|

市场调查报告书

商品编码

1404104

声学感测器:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Sound Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

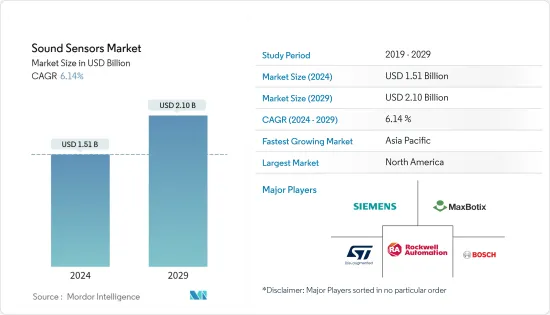

声学感测器市场规模预计到2024年为15.1亿美元,预计到2029年将达到21亿美元,在市场估计和预测期间(2024-2029年)复合年增长率为6.14%。

由于新兴应用是声学感测器的潜在市场,例如自动驾驶和半自动车辆以及自动自动导引运输车,预计未来对声学感测器的需求将增长。

主要亮点

- 声音感测器的核心是侦测声波的感测模组。声波通常以移动空气或水分子的机械震动的形式出现,然后转换为电讯号。声音感测器的主要部件包括侦测声音来源的麦克风、峰值检测器和音讯放大器。声音感测器主要用于安全、开关和监控应用。

- 推动该市场成长的因素是声学感测器应用基础的扩展和技术的快速进步。智慧家庭设备对可靠、高性能感测器的需求不断增长也是推动声音感测器市场高速成长的主要因素。此外,大公司在开发具有成本效益和高效的感测器方面的投资导致感测器变得更小,并在家用电子电器产业中找到了重要的应用。

- 声音感测器,包括超音波和音讯感测器,具有成本低、灵敏度高、能够在许多行业工作等优点。因此,各领域的采用正在取得进展。例如,这些感测器整合到太阳能城市污染监测 (SPCPM) 系统中,在声音污染成为人们关注的问题时,有助于监测城市的声音品质。

- 此外,近年来,智慧家居设备变得越来越普及。这些感测器越来越多地被纳入安全系统、带有语音命令的家用电器以及父母和看护者的婴儿监控系统中。由于该领域不断的技术创新,越来越多的新使用案例被识别出来,为所研究的市场带来了机会。例如,正在研究开发婴儿监视器,该监视器可以阻挡其他噪音,同时在婴儿需要关注时提醒父母。

- 然而,该领域的一个重大限制是担心表面声波感测器将被质量灵敏度较低的其他感测器替代。此外,随着新技术的不断出现,预计会出现新的挑战并挑战所研究市场的成长。

- 另一个技术限制是声学感测器在真空中使用时的性能有限,因为声波的传输需要空气。此外,特定声学感测器的功能也会受到任何表面或软边缘的影响,因为某些温度水平可能会阻碍市场成长。

声学感测器市场趋势

医疗保健预计将占据很大的市场占有率

- 声音或声学感测器是医疗业务的一个组成部分。涉及感测器的医疗业务是高度敏感的功能,需要适当的品质和可靠性。使用超音波换能器进行超音波检查也是声学感测器在医学领域的一个非常重要的特点。

- 连网型医疗服务的发展以及对用于监测关键人体生命体征的低功耗声学感测器的持续研究正在扩大这些解决方案的应用领域,并将继续推动这一领域的发展。预计将成为推动需求的关键因素之一。

- 近年来,低成本、穿戴式医疗保健设备的采用显着增加。压电心音感测器非常适合长期动态监测心臟功能,并为心臟病的初步诊断提供技术支持,从而增加具有健康监测普及的可穿戴设备的采用,将推动所研究市场的机会。

- 世界各地的人均医疗支出不断增加,对先进医疗设备和技术以帮助改善医疗基础设施的需求也在增加。例如,根据经合组织的数据,美国在人均医疗支出方面领先全球(12,555.3美元),其次是瑞士(8,049.1美元)和德国(8,010.9美元)。

- 此外,声音感测器製造和感测能力的进步将使医疗设备製造商受益,考虑到它们的微调和提供清晰明确结果的能力,利用在医疗领域不同领域整合感测器的需求。创造机会。在不久的将来可能会快速渗透到医疗领域,这反过来将为声学感测器市场的成长做出重大贡献。

预计北美将占据较大市场占有率

- 由于其发达的工业部门以及与其他地区相比安全支出的天文数字差异,预计北美将占据大部分市场占有率。高支出表明感测器已经在各个方面开发和有效部署,相对于其他感测器建立了显着的技术和资讯优势。

- 美国在医疗保健、国防、工业、消费性电子和通讯方面的支出仍然位居世界前列。例如,根据消费者技术协会 (CTA) 的数据,2023 年美国智慧家庭设备销售额预计将达到 235 亿美元。同样,该国可穿戴设备的销售额预计将大幅成长,到 2023 年将达到 138 亿美元,而 2018 年为 77 亿美元。

- 此外,该市场还得到强大生态系统的支持,支持该地区新技术的快速采用。例如,该地区正在迅速采用工业物联网(IIOT),因为随着无线通讯、连网型设备和工厂自动化的采用,已经存在了最大限度地效用声学感测器的必要基础设施,它为市场提供了支援。此外,「美国製造」等政府倡议预计将进一步推动工业领域先进技术的采用,并在预测期内为调查市场创造机会。

- 此外,美国也是汽车、国防车辆/设备和飞机的领先製造商之一。例如,该国是波音、洛克希德火星公司和诺斯罗普格鲁曼公司等主要飞机製造商的所在地。 2022年,波音在全球交付了约480架飞机。随着声学感测器广泛应用于汽车和飞机系统,这些趋势正在支持北美市场的成长。

声学感测器产业概况

声学感测器市场竞争适度,由几家主要企业组成。儘管就市场占有率,但不断增长的需求正在吸引新参与者进入市场,并加剧供应商之间的竞争。製造商寻求透过提高产品专业知识来获得竞争优势。主要市场参与者包括罗克韦尔自动化、西门子、义法半导体和罗伯特博世有限公司。

2023年3月,凸版印刷开发了一种感测系统,可以远端监测工厂和设施正常运作期间不会出现的摩擦噪音和金属对金属碰撞声音等异常声音。

2023 年 2 月,PolySense 推出了适用于工业环境和智慧城市的室内外声学和噪音感测器集群,支援健康监测和城市管理。新型声学/噪音感测器由新的 iEdge 4.0 OS 模组化和可配置 WxS 产品平台提供支持,可为用户提供更强大的功能来监控噪音污染并采取行动。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 由于市场技术进步,采用率增加

- 製造成本低

- 市场抑制因素

- 替代技术的出现

第 6 章 技术概览

- 水听器

- 定向

- 定向的

- 麦克风

- 驻极体麦克风

- 压电麦克风

- 电容麦克风

- 动圈/磁力麦克风

- 其他麦克风

第七章市场区隔

- 按最终用户产业

- 消费性电子产品

- 通讯

- 产业

- 防御

- 卫生保健

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第八章竞争形势

- 公司简介

- CTS Corporation

- General Electric

- Maxbotix, Inc.

- Rockwell Automation, Inc.

- Siemens AG

- ST Microelectronics, Inc.

- Robert Bosch Gmbh

- Panasonic Corporation

- Bruel & Kjar GmbH

- Teledyne Technologies Incorporated

第九章投资分析

第十章市场机会与未来趋势

The Sound Sensors Market size is estimated at USD 1.51 billion in 2024, and is expected to reach USD 2.10 billion by 2029, growing at a CAGR of 6.14% during the forecast period (2024-2029).

With emerging applications that have become potential markets for sound sensors, such as autonomous and semi-autonomous self-driving cars and AGVs, the demand for sound sensors is expected to gain momentum in the future.

Key Highlights

- A sound sensor at its core is a sensing module that detects sound waves, usually produced as mechanical vibration of moving air or water molecules, and converts them into electrical signals. A sound sensor's key components include a microphone that detects the sound source, a peak detector, and an audio power amplifier. Sound sensors are primarily adopted in security, switching, and monitoring applications.

- Essential drivers for the growth of this market are the expanding application base for sound sensors and rapid technological advancements. The rising demand for reliable and high-performance sensors in smart home devices is another primary driver that is responsible for the high growth rate of the sound sensors market. Furthermore, investments by major players in developing cost-effective and efficient sensors have also led to miniaturized sensors, which find significant applications in the consumer electronics industry.

- Sound sensors, including acoustic, ultrasound, and audio sensors, have several advantages, like low cost, high sensitivity, and ability to function across many industries. As a result, their adoption has been growing across various sectors. For instance, these sensors are being incorporated into Solar Powered City Pollution Monitor (SPCPM) systems, which can help monitor sound quality in the city, as sound pollution is a growing concern nowadays.

- Furthermore, in recent years, the penetration of smart home devices has also grown significantly. These sensors are increasingly being incorporated into security systems, appliances with voice command features, baby monitoring systems for parents or caretakers, etc. With innovations being a constant in this domain, new use cases are increasingly being identified, driving opportunities in the studied market. For instance, research works are being undertaken to develop a baby monitor that alerts parents when their baby needs attention while filtering out the noise from other sources.

- However, a significant limitation of this sector is the concern with respect to surface acoustic wave sensors being substituted with other sensors with a low mass sensitivity. Furthermore, with new technologies continuously emerging, new challenges are also anticipated to appear and challenge the growth of the studied market.

- Other technical limitations include the performance limitation of sound sensors when used in a vacuum, as sound waves require air for transmission. Additionally, the capabilities of specific sound sensors are also affected by any surface or soft edges, as a certain temperature level is likely to hamper the growth of the studied market.

Sound Sensors Market Trends

Healthcare is Expected to Hold a Significant Market Share

- Sound or acoustic sensors form an integral part of medical operations. Medical operations, including the sensors, are extremely sensitive functions that require proper quality and reliability. Using ultrasonic transducers for sonography is another very important function of sound sensors in the medical sector.

- The evolution of connected medical services and the continued research in low-power sound-based sensors used in monitoring the critical vitals of the human body have broadened the application area for these solutions, and this is expected to remain one of the significant factors driving the demand for this segment.

- In recent years, the adoption of low-cost and wearable healthcare devices has grown significantly. As piezoelectric heart sound sensors are highly suitable for long-term dynamic monitoring of the heart's functioning and provide technical support for preliminary diagnosis of heart disease, the growing penetration of wearables with health monitoring facilities will drive opportunities in the studied market.

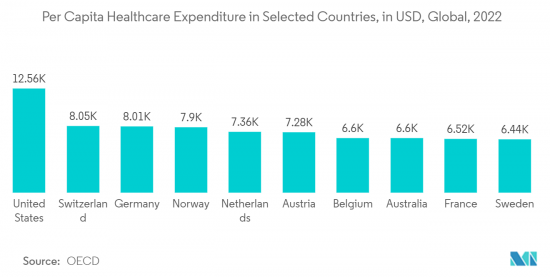

- With per capita healthcare expenditure growing across the globe, the demand for advanced medical devices and technologies to help improve the healthcare infrastructure is also growing, which in turn is creating a favorable outlook for the growth of the studied market. For instance, according to the OECD, the United States leads the world in terms of per capita healthcare expenditure (USD 12,555.3), followed by Switzerland (USD 8,049.1) and Germany (USD 8,010.9)

- Furthermore, advancements in the fabrication and sensing capabilities of sound sensors have also created an opportunity for medical device manufacturers to capitalize on the need for the integration of sensors in different fields of the healthcare sector, considering its ability to fine-tune and provide definite and clear results. A rapid penetration in the medical sector is plausible and can be observed in the near future, which, in turn, will contribute significantly to the growth of the sound sensors market.

North America is Expected to Hold a Major Market Share

- North America is expected to hold most of the market share, owing to its developed industrial segment and the astronomical difference in security spending compared to others. The high spending indicates a developed and efficient implementation of sensors on different fronts to establish a significant technological and intelligence advantage over others.

- The healthcare, defense, industrial, consumer electronics, and telecommunication-related expenses in the United States are still among the highest in the world. For instance, according to the Consumer Technology Association (CTA), the sales of smart home devices in the United States are anticipated to reach USD 23.5 billion in 2023. Similarly, wearable device sales revenue in the country is also anticipated to grow significantly, reaching USD 13.8 billion in 2023, compared to USD 7.7 billion in 2018.

- Furthermore, the market has also been helped by a robust ecosystem supporting the fast adoption of new technology in the region. For instance, IIOT adoption has been fast in the region, as adopters of wireless communication, connected devices, and factory automation have helped the market, as the infrastructure necessary to maximize the utility of acoustic sensors is already there. Additionally, government initiatives such as "Made in America" are anticipated to further drive the adoption of advanced technologies in the industrial domain, creating opportunities in the studied market during the forecast period.

- Moreover, the United States is also among the leading manufacturers of automobiles, defense vehicles/equipment, and aircraft. For instance, the country is home to some of the leading aircraft manufacturers, including Boeing, Lockheed Martien, Northrop Grumman Corp, etc. In 2022, Boeing delivered about 480 aircraft globally. As sound sensors are widely used in automobiles and aircraft systems, such trends support the studied market's growth in North America.

Sound Sensors Industry Overview

The sound sensors market is moderately competitive and consists of several major players. A few of the major players currently dominate the market in terms of market share; however, the growing demand is attracting new players into the market, driving competitive rivalry among the vendors. The manufacturers are trying to gain a competitive advantage by improving their expertise in the product. Some key market players include Rockwell Automation, Siemens, STMicroelectronics, and Robert Bosch Gmbh, among others.

In March 2023, Toppan developed a sensing system for remotely monitoring abnormal sounds, such as friction and metal-on-metal impacts, that do not occur during normal operation at factories and facilities to drive greater efficiency for inspection and maintenance work by promptly identifying abnormalities in equipment, indicating when machinery parts need maintenance or replacement.

In February 2023, Polysense announced indoor and outdoor sound/noise sensor clusters for industrial environments and smart cities, enabling health monitoring and city management. Powered by the new iEdge 4.0 OS modular and configurable WxS product platform, the new sound/noise sensor can equip users with more powerful capabilities to monitor and take action on noise pollution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technology Advancement in the Market, Leading to Increasing Adoption

- 5.1.2 Low Manufacturing Cost

- 5.2 Market Restraints

- 5.2.1 Emergence of Alternative Technologies

6 TECHNOLOGY SNAPSHOT

- 6.1 Hydrophone

- 6.1.1 Omni-directional

- 6.1.2 Directional

- 6.2 Microphone

- 6.2.1 Electret Microphones

- 6.2.2 Piezoelectric Microphones

- 6.2.3 Condenser Microphones

- 6.2.4 Dynamic/Magnetic Microphones

- 6.2.5 Other Microphones

7 MARKET SEGMENTATION

- 7.1 By End-User Industry

- 7.1.1 Consumer Electronics

- 7.1.2 Telecommunications

- 7.1.3 Industrial

- 7.1.4 Defense

- 7.1.5 Healthcare

- 7.1.6 Other End-User Industries

- 7.2 By Geography

- 7.2.1 North America

- 7.2.2 Europe

- 7.2.3 Asia-Pacific

- 7.2.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 CTS Corporation

- 8.1.2 General Electric

- 8.1.3 Maxbotix, Inc.

- 8.1.4 Rockwell Automation, Inc.

- 8.1.5 Siemens AG

- 8.1.6 ST Microelectronics, Inc.

- 8.1.7 Robert Bosch Gmbh

- 8.1.8 Panasonic Corporation

- 8.1.9 Bruel & Kjar GmbH

- 8.1.10 Teledyne Technologies Incorporated

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

表面声波感测器:市场占有率分析、产业趋势、成长预测(2024-2029)

表面声波感测器:市场占有率分析、产业趋势、成长预测(2024-2029) 表面声波感测器的全球市场:分析 - 按感测类型、最终用户、地区、预测(至 2030 年)

表面声波感测器的全球市场:分析 - 按感测类型、最终用户、地区、预测(至 2030 年) 声学感测器市场:按类型、波形、感测参数、应用分类 - 2024-2030 年全球预测

声学感测器市场:按类型、波形、感测参数、应用分类 - 2024-2030 年全球预测 声波感测器市场:按产品类型、设备、感测参数、产业划分 - 2024-2030 年全球预测

声波感测器市场:按产品类型、设备、感测参数、产业划分 - 2024-2030 年全球预测 2022-2029年全球声音传感器市场规模研究和预测,按行业(消费电子、电信、工业、国防、医疗保健、其他终端用户行业)和区域分析

2022-2029年全球声音传感器市场规模研究和预测,按行业(消费电子、电信、工业、国防、医疗保健、其他终端用户行业)和区域分析 声波传感器全球市场研究报告 - 2023-2030 年行业分析、规模、份额、增长、趋势和预测

声波传感器全球市场研究报告 - 2023-2030 年行业分析、规模、份额、增长、趋势和预测 全球表面声波传感器市场研究与预测:按传感类型(压力传感器、扭矩传感器、粘度传感器)、最终用户行业(汽车、消费电子、工业)、区域分析,2022-2029 年

全球表面声波传感器市场研究与预测:按传感类型(压力传感器、扭矩传感器、粘度传感器)、最终用户行业(汽车、消费电子、工业)、区域分析,2022-2029 年 声学传感器市场 - 增长、趋势、COVID-19 影响和预测(2022-2027 年)

声学传感器市场 - 增长、趋势、COVID-19 影响和预测(2022-2027 年) 音感测器的全球市场 - 成长,未来展望,竞争分析(2022年~2030年)

音感测器的全球市场 - 成长,未来展望,竞争分析(2022年~2030年) 声波感测器的全球市场预测:各趋势类型(表面趋势感测器(SWS),散装趋势感测器(BWS)),感测参数(化学气相淀积,扭矩,温度,粘度,压力),各地区的分析(到2028年)

声波感测器的全球市场预测:各趋势类型(表面趋势感测器(SWS),散装趋势感测器(BWS)),感测参数(化学气相淀积,扭矩,温度,粘度,压力),各地区的分析(到2028年)