|

市场调查报告书

商品编码

1403849

模组化资料中心:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Modular Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

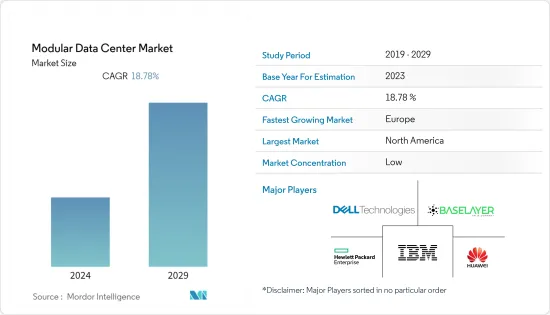

今年模组化资料中心市场规模预计为255.5亿美元。

预计五年内将达到 604.1 亿美元,预测期内复合年增长率为 18.78%。

分解的资料中心解决方案单元可让您轻鬆建置IT基础设施。模组化方法既可以应用于资料中心级别,也可以应用于更通用的级别。

主要亮点

- 随着云端基础的分散式技术变得越来越可用,模组化架构可以支援多种工作负载以满足企业的需求。为了满足对云端、行动和社交分析不断增长的需求,这些可携式资料中心提供了一种有效且经济高效的方法来保护电脑效能,同时节省占地面积。

- 该市场的成长是由对环保资料中心的高需求所推动的。绿色资料中心采用节能管理实务和技术,为企业提供最佳效率和较低的环境影响。由于世界各国政府不断增加的能源消费量和环保要求,模组化资料中心的需求量很大。模组化资料中心最显着的优势之一是比传统资料中心功耗更低、更节能,满足企业减少能源使用的基本需求。

- 在大容量资料中心领域,越来越需要以相对密集的配置快速部署基础设施,并专注于能源和热效率。预计该细分市场的模组成长将比传统方法更为显着。

- 在安装速度和低资本投资方面,模组化资料中心对传统的砖砌资料中心构成了挑战。然而,传统资料中心很可能会继续成为现实,并且可能存在更适合模组化资料中心的应用程式。

- 全球最大的投资者都在关注数位基础设施市场,该市场对资本的需求很高,以推动资料经济。即使在 COVID-19 的情况下,投资者的兴趣仍然很高。随着超大规模运算的发展,资料中心的投资也随之增加。随着对现代、弹性和高度扩充性的资料中心的需求增加,资料中心投资预计将为模组化资料中心的采用创造机会。

模组化资料中心市场趋势

IT产业保持着主要的市场成长

- 提供云端、主机代管和网路託管服务的公司数量不断增加,增加了 IT 公司对模组化资料中心的需求。推动该行业持续成长的关键因素是越来越多的公司继续采用云端处理。

- 主要企业正在透过提供安全、合规的资料中心以及世界一流通讯业者和云端处理服务供应商的正确存取权限,帮助 IT 公司实现混合IT 的成功。我支持。资讯和通讯技术产业正在为模组化和微模组化资料中心提供许多服务,寻求最快的回应。

- 世界各地正在出现趋势,例如出于安全考虑,公司采用模组化资料中心。资讯科技领域的模组化资料中心市场受到对资料储存及其稳健且高效处理的需求不断增长的正面影响。

- 根据中国IT企业的规模,需要私有储存设施和大型资料中心。此外,由于软体服务供应商的激增,云端储存选项随着时间的推移而稳定增加,这使得提供者能够增加容量并创造对资料中心的需求。 SaaS平台即服务(PaaS)和基础设施即服务(IaaS)是中国三大云端处理之一。这增加了对更多资料中心的需求。

北美占据主要市场占有率

- 行动宽频的成长、巨量资料分析和云端处理水准的提高推动了该地区对新资料中心基础设施的需求。北美有许多资料中心,许多公司正在从硬体转向基于软体的服务,使该市场成为资料中心安装的潜在目标。

- 组织正在寻找模组化服务,使他们能够在整合产品组合中选择所需的服务,以优化其基础设施。作为标准化部署的一部分,我们的线上目录中提供了多种服务选项。这些选择为公司提供了降低初始投资的可能性。这种情况的一个很好的例子是 IBM 的整合託管基础架构服务。

- 此外,巨量资料和物联网在该地区的渗透将显着改变下一代模组化资料中心的规模和范围。鑑于现有的竞争,组织需要开发 IT 可扩展性和能力。模组化资料中心由于能够在最短的时间内弹性设置设施以适应资料的指数增长,再加上混合云和第三方资料中心外包,因此正在获得发展势头。

- 此外,物联网的渗透正在推动对边缘资料中心的需求。许多公司正在将物联网用于从零售到医疗保健的广泛应用,并且产生的资料量非常巨大。

模组化资料中心产业概况

模组化资料中心市场分散且竞争激烈。目前,只有少数几家大型企业占据市场主导地位,而这些市场份额突出的大型企业正专注于扩大海外基本客群。此外,新的参与者正在透过应对激烈竞争的策略合作措施进入这个市场。主要参与者有IBM公司、华为技术公司等。

2023 年 2 月,Vertiv Co. 推出了 Vertiv MegaMod 和 Vertiv MegaMod Plus承包预製模组化 (PFM)资料中心解决方案。高品质的预製模组与 Vertiv 业界领先的电源管理系统、温度控管解决方案、远端监控和 IT 设备机架进行整合和测试,与传统资料中心建置相比,可提供卓越的效能和效能,最多可缩短40 的部署时间%。该解决方案目前已在欧洲、中东和非洲 (EMEA) 地区推出。

2022 年 9 月,Vertiv 在印度推出 Vertiv 预製资料中心,提供模组化资料中心和基础设施选项。此整合解决方案可根据您的 IT 资产部署进行定制,并提供快速安装容量的简单方法。它还提供简单的可扩展性,使资料中心营运商能够从满足其即时需求的解决方案开始,并根据需要进行扩展。 Vertiv 针对预製模组化资料中心采用了关键的电源和热管理功能以及监控技术。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究成果和先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 模组化资料中心的移动性和扩充性

- 灾难復原的优点

- 市场挑战

- 资料中心面临能源效率和永续性挑战。

第六章市场区隔

- 解决方案和服务

- 功能模组解决方案(单一功能模组和一体化功能模组)

- 服务

- 目的

- 灾难备份

- 高效能/边缘运算

- 资料中心扩建

- 启动资料中心

- 最终用户

- IT

- 电信

- BFSI

- 政府机关

- 其他最终用户(医疗保健、零售、国防等)

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- IBM Corporation

- Huawei Technologies Co. Ltd.

- Dell EMC

- HPE Company

- Baselayer Technology LLC

- Vertiv Co.

- Schneider Electric SE

- Cannon Technologies Ltd

- Rittal Gmbh & Co. KG

- Instant Data Centers LLC

- Colt Group SA

- Bladeroom Group Ltd.

第八章投资分析

第九章 市场机会及未来趋势

The Modular Data Center Market size was estimated at USD 25.55 billion in the current year. The market is expected to reach USD 60.41 billion in five years, registering a CAGR of 18.78% during the forecast period.

Disaggregated data center solution units facilitate the building of the IT infrastructure. A modular approach can be applied at the level of data centers or a more general level.

Key Highlights

- Modular architecture can support more than one workload to meet the needs of businesses as organizations continue to use cloud-based dispersed technologies. To meet the growing demand for cloud, mobile, and social analytics, these transportable data centers offer an effective, cost-efficient way of protecting computer performance while leaving no more floor space.

- This market's growth is driven by the high demand for environmentally friendly data centers. Green data centers use energy-efficient management methods and technology, providing enterprises with little environmental impact and optimum efficiency. Modular data centers are highly requested because of increased energy consumption and environmental protection requirements laid down by governments worldwide. One of the most significant advantages of modular data centers is that, compared to traditional data centers, they consume less power and are more energy-efficient, allowing them to meet companies' intrinsic requirements for lower energy usage.

- In the high-volume data center segment, there is a clear need for rapid infrastructure deployment in comparatively very dense configurations with an emphasis on energy and heat efficiency. We will likely see a much more significant module growth in this segment than conventional approaches.

- Regarding installation speeds and low capex, Modular Data Centres represent a challenge to traditional brick-and-mortar data centers. But, traditional data centers are likely to remain a reality, and some applications may be more suitable for modular data centers.

- The largest global investors are focusing on the market for digital infrastructure, with the extraordinary demand for capital to boost the data economy. The interest of investors remains high even during the COVID-19 situation. The investments in data centers increased after the growth of hyperscale computing. As the demand for modern, flexible, and scalable data centers increases, investments in data centers are expected to create opportunities to adopt modular data centers.

Modular Data Center Market Trends

IT Sector to Hold Significant Market Growth

- Due to the growing number of companies that provide cloud, colocation, and Web hosting services, demand from IT firms for modular data centers is increasing. The significant factor driving the continued growth of this segment is an ever growing number of enterprises adopting cloud computing.

- By providing secure and compliant data centers with adequate access to the world's top telecommunications operators and cloud computing services providers, studied market players help IT companies achieve hybrid IT success. The information and communications technology industry seeks the fastest possible response time and provides services for Modular and micromodular data centers with much to offer.

- A trend is emerging worldwide, such as enterprises adopting modular data centers due to security concerns. The Modular Data Centre Market in the Information Technology sector has been positively influenced by an increasing demand for data storage and its robust and efficient processing.

- Based on the size of Chinese IT companies, private storage facilities and large-scale data centers are required. Furthermore, cloud storage selection has steadily increased over time due to the growing number of Software Service Providers, enabling them to improve their capacity and create demand for data centers. SaaS platform as a service (PaaS) and infrastructure as a service (IaaS) are among China's three major cloud computing categories. This fuels the demand for more data centers.

North America accounts for the Significant Market Share

- The demand for new data center infrastructure in this region is triggered by the growth of Mobile Broadband, increased levels of Big Data Analytics, and cloud computing. Many data centers are present in North America, with many companies switching from hardware to software-based services, and it is estimated that this market will be a potential target for data center installation.

- Organizations are looking for modular services that allow them to select the desired service in an integrated portfolio to optimize infrastructure. Several service options are available from the online catalogs as part of a standardized deployment. These options offer the possibility of lowering an initial investment for companies. An excellent example of this situation is the IBM Integrated Managed Infrastructure Service.

- Moreover, the size and scope of next-generation modular data centers will significantly change due to the penetration of Big Data and the Internet of Things in this region. Given the existing competition, IT scalability and capacity need to be developed by organizations. Modular data centers are gaining momentum, given their flexibility to install a facility in the least time due to an exponential growth of data, coupled with hybrid cloud and outsourcing third-party data centers.

- Additionally, the increasing penetration of IoT is driving the demand for edge data centers. Many companies are taking advantage of IoT for applications ranging from retail to healthcare, and the amount of data generated is enormous.

Modular Data Center Industry Overview

The modular data center market is fragmented, where competition tends to increase and consists of several major players. Few of the major players currently dominate the market, and these major players with a prominent share in the market are focusing on expanding their customer base across foreign countries. Further, new players enter this market through strategic collaborative initiatives catering to intense rivalry. Key players are IBM Corporation, Huawei Technologies Co. Ltd, etc.

In February 2023, Vertiv Co. introduced the Vertiv MegaMod and Vertiv MegaMod Plus, a turnkey prefabricated modular (PFM) data center solution, deployable in expandable units of 0.5 or 1 megawatts for IT loads up to 2 megawatts or more. The high-quality prefabricated modules are integrated and tested with industry-leading Vertiv power management systems, thermal management solutions, remote monitoring, and IT equipment racks to deliver exceptional performance and help companies reduce deployment time by up to 40% compared to a traditional data center build. The solutions are now available across Europe, the Middle East and Africa (EMEA).

In September 2022, Vertiv offered modular data centers and infrastructure options by introducing Vertiv Prefab Data Centres in India. Integrated solutions can be adapted to IT asset deployment and provide a simple way to install capacity quickly. Simple scalability is also offered, enabling the data center operator to start with a solution that meets Immediate needs and then scale up as needed. Vertiv uses its prefabricated modular data centers' key power and temperature management capabilities and monitoring and control technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables & Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Mobility and Scalability of Modular Data Centers

- 5.1.2 Disaster Recovery Advantages

- 5.2 Market Challenges

- 5.2.1 Data Centers Facing Power Efficiency and Sustainability Issues along with Power and cooling

6 MARKET SEGMENTATION

- 6.1 Solution and Services

- 6.1.1 Function Module Solution (Individual Function Module and All-in-One Function Module)

- 6.1.2 Services

- 6.2 Application

- 6.2.1 Disaster Backup

- 6.2.2 High Performance/ Edge Computing

- 6.2.3 Data Center Expansion

- 6.2.4 Starter Data Centers

- 6.3 End User

- 6.3.1 IT

- 6.3.2 Telecom

- 6.3.3 BFSI

- 6.3.4 Government

- 6.3.5 Other End Users (Healthcare, Retail, Defense, etc.)

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Huawei Technologies Co. Ltd.

- 7.1.3 Dell EMC

- 7.1.4 HPE Company

- 7.1.5 Baselayer Technology LLC

- 7.1.6 Vertiv Co.

- 7.1.7 Schneider Electric SE

- 7.1.8 Cannon Technologies Ltd

- 7.1.9 Rittal Gmbh & Co. KG

- 7.1.10 Instant Data Centers LLC

- 7.1.11 Colt Group SA

- 7.1.12 Bladeroom Group Ltd.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

模组化资料中心市场:按组件、资料中心规模、层级类型、应用、产业划分 - 2025-2030 年全球预测

模组化资料中心市场:按组件、资料中心规模、层级类型、应用、产业划分 - 2025-2030 年全球预测 全球模组化资料中心市场:按解决方案、外形规格、架构类型 - 预测(~2030 年)

全球模组化资料中心市场:按解决方案、外形规格、架构类型 - 预测(~2030 年) 模组化资料中心的全球市场,2024-2028

模组化资料中心的全球市场,2024-2028 模组化资料中心市场规模、份额和成长分析:按组成部分、组织规模、行业和地区 - 行业预测,2024-2031 年

模组化资料中心市场规模、份额和成长分析:按组成部分、组织规模、行业和地区 - 行业预测,2024-2031 年 模组化资料中心市场、机会、成长动力、产业趋势分析与预测,2024-2032

模组化资料中心市场、机会、成长动力、产业趋势分析与预测,2024-2032 2024-2032 年模组化资料中心市场报告(按组件、资料中心规模、应用、垂直行业和地区)

2024-2032 年模组化资料中心市场报告(按组件、资料中心规模、应用、垂直行业和地区) 模组型资料中心市场规模,占有率,预测,趋势分析:各提供,各组织规模,各终端用户,各地区-2031年前的世界预测

模组型资料中心市场规模,占有率,预测,趋势分析:各提供,各组织规模,各终端用户,各地区-2031年前的世界预测 全球模组化资料中心市场:展望与预测(2023-2028)

全球模组化资料中心市场:展望与预测(2023-2028) 全球预製模组化资料中心市场:2024年至2029年预测

全球预製模组化资料中心市场:2024年至2029年预测 模组化资料中心市场-2024年至2029年预测

模组化资料中心市场-2024年至2029年预测