|

市场调查报告书

商品编码

1404322

气体探测器:市场占有率分析、行业趋势和统计、2024-2029 年成长预测Gas Detectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

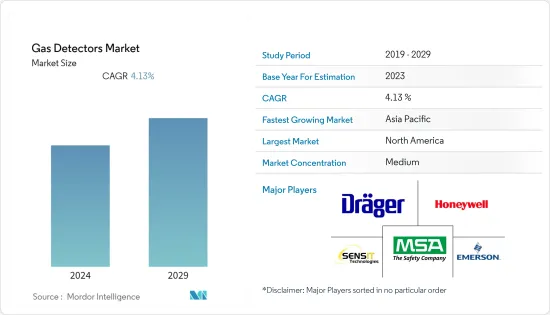

气体侦测器市场规模预计将从2024年的32.5亿美元成长到2029年的39.8亿美元,预测期间(2024-2029年)复合年增长率为4.13%。

主要亮点

- 有几个因素显着推动了研究市场的成长,包括职场安全意识的增强、提高准确性和可靠性的技术进步、气体探测器的使用、快速工业化以及对环境监测的日益关注。

- 几家主要市场供应商正在开发先进的气体检测器,其应用范围涵盖临床分析、环境排放控制、爆炸物检测、农业储存、出货和职场危险监测。例如,ATO Inc. 于 2023 年 7 月宣布推出适用于密闭空间和其他复杂环境的新系列多气体探测器。透过同时监测多达四种不同的气体,该系统可以快速识别有毒化合物、可燃性气体和氧气含量,从而提高工人的安全。

- 严格的政府法规也提高了车辆的燃烧效率,以限制有害污染物的排放。这导致气体感测器和探测器的进一步采用,它们越来越多地用于向车辆排放气体管理系统提供即时回馈。 2023年6月,拜登-哈里斯政府发起了一项全政府范围的努力,以大幅减少温室气体排放。此外,拜登总统的国家目标是到2030年将全球甲烷排放量比2020年的水平减少30%,这也对气体探测器在汽车行业的普及起到了重要作用。各个最终用户产业中气体洩漏案例的数量不断增加,对气体探测器的需求进一步增加。

- 此外,无线/便携式气体探测器由于较低的初始成本和经常性成本、降低的维护成本、改进的劳动力管理、更快的资源工作流程和更高的安全性而被广泛采用。此外,感测器能力的发展和小型化以及通讯能力的提高使得物联网感测器能够整合到大量机器和设备中,而不会影响安全距离内有毒和可燃性气体的检测。随着物联网感测器的成本不断下降,危险物质/爆炸物产业开始将这些感测器纳入日常业务中,以提高环境安全和业务效率。

- 政府机构正在采取积极措施强制在潜在危险场所使用气体探测器,气体探测器主要用于化学、工业、医疗和汽车行业来监测空气品质。它积极用于检测可燃性气体它被认为是多个行业的关键齿轮,可在气体浓度异常升高时触发紧急程序。随着一些知名公司不断增加研发力度和技术进步,可调谐二极体雷射(TDLA) 等技术正在开发中,用于检测和测量空气中低浓度的气体。这提供了多种测量优势,包括高度稳定的校准和减少因干扰而产生的干扰。是否存在其他气体。

- 另一方面,技术纯熟劳工的缺乏是气体探测器市场的重要抑制因素。与气体洩漏检测仪具体应用相关的培训至关重要,缺乏熟练人员可能会阻碍气体检测仪的采用和有效使用。

- 此外,无线气体侦测器的高製造成本以及无法限制火灾危险可能会阻碍气体侦测器的普及。

气体检测仪市场趋势

石油和天然气产业预计将占据主要份额

- 由于对气体监测设施识别有害气体存在的需求不断增加,尤其是在工业领域,气体检测仪市场预计将继续成长。在石油和天然气领域使用物联网可以改善油田的现场通讯、即时监控、数位基础设施,降低维护成本,降低电力消耗,提高产量,并提高工人和资产的安全保障。例如,浪费汽油是一个需要解决的严重问题。液化石油气高度易燃,对人员和财产造成危险。当与物联网结合使用时,气体探测器可以极大地协助气体检测并防止气体浪费。

- 根据石油输出国组织的数据,预计2022年全球原油需求(包括生质燃料)将达到9,957万桶/日以上,2023年将增加至约1,0189万桶/日。此外,根据EIA的数据,到年终,全球液体燃料消费量预计将达到约1.0214亿桶/日。对原油和燃料的需求不断增长可能会推动所研究市场的成长。

- 由于存在大量石油钻探设施,预计北美地区将稳定成长。据贝克休斯称,北美持有世界上最多的石油和天然气钻井平台。截至 2023 年 5 月,该地区有 776 个陆上钻井平台,另有 22 个海上钻井平台。到年终,全球将有 1,532 个陆上石油钻井平台运作中,而海上钻井平台数量为 231 个。

- 美国内政部 (DoI)核准的 2019-24 年度国家大陆棚石油和天然气租赁计划使近 90% 的外大陆棚(OCS) 英亩可用于海上勘探钻探,增加了正在考虑潜在的市场供应商。预计机会将会出现。

- 根据RegData的行业监管指数,石油和天然气开采行业是美国监管最严格的10个行业之一。负责执行美国海上石油和天然气行业安全和环境保护保护条例的安全与环境执法局 (BSEE) 等监管机构已扩展到欧洲等地区。这些机构的严格监管正在促进气体探测器市场的开拓。

- 根据《石油与天然气日誌》报告,与未采用先进技术的公司相比,利用先进技术来管理安全和营运绩效的公司可将计划外资产停机时间减少约8%,并将合规相关成本减少约8%。据报道,可以减少违规行为13%,违规执法减少 8%,营业报酬率比公司计画目标高出 2% 以上。而且,气体探测器提供的众多优势预计将在预测期内增加市场需求。

北美预计将占据很大份额

- 由于大型供应商的存在以及政府有关气体排放限制的法规,北美的气体探测器出现成长。在北美地区,美国环保署(EPA)和美国职业安全与健康管理局(OSHA)严格执行工业安全并推广气体侦测器的采用。

- 美国几乎每家企业都必须遵守 OSHA 标准,这使其成为各行业雇主和员工的主要关注点。美国环保署宣布了新的排放绩效标准,以衡量和限制新建、重建和改造资产的甲烷排放。

- 美国环保署也强制要求在采矿中使用气体探测器。总部位于美国的卡罗尔技术集团是为采矿业提供手持式气体探测器的先驱。其中一款产品是矿山安全设备 (MSA) Altair 4X 探测器,它会在检测后 15 秒内向矿工发出警报。

- 此外,北美拥有世界上最活跃的采矿业之一。根据加拿大矿业协会的数据,加拿大是世界上 13 种矿物和金属的生产国之一,其中包括铀、镍、钴、钾肥、铝、钻石、钛和黄金。此外,根据美国地质调查局的数据,2022年美国采矿业的运转率预计为87%,高于2021年的81%。此类案例预计将为所研究市场的成长提供有利可图的机会。

- 该地区是世界各地主要製造设施的主要枢纽。此外,在美国和加拿大等国家,由于地方当局要求高水准的安全性,气体探测器正在引入该行业。此外,2022 年 10 月,美国劳工部矿山安全与健康管理局 (MSHA)津贴985,284 美元,用于支援安全课程和其他计画。

气体检测仪产业概况

气体探测器市场的竞争是温和的,并由几家大公司组成。从市场占有率来看,目前该市场由几家大型企业占据主导地位。这些拥有突显市场占有率的大公司正致力于扩大海外基本客群。这些公司利用策略合作计划来增加市场占有率和盈利。竞争、快速的技术进步和消费者偏好的频繁变化预计将威胁公司在预测期内的成长。

2022年10月,德尔格海工宣布推出移动式气体侦测仪X-am 2800。该新产品可同时测量多达四种气体,用于密闭空间,以保护在可能存在爆炸性环境、氧气消耗和有毒物质的区域工作的员工。

2022 年 10 月,Blackline Safety Corporation 在 2022 年阿布达比国际石油展及会议上宣布预览其新型 G6 单一气体检测仪。据该公司称,ADIPEC 将是中东经销商、客户、媒体和分析师第一次有机会看到这项针对石化、石油和天然气及其他工业职场的突破性连网型创新。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- COVID-19 影响评估

第五章市场动态

- 市场驱动因素

- 主要产业风险意识不断增强

- 严格的政府法规保障工人安全

- 专注于智慧探测器的企业

- 市场抑制因素

- 市场竞争加剧

第六章市场区隔

- 依通讯类型

- 有线

- 无线的

- 按下检测器类型

- 固定式

- 便携的

- 按最终用户产业

- 油和气

- 化工/石化

- 用水和污水

- 金属/矿业

- 公共产业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章竞争形势

- 公司简介

- Honeywell International Inc.

- Dragerwerk AG & Co. KGaA

- MSA Safety Inc.

- Emerson Electric Company

- SENSIT Technologies, LLC

- Industrial Scientific Corporatioh

- New Cosmos Electric Co. Ltd

- Trolex Ltd

- Crowncon Detection Instruments Limited

- Hanwei Electronics Group Corporation

- International Gas Detectors Ltd

- Sensidyne LP

第八章投资分析

第9章市场的未来

The Gas Detectors Market size is expected to grow from USD 3.25 billion in 2024 to USD 3.98 billion by 2029, registering a CAGR of 4.13% during the forecast period (2024-2029).

Key Highlights

- Several factors, like the increasing awareness of workplace safety, advancements in technology leading to enhancements in accuracy, reliability, use of gas detectors, rapid industrialization, and growing focus on environmental monitoring, are anticipated to drive the growth of the studied market significantly.

- Several major market vendors are developing advanced gas detectors with applications across clinical assays, environmental emission control, explosive detection, agricultural storage, shipping, and workplace hazard monitoring. For instance, in July 2023, ATO Inc. introduced its new line of multi-gas detectors for confined spaces and other complex environments. It is claimed to improve worker safety by quickly identifying poisonous compounds, flammable gases, and oxygen levels by monitoring up to four different gases simultaneously.

- Stringent government regulations have also resulted in the efficiency enhancement of combustion within the vehicle to limit the emission of harmful pollutants. This has further increased the adoption of gas sensors and detectors, therefore gaining applications in providing real-time feedback to emission management systems of automobiles. In June 2023, the Biden-Harris Administration launched a whole-of-government initiative to significantly reduce greenhouse gas emissions. In addition, President Biden's national goal is to cut global methane emissions by 30 percent below 2020 levels by 2030, which also plays an important role in the penetration of gas detectors in the automotive industry. The increasing cases of gas leaks in various end-user industries are further creating a demand for gas detectors.

- Wireless/portable gas detectors are also witnessing widespread adoption owing to their reduced initial implementation costs and recurrent savings, lower maintenance costs, better workforce management, faster resource workflow, and improved safety. Moreover, the development of sensor capabilities and miniaturization, coupled with improved communication capabilities, enables the integration of IoT sensors into numerous machines and devices without compromising the detection of toxic or flammable gases at safe distances. As IoT sensors' cost is declining, industries dealing with hazardous/explosive materials have started integrating these sensors into their day-to-day operations to improve environmental safety and operational efficiency.

- Governmental agencies have been taking proactive measures to enforce the use of gas detectors in potentially hazardous locations, where they are seen as a vital cog for triggering emergency procedures across several industries in case of an abnormal increase in the concentration of gases that are actively employed for monitoring the air quality and detection of combustible gases primarily in the chemical, industrial, medical, and automotive industries. With increased R&D efforts, along with the technological advancements by some prominent players, technologies such as tunable diode lasers (TDLA) are being developed, which detect and measure gases at a low density of air, thereby offering several measurement advantages, such as highly stable calibration and less cross-interference from the presence of other gases.

- On the flip side, the lack of skilled labor is an essential restraining factor for the gas detector market. Training associated with specific applications of gas leak detectors is essential, and the shortage of skilled personnel could hinder the adoption and effective use of gas detectors.

- Further, the high cost of production of wireless gas detectors and the inability of the detectors to restrict probable fire hazards could hinder the widespread adoption of gas detectors.

Gas Detector Market Trends

Oil and Gas Sector is Expected to Hold Major Share

- The market for gas detectors is expected to continue to rise, especially in the industrial sector, as there is an increasing need for gas monitoring amenities to identify the presence of hazardous gases. The use of IoT in the oil and gas sector has resulted in improved field communication, real-time monitoring, digital infrastructure for oil fields, decreased maintenance costs, lower power consumption, more production, and increased safety and security for workers and assets. For instance, petrol waste is a serious problem that must be resolved. Liquefied petroleum gas is highly combustible and dangerous to both people and property. When used in conjunction with IoT, gas detectors can significantly aid in gas detection and prevent gas wastage.

- According to the Organization of the Petroleum Exporting Countries, the global demand for crude oil (including biofuels) in 2022 amounted to over 99.57 million barrels per day, and it is estimated to increase to approximately 101.89 million barrels per day in 2023. Also, according to EIA, the worldwide consumption of liquid fuels is forecasted to reach approximately 102.14 million barrels per day by the end of 2023. The increasing demand for crude oil and fuel is likely to boost the growth of the studied market.

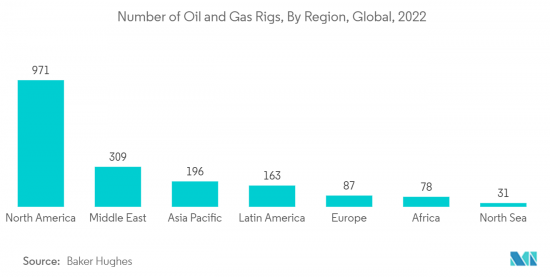

- North America is estimated to witness robust growth owing to the presence of numerous oil rigs. According to Baker Hughes, North America hosts the most oil and gas rigs worldwide. As of May 2023, there were 776 land rigs in that region, with a further 22 rigs located offshore. By the end of 2022, there were 1,532 operational onshore oil rigs globally, compared with 231 offshore rigs.

- The National Outer Continental Shelf Oil and Gas Leasing Program for 2019-24, approved by the U.S. Department of the Interior (DoI), allows for offshore exploratory drilling on nearly 90% of the Outer Continental Shelf (OCS) acreage, and this is expected to create new opportunities for the market vendors under consideration.

- According to the RegData's Industry Regulation Index, the oil and gas extraction industry is among the top 10 most regulated industries in the United States. Regulatories like the Bureau of Safety and Environmental Enforcement (BSEE) - which enforces safety and environmental protection regulations for the offshore oil & natural gas industry in the United States - are also prevalent across regions like Europe. The strict rules imposed by such institutions facilitate the development of the gas detector market.

- According to the Oil & Gas Journal, companies that are utilizing advanced technologies to manage safety & operations performance are reported to have approximately 8 percent less unscheduled asset downtime (over those who do not), experience about 13 percent reduction in compliance-related costs, 8 percent fewer regulation citations, and realize operating margins 2 percent or greater than targeted in the corporate plan. Then, numerous benefits offered by gas detectors would augment the market demand during the forecast period.

North America is Expected to Hold Significant Share

- North America is witnessing the growth of gas detectors due to the presence of major vendors and government regulations regarding limiting gas emissions. In the North American region, the Environmental Protection Agency (EPA) and the U.S. Occupational Safety and Health Administration (OSHA) strictly implement industrial safety, driving the adoption of gas detectors.

- Almost all businesses in the United States are subject to OSHA standards, so they are a significant concern for employers and employees in various industries. The Environmental Protection Agency has released the New Source Performance Standards to measure and limit methane emissions from new, reconstructed, or modified assets.

- The EPA has also mandated the use of gas detectors in the mining industry. USA-based Carroll Technologies Group is a pioneer in offering handheld gas detectors for the mining industry. One of the products is the Mine Safety Appliances (MSA) Altair 4X Detector, which alerts the miner within 15 seconds of detection.

- Additionally, North America has one of the most active mining industries in the world. According to the Mining Association of Canada, Canada ranks among the top 5 members for the global production of 13 minerals and metals such as uranium, nickel, cobalt, potash, aluminum, diamonds, titanium, and gold. Further, according to the U.S. Geological Survey, in 2022, the capacity utilization of the United States' mining industry stood at an estimated 87 percent, which increased from 81 percent in 2021. Such instances are anticipated to offer lucrative opportunities for the growth of the studied market.

- The region is the primary hub for all the major manufacturing establishments worldwide. The regional authority further demands high safety concerns in countries such as the United States and Canada, which also encourages gas detectors to be deployed across the respective industries. Moreover, in October 2022, the United States Department of Labor's Mine Safety and Health Administration (MSHA) awarded USD 985,284 in grant funding to support safety courses and other programs.

Gas Detector Industry Overview

The gas detectors market is moderately competitive and consists of several major players. In terms of market share, few major players currently dominate the market. With a prominent share in the market, these major players are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market share and profitability. The competition, rapid technological advancements, and frequent changes in consumer preferences are expected to threaten the growth of companies during the forecast period.

In October 2022, Drager Marine & Offshore announced the release of the mobile gas detector, the X-am 2800. The new product simultaneously measured up to four different gases for application in confined spaces to safeguard employees working in areas at risk of explosive atmospheres, oxygen depletion, or those where toxic substances may be present.

In October 2022, Blackline Safety Corporation announced a preview of its new G6 single gas detector at the 2022 Abu Dhabi International Petroleum Exhibition and Conference. As per the company, ADIPEC is an opportunity for distributors, customers, media, and analysts in the Middle East to get a first look at this trailblazing connected safety innovation for petrochemical, oil and gas, and other industrial workplaces.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Assessment of the Impact of COVID-19

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Awareness about Hazards across Major Industries

- 5.1.2 Stringent Government Regulations for Safety of Workers

- 5.1.3 Companies Focusing on Smart Detectors

- 5.2 Market Restraints

- 5.2.1 Intense Competition in the Market

6 MARKET SEGMENTATION

- 6.1 By Communication Type

- 6.1.1 Wired

- 6.1.2 Wireless

- 6.2 By Type of Detector

- 6.2.1 Fixed

- 6.2.2 Portable and Transportable

- 6.3 By End-User Industry

- 6.3.1 Oil and Gas

- 6.3.2 Chemicals and Petrochemicals

- 6.3.3 Water and Wastewater

- 6.3.4 Metal and Mining

- 6.3.5 Utilities

- 6.3.6 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 Dragerwerk AG & Co. KGaA

- 7.1.3 MSA Safety Inc.

- 7.1.4 Emerson Electric Company

- 7.1.5 SENSIT Technologies, LLC

- 7.1.6 Industrial Scientific Corporatioh

- 7.1.7 New Cosmos Electric Co. Ltd

- 7.1.8 Trolex Ltd

- 7.1.9 Crowncon Detection Instruments Limited

- 7.1.10 Hanwei Electronics Group Corporation

- 7.1.11 International Gas Detectors Ltd

- 7.1.12 Sensidyne LP

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

气体分析仪:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

气体分析仪:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 雷射气体分析仪:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

雷射气体分析仪:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 2024-2032 年按应用(石油和天然气、电力、化学品、食品和饮料、製药等)和地区分類的气体分析仪市场报告

2024-2032 年按应用(石油和天然气、电力、化学品、食品和饮料、製药等)和地区分類的气体分析仪市场报告 定置型气体分析仪市场报告:2030 年趋势、预测与竞争分析

定置型气体分析仪市场报告:2030 年趋势、预测与竞争分析 溶解气体分析仪市场:依气体类型、产品类型、萃取类型、技术、额定功率输出划分 - 2024-2030 年全球预测

溶解气体分析仪市场:依气体类型、产品类型、萃取类型、技术、额定功率输出划分 - 2024-2030 年全球预测 气体分析仪、感测器、检测器市场:按技术、最终用户、安装位置划分 - 全球预测 2024-2030 年

气体分析仪、感测器、检测器市场:按技术、最终用户、安装位置划分 - 全球预测 2024-2030 年 到 2030 年半导体雷射气体分析仪的全球市场预测:按类型、应用、最终用户和地区分類的全球分析

到 2030 年半导体雷射气体分析仪的全球市场预测:按类型、应用、最终用户和地区分類的全球分析 碳氢化合物气体分析仪系统市场规模 - 按技术(电化学、顺磁、氧化锆 (ZR)、非分散红外线 (NDIR))和预测,2023 - 2032 年

碳氢化合物气体分析仪系统市场规模 - 按技术(电化学、顺磁、氧化锆 (ZR)、非分散红外线 (NDIR))和预测,2023 - 2032 年 TDLAS气体分析仪的全球市场:~2029年

TDLAS气体分析仪的全球市场:~2029年 溶解气体分析仪市场规模、份额、趋势分析报告:按萃取类型、额定功率输出、分析类型、地区、细分市场预测,2023-2030 年

溶解气体分析仪市场规模、份额、趋势分析报告:按萃取类型、额定功率输出、分析类型、地区、细分市场预测,2023-2030 年