|

市场调查报告书

商品编码

1850282

全球分散式天线系统市场:市场份额分析、产业趋势、统计数据和成长预测(2025-2030 年)Global Distributed Antenna Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

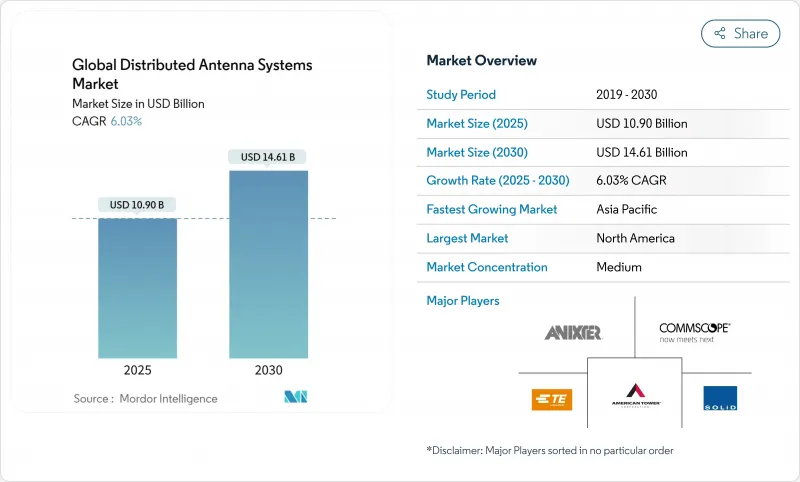

全球分散式天线系统市场预计到 2025 年将达到 109 亿美元,到 2030 年将达到 146.1 亿美元,在预测期(2025-2030 年)内复合年增长率为 6.03%。

分散式天线系统(DAS)市场预计在2025年达到109亿美元,到2030年达到146.1亿美元,预测期间内复合年增长率(CAGR)为6.03%。随着5G网路密集化暴露室内覆盖盲区,以及中立主机经营模式降低场馆所有者的资本负担,市场需求正在加速成长。被动式架构继续主导对成本敏感的部署,而公共无线电覆盖的监管要求则确保了支出週期在经济波动期间的稳定性。基于人工智慧的自优化网路正开始降低营运成本,而数位DAS设计正在降低能耗,并符合企业日益增长的永续性目标。

全球分散式天线系统市场趋势与洞察

5G网路密集化将提升对室内覆盖的需求

行动数据使用模式证实,超过 80% 的流量发生在室内,然而,为高容量 5G 基地台提供支援的中频段和毫米波讯号在建筑物内会迅速衰减。为了保持服务质量,像 Verizon 这样的通讯业者正在将固定无线服务与毫米波分散式天线系统 (DAS) 部署相结合。如今,场馆业主将房产估值与室内网路连接的保障挂钩,这迫使即使在对成本高度敏感的商业房地产领域,也必须做出投资决策。

建筑物内公共覆盖范围的监管要求

以国际消防规范为蓝本的建筑规范要求整个设施的讯号覆盖率达到95%,关键区域(例如楼梯间)的覆盖率达到99%,这使得公共分散式天线系统(DAS)成为一项不可或缺的需求。根据美国国家消防协会(NFPA)的规定,年度重新认证也为DAS带来了定期服务收入。如今,医院和交通枢纽也强制安装公共DAS,使其成为基本的建筑基础设施,而非可选项。

多运营商协调和频谱清理的复杂性

需要满足四家或更多行动网路营运商需求的部署项目,可能会因相关人员协调设计、讯号源和频率许可等事宜而停滞 6 至 12 个月。数位 DAS 平台透过提供软体定义的灵活性来减轻这种负担,而提供端到端解决方案的中立主机整合商通常能够为业主承担复杂的部署工作,从而加快部署速度。

细分市场分析

到2024年,被动式架构将占据分散式天线系统(DAS)市场63%的份额,吸引那些优先考虑低安装成本和简化维护的中型场馆业主。这些系统透过同轴电缆和分路器传输射频讯号,无需笨重的主动电子设备,从而降低了功耗。混合式DAS结合了回程传输和被动式分配,预计将以9.06%的复合年增长率增长,因为酒店和学术园区需要在性能和预算限制之间取得平衡。主动式DAS在大型体育场馆和机场仍将发挥重要作用,因为在这些场所,全面覆盖和高容量比成本更为重要;而数位DAS因其软体定义的灵活性而日益受到青睐,未来可支援多家营运商。

融合的技术蓝图正在模糊传统类别之间的界限。康宁的 Everon 5G 企业无线存取网整合了小型基地台无线电和 DAS 前端,与传统系统相比,安装时间缩短了 75%,整体拥有成本降低了 50%。供应商强调节能和模组化扩展性,下一代平台旨在满足效能和永续性要求,同时避免将买家锁定在固定的拓扑结构中。

区域分析

预计到2024年,北美将以39%的市占率引领分散式天线系统市场。国际消防规范和美国国家消防协会标准中规定的要求,使其市场需求强劲,不受宏观经济週期的影响。美国通讯业者正大力依赖毫米波小型基地台和分散式天线系统来补充宏观网路的密集化部署,而业主也越来越倾向于选择中立主机平台,因为这些平台既能提供更佳的覆盖范围,又能降低前期成本。

随着老旧办公大楼为满足不断变化的建筑规范和永续性目标而进行翻新,欧洲对维修的需求持续增长。英国和德国已出现多运营商之间复杂谈判的早期案例,这往往导致部署週期较长,但也为能够简化核准的整合商提供了有利条件。同时,法国和西班牙政府支持的宽频政策正将补贴用于数位基础设施建设,为交通枢纽和医疗园区等地的公私伙伴关係开发分散式天线系统(DAS)铺平了道路。

亚太地区是成长最快的地区,预计到2030年将以9.37%的复合年增长率成长,这主要得益于中国持续的都市化、日本高密度的交通系统以及印度对高端商业地产的追赶式投资。中国的部署与智慧城市计划相契合,这些计画将分散式天线系统(DAS)与物联网感测器骨干网相结合;而日本营运商则在大型体育赛事举办前优先考虑地铁站和购物中心的无缝连接。诸如日本的本地5G和印度的私人LTE牌照等频谱共用机制,反映了全部区域向成本优化的室内覆盖模式转变的趋势,并为中立主机实验提供了监管空间。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 5G网路密集化将增加对室内覆盖的需求

- 建筑物内公共方面的监管义务

- 中立房东经营模式可降低房东的资本支出。

- AI驱动的DAS自优化降低了网路营运成本

- 市场限制

- 多运营商协调和频谱清理的复杂性

- 能源密集型系统面临的永续性压力

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 积极的

- 被动的

- 数位的

- 杂交种

- 最终用户

- 製造业

- 卫生保健

- 政府和公共

- 运输/物流

- 体育和娱乐场所

- 通讯业者

- 其他商业领域

- 透过使用

- 企业DAS

- 公共DAS

- 中立主机/多运营商分散式天线系统

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- CommScope Holding Company Inc.

- Corning Incorporated

- ATandT Inc.

- American Tower Corporation

- Cobham Limited

- SOLiD Inc.

- TE Connectivity Ltd.

- Comba Telecom Systems Holdings Ltd.

- Boingo Wireless Inc.

- JMA Wireless

- Dali Wireless Inc.

- Zinwave(Wilson Electronics)

- Nokia Corporation

- Ericsson AB

- Huawei Technologies Co. Ltd.

- Radio Frequency Systems(RFS)

- Advanced RF Technologies(ADRF)Inc.

- PBE Axell Wireless

- Maven Wireless Sweden AB

- Baicells Technologies Co. Ltd.

- Tower Bersama Group

- Anixter International Inc.(Wesco)

- Amphenol Corporation

- Antenna Products Corporation

第七章 市场机会与未来展望

The Global Distributed Antenna Systems Market size is estimated at USD 10.90 billion in 2025, and is expected to reach USD 14.61 billion by 2030, at a CAGR of 6.03% during the forecast period (2025-2030).

The distributed antenna systems market size stands at USD 10.90 billion in 2025 and is forecast to reach USD 14.61 billion by 2030, reflecting a 6.03% CAGR over the period. Demand is accelerating as 5G densification exposes indoor coverage gaps, while neutral-host business models ease capital burdens for venue owners. Passive architecture continues to dominate cost-sensitive deployments, and regulatory mandates for public-safety radio coverage keep the spending cycle resilient during economic swings. Artificial-intelligence-based self-optimizing networks are beginning to trim operating costs, and digital DAS designs are tempering energy draw, aligning deployments with rising corporate sustainability goals.

Global Distributed Antenna Systems Market Trends and Insights

5G Network Densification Boosting Indoor-Coverage Demand

Mobile data-use patterns confirm that more than 80% of traffic originates indoors, yet the same mid-band and millimeter-wave signals powering high-capacity 5G cells attenuate quickly inside buildings. These physics trigger urgent demand for in-building infrastructure, leading carriers such as Verizon to pair fixed-wireless offerings with millimeter-wave DAS rollouts to sustain service quality. Venue owners now link property valuations to guaranteed indoor connectivity, compelling investment decisions even in cost-sensitive commercial real-estate segments.

Regulatory Mandates for In-Building Public-Safety Coverage

Building codes modeled on the International Fire Code require 95% signal coverage throughout facilities and 99% in critical zones such as stairwells, creating non-discretionary demand for public-safety DAS. Annual recertification under National Fire Protection Association rules adds a recurring-services layer to revenue streams. As mandates spread to hospitals and transit hubs, public-safety DAS is becoming baseline building infrastructure rather than an optional amenity.

Multi-Operator Coordination & Spectrum-Clearance Complexity

Deployments that must satisfy four or more mobile network operators can stall for 6-12 months while parties align on design, signal sources, and frequency clearance. Digital DAS platforms lighten this burden by offering software-defined flexibility, but neutral-host integrators who broker end-to-end solutions frequently expedite rollouts by absorbing the complexity on behalf of property owners.

Other drivers and restraints analyzed in the detailed report include:

- Neutral-Host Business Models Lowering Property-Owner CAPEX

- AI-Driven DAS Self-Optimisation Lowers Network OPEX

- Sustainability Pressure on Energy-Intensive Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passive architectures captured a 63% distributed antenna systems market share in 2024, appealing to owners of mid-sized venues who prioritize low installation cost and simple maintenance. These systems route RF over coaxial cables and splitters, eliminating the need for extensive active electronics and thereby shrinking power requirements. Hybrid DAS, combining fiber backhaul and passive distribution, is forecast to grow at a 9.06% CAGR as it balances performance and budget constraints in hospitality properties and academic campuses. Active DAS retains its role in large stadiums and airports where blanket coverage and high capacity override cost concerns, while digital DAS gains traction for its software-defined flexibility that future-proofs multi-operator support.

Converging technology roadmaps blur historical boundaries among categories. Corning's Everon 5G Enterprise Radio Access Network integrates small-cell radios with DAS head-ends, trimming installation time 75% and ownership costs 50% compared with earlier systems. Vendors increasingly highlight energy savings and modular scalability, positioning next-generation platforms to satisfy both performance and sustainability requirements without locking buyers into fixed topologies.

Global Distributed Antenna Systems Market Report is Segmented by Type (Active, Passive, and More), End-User (Manufacturing, Healthcare, Government and Public Safety, Transportation and Logistics, Sports and Entertainment Venues, and More), Application (Enterprise DAS, Public Safety DAS, Neutral-Host / Multi-Operator DAS), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with a 39% distributed antenna systems market share in 2024, propelled by strict public-safety codes and rapid 5G rollouts. Requirements embedded in the International Fire Code and National Fire Protection Association standards create mandatory demand regardless of macroeconomic cycles. Carriers in the United States lean heavily on millimeter-wave small cells and DAS to complement macro densification, and property owners increasingly prefer neutral-host platforms that cap upfront costs while enhancing coverage.

Europe exhibits steady replacement demand as older office stock undergoes retrofit to meet revised building codes and sustainability targets. Both the United Kingdom and Germany extend early examples of multi-operator negotiation complexity, often lengthening deployment timelines but providing fertile ground for integrators able to streamline approvals. Meanwhile, government-backed broadband agendas in France and Spain channel grants toward digital infrastructure, carving a path for public-private DAS partnerships in transport hubs and healthcare campuses.

Asia-Pacific is the fastest-growing region at a 9.37% CAGR through 2030, buoyed by China's ongoing urbanization, Japan's high-density transit systems, and India's catch-up investments in premium commercial real estate. Chinese deployments align with smart-city projects that merge DAS with IoT sensor backbones, while Japanese operators prioritize seamless connectivity in metro stations and commercial complexes ahead of large sporting events. Spectrum-sharing mechanisms such as Japan's local 5G and India's private LTE licenses provide the regulatory runway for neutral-host experiments, reflecting a broader shift toward cost-optimized indoor coverage models across the region.

- CommScope Holding Company Inc.

- Corning Incorporated

- ATandT Inc.

- American Tower Corporation

- Cobham Limited

- SOLiD Inc.

- TE Connectivity Ltd.

- Comba Telecom Systems Holdings Ltd.

- Boingo Wireless Inc.

- JMA Wireless

- Dali Wireless Inc.

- Zinwave (Wilson Electronics)

- Nokia Corporation

- Ericsson AB

- Huawei Technologies Co. Ltd.

- Radio Frequency Systems (RFS)

- Advanced RF Technologies (ADRF) Inc.

- PBE Axell Wireless

- Maven Wireless Sweden AB

- Baicells Technologies Co. Ltd.

- Tower Bersama Group

- Anixter International Inc. (Wesco)

- Amphenol Corporation

- Antenna Products Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G network densification boosting indoor-coverage demand

- 4.2.2 Regulatory mandates for in-building public-safety coverage

- 4.2.3 Neutral-host business models lowering property-owner CAPEX

- 4.2.4 AI-driven DAS self-optimisation lowers network OPEX

- 4.3 Market Restraints

- 4.3.1 Multi-operator coordination and spectrum-clearance complexity

- 4.3.2 Sustainability pressure on energy-intensive systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Active

- 5.1.2 Passive

- 5.1.3 Digital

- 5.1.4 Hybrid

- 5.2 By End-User

- 5.2.1 Manufacturing

- 5.2.2 Healthcare

- 5.2.3 Government and Public Safety

- 5.2.4 Transportation and Logistics

- 5.2.5 Sports and Entertainment Venues

- 5.2.6 Telecommunications Operators

- 5.2.7 Other Commercial Sectors

- 5.3 By Application

- 5.3.1 Enterprise DAS

- 5.3.2 Public Safety DAS

- 5.3.3 Neutral-Host / Multi-Operator DAS

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CommScope Holding Company Inc.

- 6.4.2 Corning Incorporated

- 6.4.3 ATandT Inc.

- 6.4.4 American Tower Corporation

- 6.4.5 Cobham Limited

- 6.4.6 SOLiD Inc.

- 6.4.7 TE Connectivity Ltd.

- 6.4.8 Comba Telecom Systems Holdings Ltd.

- 6.4.9 Boingo Wireless Inc.

- 6.4.10 JMA Wireless

- 6.4.11 Dali Wireless Inc.

- 6.4.12 Zinwave (Wilson Electronics)

- 6.4.13 Nokia Corporation

- 6.4.14 Ericsson AB

- 6.4.15 Huawei Technologies Co. Ltd.

- 6.4.16 Radio Frequency Systems (RFS)

- 6.4.17 Advanced RF Technologies (ADRF) Inc.

- 6.4.18 PBE Axell Wireless

- 6.4.19 Maven Wireless Sweden AB

- 6.4.20 Baicells Technologies Co. Ltd.

- 6.4.21 Tower Bersama Group

- 6.4.22 Anixter International Inc. (Wesco)

- 6.4.23 Amphenol Corporation

- 6.4.24 Antenna Products Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

室内分散式天线系统市场:按组件、系统类型、技术、频段、应用和最终用户划分-2026-2032年全球市场预测

室内分散式天线系统市场:按组件、系统类型、技术、频段、应用和最终用户划分-2026-2032年全球市场预测 分散式天线系统市场报告:按产品、系统类型、覆盖范围、技术、最终用途和地区划分(2026-2034 年)室内分散式基地台市场:依产品类型、技术、频段、组件、安装类型和最终用户划分,全球预测,2026-2032年

分散式天线系统市场报告:按产品、系统类型、覆盖范围、技术、最终用途和地区划分(2026-2034 年)室内分散式基地台市场:依产品类型、技术、频段、组件、安装类型和最终用户划分,全球预测,2026-2032年 分散式天线系统 (DAS) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、安装类型和解决方案划分

分散式天线系统 (DAS) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、安装类型和解决方案划分 分散式天线系统市场:机会、成长要素、产业趋势分析及2026年至2035年预测

分散式天线系统市场:机会、成长要素、产业趋势分析及2026年至2035年预测 全球分散式天线系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球分散式天线系统市场规模、份额、趋势和成长分析报告(2026-2034年) 分散式天线系统市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、应用、地区和竞争格局划分,2021-2031年室内分散式天线系统市场-全球产业规模、份额、趋势、机会、预测:按组件、类型、应用、地区和竞争格局划分,2021-2031年主动式分散式天线系统市场:按组件、技术、安装类型、频宽和最终用户划分,全球预测(2026-2032年)

分散式天线系统市场-全球产业规模、份额、趋势、机会、预测:按类型、最终用户、应用、地区和竞争格局划分,2021-2031年室内分散式天线系统市场-全球产业规模、份额、趋势、机会、预测:按组件、类型、应用、地区和竞争格局划分,2021-2031年主动式分散式天线系统市场:按组件、技术、安装类型、频宽和最终用户划分,全球预测(2026-2032年) 美国分散式天线系统市场:市场规模、份额、趋势分析(按接收区域、所有权类型、讯号源和应用划分)、细分市场预测(2025-2030 年)

美国分散式天线系统市场:市场规模、份额、趋势分析(按接收区域、所有权类型、讯号源和应用划分)、细分市场预测(2025-2030 年)