|

市场调查报告书

商品编码

1718485

智慧商业建筑联网平台市场(2025-2030)-物联网市场规模与竞争格局IoT Platforms in Smart Commercial Buildings 2025 to 2030 - Total IoT Market Sizing & Competitive Landscape |

||||||

探索智慧建筑中的物联网平台生态系统:2030 年完整市场分析

随着商业大楼转变为响应式、数据驱动的环境,物联网平台正在成为将先前脱节的系统连接到统一网路的关键编排层。这份综合报告揭示了全球楼宇物联网市场到 2030 年将如何成长到 1,010 亿美元,并重塑办公室、零售、饭店和资料中心的房地产营运。

我们的分析清楚地展现了碎片化的物联网平台生态系统,并研究了领先供应商到 2030 年的架构演进、竞争定位和策略路线图。透过对三种情境的详细市场预测和针对不同利害关係人群体量身定制的可行建议,本报告提供了利用新兴技术并将技术投资与可衡量的业务成果联繫起来所需的策略情报。

本研究包括三电子錶格和一个包含高解析度图形和图表的简报文件。本报告是我们 2025 年物联网报告系列的第二份,第一份是关于物联网设备的。该研究是我们 2025 年企业订阅服务报告的一部分。

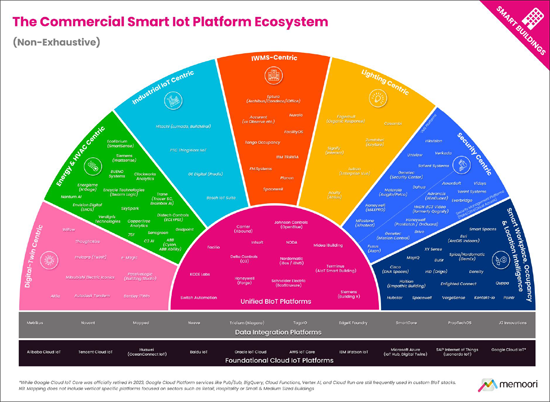

为了帮助您驾驭分散且快速发展的 BIoT 平台解决方案市场,本报告提供了两个关键资源:物联网平台生态系统的高阶映射(见上文)和附录 A 中的结构化平台比较。虽然我们对市场进行了广泛而系统的研究,但需要注意的是,生态系统地图并非旨在列出所有供应商。

在此映射中,Memoori 将每个平台分类为最能反映其关键策略定位和平台能力的部分。

关于物联网平台的热门议题

- 评估物联网平台时,组织应该寻找哪些关键功能? 寻找开放式架构来防止供应商锁定、用于供应商中立整合的单独资料层以及强大的安全协定。儘管各大供应商都在向统一平台迈进,但没有一家供应商能够提供涵盖所有建筑系统的综合解决方案。组织应优先考虑互通性和模组化方法,以允许最佳解决方案有效地协同工作。

- 除了行销炒作之外,人工智慧如何改变建筑运作?人工智慧正在三个明确的领域从理论转向实践:包括能够主动调整暖通空调的操作预测、比传统方法提前几天识别设备故障的故障检测演算法,以及可将消耗降低 15-25% 的自主能源优化。像BrainBox AI这样的公司已经被收购。然而,市场仍然存在着两种类型:纯人工智慧驱动的平台和仅以 "人工智慧" 为幌子提供基于规则的自动化的平台。

- 最近的併购交易揭示了竞争格局的哪些面向? 2023 年及以后计划进行的 168 亿美元併购交易表明,传统原始设备製造商 (OEM) 将数位平台定位为其未来收入模式的核心。 特灵和施耐德电机等企业买家正在引领收购,将投资重点放在符合永续发展趋势的资本充足平台上。为了与整合平台竞争,小型供应商被迫透过专门的功能和不同的商业模式来实现差异化。

这份长达 152 页、包含 18 幅图表的报告提炼了所有关键事实并得出结论,以便您能够准确瞭解哪些因素正在塑造商业智慧建筑的未来。

- 可行的转型路线图:利用针对建筑业主、平台供应商、设施经理和投资者的客製化策略建议来解决当前的采用障碍,并使您的组织能够利用新的平台融合趋势。

- 多重情境市场预测:透过三种经济情境的详细预测来应对前所未有的市场不确定性,并按技术类别、建筑类型和地区细分到 2030 年的成长预测。

- 全面的供应商格局分析:我们使用专有的评估框架对87家平台供应商进行评估,该框架突破行销宣传,揭示他们在多系统整合、边缘运算、安全协定和人工智慧实施成熟度方面的实际能力。

本报告提供了有价值的信息,帮助公司改善其策略规划和考虑业务发展机会。

谁应该购买此报告?

对于建筑业主、技术提供者和投资者来说,瞭解这种不断变化的情况对于在日益复杂的市场中保持竞争优势至关重要。

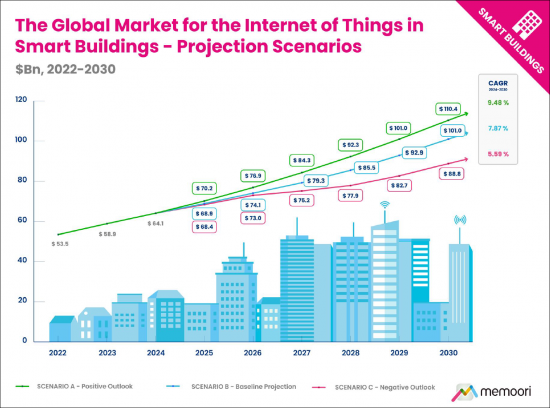

在基准情境下,全球建筑物连网市场预计将从 2024 年的 641 亿美元成长到 2030 年的 1,010 亿美元(复合年增长率为 7.87%),远低于 10-16% 的历史成长率。鑑于前所未有的宏观经济不确定性,我们制定了三种不同的预测情境:正面展望(复合年增长率 9.48%)、基线预测(复合年增长率 7.87%)和负面展望(复合年增长率 5.59%)。数据整合、分析和软体是规模最大、成长最快的类别(复合年增长率为 9.53%),这表明市场越来越关注软体定义的价值,而不是硬体。

目录

前言

执行摘要

第1章简介

- 智慧商业建筑物连网市场概览

- 绘製 BIoT 供应链图

- 物联网解决方案的成熟度与市场发展

第2章影响BIoT市场的经济与政策压力

- 评估贸易战的影响

- 中美贸易与技术摩擦

- 更广泛的区域贸易和政策影响

- 评估更广泛的技术市场的现状

第3章市场规模评估与区域分析

- 市场预测情景

- 情境框架与假设

- 情境预测

- 全球市场细分

- 按硬体、软体和服务划分的市场

- 以建筑类型划分的市场

- 按应用程式细分的市场

- 区域预测与分析

- 北美

- 拉丁美洲

- 亚太地区

- 欧洲

- 中东和非洲

第4章 物联网平台

- 物联网平台在智慧商业建筑中的作用

- BIoT 堆迭

第5章 物联网平台生态系及竞争格局

- 绘製物联网平台生态系图

- 竞争格局评估

- 底层云物联网平台

- 资料整合平台

- 以数位孪生为中心的平台

- 以能源和暖通空调为中心的平台

- 以工业物联网为中心的平台

- 以 IWMS 为中心的平台

- 以照明为中心的平台

- 以安全为中心的平台

- 智慧工作场所/占用/位置智慧平台

- 整合的BIoT平台

- 产业特定平台

- 值得关注的平台趋势

- 融合与整合的动态

- 迈向开放、模组化、可扩充的 BIoT 平台

- 不断发展的计算模型

- 人工智慧、分析与自主控制

- 不断发展的商业模式

- 风险管理

- 区域市场动态与市场分化

- 对利害关係人的建议

- 解决 BIoT 平台中的常见课题

- 评估平台成熟度的清单

- 针对不同利害关係人群体的策略建议

第6章 併购与投资趋势

- 投资

- 合併与收购

Navigate the Smart Building IoT Platforms Ecosystem: Complete Market Analysis Through to 2030

As commercial buildings transform into responsive, data-driven environments, IoT platforms have emerged as the critical orchestration layer connecting previously isolated systems into unified networks. This comprehensive report reveals how the global Building IoT market will grow to $101 billion by 2030, reshaping property operations across offices, retail, hospitality, and data centers.

Our analysis provides clarity on the fragmented IoT platforms ecosystem, examining the architectural evolution, competitive positioning, and strategic roadmaps of key vendors through to 2030. With detailed market forecasts across three scenarios and actionable recommendations tailored to different stakeholder groups, this report delivers the strategic intelligence needed to capitalize on emerging technologies and align technology investments with measurable business outcomes.

The research includes 3 spreadsheets AND a presentation file with high-resolution versions of the charts. It is the 2nd in our 2025 series of IoT reports, with the 1st on IoT Devices. The research is included in our 2025 Enterprise Subscription Service.

To help navigate the fragmented and rapidly evolving market for BIoT platform solutions, this report provides two key resources: a high-level mapping of the IoT platform ecosystem (see above) and a structured platform comparison presented in Appendix A. While we conducted a broad and systematic survey of the market, it is important to note that the Ecosystem Map is not intended to include every single vendor.

It should also be noted that many vendors could arguably fit into multiple segments, depending on how their portfolios and go-to-market strategies are interpreted. For the purposes of this mapping, Memoori has placed each platform into the segment that we assess best reflects its primary strategic positioning and platform functionality.

KEY QUESTIONS ADDRESSED ABOUT IOT PLATFORMS:

- What key capabilities should organizations look for when evaluating IoT platforms? Look for open architectures to prevent vendor lock-in, independent data layers for vendor-neutral integration, and robust security protocols. Despite the trend toward unified platforms from major vendors, no single provider offers comprehensive solutions across all building systems. Organizations should prioritize interoperability and modular approaches that allow best-of-breed solutions to work together effectively.

- How is AI transforming building operations beyond the marketing hype? AI is moving from theory to practice in three obvious areas: occupancy prediction that enables proactive HVAC adjustments, fault detection algorithms that identify equipment failures days before traditional methods, and autonomous energy optimization that reduces consumption by 15-25%. Companies like BrainBox AI are being acquired specifically for these capabilities. However, the market remains fragmented between genuinely AI-driven platforms and those merely offering rule-based automation rebranded as "artificial intelligence."

- What does recent M&A activity reveal about the competitive landscape? The $16.8 billion in M&A transactions since 2023 shows traditional OEMs positioning digital platforms at the center of future revenue models. Corporate buyers like Trane and Schneider Electric are dominating acquisitions, while investment is concentrating among well-capitalized platforms aligned with sustainability trends. Smaller vendors face growing pressure to differentiate through specialized functionality or different business models to compete against integrated platforms.

WITHIN ITS 152 PAGES AND 18 CHARTS AND TABLES, THE REPORT FILTERS OUT ALL THE KEY FACTS AND DRAWS CONCLUSIONS, SO YOU CAN UNDERSTAND EXACTLY WHAT IS SHAPING THE FUTURE OF COMMERCIAL SMART BUILDINGS.

- Actionable Transformation Roadmaps: Leverage tailored strategic recommendations for building owners, platform vendors, facility managers, and investors that address immediate adoption barriers while positioning organizations to capitalize on emerging platform convergence trends.

- Multi-Scenario Market Forecasts: Navigate unprecedented market uncertainty with detailed projections across three economic scenarios, breaking down growth expectations by technology category, building type, and geographic region through 2030.

- Comprehensive Vendor Landscape Analysis: Evaluate 87 platform providers using our proprietary assessment framework that cuts through marketing claims to reveal actual capabilities in multi-system integration, edge computing, security protocols, and AI implementation maturity.

This report provides valuable information to companies so they can improve their strategic planning exercises AND look at the potential for developing their business.

WHO SHOULD BUY THIS REPORT?

For building owners, technology providers, and investors, understanding this evolving landscape has become essential for maintaining a competitive advantage in an increasingly complex market.

The report projects the global Building IoT market will grow from $64.1 billion in 2024 to $101.0 billion by 2030 (7.87% CAGR) under our baseline scenario, significantly lower than historical growth rates of 10-16%. We've developed three distinct projection scenarios to account for unprecedented macroeconomic uncertainty: Positive Outlook (9.48% CAGR), Baseline Projection (7.87% CAGR), and Negative Outlook (5.59% CAGR). Data Integration, Analytics & Software represents the largest and fastest-growing category (9.53% CAGR), indicating a market increasingly focused on software-defined value rather than hardware.

Table of Contents

Preface

Executive Summary

1. Introduction

- 1.1. Overview of the IoT Market in Smart Commercial Buildings

- 1.2. Mapping the BIoT Supply Chain

- 1.3. IoT Solution Maturity and Market Evolution

2. Economic and Policy Pressures Impacting BIoT Markets

- 2.1. Evaluating the Impact of the Trade War

- 2.1.1. US-China Trade and Technology Tensions

- 2.1.2. Broader Regional Trade and Policy Impacts

- 2.2. Evaluating the State of Broader Technology Markets

3. Market Sizing & Regional Analysis

- 3.1. Market Projection Scenarios

- 3.1.1. Scenario Framework and Assumptions

- 3.1.2. Scenario Forecasts

- 3.2. Global Market Breakdowns

- 3.2.1. Market Breakdown by Hardware, Software & Services

- 3.2.2. Market Breakdown by Building Vertical

- 3.2.3. Market Breakdown by Application

- 3.3. Regional Forecasts & Analysis

- 3.3.1. North America

- 3.3.2. Latin America

- 3.3.3. Asia Pacific

- 3.3.4. Europe

- 3.3.5. Middle East & Africa

4. IoT Platforms

- 4.1. The Role of IoT Platforms in Smart Commercial Buildings

- 4.2. The BIoT Stack

5. The IoT Platform Ecosystem & Competitive Landscape

- 5.1. Mapping the IoT Platform Ecosystem

- 5.2. Evaluating the Competitive Landscape

- 5.2.1. Foundational Cloud IoT Platforms

- 5.2.2. Data Integration Platforms

- 5.2.3. Digital Twin-Centric Platforms

- 5.2.4. Energy & HVAC-Centric Platforms

- 5.2.5. Industrial IoT-Centric Platforms

- 5.2.6. IWMS-Centric Platforms

- 5.2.7. Lighting-Centric Platforms

- 5.2.8. Security-Centric Platforms

- 5.2.9. Smart Workplace / Occupancy / Location Intelligence Platforms

- 5.2.10. Unified BIoT Platforms

- 5.2.11. Vertical Specific Platforms

- 5.3. Notable Platform Trends

- 5.3.1. Convergence and Integration Dynamics

- 5.3.2. A Shift Towards Open, Modular, and Scalable BIoT Platforms

- 5.3.3. Evolving Computational Models

- 5.3.4. AI, Analytics, and Autonomous Control

- 5.3.5. Evolving Business Models

- 5.3.6. Risk Management

- 5.3.7. Regional Market Dynamics & Market Bifurcation

- 5.4. Recommendations for Stakeholders

- 5.4.1. Navigating Common Challenges in BIoT Platforms

- 5.4.2. A Checklist for Evaluating Platform Maturity

- 5.4.3. Strategic Recommendations by Stakeholder Group

6. M&A & Investment Trends

- 6.1. Investments

- 6.1.1. Notable Investment Trends

- 6.2. Mergers & Acquisitions

- 6.2.1. Notable M&A Trends

List of Charts and Figures

- Fig 1.1: The Internet of Things in Smart Commercial Buildings 2025 v6.0

- Fig 1.2: The BIoT Supply Chain

- Fig 1.3: BIoT Solution Maturity

- Fig 2.1: US/China Trade Barriers - A Timeline - 2018 to Present

- Fig 3.1: The Global Market for the Internet of Things in Smart Building - Projection Scenarios to 2030

- Fig 3.2: The Global Market for the Internet of Things in Smart Building, Breakdown by Hardware, Software & Services 2024

- Fig 3.3: Market Breakdown by Hardware, Software & Services, Breakdown by Category 2024

- Fig 3.4: The Internet of Things in Smart Commercial Buildings Market by Vertical 2024

- Fig 3.5: The Internet of Things in Smart Commercial Buildings Market by Application 2024

- Fig 3.6: Regional Growth Indicators

- Fig 3.7: The Internet of Things in Smart Commercial Buildings Market by Region 2024

- Fig 3.8: The Market for the Internet of Things in Smart Commercial Buildings North America 2024

- Fig 3.9: The Market for the Internet of Things in Smart Commercial Buildings Latin America 2024

- Fig 3.10: The Market for the Internet of Things in Smart Commercial Buildings Asia Pacific 2024

- Fig 3.11: The Market for the Internet of Things in Smart Commercial Buildings Europe 2024

- Fig 3.12: The Market for the Internet of Things in Smart Commercial Buildings Middle East & Africa 2024

- Fig 4.1: Typical IoT Platform Functionality

- Fig 5.1: The Commercial Smart IoT Platform Ecosystem

- Appendix A - BIoT Platform Comparison Matrix

- Appendix B - M&A & Investments Summary

建筑能源模拟软体市场分析与预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署、最终用户、功能、解决方案

建筑能源模拟软体市场分析与预测(至2035年):类型、产品类型、服务、技术、组件、应用、部署、最终用户、功能、解决方案 2026年全球建筑能源模拟软体市场报告2026年智慧建筑与基础设施人工智慧全球市场报告

2026年全球建筑能源模拟软体市场报告2026年智慧建筑与基础设施人工智慧全球市场报告 2026年智慧建筑领域五大成长机会智慧建筑市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分智慧建筑市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

2026年智慧建筑领域五大成长机会智慧建筑市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、设备、部署类型及最终用户划分智慧建筑市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 智慧建筑新创公司(2026):併购与投资 | 贯穿 AEC/O 生命週期的数位孪生与人工智慧新创公司

智慧建筑新创公司(2026):併购与投资 | 贯穿 AEC/O 生命週期的数位孪生与人工智慧新创公司 智慧建筑市场规模、份额和趋势分析报告:按组件、解决方案、服务、最终用途、地区和细分市场预测(2026-2033 年)

智慧建筑市场规模、份额和趋势分析报告:按组件、解决方案、服务、最终用途、地区和细分市场预测(2026-2033 年) 智慧建筑市场规模、份额和成长分析(按组件、建筑类型、解决方案和地区划分)-2026-2033年产业预测智慧建筑的全球市场 (~2035年):解决方案类型·技术·用途·建筑物类型·功能类型·各地区

智慧建筑市场规模、份额和成长分析(按组件、建筑类型、解决方案和地区划分)-2026-2033年产业预测智慧建筑的全球市场 (~2035年):解决方案类型·技术·用途·建筑物类型·功能类型·各地区