|

市场调查报告书

商品编码

1850046

汽车网路安全:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Cybersecurity For Cars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

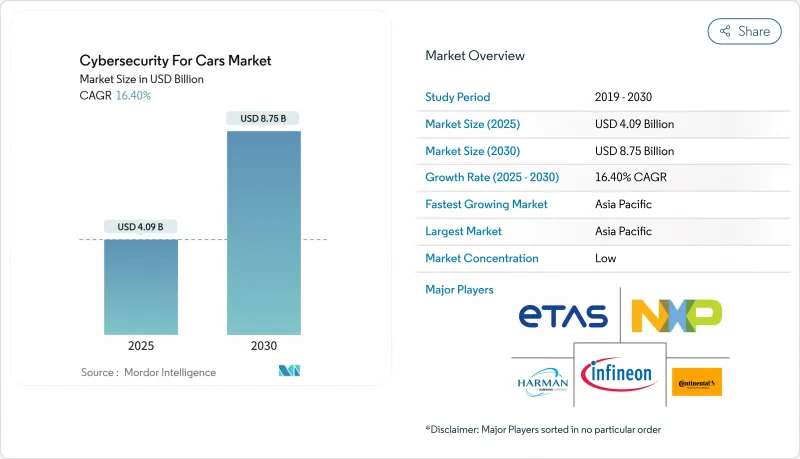

据估计,汽车网路安全市场规模将在 2025 年达到 40.9 亿美元,到 2030 年达到 87.5 亿美元,在预测期(2025-2030 年)内复合年增长率将达到 16.40%。

汽车的快速数位化、日益严格的监管审查以及5G/V2X技术的广泛部署正在重塑竞争策略,并开闢新的服务主导收入来源。製造商正竞相在UNECE R155/R156审核前完成网路安全管理系统的认证,而随着软体定义车辆对持续保护的需求不断增长,云端原生安全平台也日益受到青睐。同时,电动车的普及、双向充电以及配备丰富感测器的ADAS功能的出现,正在扩大攻击面,吸引那些承诺提供即时威胁情报和自动化回应的专业解决方案供应商。原始设备製造商(OEM)也在寻求透过空中下载安全更新和基于使用量的保险计划来实现盈利,这些计划奖励经过认证的网路安全加固措施,从而部分抵消高昂的整合成本。

全球汽车网路安全市场趋势与洞察

更严格的监管将推动根本变革。

全球认证的关键在于证明端到端的安全性。光是联合国欧洲经济委员会R155一项标准,到2030年就将创造21亿美元的合规机会,因为原始设备製造商(OEM)必须证明他们能够追踪69种攻击途径,并在车辆的整个生命週期内持续监控这些途径。 ISO/SAE 21434标准将网路安全工程硬性纳入概念设计和退役阶段,促使汽车製造商扩充其专业团队。类似的规则正在日本和美国涌现,从而消除先发劣势,并建立全球标准化的基准。

联网汽车的兴起扩大了攻击面

现代车辆最多可搭载 150 个电子控制单元 (ECU) 和 1 亿行代码,到 2030 年这一数字可能会增长三倍,这将给传统防御系统带来巨大压力。后端伺服器已占安全事件的 43%,95% 的攻击源自远端。基于 5G 的车联网 (V2X) 通讯增加了一个高频宽的攻击途径,揭露了远端资讯处理网关,而针对经销商 IT 系统的勒索软体攻击则凸显了车辆边界之外的供应链漏洞。

传统架构整合成本阻碍了其广泛应用。

在传统平台上改装超过150个ECU可能会使车辆开发预算增加15%至20%。大陆集团2022年的违规行为暴露了其供应商网络,并迫使其进行代价高昂的架构改造。这种财务拖累会减缓大众市场品牌的上市速度,即便合规期限将近。

细分市场分析

到了2024年,以软体为基础的平台将占总收入的41.2%,凸显其在软体定义汽车时代的核心地位。在这个时代,嵌入式防火墙、安全韧体和运行时入侵侦测正在融合。同时,差距分析、威胁建模、审核准备等工作外包给专家顾问,主导服务预计将以19.8%的复合年增长率成长。汽车网路安全市场越来越青睐那些能够将持续监控与UNECE R155文件支援结合的供应商,例如哈曼的端对端WP.29软体套件。

当硬体安全模组、PKI 套件和云端 SOC 平台必须在紧迫的开发时间内实现互通时,专业服务还能协调多供应商整合。这种跨学科的协调使服务提供者成为合规蓝图的关键安全隔离网闸,并将收入转向定期评估和託管检测合约。因此,汽车网路安全市场正在出现包含服务保留条款的合作关係,以帮助软体授权人确保终身利润。

到2024年,端点防御仍将维持30.1%的市场份额,因为加密金钥、安全启动和ECU级防火墙仍然是基础。然而,随着汽车製造商将资料湖、OTA编配和车队分析等功能迁移到云端,云端防御将以21.3%的复合年增长率领先。在Upstream与Google云端等合作专案的推动下,云端保护在汽车网路安全市场的规模正逐季成长。 2024年大众汽车资料外洩事件的教训表明,遥测资料加密不足会导致连锁声誉损害。

网路层分段和TLS v1.3升级与云端运算的快速发展相辅相成,而随着汽车每週下载微服务,以应用为中心的安全加固变得至关重要。无线安全是保护5G链路的最后一公里,这些链路支撑着车队编组和V2I信令通讯。随着虚拟ECU将任务卸载到边缘,结合车载安全措施和远端AI辅助分析的混合架构正在为汽车网路安全市场建立新的蓝图。

汽车网路安全市场按解决方案类型(软体解决方案、硬体解决方案及其他)、安全类型(网路安全、应用安全及其他)、车辆类型(乘用车、轻型商用车及其他)、应用领域(资讯娱乐、远端资讯处理、连网互通及其他)、模式(车载模式、外部云端服务)和地区进行细分。市场预测以美元计价。

区域分析

预计到2024年,亚太地区汽车网路安全市场营收将成长35.6%,复合年增长率达20.2%,成为该市场成长最快的地区。中国互联电动车产量的扩张正在推动对支援V2G功能的PKI和ECU加固套件的大规模采购。韩国的5G网路建设推动了对即时空中修补技术的需求,而印度新兴的出口雄心则推动了对ISO 21434合规工具的投资。这些趋势正促使该地区的供应商提供託管在资料居住合规区域内的低延迟云端SOC服务。

北美是一个日趋成熟但仍在不断发展的市场,高端汽车和健全的保险生态系统正在推动网路安全的商业化。美国的连网汽车法规将于2025年3月生效,这将迫使汽车製造商对其供应链进行审核,确保零件符合规定,并转向采购国产晶片组和安全模组。加拿大的一级供应商正利用其接近性和监管一致性来整合安全的乙太网路骨干网,而墨西哥的组装厂则正在采用託管安全服务来应对针对即时物流的勒索软体攻击。

欧洲仍然是监管趋势的领导者和研发中心。德国拥有博世ETAS和大陆集团等主要供应商,后者先前曾遭遇安全漏洞,凸显了其集中式架构的脆弱性。法国和英国正将公共津贴用于量子安全汽车密码技术,而ENX VCS审核框架则以ISO 21434为基础,实现了供应商评估的标准化。东欧的工程中心为企业提供了具有竞争力的人才,但与战争相关的网路制裁正在重塑筹资策略。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 监管要求(UNECE R155/R156、ISO 21434)合规性浪潮

- 联网汽车快速成长及5G/V2X部署

- ADAS/自动驾驶功能的普及增加了网路风险

- 车网互动(V2G)充电创造了一个新的攻击面

- 与认证网路安全加固措施一致的基于使用量的保险折扣

- 软体定义汽车中 OTA 安全更新的 OEM 获利模式

- 市场限制

- 高昂的整合成本和传统的电子电气架构

- 标准碎片化和认证超负荷

- 汽车业网路安全人才严重短缺

- 对长寿命车辆保固期后责任的担忧

- 产业价值链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 影响市场的宏观经济因素

第五章 市场规模与成长预测

- 按解决方案类型

- 基于软体

- 基于硬体

- 专业服务

- 一体化

- 其他解决方案

- 按安全类型

- 网路安全

- 应用程式安全

- 云端安全

- 端点安全

- 无线安全

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 大型商用车辆

- 电动车(纯电动车/油电混合车/插电式油电混合车)

- 透过使用

- 资讯娱乐

- 车载资讯系统和连接

- 动力传动系统/推进控制

- ADAS及安全性

- 充电基础设施和V2G

- 依表单类型

- 车载(嵌入式)

- 外部云端服务

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 新加坡

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Continental AG

- Harman International(Samsung)

- Bosch ETAS GmbH

- Infineon Technologies AG

- NXP Semiconductors NV

- Cisco Systems Inc.

- DENSO Corporation

- Visteon Corporation

- Delphi Technologies plc

- Honeywell International Inc.

- Argus Cyber Security Ltd.

- Karamba Security Ltd.

- Arilou Technologies Ltd.

- Escrypt GmbH

- Secunet Security Networks AG

- Upstream Security Ltd.

- VicOne Inc.(Trend Micro)

- GuardKnox Cyber-Technologies Ltd.

- BlackBerry QNX

- SafeRide Technologies Ltd.

- Cybellum Technologies Ltd.

- Trillium Secure Inc.

- Vector Informatik GmbH

- Comsec Automotive Ltd.

- GuardSquare NV

- AutoCrypt Co. Ltd.

第七章 市场机会与未来趋势

The Cybersecurity For Cars Market size is estimated at USD 4.09 billion in 2025, and is expected to reach USD 8.75 billion by 2030, at a CAGR of 16.40% during the forecast period (2025-2030).

Rapid vehicle digitalization, growing regulatory scrutiny, and wider 5G/V2X roll-outs are reshaping competitive strategies and opening new service-led revenue pools. Manufacturers race to certify Cybersecurity Management Systems before UNECE R155/R156 audits, while cloud-native security platforms gain traction as software-defined vehicles demand continuous protection. Simultaneously, electric-vehicle adoption, bidirectional charging, and sensor-rich ADAS features multiply the attack surface, attracting specialized solution vendors that promise real-time threat intelligence and automated response. OEMs also eye monetization of over-the-air security updates and usage-based insurance programs that reward certified cyber-hardening, partially offsetting high integration costs.

Global Cybersecurity For Cars Market Trends and Insights

Regulatory mandates drive fundamental change

Global homologation now hinges on demonstrating end-to-end security. UNECE R155 alone creates a USD 2.1 billion compliance opportunity by 2030 as OEMs must track 69 attack vectors and prove continuous monitoring throughout vehicle lifecycles. ISO/SAE 21434 hardcodes cybersecurity engineering into concept and decommission phases, prompting carmakers to expand specialist teams. Similar rules emerge in Japan and the United States, eliminating first-mover disadvantages and standardizing baselines worldwide.

Connected-vehicle fleet expansion multiplies attack surfaces

Modern cars host up to 150 ECUs and 100 million lines of code-volumes that could triple by 2030, stressing legacy defenses. Backend servers already account for 43% of incidents, and 95% of attacks originate remotely. 5G-based V2X exchanges add high-bandwidth vectors exposing telematics gateways, while ransomware targeting dealership IT highlights supply-chain vulnerabilities beyond the vehicle perimeter.

Legacy architecture integration costs constrain adoption

Retrofitting 150-plus ECUs in legacy platforms can add 15-20% to vehicle development budgets. Continental's 2022 breach illustrated supplier-network exposure and forced expensive architecture reviews. Such financial drag delays roll-outs among volume brands, even as compliance deadlines loom.

Other drivers and restraints analyzed in the detailed report include:

- ADAS proliferation elevates safety-critical risks

- Vehicle-to-Grid integration creates bidirectional pathways

- Automotive cybersecurity talent shortage limits execution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software-based platforms held 41.2% of 2024 revenue, underscoring their centrality in a software-defined vehicle era where embedded firewalls, secure firmware, and runtime intrusion detection converge. Consulting-led offerings, however, are on a 19.8% CAGR ascent as OEMs outsource gap analyses, threat modeling, and audit preparation to specialist advisors. The cybersecurity for cars market increasingly rewards vendors capable of bundling continuous monitoring with UNECE R155 documentation support, a capability visible in HARMAN's end-to-end WP.29 packages.

Professional services also orchestrate multi-vendor integration when hardware security modules, PKI suites, and cloud SOC platforms must interoperate inside tight development timelines. Such cross-domain coordination positions service providers as primary gatekeepers of compliance roadmaps, shifting revenue toward recurring assessment and managed-detection contracts. Consequently, the cybersecurity for cars market is witnessing alliances where software licensors embed service retainer clauses to secure lifetime margins.

Endpoint controls retained a 30.1% share in 2024 because cryptographic keys, secure boot, and ECU-level firewalls remain foundational. Yet cloud defenses are racing ahead at 21.3% CAGR as automakers shift data lakes, OTA orchestration, and fleet analytics off-board. The cybersecurity for cars market size for cloud protection is swelling each quarter, buoyed by collaborations such as Upstream's tie-up with Google Cloud. Incident lessons from the 2024 Volkswagen data breach showed that insufficient encryption of telemetry can cascade into reputational damage.

Network-layer segmentation and TLS v1.3 upgrades ride parallel with cloud growth, while application-centric hardening becomes imperative as vehicles download microservices weekly. Wireless security remains the final mile, guarding 5G links that now underpin platooning and V2I signalling. As virtual ECUs offload tasks to the edge, hybrid architectures combining in-vehicle enforcement with remote AI-assisted analytics form the emerging blueprint across the cybersecurity for cars market.

Cybersecurity for Cars Market is Segmented by Solution Type (Software-Based, Hardware-Based, and More), Security Type (Network Security, Application Security, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Infotainment, Telematics and Connectivity, and More), Form Type (In-Vehicle and External Cloud Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 35.6% revenue in 2024 and is projected to grow at 20.2% CAGR, making it the fastest-advancing geography within the cybersecurity for cars market. China's scaling of connected-EV production fuels large-scale procurement of V2G-ready PKI and ECU hardening suites, while Japan's early alignment with UNECE rules accelerates supplier certification programs. South Korea's 5G highways amplify demand for real-time over-the-air patching technologies, and India's emergent export ambitions trigger investments in ISO 21434 compliance tooling. Collectively, these dynamics push regional vendors to deliver low-latency cloud SOC services hosted within data-residency-compliant zones.

North America represents a mature yet evolving arena where premium vehicle trims and robust insurance ecosystems encourage cybersecurity monetization. The United States Connected Vehicles Rule, effective March 2025, forces OEMs to audit supply chains for sanctioned components, redirecting procurement toward domestic chipsets and security modules. Canada's tier-one suppliers leverage proximity and regulatory alignment to integrate secure Ethernet backbones, while Mexico's assembly plants adopt managed-security services to counter rising ransomware aimed at just-in-time logistics.

Europe remains a regulatory trendsetter and R&D hub. Germany hosts flagship suppliers such as Bosch ETAS and Continental, although the latter's prior breach highlighted vulnerabilities in centralized architecture. France and the United Kingdom channel public grants into quantum-safe automotive cryptography, while the ENX VCS audit framework overlays ISO 21434 to standardize supplier assessments. Eastern European engineering hubs contribute competitive talent, though war-related cyber sanctions reshape sourcing strategies.

- Continental AG

- Harman International (Samsung)

- Bosch ETAS GmbH

- Infineon Technologies AG

- NXP Semiconductors NV

- Cisco Systems Inc.

- DENSO Corporation

- Visteon Corporation

- Delphi Technologies plc

- Honeywell International Inc.

- Argus Cyber Security Ltd.

- Karamba Security Ltd.

- Arilou Technologies Ltd.

- Escrypt GmbH

- Secunet Security Networks AG

- Upstream Security Ltd.

- VicOne Inc. (Trend Micro)

- GuardKnox Cyber-Technologies Ltd.

- BlackBerry QNX

- SafeRide Technologies Ltd.

- Cybellum Technologies Ltd.

- Trillium Secure Inc.

- Vector Informatik GmbH

- Comsec Automotive Ltd.

- GuardSquare NV

- AutoCrypt Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory mandates (UNECE R155/R156, ISO 21434) compliance wave

- 4.2.2 Rapid growth in connected-vehicle fleet and 5G/V2X roll-outs

- 4.2.3 ADAS/autonomous feature proliferation elevating cyber-risk

- 4.2.4 Vehicle-to-Grid (V2G) bidirectional charging introduces new attack surface

- 4.2.5 Usage-based-insurance discounts tied to certified cyber-hardening

- 4.2.6 OEM monetisation of OTA security updates in software-defined cars

- 4.3 Market Restraints

- 4.3.1 High integration cost and legacy E/E architectures

- 4.3.2 Fragmented standards and certification overload

- 4.3.3 Acute shortage of automotive-grade cyber-talent

- 4.3.4 Post-warranty liability concerns for long-life vehicles

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Solution Type

- 5.1.1 Software-Based

- 5.1.2 Hardware-Based

- 5.1.3 Professional Services

- 5.1.4 Integration

- 5.1.5 Other Solutions

- 5.2 By Security Type

- 5.2.1 Network Security

- 5.2.2 Application Security

- 5.2.3 Cloud Security

- 5.2.4 Endpoint Security

- 5.2.5 Wireless Security

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Electric Vehicles (BEV/HEV/PHEV)

- 5.4 By Application

- 5.4.1 Infotainment

- 5.4.2 Telematics and Connectivity

- 5.4.3 Powertrain/Propulsion Control

- 5.4.4 ADAS and Safety

- 5.4.5 Charging Infrastructure and V2G

- 5.5 By Form Type

- 5.5.1 In-Vehicle (Embedded)

- 5.5.2 External Cloud Services

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Malaysia

- 5.6.4.6 Singapore

- 5.6.4.7 Australia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 Harman International (Samsung)

- 6.4.3 Bosch ETAS GmbH

- 6.4.4 Infineon Technologies AG

- 6.4.5 NXP Semiconductors NV

- 6.4.6 Cisco Systems Inc.

- 6.4.7 DENSO Corporation

- 6.4.8 Visteon Corporation

- 6.4.9 Delphi Technologies plc

- 6.4.10 Honeywell International Inc.

- 6.4.11 Argus Cyber Security Ltd.

- 6.4.12 Karamba Security Ltd.

- 6.4.13 Arilou Technologies Ltd.

- 6.4.14 Escrypt GmbH

- 6.4.15 Secunet Security Networks AG

- 6.4.16 Upstream Security Ltd.

- 6.4.17 VicOne Inc. (Trend Micro)

- 6.4.18 GuardKnox Cyber-Technologies Ltd.

- 6.4.19 BlackBerry QNX

- 6.4.20 SafeRide Technologies Ltd.

- 6.4.21 Cybellum Technologies Ltd.

- 6.4.22 Trillium Secure Inc.

- 6.4.23 Vector Informatik GmbH

- 6.4.24 Comsec Automotive Ltd.

- 6.4.25 GuardSquare NV

- 6.4.26 AutoCrypt Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment

汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测

汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测 联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测

联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测 汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分人工智慧在汽车网路安全领域的市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分人工智慧在汽车网路安全领域的市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 汽车网路安全市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、安全类型、应用类型、地区和竞争格局划分,2021-2031年

汽车网路安全市场-全球产业规模、份额、趋势、机会和预测:按车辆类型、安全类型、应用类型、地区和竞争格局划分,2021-2031年 全球汽车网路安全解决方案市场:未来预测(至 2032 年)—按安全类型、产品/服务、车辆类型、应用和区域分類的分析

全球汽车网路安全解决方案市场:未来预测(至 2032 年)—按安全类型、产品/服务、车辆类型、应用和区域分類的分析 日本汽车网路安全市场报告(按安全类型、形式、车辆类型、应用和地区划分,2026-2034 年)

日本汽车网路安全市场报告(按安全类型、形式、车辆类型、应用和地区划分,2026-2034 年) 汽车网路安全市场规模、份额和成长分析(按组件、应用、模式、安全类型、方法、车辆类型、动力类型和地区划分)—产业预测,2026-2033年汽车网路安全市场预测至2032年:按安全类型、解决方案、车辆类型、外形规格、应用和地区分類的全球分析

汽车网路安全市场规模、份额和成长分析(按组件、应用、模式、安全类型、方法、车辆类型、动力类型和地区划分)—产业预测,2026-2033年汽车网路安全市场预测至2032年:按安全类型、解决方案、车辆类型、外形规格、应用和地区分類的全球分析 全球联网汽车安全市场按应用、电动车类型、配置、安全类型、解决方案类型和地区划分-预测至2032年

全球联网汽车安全市场按应用、电动车类型、配置、安全类型、解决方案类型和地区划分-预测至2032年