|

市场调查报告书

商品编码

1404381

针状焦:市场占有率分析、产业趋势与统计、2024年至2029年成长预测Needle Coke - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

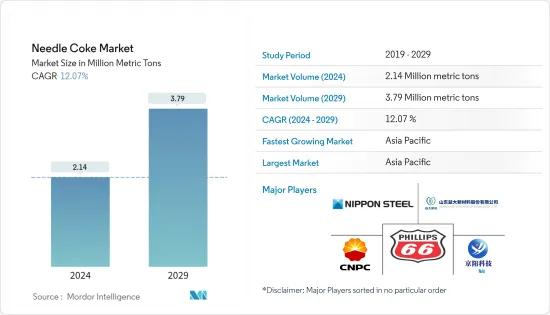

2024年针状焦市场规模预估为214万吨,预估2029年将达379万吨,预测期(2024-2029年)复合年增长率为12.07%。

COVID-19 大流行对针状焦市场产生了负面影响。疫情期间,钢厂需求减少显着影响石墨电极生产,针状焦消耗量减少。自2020年以来,由于石墨电极的持续生产,市场稳步扩大。

主要亮点

- 短期来看,电弧炉钢铁製造投资的增加以及政府增加废钢消费的政策是市场成长的主要动力。

- 另一方面,与石油焦相关的健康危害正在阻碍针状(石油基)焦市场的成长。

- 在预测期内,全球锂离子电池产量的成长可能会为受访市场带来机会。

- 亚太地区主导市场,预计在预测期内复合年增长率最高。

针状焦市场趋势

石墨电极占据市场主导地位

- 针状焦是由煤焦油和石油生产的优质碳原料。一种高品位、高价值的石油焦,用于生产钢铁工业电弧炉的热膨胀係数 (CTE) 极低的石墨电极。

- 石墨电极主要用于电炉炼钢、合金钢、各种合金、非金属熔炼等。此外,石墨具有高导热性,并且非常耐热和耐衝击。它还具有低电阻,这对于承载熔化铁所需的大电流是必需的。这使其能够保持 EAF(电炉)产生的极高水平的热量。

- 粗钢和铝产量的增加预计将推动石墨电极的使用并推动针状焦的需求。然而,这些金属的生产趋势预计将不规则,并为市场需求带来不确定性。

- 2023年4月,世界钢铁协会发布了2023年和2024年钢铁需求短期展望(SRO)预测,显示2023年钢铁需求将恢復2.3%,达到1,822.3吨,2024年将增长1.7%。预计将达到1,854.0 Mt 。此外,2022年全球粗钢产量将为1,878.5吨,与前一年同期比较下降4.2%。

- 中国是最大的石墨电极生产国。中国石墨电极产量占全球60%以上。此外,中国也是石墨电极最大的消费国,因为它拥有最大的钢铁工业。过去几年,石墨电极的价格大幅上涨。

- 根据国际回收局统计,中国钢铁製造过程中约有2.262亿吨废钢被用于回收。此外,中国废铁供应量的增加显示石墨电极生产中使用的针状焦消费量增加。

- 美国钢铁公司已开始寻找新的电炉 (EAF)位置来生产高级钢,耗资约 30 亿美元。预计这一趋势将支撑受访市场。

- 不过,欧洲钢铁协会(EUROFER)调整了消费量的预测。与2022年2月预测的地区金属消费量成长3.2%相比,该协会预计将下降约1.9%。

- 国际铝业协会的数据显示,2022年全球铝产量仅成长2.0%,低于2021年的2.7%,是2019年以来最慢的成长速度。

- 上述因素可能会影响预测期内石墨电极应用的针状焦需求。

亚太地区主导市场

- 亚太地区预计将主导针状焦市场,因为该地区包括中国(最大的针状焦生产国和消费国)和日本等国家。

- 中国石墨电极消费量和产能占据全球最大份额,展现了中国钢铁生产的潜力。目前,中国有40多家官方石墨电极製造商,过去几年,已有30家新公司进入市场,与电极一起,其他耐火材料产品也加入了市场。

- 除此之外,中国政府也致力于发展环保钢铁生产方式。数十万吨容量的新电弧炉已经在准备中。

- 日本是石油、煤炭和焦油针状焦的主要生产国和出口国之一。日本公司是世界上最大的石墨电极生产商之一。石墨电极的市场领导者包括 Showa Denko、Nippon Carbon、SEC Carbon 和 Tokai Carbon。

- 日本的 UPS 需求是由资料中心对评级电源的需求不断增长以及国内技术发展的不断增长所推动的。对用于储存太阳能的重力储能电池的需求不断增加预计将推动国内锂离子电池市场。

- 2022年3月,松下公司宣布有意在其和歌山工厂投资建立一家工厂,专门为电动车市场生产新型4,680锂离子电池。该工厂计划于 2024 年 3 月开始生产。

- 印度是世界第二大钢铁生产国。根据世界钢铁协会的资料,2022年印度粗钢产量增加约5.80%,达到1.244亿吨,而2021年为1.182亿吨。该国每年约占全球钢铁产量的4.8%。

- 2022年11月,HEG Ltd宣布未来三年将在印度建立一座新的锂离子电池石墨电极製造厂。

- 因此,由于上述方面,亚太地区预计将主导全球市场。

针状焦产业概况

针状焦市场具有综合性。市场主要企业(排名不分先后)包括菲利普斯66公司、辽宁宝莱生物能源公司、中国石油天然气集团公司(中石油)、山东亿达融通贸易有限公司和山东景阳科技有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 加大对电炉钢生产的投资

- 政府政策增加废铁消耗

- 抑制因素

- 与石油焦相关的健康危害

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 价格走势分析

第五章市场区隔

- 依产品类型

- 石油基

- 煤焦油沥青基质

- 按用途

- 石墨电极

- 锂离子电池

- 其他的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太地区其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太地区

第六章竞争形势

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Baosteel Group

- China National Petroleum Corporation(CNPC)

- Indian Oil Corporation

- Liaoning Baolai Bioenergy Co. Ltd

- Mitsubishi Chemical Corporation

- Nippon Steel Corporation

- Phillips 66

- POSCO MC Materials

- Seadrift Coke LP(Graftech International Ltd)

- Shandong DongYang Technology Co. Ltd

- Shandong Yida Rongtong Trading Co.

- Shanxi Hongte Coal Chemical Co. Ltd

- China Petroleum & Chemical Corporation(SINOPEC)

第七章 市场机会及未来趋势

- 锂离子电池提振针状焦需求

The Needle Coke Market size is estimated at 2.14 Million metric tons in 2024, and is expected to reach 3.79 Million metric tons by 2029, growing at a CAGR of 12.07% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the needle coke market. During the pandemic, the manufacturing of graphite electrodes was heavily impacted due to less demand from the steel manufacturing plants, which reduced the consumption of needle coke. After 2020, the market expanded steadily because of the continuous manufacturing of graphite electrodes.

Key Highlights

- Over the short term, the major factors driving the growth of the market studied are the increasing investments in EAF steel manufacturing and the government policies to increase scrap steel consumption.

- On the flip side, health hazards associated with petroleum coke act as a roadblock to the growth of the needled (petroleum-based) coke market.

- An increase in lithium-ion battery production globally is likely to act as an opportunity for the market studied during the forecast period.

- Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Needle Coke Market Trends

Graphite Electrodes Segment to Dominate the Market

- Needle coke is a high-quality carbon raw material that is produced from coal tar and petroleum. It is a premium grade, high-value petroleum coke used in the manufacturing of graphite electrodes of very low coefficient of thermal expansion (CTE) for the electric arc furnaces in the steel industry.

- The graphite electrodes are primarily used in electric arc furnace steel manufacturing, alloy steel, various alloys, and nonmetals melting. Furthermore, graphite has high thermal conductivity and is very resistant to heat and impact. It also has low electrical resistance, which is needed to conduct the large electrical currents necessary to melt iron. Thus, it can sustain sustaining the extremely high levels of heat generated in EAF (Electric Arc Furnace).

- The increase in crude steel and aluminum production is expected to drive the usage of graphite electrodes, which in turn is expected to favor the demand for needle coke. However, irregular trends in the production of these metals are expected to cause uncertainty in market demand.

- In April 2023, the World Steel Association released its Short-Range Outlook (SRO) steel demand forecast for 2023 and 2024, which stated that the steel demand would see a 2.3% rebound to reach 1,822.3 Mt in 2023, and it is forecasted to grow by 1.7% in 2024 to reach 1,854.0 Mt. In addition, the total world crude steel production was 1,878.5 Mt in 2022, a 4.2% decrease as compared to the value in the previous year.

- China is the largest producer of graphite electrodes. The country accounted for more than 60% of the global graphite electrode production. Furthermore, owing to the largest steel industry, China is also the largest consumer of graphite electrodes. Over the past few years, graphite electrodes witnessed a significant rise in prices.

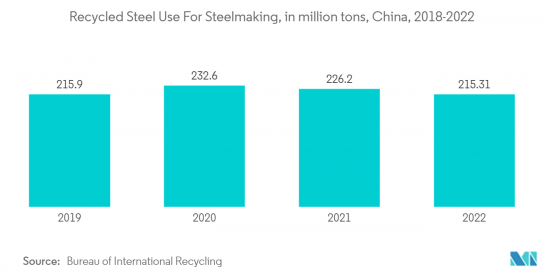

- According to the Bureau of International Recycling, in China, approximately 226.2 million tons of steel scrap were used for recycling purposes for the steel manufacturing process. In addition, the rising availability of steel scrap in China shows the increasing consumption of needle coke used for graphite electrode manufacturing.

- United States Steel Corporation has started to explore new locations for electric arc furnaces (EAF) to produce advanced grades of steel, which will cost approximately USD 3 billion. This trend is expected to support the studied market.

- However, the European Steel Association (EUROFER) has adjusted its forecast for the consumption of steel products in the European Union in 2022. In comparison to the February 2022 forecast and the expectation of regional metal consumption growth of 3.2%, there is a decline of around 1.9% expected by the association.

- According to the International Aluminum Institute, global aluminum production rose by a marginal 2.0% in 2022 compared to a growth rate that was down from 2.7% in 2021 and the slowest since 2019.

- The above-mentioned factors are likely to affect the demand for needle coke for graphite electrode application during the forecast period.

Asia Pacific region to Dominate the Market

- The Asia-Pacific region is expected to dominate the needle coke market as the region has countries such as China (the biggest producer and consumer of needle coke) and Japan.

- China holds the largest share in terms of consumption and production capacity of graphite electrodes in the global scenario, thus presenting the scope for steel production in the country. At present, there are more than 40 official graphite electrode producers in China, with 30 new entrants that have made other refractory products, along with electrodes, added to the market in the past 2-3 years.

- In addition to this, the Chinese government is also focusing on developing eco-friendly means of producing steel. Several hundred thousand metric tons of new capacity electric arc furnace is already in the pipeline.

- Japan is one of the leading producers and exporters of petroleum, coal, and tar-based pitch needle coke. Japanese companies are one of the largest producers of graphite electrodes in the world. The market giants of graphite electrodes include Showa Denko, Nippon Carbon, SEC Carbon, and Tokai Carbon.

- Japan UPS demand is fueled by the rising demand for high-rated power supply from data centers, coupled with rising technological developments in the country. The increase in demand for heavy-energy storage batteries to store solar power is expected to drive the market for lithium-ion batteries in the country.

- In March 2022, Panasonic Corporation announced its intention to invest in the establishment of a facility at its Wkayama Factory, which will be dedicated to the manufacturing of the new '4680' lithium-ion batteries for the electric vehicle market. The production at the planned facility is slated to begin by March 2024.

- India is the second-largest producer of steel globally. According to World Steel Association data, the crude steel production in India rose by around 5.80% to 124.4 million tons (MT) in 2022, as compared to 118.2 MT in 2021. The country accounts for around 4.8% of the global production of steel every year.

- In November 2022, HEG Ltd announced that it set up a new manufacturing facility for a graphite electrode for lithium-ion batteries in the next three years in India.

- Hence, the Asia-Pacific region is expected to dominate the global market based on the above mentioned aspects.

Needle Coke Industry Overview

The needle coke market is consolidated in nature. Some of the major players in the market (not in any particular order) include Phillips 66 Company, Liaoning Baolai Bioenergy Co. Ltd, China National Petroleum Corporation (CNPC), Shandong Yida Rongtong Trading Co., and Shandong Jing Yang Technology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Investments in EAF Steel Manufacturing

- 4.1.2 Government Policies to Increase Scrap Steel Consumption

- 4.2 Restraints

- 4.2.1 Health Hazards Associated with Petroleum Coke

- 4.3 Industry Value-Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trend Analysis

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Petroleum Based

- 5.1.2 Coal-tar Pitch Based

- 5.2 By Application

- 5.2.1 Graphite Electrodes

- 5.2.2 Lithium-ion Battery

- 5.2.3 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Baosteel Group

- 6.4.2 China National Petroleum Corporation (CNPC)

- 6.4.3 Indian Oil Corporation

- 6.4.4 Liaoning Baolai Bioenergy Co. Ltd

- 6.4.5 Mitsubishi Chemical Corporation

- 6.4.6 Nippon Steel Corporation

- 6.4.7 Phillips 66

- 6.4.8 POSCO MC Materials

- 6.4.9 Seadrift Coke LP (Graftech International Ltd)

- 6.4.10 Shandong DongYang Technology Co. Ltd

- 6.4.11 Shandong Yida Rongtong Trading Co.

- 6.4.12 Shanxi Hongte Coal Chemical Co. Ltd

- 6.4.13 China Petroleum & Chemical Corporation (SINOPEC)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Lithium-ion Batteries to Boost the Demand for Needle Coke

全球针状焦市场:按应用、类型、等级、最终用途和国家进行分析 - 分析和预测(2023-2033)

全球针状焦市场:按应用、类型、等级、最终用途和国家进行分析 - 分析和预测(2023-2033) 2023-2028 年针状焦市场报告(按类型、等级、应用、最终用途行业和地区)

2023-2028 年针状焦市场报告(按类型、等级、应用、最终用途行业和地区) 针状焦市场:按类型、等级、用途和最终用途- 2023-2030 年全球预测

针状焦市场:按类型、等级、用途和最终用途- 2023-2030 年全球预测 针状焦市场 - 2023 年至 2028 年预测

针状焦市场 - 2023 年至 2028 年预测 针状焦市场:按产品类型、应用(石墨电极、锂离子电池等)、地区 - 规模、份额、展望、机会分析,2023-2030 年

针状焦市场:按产品类型、应用(石墨电极、锂离子电池等)、地区 - 规模、份额、展望、机会分析,2023-2030 年 全球针状焦市场 - 行业规模、份额、趋势、机会、2017-2027 年预测、按产品类型、按产品等级、按应用、按公司、按地区分析

全球针状焦市场 - 行业规模、份额、趋势、机会、2017-2027 年预测、按产品类型、按产品等级、按应用、按公司、按地区分析 针状焦市场:按类型(石油基、煤基)、应用(石墨电极、锂离子电池、特种碳材料、橡胶复合材料等)2021-2031全球机遇分析和行业预测

针状焦市场:按类型(石油基、煤基)、应用(石墨电极、锂离子电池、特种碳材料、橡胶复合材料等)2021-2031全球机遇分析和行业预测 针状焦的全球市场(2016年~2032年)

针状焦的全球市场(2016年~2032年) 全球及中国针状焦行业分析(2022-2027)

全球及中国针状焦行业分析(2022-2027)