1.17 LTIMINDTREE

- 11.1.18 INFOSYS

- 11.1.19 WIPRO

- 11.1.20 ROCKET SOFTWARE, INC.

- 11.1.21 FUJITSU

- 11.1.22 HEXAWARE TECHNOLOGIES

- 11.1.23 VIRTUSA

- 11.1.24 MONGODB

- 11.1.25 SCIENCESOFT

- 11.1.26 SIMFORM

- 11.1.27 UTTHUNGA

- 11.1.28 RISHABH SOFTWARE

- 11.1.1 IBM

- 11.2 STARTUPS/SMES

- 11.2.1 SOFTURA

- 11.2.2 CLOUDHEDGE TECHNOLOGIES PVT. LTD.

- 11.2.3 D3V TECHNOLOGY

- 11.2.4 BAYSHORE INTELLIGENCE SOLUTIONS

- 11.2.5 OPINOV8

- 11.2.6 ICREON

- 11.2.7 SYMPHONY SOLUTIONS

- 11.2.8 CLEVEROAD

- 11.2.9 TECHAHEAD

- 11.2.10 GEOMOTIV

- 11.2.11 SOFT SUAVE

- 11.2.12 PALMDIGITALZ

- 11.2.13 AVERISOURCE

- 11.2.14 VERITIS

12 ADJACENT AND RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 DIGITAL TRANSFORMATION MARKET

- 12.2.1 MARKET DEFINITION

- 12.3 MAINFRAME MODERNIZATION MARKET

- 12.3.1 MARKET DEFINITION

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2020-2024

- TABLE 2 APPLICATION MODERNIZATION SERVICES MARKET: ECOSYSTEM

- TABLE 3 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 4 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SERVICE TYPE, 2024

- TABLE 8 INDICATIVE PRICING LEVELS OF APPLICATION MODERNIZATION SERVICES, 2024

- TABLE 9 PORTER'S FIVE FORCES IMPACT ON APPLICATION MODERNIZATION SERVICES MARKET

- TABLE 10 LIST OF KEY PATENTS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- TABLE 12 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- TABLE 13 APPLICATION MODERNIZATION SERVICES MARKET: DETAILED LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 14 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 15 EXPECTED CHANGE IN PRICES AND LIKELY IMPACT ON END-USE MARKET DUE TO TARIFF IMPACT

- TABLE 16 APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 17 APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 18 APPLICATION PORTFOLIO ASSESSMENT SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 19 APPLICATION PORTFOLIO ASSESSMENT SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 20 CLOUD APPLICATION MIGRATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 21 CLOUD APPLICATION MIGRATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 22 APPLICATION RE-PLATFORMING SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 23 APPLICATION RE-PLATFORMING SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 24 APPLICATION INTEGRATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 25 APPLICATION INTEGRATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 26 UI/UX MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 27 UI/UX MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 28 POST-MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 29 POST-MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 30 APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 31 APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 32 LEGACY APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 33 LEGACY APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 34 CLOUD-HOSTED APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 35 CLOUD-HOSTED APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 36 CLOUD-NATIVE APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 37 CLOUD-NATIVE APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 38 APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 39 APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 40 APPLICATION MODERNIZATION SERVICES MARKET IN BFSI, BY REGION, 2018-2024 (USD MILLION)

- TABLE 41 APPLICATION MODERNIZATION SERVICES MARKET IN BFSI, BY REGION, 2025-2031 (USD MILLION)

- TABLE 42 APPLICATION MODERNIZATION SERVICES MARKET IN IT & ITES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 43 APPLICATION MODERNIZATION SERVICES MARKET IN IT & ITES, BY REGION, 2025-2031 (USD MILLION)

- TABLE 44 APPLICATION MODERNIZATION SERVICES MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 45 APPLICATION MODERNIZATION SERVICES MARKET IN HEALTHCARE & LIFE SCIENCES, BY REGION, 2025-2031 (USD MILLION)

- TABLE 46 APPLICATION MODERNIZATION SERVICES MARKET IN MANUFACTURING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 47 APPLICATION MODERNIZATION SERVICES MARKET IN MANUFACTURING, BY REGION, 2025-2031 (USD MILLION)

- TABLE 48 APPLICATION MODERNIZATION SERVICES MARKET IN TELECOM, BY REGION, 2018-2024 (USD MILLION)

- TABLE 49 APPLICATION MODERNIZATION SERVICES MARKET IN TELECOM, BY REGION, 2025-2031 (USD MILLION)

- TABLE 50 APPLICATION MODERNIZATION SERVICES MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 51 APPLICATION MODERNIZATION SERVICES MARKET IN TRANSPORTATION & LOGISTICS, BY REGION, 2025-2031 (USD MILLION)

- TABLE 52 APPLICATION MODERNIZATION SERVICES MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 53 APPLICATION MODERNIZATION SERVICES MARKET IN MEDIA & ENTERTAINMENT, BY REGION, 2025-2031 (USD MILLION)

- TABLE 54 APPLICATION MODERNIZATION SERVICES MARKET IN RETAIL & E-COMMERCE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 55 APPLICATION MODERNIZATION SERVICES MARKET IN RETAIL & E-COMMERCE, BY REGION, 2025-2031 (USD MILLION)

- TABLE 56 APPLICATION MODERNIZATION SERVICES MARKET IN GOVERNMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 57 APPLICATION MODERNIZATION SERVICES MARKET IN GOVERNMENT, BY REGION, 2025-2031 (USD MILLION)

- TABLE 58 APPLICATION MODERNIZATION SERVICES MARKET IN OTHER VERTICALS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 59 APPLICATION MODERNIZATION SERVICES MARKET IN OTHER VERTICALS, BY REGION, 2025-2031 (USD MILLION)

- TABLE 60 APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2018-2024 (USD MILLION)

- TABLE 61 APPLICATION MODERNIZATION SERVICES MARKET, BY REGION, 2025-2031 (USD MILLION)

- TABLE 62 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 63 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 64 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 65 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 66 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 67 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 68 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 69 NORTH AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 70 US: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 71 US: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 72 US: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 73 US: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 74 US: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 75 US: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 76 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 77 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 78 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 79 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 80 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 81 CANADA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 82 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 83 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 84 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 85 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 86 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 87 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 88 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 89 EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 90 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 91 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 92 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 93 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 94 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 95 UK: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 96 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 97 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 98 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 99 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 100 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 101 GERMANY: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 102 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 103 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 104 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 105 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 106 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 107 FRANCE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 108 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 109 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 110 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 111 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 112 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 113 ITALY: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 114 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 115 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 116 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 117 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 118 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 119 REST OF EUROPE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 120 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 121 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 122 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 123 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 124 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 125 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 126 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 127 ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 128 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 129 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 130 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 131 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 132 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 133 CHINA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 134 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 135 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 136 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 137 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 138 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 139 JAPAN: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 140 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 141 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 142 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 143 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 144 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 145 INDIA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 146 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 147 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 148 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 149 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 150 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 151 REST OF ASIA PACIFIC: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 152 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 153 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 154 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 155 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 156 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 157 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 158 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 159 MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 160 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 161 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 162 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 163 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 164 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 165 UAE: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 166 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 167 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 168 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 169 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 170 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 171 KSA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 172 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 173 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 174 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 175 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 176 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 177 AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 178 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 179 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 180 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 181 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 182 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 183 REST OF MIDDLE EAST & AFRICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 184 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 185 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 186 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 187 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 188 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 189 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 190 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 191 LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY COUNTRY, 2025-2031 (USD MILLION)

- TABLE 192 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 193 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 194 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 195 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 196 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 197 BRAZIL: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 198 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 199 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 200 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 201 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 202 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 203 MEXICO: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 204 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2018-2024 (USD MILLION)

- TABLE 205 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY SERVICE TYPE, 2025-2031 (USD MILLION)

- TABLE 206 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2018-2024 (USD MILLION)

- TABLE 207 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY APPLICATION TYPE, 2025-2031 (USD MILLION)

- TABLE 208 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2018-2024 (USD MILLION)

- TABLE 209 REST OF LATIN AMERICA: APPLICATION MODERNIZATION SERVICES MARKET, BY VERTICAL, 2025-2031 (USD MILLION)

- TABLE 210 OVERVIEW OF STRATEGIES ADOPTED BY KEY APPLICATION MODERNIZATION SERVICES PLAYERS, JANUARY 2022-JULY 2025

- TABLE 211 APPLICATION MODERNIZATION SERVICES MARKET: DEGREE OF COMPETITION

- TABLE 212 SERVICE TYPE FOOTPRINT, 2024

- TABLE 213 APPLICATION TYPE FOOTPRINT, 2024

- TABLE 214 VERTICAL FOOTPRINT, 2024

- TABLE 215 REGIONAL FOOTPRINT, 2024

- TABLE 216 APPLICATION MODERNIZATION SERVICES MARKET: KEY STARTUPS/SMES, 2024

- TABLE 217 APPLICATION MODERNIZATION SERVICES MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

- TABLE 218 APPLICATION MODERNIZATION SERVICES MARKET: PRODUCT LAUNCHES, JANUARY 2022-AUGUST 2024

- TABLE 219 APPLICATION MODERNIZATION SERVICES MARKET: DEALS, JANUARY 2022-AUGUST 2024

- TABLE 220 IBM: COMPANY OVERVIEW

- TABLE 221 IBM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 222 IBM: PRODUCT LAUNCHES

- TABLE 223 IBM: DEALS

- TABLE 224 MICROSOFT: COMPANY OVERVIEW

- TABLE 225 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 MICROSOFT: PRODUCT LAUNCHES

- TABLE 227 MICROSOFT: DEALS

- TABLE 228 HCL TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 229 HCL TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 230 HCL TECHNOLOGIES: PRODUCT LAUNCHES

- TABLE 231 HCL TECHNOLOGIES: DEALS

- TABLE 232 ACCENTURE: COMPANY OVERVIEW

- TABLE 233 ACCENTURE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 234 ACCENTURE: DEALS

- TABLE 235 AWS: COMPANY OVERVIEW

- TABLE 236 AWS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 AWS: DEALS

- TABLE 238 ATOS: COMPANY OVERVIEW

- TABLE 239 ATOS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 240 ATOS: PRODUCT LAUNCHES

- TABLE 241 ATOS: DEALS

- TABLE 242 CAPGEMINI: COMPANY OVERVIEW

- TABLE 243 CAPGEMINI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 CAPGEMINI: PRODUCT LAUNCHES

- TABLE 245 CAPGEMINI: DEALS

- TABLE 246 ORACLE: COMPANY OVERVIEW

- TABLE 247 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 248 ORACLE: PRODUCT LAUNCHES

- TABLE 249 ORACLE: DEALS

- TABLE 250 COGNIZANT: COMPANY OVERVIEW

- TABLE 251 COGNIZANT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 252 COGNIZANT: DEALS

- TABLE 253 TCS: COMPANY OVERVIEW

- TABLE 254 TCS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 255 TCS: PRODUCT LAUNCHES

- TABLE 256 TCS: DEALS

- TABLE 257 DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 258 DIGITAL TRANSFORMATION MARKET, BY OFFERING, 2024-2030 (USD MILLION)

- TABLE 259 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2019-2023 (USD BILLION)

- TABLE 260 DIGITAL TRANSFORMATION MARKET, BY TECHNOLOGY, 2024-2030 (USD BILLION)

- TABLE 261 DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2019-2023 (USD BILLION)

- TABLE 262 DIGITAL TRANSFORMATION MARKET, BY BUSINESS FUNCTION, 2024-2030 (USD BILLION)

- TABLE 263 DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2019-2023 (USD BILLION)

- TABLE 264 DIGITAL TRANSFORMATION MARKET, BY VERTICAL, 2024-2030 (USD BILLION)

- TABLE 265 DIGITAL TRANSFORMATION MARKET, BY REGION, 2019-2023 (USD BILLION)

- TABLE 266 DIGITAL TRANSFORMATION MARKET, BY REGION, 2024-2030 (USD BILLION)

- TABLE 267 MAINFRAME MODERNIZATION MARKET, BY OFFERING, 2019-2024 (USD MILLION)

- TABLE 268 MAINFRAME MODERNIZATION MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 269 MAINFRAME MODERNIZATION MARKET, BY ORGANIZATION SIZE, 2019-2024 (USD MILLION)

- TABLE 270 MAINFRAME MODERNIZATION MARKET, BY ORGANIZATION SIZE, 2025-2030 (USD MILLION)

- TABLE 271 MAINFRAME MODERNIZATION MARKET, BY VERTICAL, 2019-2024 (USD MILLION)

- TABLE 272 MAINFRAME MODERNIZATION MARKET, BY VERTICAL, 2025-2030 (USD MILLION)

- TABLE 273 MAINFRAME MODERNIZATION MARKET, BY REGION, 2019-2024 (USD MILLION)

- TABLE 274 MAINFRAME MODERNIZATION MARKET, BY REGION, 2025-2030 (USD MILLION)

List of Figures

- FIGURE 1 APPLICATION MODERNIZATION SERVICES MARKET SEGMENTATION

- FIGURE 2 APPLICATION MODERNIZATION SERVICES MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 KEY INDUSTRY INSIGHTS

- FIGURE 5 APPLICATION MODERNIZATION SERVICES MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 6 APPROACH 1 (SUPPLY SIDE): REVENUE OF VENDORS IN APPLICATION MODERNIZATION SERVICES MARKET

- FIGURE 7 APPROACH 2 (DEMAND SIDE): APPLICATION MODERNIZATION SERVICES MARKET

- FIGURE 8 MARKET SIZE ESTIMATION METHODOLOGY: DEMAND-SIDE ANALYSIS

- FIGURE 9 MARKET SIZE ESTIMATION USING BOTTOM-UP APPROACH

- FIGURE 10 DATA TRIANGULATION

- FIGURE 11 APPLICATION MODERNIZATION SERVICES MARKET, 2024-2031 (USD MILLION)

- FIGURE 12 APPLICATION MODERNIZATION SERVICES MARKET, BY REGION

- FIGURE 13 RAPID ADOPTION OF CLOUD-NATIVE TECHNOLOGIES AND AI-DRIVEN AUTOMATION ACTS AS OPPORTUNITY IN APPLICATION MODERNIZATION SERVICES MARKET

- FIGURE 14 CLOUD APPLICATION MIGRATION SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 15 LEGACY APPLICATIONS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 16 BFSI SEGMENT TO ACCOUNT FOR SIGNIFICANT MARKET SHARE

- FIGURE 17 CLOUD APPLICATION MIGRATION AND LEGACY APPLICATION SEGMENTS TO ACCOUNT FOR SIGNIFICANT MARKET SHARES IN 2025

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: APPLICATION MODERNIZATION SERVICES MARKET

- FIGURE 19 EVOLUTION OF APPLICATION MODERNIZATION SERVICES

- FIGURE 20 KEY PLAYERS IN APPLICATION MODERNIZATION SERVICES MARKET ECOSYSTEM

- FIGURE 21 APPLICATION MODERNIZATION SERVICES MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 22 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SERVICE TYPE, 2024 (USD)

- FIGURE 23 APPLICATION MODERNIZATION SERVICES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 24 PATENT ANALYSIS FOR APPLICATION MODERNIZATION SERVICES, 2016-2025

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE VERTICALS

- FIGURE 27 KEY BUYING CRITERIA FOR TOP THREE VERTICALS

- FIGURE 28 INVESTMENT AND FUNDING SCENARIO, 2022-2024 (USD MILLION)

- FIGURE 29 USE CASES OF GENERATIVE AI IN APPLICATION MODERNIZATION SERVICES

- FIGURE 30 GENERATIVE AI BEST PRACTICES ACROSS MAJOR INDUSTRIES

- FIGURE 31 CLOUD APPLICATION MIGRATION SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 32 CLOUD-NATIVE APPLICATIONS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 33 TELECOM SEGMENT TO REGISTER HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 34 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 35 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 36 SHARE OF LEADING COMPANIES IN APPLICATION MODERNIZATION SERVICES MARKET, 2024

- FIGURE 37 MARKET RANKING ANALYSIS OF TOP FIVE PLAYERS

- FIGURE 38 REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024 (USD MILLION)

- FIGURE 39 APPLICATION MODERNIZATION SERVICES MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 40 FINANCIAL METRICS OF KEY APPLICATION MODERNIZATION SERVICES VENDORS, 2025

- FIGURE 41 COMPANY VALUATION, 2025

- FIGURE 42 APPLICATION MODERNIZATION SERVICES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 43 COMPANY FOOTPRINT, 2024

- FIGURE 44 APPLICATION MODERNIZATION SERVICES MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 45 IBM: COMPANY SNAPSHOT

- FIGURE 46 MICROSOFT: COMPANY SNAPSHOT

- FIGURE 47 HCL TECHNOLOGIES: COMPANY SNAPSHOT

- FIGURE 48 ACCENTURE: COMPANY SNAPSHOT

- FIGURE 49 AWS: COMPANY SNAPSHOT

- FIGURE 50 ATOS: COMPANY SNAPSHOT

- FIGURE 51 CAPGEMINI: COMPANY SNAPSHOT

- FIGURE 52 ORACLE: COMPANY SNAPSHOT

- FIGURE 53 COGNIZANT: COMPANY SNAPSHOT

- FIGURE 54 TCS: COMPANY SNAPSHOT

2026年全球应用现代化服务市场报告

2026年全球应用现代化服务市场报告 应用现代化系统整合商市场规模、份额和成长分析:按现代化类型、部署模式、组织规模、最终用户和地区划分 - 2026-2033 年行业预测

应用现代化系统整合商市场规模、份额和成长分析:按现代化类型、部署模式、组织规模、最终用户和地区划分 - 2026-2033 年行业预测 2026-2030年全球应用现代化服务市场

2026-2030年全球应用现代化服务市场 应用现代化服务市场分析及预测(至 2035 年):按类型、产品、服务、技术、组件、应用、流程、部署模式、最终用户和解决方案划分

应用现代化服务市场分析及预测(至 2035 年):按类型、产品、服务、技术、组件、应用、流程、部署模式、最终用户和解决方案划分 全球大型主机现代化服务市场规模、份额、趋势和成长分析报告(2026-2034年)

全球大型主机现代化服务市场规模、份额、趋势和成长分析报告(2026-2034年) 大型主机现代化与迁移服务市场:按服务类型、组织规模、部署模式、迁移类型和产业垂直领域划分 - 全球预测 2026-2032 年大型主机现代化市场:按类型、部署模式、组织规模和产业垂直领域划分 - 2026-2032 年全球预测

大型主机现代化与迁移服务市场:按服务类型、组织规模、部署模式、迁移类型和产业垂直领域划分 - 全球预测 2026-2032 年大型主机现代化市场:按类型、部署模式、组织规模和产业垂直领域划分 - 2026-2032 年全球预测 全球电信IT现代化服务市场:预测至2032年-按用例、合作模式、部署方式、组织规模、技术、最终用户和地区进行分析电信BSS现代化市场预测至2032年:按组件、部署模式、组织规模、最终用户和地区分類的全球分析

全球电信IT现代化服务市场:预测至2032年-按用例、合作模式、部署方式、组织规模、技术、最终用户和地区进行分析电信BSS现代化市场预测至2032年:按组件、部署模式、组织规模、最终用户和地区分類的全球分析 应用现代化服务市场规模、份额和成长分析(按应用程式、部署类型、最终用户和地区划分)—2026-2033年产业预测

应用现代化服务市场规模、份额和成长分析(按应用程式、部署类型、最终用户和地区划分)—2026-2033年产业预测