|

市场调查报告书

商品编码

1334504

媒体流媒体市场规模和份额分析 - 增长趋势和预测(2023-2028)Media Streaming Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

流媒体市场规模预计将从2023年的1190.1亿美元增长到2028年的1737.3亿美元,预测期内(2023-2028年)复合年增长率为7.86%。

市场增长的推动因素包括订阅服务需求的增长、本地化和原创内容的增加以及体育直播的普及。这些市场驱动因素正在改变供应商的策略,他们更加註重通过个性化和低成本服务来改善客户体验。

主要亮点

- 通过利用区块链技术和人工智能(AI)等创新来提高媒体质量。剪辑、拍摄、配音、脚本以及视频创作和上传的许多其他方面都得到了人工智能的大力帮助。这些进步预计将对市场扩张产生积极影响。许多采用人工智能的媒体流解决方案供应商正在提高媒体内容质量。如今,这些频道比 YouTube 和 Netflix 等主流媒体更受欢迎。

- 此外,广告和收入模式在这个市场中发挥着重要作用。许多人对流媒体平台上的广告比社交媒体上的广告更关注。例如,全球最大的独立全渠道卖方广告平台 Magnite 今天发布的一份题为《印度进入流媒体时代》的报告显示,流媒体平台上的广告比社交媒体上的广告更受关注。研究发现,近三分之二 (64%) 的印度主播更愿意在流媒体平台上投放广告,其中许多人经常搜索产品 (48%),然后进行购买 (33%)。

- Netflix 最基本的套餐起价为每月 8.99 美元,高清服务起价为 12.99 美元。Amazon Prime 客户只需支付 119 美元即可成为年度会员,或每月支付 12.99 美元。由于价格战以及Apple和Disney等大公司的进入,市场竞争变得更加激烈。

- 此外,智能手机和基于云的服务的快速采用,与传统付费电视相比,OTT 平台渗透率的提高,以及监管直播流媒体的能力,提供对消费者使用模式和合作伙伴关係的洞察,并增加了提供更多本地化内容的人工智能和机器学习正在推动该地区视频流媒体行业的增长。例如,Netflix 拥有 75,000 种不同的内容类型,并通过算法向每个用户提供个性化内容推荐。

- 随着软禁措施的实施,冠状病毒疫情正在对媒体流媒体行业产生积极影响。由于在线流媒体需求增加和消费者转变,供应商见证了整个地区的订户增长和收视率峰值。例如,截至 3 月 31 日的 2020 年第一季度,Netflix 在全球拥有 1580 万订阅用户,是预期 720 万的两倍多,同比增长 22.5%。此外,Netflix 报告称,2020 年 3 月,其移动应用程序的新安装量在意大利增长了 50% 以上,在西班牙增长了 30% 以上。

流媒体市场趋势

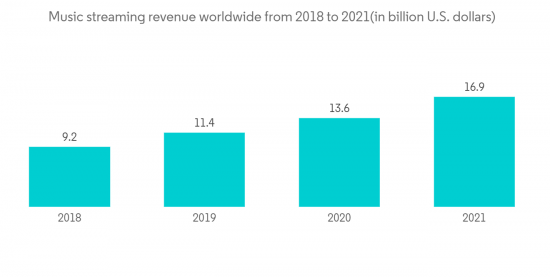

音乐流媒体市场预计将强劲增长

- 通过提供播客和原创内容等独家内容,音乐流媒体提供商首先吸引人们使用他们的平台,并最终将他们转化为订阅者。此外,运营商在不断增长的市场中推出的订阅费降低和捆绑优惠等促销活动预计将进一步促进增长。例如,由于 Spotify Premium Free 3 个月和订阅模式折扣等促销活动的增加,Spotify 的总收入同比增长 31%,总付费订阅份额增长 35%。

- 全球市场最热门的趋势之一是 5G 连接的使用不断增加。Amazon利用这一机会推出了新的音乐高清服务,为美国、英国、德国和日本的音乐爱好者提供无损音乐流媒体和下载。一旦 5G 变得普遍,它将能够以比 4G 快很多倍的速度传输数据,从而使企业能够提供高保真音乐流。虚拟现实 (VR)、增强现实 (AR) 和全息音乐会预计将在直播音乐视频中变得相当普遍。这些新发展正在加速市场扩张。

- 市场上的播放器正在提供新功能,例如精选播放列表、夜间模式和无损音乐,以提高针对性。这样做也是为了随着市场选择数量的不断增加而提高客户保留率。例如,在2021年12月25日至2022年1月31日期间,创建了大约82,000个除夕夜播放列表,并且在除夕夜本身创建了近40,000个播放列表。

- 儘管全球玩家采取了各种策略大力渗透音乐流媒体平台,但由于区域曝光度和区域内容高度集中,区域玩家在各自地区仍然拥有据点。我正在建设它。例如,Gaana 仍然是印度市场的第一大玩家,而 Yandex Music 在俄罗斯市场处于领先地位。同样,Tencent Music Group凭藉其QQ Music、Kugou、Kuwo应用程序在中国市场处于领先地位。

亚太地区实现显着增长

- 对内容製作的投资不断增加,新内容不断被创造。印度正在成为内容中心之一,国内外消费了大量的内容。例如,2020年6月,Tencent宣布为马来西亚视频流媒体平台Iflix提供内容技术和资源,扩大其在东南亚的影响力。

- 北美仍然主导着媒体流媒体市场,但亚太地区正在经历快速增长。Disney和Apple等大公司计划于 2020 年在亚太地区推出平台,利用不断增长的移动使用量和快速改善的高速互联网接入。

- IFPI 2022 年音乐报告《IFPI Music Report 2022, Engaging with Music 2022》是一份关于世界各地人们如何享受和参与音乐的全球报告。该报告由代表全球唱片业的 IFPI 今天发布。该调查基于 22 个国家超过 44,000 人的反馈,是有史以来规模最大的音乐调查。超过 45% 的客户选择付费会员服务,46% 的受访者使用音频流订阅服务。

- 此外,97% 的人使用智能手机听音乐,62% 使用社交媒体网站和应用程序听音乐或观看音乐视频。这表明该地区正在进行的数字媒体转型预计将进一步增长媒体流市场。

流媒体行业概述

由于市场参与者众多且竞争日益激烈,流媒体市场高度分散。为了在市场竞争中获得优势并通过获取更多客户来提高市场地位,供应商正在专注于提供高价值的捆绑包、创新功能以及高质量、原创、本地化的内容。供应商还通过联盟和收购来加强其市场地位。

2022 年 11 月,Paramount和 Virgin Media 宣布了一项新的多年发行协议,将双方的长期合作扩展到Paramount在英国的所有线性频道和流媒体平台。2023 年,新的合作伙伴关係将使 Virgin TV 推出 Paramount+,一项全球订阅视频点播 (SVOD) 服务。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 调查范围

第二章研究方法论

第三章执行摘要

第四章市场洞察

- 市场概况

- 行业吸引力——波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场动态

- 市场动态导论

- 市场驱动力

- 在各种音频流平台上轻鬆访问和自定义播放列表

- 越来越多地采用订阅视频点播 (SVoD) 服务

- 体育赛事直播服务日益普及

- 市场挑战

- 延迟、可靠性和设备兼容性挑战

- 市场机会

- 扩大 360 度视频、AR 和 VR 的采用

- 使用机器学习和人工智能提高内容製作和分发的效率和管理

- 通过广播网络和SVoD平台提供8K内容

- COVID-19 对全球媒体流市场的影响

第六章市场细分

- 按内容类型

- 音乐串流

- 视频流

- 按收入模式

- 广告

- 订阅

- 通过流媒体平台

- 智能手机和平板电脑

- 笔记本电脑和台式机

- 智能电视

- 游戏机

- 按地区

- 北美

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳大利亚

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯联合酋长国

- 沙特阿拉伯

- 南非

- 其他中东和非洲

- 北美

第七章竞争格局:主要供应商概况

- Spotify Technology S.A.

- Apple Inc.

- Amazon Prime(Amazon.com Inc.)

- Tencent Holdings Limited

- Deezer SA

- YouTube(Alphabet Inc.)

- AT&T Inc.

- Pandora Media Inc.

- The Walt Disney Company

- Baidu Inc.

- British Broadcasting Corporation

第八章投资分析

第九章 全球流媒体市场的未来

The Media Streaming Market size is expected to grow from USD 119.01 billion in 2023 to USD 173.73 billion by 2028, at a CAGR of 7.86% during the forecast period (2023-2028).

The growth of the market is fuelled by the growing demand for subscription-based services, increasing availability of region-specific and original content, and the popularity of live sports. These drivers are changing the strategies adopted by the vendors in the market as the emphasis on enhanced customer experience by providing personalization and low-cost services is increasing daily.

Key Highlights

- Media quality is improved by using innovations like blockchain technology and artificial intelligence (AI). Editing, cinematography, voice-overs, scriptwriting, and many other facets of video creation and upload are all greatly aided by AI. It is projected that these advancements will have a favorable impact on the market's expansion. The content quality of media is being improved by a number of suppliers of media streaming solutions employing AI. Recently, these channels have become much more popular than mainstream media outlets like YouTube and Netflix.

- Moreover, the advertising and revenue model plays a crucial role in this market. More people pay attention to ads on streaming platforms than on social media. For instance, In a report titled "India Embraces the Streaming Era," published today by Magnite, the largest independent omnichannel sell-side advertising platform in the world, it was discovered that ads on streaming platforms attract more attention than those on social media. Almost two-thirds of streamers in India (64%) are more receptive to advertising on streaming platforms, with many claiming to frequently do a product search (48%) and make a purchase (33%) after the fact.

- Netflix offers its most basic plan starting at USD 8.99 per month and USD 12.99 for its high-definition service. Amazon Prime customers can get an annual membership for USD 119 or pay USD 12.99 a month. The market is, therefore, getting more competitive with such price wars and more big players entering the market, such as Apple and Disney.

- Furthermore, the rapid adoption of smartphones and cloud-based services, increased penetration of OTT platforms as compared to traditional pay-tv, and incorporation of AI and machine learning to help regulate live streaming and provide insights on consumer usage patterns and partnerships to offer more and region-specific content has increased the growth of video streaming segment across regions. For instance, Netflix has 75,000 different content genres and provides personalized content for individual users through recommendation, which is possible due to the algorithms allowing it to do so.

- The ongoing spread of coronavirus has positively impacted the media streaming industry due to enforced home confinement measures. The vendors were witnessing a spike in the number of subscribers and a peak in viewership across regions due to increased demand for online streaming and changed consumers. For instance, In the first quarter of 2020, ending on March 31, Netflix added 15.8 million subscribers globally, which is more than double the 7.2 million that was expected and a growth of 22.5% year on year. Further, Netflix reported a rise in the quantity of new mobile application installations of more than 50% in Italy and more than 30% in Spain in March 2020.

Media Streaming Market Trends

Music Streaming Segment is Expected to Witness Significant Growth

- Music streaming providers are offering exclusive content with podcasts and original content, which first attracts people towards the platform and eventually turns them as subscribers. Moreover, promotional activities like price cuts in subscriptions in growing markets and bundled offers from telecommunications players are expected to boost the growth further. For instance, Spotify witnessed a YOY growth of 31% of the total revenue and a 35% share of the total paid subscriptions, mainly due to increased promotional activities such as free Spotify premium for three months, price cuts in subscription models, etc.

- One of the most well-liked trends in the global market is the expanding use of 5G connections. Amazon has taken advantage of this chance by launching a new music HD service that will give music lovers in the United States, the United Kingdom, Germany, and Japan access to lossless music streams and downloads. As 5G becomes more commonly used, businesses will be able to provide high-fidelity music streams because of its ability to transport data multiple times quicker than 4G. Virtual Reality (VR), Augmented Reality (AR), and hologram concerts are anticipated to become quite popular for live-streaming music videos. These new developments are accelerating the market's expansion.

- Players in the market are offering new features such as curated playlists, night mode, and lossless music for improved targeting, which is also providing companies with a competitive edge over others, thus making the market competition stronger. This is also done to improve customer retention as the number of options in the market increase continually. For instance, between December 25, 2021, and January 31, 2022, about 82,000 New Year's Eve playlists were made; on New Year's Eve itself, almost 40,000 playlists were made.

- Although global players are strongly penetrating their music streaming platforms by adopting various strategies, regional players still have a stronghold in their respective regions, owing to regional exposure and a high focus on local content. For instance, Gaana continues to be the number 1 player in the Indian market, whereas Yandex Music is leading in Russia. Similarly, Tencent Music Group is one of the leading players in China market because of its apps QQ Music, Kugou, and Kuwo.

Asia Pacific to Witness Significant Growth

- Rising investment in content creation has led to the creation of new content offerings. Increasingly, India is becoming one of the content hubs, with a wealth of material being created for consumption locally and around the world. For instance, In June 2020, Tencent announced the Malaysian video streaming platform Iflix's content technology and resources to grow its presence in Southeast Asia.

- Although North America still dominates the media streaming market, Asia Pacific is showing a rapid increase in the growth rate. Giants such as Disney and Apple Inc. are set to launch their platforms across the Asia Pacific in 2020, leveraging growing mobile usage and rapidly improving access to faster-speed Internet.

- According to IFPI Music Report 2022, Engaging with Music 2022 is a global report on how people all around the world enjoy and engage with music. It was published today by IFPI, which represents the recording business globally. The survey, which is based on responses from more than 44,000 people in 22 countries, is the biggest music study ever conducted. More than 45% of customers choose paid membership services, and 46% of respondents use audio streaming subscription services, which provide continuous and on-demand access to millions of licensed songs.

- Moreover, 97% of the population listens to music using a smartphone; 62% use social media sites or apps to listen to music or watch music videos. This shows the ongoing transformation towards digital media in the region is further expected to grow the market for media streaming.

Media Streaming Industry Overview

The media streaming market is highly fragmented owing to the presence of significant players in the market and growing competitiveness in the market. Vendors in the market are concentrating on providing high-value bundles, innovative features, and High quality, original and region-specific content to gain a competitive advantage and improve their market position by acquiring more customers. Vendors are also adopting partnerships and acquisitions to strengthen their place in the market.

In November 2022, A new multi-year distribution arrangement was announced between Paramount and Virgin Media, extending their long-standing collaboration across all of Paramount's linear channels and streaming platforms in the UK. In 2023, Virgin TV would launch Paramount+, a global subscription video-on-demand (SVOD) service, owing to the partnership's renewal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Introduction to Market Dynamics

- 5.2 Market Drivers

- 5.2.1 Easy Accessibility and Playlist Customization on Various Audio Streaming Platforms

- 5.2.2 Growing Adoption of Subscription Video on Demand (SVoD) Services

- 5.2.3 Increasing Popularity of Live Sports Streaming Services

- 5.3 Market Challenges

- 5.3.1 Challenges Regarding Latency, Reliability, and Device Compatibility

- 5.4 Market Opportunities

- 5.4.1 Increasing Adoption of 360-degree Video, AR, and VR

- 5.4.2 Streamlining and managing Content Production and Distribution by Machine Learning and AI

- 5.4.3 8K Content Offering from Broadcasting Networks and SVoD Platforms

- 5.5 Impact of COVID-19 on Global Media Streaming Market

6 MARKET SEGMENTATION

- 6.1 By Content Type

- 6.1.1 Music Streaming

- 6.1.2 Video Streaming

- 6.2 By Revenue Model

- 6.2.1 Advertising

- 6.2.2 Subscription

- 6.3 By Streaming Platform

- 6.3.1 Smartphone & Tablet

- 6.3.2 Laptop and Desktop

- 6.3.3 Smart TV

- 6.3.4 Gaming Console

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 UK

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.6 UAE

- 6.4.7 Saudi Arabia

- 6.4.8 South Africa

- 6.4.9 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE - KEY VENDOR PROFILES

- 7.1 Spotify Technology S.A.

- 7.2 Apple Inc.

- 7.3 Amazon Prime (Amazon.com Inc.)

- 7.4 Tencent Holdings Limited

- 7.5 Deezer SA

- 7.6 YouTube (Alphabet Inc.)

- 7.7 AT&T Inc.

- 7.8 Pandora Media Inc.

- 7.9 The Walt Disney Company

- 7.10 Baidu Inc.

- 7.11 British Broadcasting Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE GLOBAL MEDIA STREAMING MARKET

企业串流媒体市场:按企业规模、按部署类型、按串流媒体类型、最终用户、按内容类型、按服务类型、按定价模式、收益- 2025-2030 年全球预测

企业串流媒体市场:按企业规模、按部署类型、按串流媒体类型、最终用户、按内容类型、按服务类型、按定价模式、收益- 2025-2030 年全球预测 全球串流媒体设备市场

全球串流媒体设备市场 2024 年串流媒体世界市场报告

2024 年串流媒体世界市场报告 按设备类型(游戏机、媒体串流、智慧电视)、应用程式(电子学习、网路浏览、游戏、即时娱乐、社交网路)、最终用途(商业、住宅)和地区 2024-2032

按设备类型(游戏机、媒体串流、智慧电视)、应用程式(电子学习、网路浏览、游戏、即时娱乐、社交网路)、最终用途(商业、住宅)和地区 2024-2032 2024-2032 年企业串流媒体市场报告(按解决方案、服务、部署、企业规模、应用程式、最终用途和地区)

2024-2032 年企业串流媒体市场报告(按解决方案、服务、部署、企业规模、应用程式、最终用途和地区) 2024年串流媒体设备全球市场报告

2024年串流媒体设备全球市场报告 2024年企业串流媒体全球市场报告

2024年企业串流媒体全球市场报告 串流媒体设备市场报告:2030 年趋势、预测与竞争分析

串流媒体设备市场报告:2030 年趋势、预测与竞争分析 企业流媒体全球市场规模研究与预测:按解决方案、服务、部署、公司规模、应用、最终用途、区域分析,2022-2029 年

企业流媒体全球市场规模研究与预测:按解决方案、服务、部署、公司规模、应用、最终用途、区域分析,2022-2029 年