|

市场调查报告书

商品编码

1403978

天然纤维增强复合材料:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Natural Fiber Reinforced Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

天然纤维增强复合材料市场预计将从2024年的4,081.05千吨成长到2029年的6,104.85千吨,预测期内复合年增长率为8.39%。

主要亮点

- 从中期来看,生物基复合材料需求的增加以及电子产业对环保复合材料需求的增加等因素将推动天然纤维增强复合材料市场的发展。

- 然而,吸湿性、有限的加工温度、与大多数聚合物基体的不相容性以及与玻璃纤维增强复合材料相比较低的抗衝击性可能是市场的抑制因素。

- 然而,天然纤维增强聚合物复合材料的阻燃性能有望为市场带来新的机会。

- 亚太地区在市场中占据主导地位,并且可能在预测期内实现最高的复合年增长率。这一增长归因于建筑业支出的迅速增加。

天然纤维增强复合材料市场趋势

建筑业的需求增加

- 建材业始终需要环保材料。基于天然纤维增强聚合物的复合材料由于其许多优点而越来越多地用于土木工程和建筑应用。

- 复合材料在建设产业中发挥着至关重要的作用。工业柱、储槽、大跨距屋顶结构、储槽、高层建筑、轻质门、窗、家具、轻质建筑、桥樑构件、成套桥樑系统均采用复合材料。作为实现长期永续性的手段,复合材料在建设产业中变得越来越重要。

- 近年来,建筑业得到了大量投资。根据牛津经济研究院预测,2020 年至 2030 年间,全球建筑业预计将成长 4.5 兆美元(42%),达到 15.2 兆美元。此外,2020年至2030年,中国、印度、美国和印尼预计将占全球建设业成长的58.3%。

- 在北美,美国在建设产业中占有很大份额。除美国外,加拿大和墨西哥也是建筑业投资的主要贡献者。美国人口普查局资料显示,2022年美国公共住宅年金额为91.5亿美元,较2017年的67.4亿美元成长35.7%。

- 同样,由于欧盟復苏基金的新投资,2022 年欧洲建筑业成长了 2.5%。儘管大多数欧盟建设公司面临价格压力,但景气预计将在 2022 年初恢復并达到 COVID-19 之前的水平。此外,随着 COVID-19 危机的缓解,建筑商将不愿意投资新建筑或维修现有房产。

- 因此,预计上述趋势将在预测期内影响建筑领域天然纤维增强复合材料的成长。

亚太地区主导市场

- 预计亚太地区将主导全球市场。中国、印度和日本等国家建设活动的增加正在增加该地区天然纤维增强复合材料的使用。

- 建筑业是中国经济持续发展的主要动力。根据中国国家统计局的数据,建筑业产值将从2021年的29.3兆元(4.2兆美元)增加至2022年的31.2兆元(4.5兆美元)。预计到 2030 年,中国将在建筑方面花费近 13 兆美元,这使得天然纤维增强复合材料的前景一片光明。

- 据住宅及城乡建设部预计,2025年,中国建筑业占GDP的比重预计将维持在6%。根据这项预测,中国政府于 2022 年 1 月宣布了一项五年计划,重点是使建筑业更加永续和以品质主导。

- 同样,天然纤维增强复合材料在电子产业的应用迅速增加也可能支持该国的工业成长。根据印度品牌股权基金会(IBEF)预测,到2025年,印度电子製造业的产值预计将达到5,200亿美元。

- 此外,汽车是天然纤维增强复合材料的主要消费者之一。印度汽车工业在技术进步和宏观经济扩张中发挥关键作用,使其成为印度经济表现的重要指标。

- 此外,印度政府也宣布加快(混合和)电动车的采用和製造,目标是到 2030 年实现 30%的电动车(EV)普及。透过我们的计划,我们正在创造动力来鼓励和一些地区强制要求,采用电动车。该计划将为电动车创造需求奖励,并支持在城市中心部署充电技术和充电站。政府设定的目标是,2030年,印度销售的70%商用车、30%私家车、40%公车以及80%两轮和三轮车为电动车。

- 因此,预计各国政府的新政策和投资将在预测期内提振亚太地区其他天然纤维增强复合材料市场的需求。

天然纤维增强复合材料产业概况

天然纤维增强复合材料市场分散,没有一家公司占据重要的市场占有率。市场主要企业(排名不分先后)包括 Trex Company Inc.、Fiberon Technologies Inc.、UPM-Kymmene Oyj、The AZEK Company、Oldcastle APG 等。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 对生物基复合材料的需求增加

- 全球汽车工业的成长

- 抑制因素

- 吸湿性、加工温度限制、与大多数聚合物基质的不相容性

- 由于暴露于外部环境而导致的劣化问题

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(基于数量的市场规模)

- 纤维

- 木纤维复合材料

- 非木纤维复合材料

- 棉布

- 亚麻

- 红麻

- 麻

- 其他非木纤维复合材料

- 聚合物

- 热固性树脂

- 热塑性塑料

- 聚乙烯

- 聚丙烯

- PVC

- 其他热塑性塑料

- 最终用户产业

- 航太

- 车

- 建筑/施工

- 电力/电子

- 运动的

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率排名分析

- 主要企业策略

- 公司简介

- Amorim Cork Composites SA

- Fiberon Technologies Inc.

- FlexForm Technologies

- Green Dot Bioplastics Inc.

- GreenGran BN

- Jelu-Werk Josef Ehrler GmbH & Co. Kg

- Meshlin Composites ZRT

- NPSP NV

- Oldcastle APG

- Polyvlies Franz Beyer GmbH & Co. Kg

- Tecnaro GmbH

- The AZEK Company

- Trex Company Inc.

- TTS

- UPM-Kymmene Oyj

第七章 市场机会及未来趋势

- 在建设产业中越来越受欢迎

简介目录

Product Code: 54642

The natural fiber reinforced composites market is expected to grow from 4,081.05 kilo tons in 2024 to 6,104.85 kilo tons by 2029, registering a CAGR of 8.39% during the forecast period.

Key Highlights

- Over the medium term, factors such as the increasing demand for bio-based composites and the growing demand for eco-friendly composites in the electronics industry would drive the natural fiber-reinforced composites market.

- However, the moisture adsorption, restricted processing temperature, incompatibility with most polymer matrices, and lower impact resistivity compared to glass fiber-reinforced composites are likely to act as restraints for the market.

- Nevertheless, the flame retardancy of natural fiber-reinforced polymer composites is expected to provide new opportunities for the market.

- The Asia-Pacific region dominates the market and is likely to witness the highest CAGR during the forecast period. This growth is attributed to the rapid rise in expenditure on the construction industry.

Natural Fiber Reinforced Composites Market Trends

Increasing Demand from the Construction Sector

- There is always a continuous requirement for eco-friendly materials in the building materials industry. Natural fiber-reinforced polymer-based composites are increasingly used in civil engineering construction applications due to their numerous advantages.

- In the building and construction industry, composite materials are extremely significant. Industrial supports, tanks, long-span roof structures, tanks, high-rise buildings and lightweight doors, windows, furnishings, lightweight buildings, bridge components, and complete bridge systems have all employed composite materials. Composite materials are becoming increasingly essential in the construction industry as a means of achieving long-term sustainability.

- The construction sector has witnessed major investments in recent years. According to Oxford Economics, the global construction industry is expected to grow by USD 4.5 trillion, or 42%, between 2020 and 2030 to reach USD 15.2 trillion. Also, China, India, the United States, and Indonesia are expected to account for 58.3% of global growth in construction between 2020 and 2030.

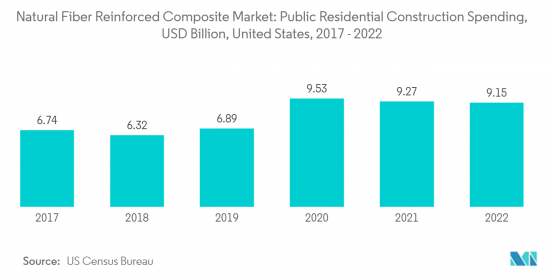

- In North America, the United States has a major share in the construction industry. Besides the United States, Canada and Mexico contribute significantly to investments in the construction sector. According to the United States Census Bureau Data, the annual value of public residential construction in the United States was valued at USD 9.15 billion in 2022, an increase of 35.7% compared to USD 6.74 billion in 2017.

- Similarly, the European construction sector grew by 2.5% in 2022 due to new investments from the EU Recovery Fund. Business confidence picked up in early 2022, despite price pressures at most EU construction firms, and is expected to reach pre-COVID-19 levels. Moreover, as the crisis due to COVID-19 abates, builders become less reluctant to invest in new corporate buildings and renovate existing properties.

- Hence, the aforementioned trends are projected to influence the growth of natural fiber-reinforced composites in the construction sector over the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the global market. With growing construction activities in countries such as China, India, and Japan, the usage of natural fiber-reinforced composites is increasing in the region.

- The construction sector is a key player in China's continued economic development. According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030, creating a positive outlook for natural fiber-reinforced composites.

- As per the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025. Keeping in view the given forecasts, the Chinese government unveiled a five-year plan in January 2022 focused on making the construction sector more sustainable and quality-driven.

- Similarly, the surging application of natural fiber-reinforced composites in the electronics industry is likely to support the industry growth in the country. According to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025.

- Furthermore, automotive is among the major consumers of natural fiber-reinforced composites. The automotive industry in India is an important indicator of the Indian economic performance, as this sector plays a vital role in both technological advancements and macroeconomic expansion.

- Additionally, the Indian government has created momentum through its Faster Adoption and Manufacturing of (Hybrid and) Electric Vehicles schemes that encourage, and in some segments, mandate the adoption of electric vehicles (EV), intending to reach 30% EV penetration by 2030. The scheme creates demand incentives for EVs and supports the deployment of charging technologies and stations in urban centers. The government has set a target of 70% of all commercial cars, 30% of private cars, 40% of buses, and 80% of two-wheelers and three-wheelers sold in India by 2030 to be electric.

- Hence, the new policies and investments made by different governments are expected to boost the demand for the natural fiber-reinforced composites market in the rest of Asia-Pacific during the forecast period.

Natural Fiber Reinforced Composites Industry Overview

The natural fiber-reinforced composites market is fragmented, with no player capturing a significant market share. The major players in the market (in no particular order) include Trex Company Inc., Fiberon Technologies Inc., UPM-Kymmene Oyj, The AZEK Company, and Oldcastle APG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Bio-based Composites

- 4.1.2 Growth in Automotive Industry Worldwide

- 4.2 Restraints

- 4.2.1 Moisture Adsorption, Restricted Processing Temperature, and Incompatibility with Most Polymer Matrices

- 4.2.2 Degradation Issue Due to Exposure to the External Environment

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Fiber

- 5.1.1 Wood Fiber Composites

- 5.1.2 Non-wood Fiber Composites

- 5.1.2.1 Cotton

- 5.1.2.2 Flax

- 5.1.2.3 Kenaf

- 5.1.2.4 Hemp

- 5.1.2.5 Other Non-wood Fiber Composites

- 5.2 Polymer

- 5.2.1 Thermosets

- 5.2.2 Thermoplastics

- 5.2.2.1 Polyethylene

- 5.2.2.2 Polypropylene

- 5.2.2.3 Poly Vinyl Chloride

- 5.2.2.4 Other Thermoplastics

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Automotive

- 5.3.3 Building and Construction

- 5.3.4 Electrical and Electronics

- 5.3.5 Sports

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Amorim Cork Composites SA

- 6.4.2 Fiberon Technologies Inc.

- 6.4.3 FlexForm Technologies

- 6.4.4 Green Dot Bioplastics Inc.

- 6.4.5 GreenGran BN

- 6.4.6 Jelu-Werk Josef Ehrler GmbH & Co. Kg

- 6.4.7 Meshlin Composites ZRT

- 6.4.8 NPSP NV

- 6.4.9 Oldcastle APG

- 6.4.10 Polyvlies Franz Beyer GmbH & Co. Kg

- 6.4.11 Tecnaro GmbH

- 6.4.12 The AZEK Company

- 6.4.13 Trex Company Inc.

- 6.4.14 TTS

- 6.4.15 UPM-Kymmene Oyj

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity in the Building and Construction Industry

02-2729-4219

+886-2-2729-4219

2024-2032 年连续纤维复合材料市场(按树脂类型、产品类型、增强类型、垂直产业和地区划分)

2024-2032 年连续纤维复合材料市场(按树脂类型、产品类型、增强类型、垂直产业和地区划分) 复合纤维:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

复合纤维:市场占有率分析、产业趋势与统计、成长预测(2024-2029) CFRTP 市场:依树脂类型、产品类型、应用划分 - 2024-2030 年全球预测

CFRTP 市场:依树脂类型、产品类型、应用划分 - 2024-2030 年全球预测 全球碳纤维增强热塑性复合材料 (CFRTP) 市场 - 2023-2030

全球碳纤维增强热塑性复合材料 (CFRTP) 市场 - 2023-2030 纤维增强复合材料市场(产品:短纤维增强复合材料和长纤维/连续增强复合材料;类型:玻璃、碳、芳纶等)-2023 年全球行业分析、规模、份额、增长、趋势和预测-2031

纤维增强复合材料市场(产品:短纤维增强复合材料和长纤维/连续增强复合材料;类型:玻璃、碳、芳纶等)-2023 年全球行业分析、规模、份额、增长、趋势和预测-2031 CFRTP 的全球市场:依产品类型、树脂类型、应用、地区 - 预测(截至 2028 年)

CFRTP 的全球市场:依产品类型、树脂类型、应用、地区 - 预测(截至 2028 年) 天然纤维增强复合材料市场:按纤维类型、按聚合物、按最终用户行业、按地区 - 规模、份额、展望、机会分析,2023-2030 年

天然纤维增强复合材料市场:按纤维类型、按聚合物、按最终用户行业、按地区 - 规模、份额、展望、机会分析,2023-2030 年 纤维强化复合材料的全球市场

纤维强化复合材料的全球市场 纤维增强复合材料市场:依纤维类型、基体类型、用途- 2023-2030 年全球预测

纤维增强复合材料市场:依纤维类型、基体类型、用途- 2023-2030 年全球预测 短纤维强化复合材料的全球市场:2016年~2032年

短纤维强化复合材料的全球市场:2016年~2032年

▼