|

市场调查报告书

商品编码

1641980

持续交付:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Continuous Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

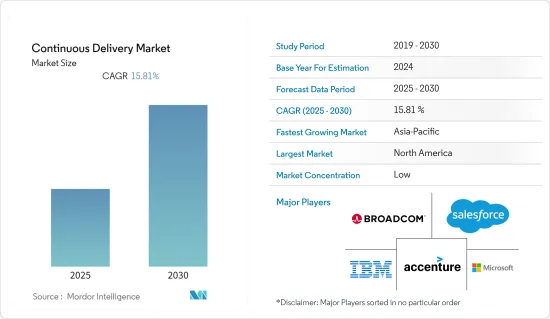

预测期内,持续交付市场预计将以 15.81% 的复合年增长率成长。

据美国软体开发公司 Perforce Software, Inc. 称,65% 的经理、软体开发人员和高阶主管报告称,他们的组织已经开始使用持续交付。

主要亮点

- 持续交付市场正在迅速扩张,主要受人工智慧 (AI) 和机器学习 (ML) 成长的推动。随着互联基础设施的快速部署和数位设备自主性的不断提高,人工智慧/机器学习技术正在改变软体开发过程。这些技术可以实现自我复製系统、自动化测试、预测部署结果、改进发布计划并提供智慧监控和警报。

- 此外,敏捷开发方法也越来越受到支持,因为它们能够更快、更灵活地交付软体。持续交付非常符合敏捷原则,以小增量而不是定期的大规模发布来更新软体。据澳洲软体公司 Atlassian Corporation 称,美国至少有 71% 的组织采用敏捷方法。此外,敏捷倡议的成功率为 64%,而瀑布计划的成功率为 49%。敏捷计划的成功率比瀑布计划高出 1.5 倍。

- 云端处理和基础设施即程式码的日益普及使得基础设施管理扩充性和适应性。持续交付使公司能够使用云端平台和基础设施即程式码工具在云端配置中快速部署和管理应用程式。持续交付 CI/CD 管道是一种自动化流程,使公司和组织能够快速可靠地建置、测试和部署软体。云端基础设施为运行这些流程提供了一个灵活、可扩展的平台,使企业能够适应不断变化的需求并优化资源使用。这些工具透过多种重要方式帮助组织实现更高的业务敏捷性:

- 然而,开放原始码持续交付计划和工具将主导商业持续交付工具领域,并推动服务持续交付市场的成长。持续交付市场正在帮助公司和企业改变其提供服务的方式,并以更高的准确性、成本节约和生产力来经营业务。它还会产生大量有用的信息,帮助您做出更好、更快的决策。这些资讯可以优化当前流程和操作,或预测何时、何地以及如何最好地提供产品和服务。

- 然而,由于公司不愿意接受改变并将新技术融入现有流程和工具链中,持续的市场扩张可能需要改进。许多企业需要支援以采用全自动化技术来使用 DevOps 和持续交付解决方案。

持续交付市场趋势

云端技术在持续交付市场的应用日益广泛

- 在云端上实施持续交付工具可提供高度的扩充性、灵活性以及以定义的权限共用的能力。那些建立持续交付工具的人正在抓住机会抢占市场份额。

- 持续交付工具提供 DevOps 功能,让团队在云端的一个地方协作、开发、测试、部署和管理软体。这使得最终用户可以访问云端上的任何内容并建立新的应用程式。

- 随着大多数企业将资料转移到云端,各行各业正在开发云端基础的解决方案并释放市场机会。预计这将推动未来几年的市场成长。

- 谷歌宣布推出 Cloud Build,这是一个完全託管的持续交付和整合平台,可协助企业快速大规模地建置、测试和部署软体。此外,企业对云端处理的投资不断增加,预计这将在未来几年推动市场成长。

- 例如,今年亚马逊公司的云端处理部门亚马逊网路服务(AWS)宣布了在印度进行重大投资的计画。该公司今年计划投资金额1.6 兆印度卢比(130 亿美元)。印度对云端服务的需求不断增长,推动了大规模投资。此项投资将主要用于扩大和加强 AWS 在全国范围内的云端基础设施。

- 公共云端使业务能够根据市场变化更快、更有效地适应和运作。该技术变得更容易使用。现在,我们可以用以前从未想像过的方式创造极具吸引力的消费者体验。

- 云端运算的采用促使人们和组织改变其行为,并使某些业务线能够透过克服技术限制来完成工作。云端趋势将影响组织如何规划投资、如何做出数位业务决策、如何选择供应商以及他们选择什么技术。

- 持续交付市场的一个突出趋势是发布管理、规划和发布自动化工具,这些工具使 DevOps 应用程式和工具能够促进软体部署到公共云端云和私有云端。例如,发布自动化工具可以让员工轻鬆设定部署配置模板,从而节省时间。

北美占据主要市场占有率

- 由于美国是云端基础技术和物联网的早期采用者,预计北美的需求将成长最高。然而,提高灵活性、敏捷性和实施新应用程式的能力等好处至关重要。

- 此外,北美的企业正在采用云端基础的应用程序,估计美国35% 的中小型企业已经采用云端解决方案。北美正在掀起一股併购热潮,以利用这个机会。例如,Steltix 与 Autodeploy 合作,将其持续部署和交付软体套件推向欧洲市场。

- 机器学习 (ML)、人工智慧 (AI)、预测分析和规范分析等新技术的兴起,以及这些新技术与持续交付模型、规则、自学、资料和推理引擎的集成,您的组织将能够运行得更顺畅。

- 这些投资的主要驱动力是新技术的不断发展,以利用以前被认为是非商业性的数量。由于这些投资,零售、医疗保健、通讯和製造应用预计将在北美占据相当大的市场占有率。

持续交付行业概览

持续交付市场是分散的。随着新技术的采用,许多参与者透过技术创新和市场发展进入市场,加剧了市场竞争。主要参与者包括 IBM 公司、微软公司、埃森哲公司、Salesforce Inc.、Wipro Limited、CA Technologies(博通公司)、XebiaLabs(DIGITAL.AI)、Electric Cloud Inc.(CloudBees Inc.)和 Red Hat Inc.。 Atlassian 等

2024 年 5 月 Octopus Deploy 是公认的持续交付 (CD) 行业标准,它宣布了旨在简化大型企业 Kubernetes CD 的功能。透过引入新的 Kubernetes 代理、容器镜像和 Helm 的外部馈送触发器,Octopus Deploy 可以轻鬆地大规模部署到 Kubernetes,从而无需复杂且昂贵的持续整合 (CI) 脚本。

2024 年 3 月,CircleCI 透过引入发布编配功能增强了其 CI/CD 平台,使开发人员能够更好地控制其应用程式部署。此附加功能使开发团队能够将其程式码的特定子集部署到生产中,并立即收到有关程式码执行情况的回馈。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 整个业务流程自动化的需求不断增加

- 云端技术的采用日益广泛

- 市场限制

- 维护资料安全和隐私

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响评估

第五章 市场区隔

- 依部署类型

- 云

- 本地

- 按组织规模

- 大型企业

- 中小企业

- 按最终用户产业

- BFSI

- 通讯和 IT

- 零售和消费品

- 医疗保健和生命科学

- 製造业

- 政府和国防

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- XebiaLabs(DIGITAL.AI)

- Broadcom Inc.(CA Technologie)

- IBM Corporation(Red Hata Inc.)

- Electric Cloud Inc.(CloudBees Inc.)

- Atlassian Corporation PLC

- Microsoft Corporation

- Accenture PLC

- Wipro Limited

- Salesforce Inc.

- Flexagon LLC

- Clarive Software Inc.

第七章投资分析

第 8 章:市场的未来

The Continuous Delivery Market is expected to register a CAGR of 15.81% during the forecast period.

According to Perforce Software, Inc., an American software developer, 65% of managers, software developers, and executives report that their organizations have started using continuous delivery.

Key Highlights

- The market for continuous delivery is expanding rapidly, owing primarily to the growth of artificial intelligence (AI) and machine learning (ML). AI/ML-powered technologies are transforming the software development process due to the rapid deployment of connected infrastructure and the rising autonomy of digital devices. These technologies enable self-regeneration systems, automate testing, forecast deployment results, improve release schedules, and provide smart monitoring and alarms.

- Moreover, Agile development approaches have grown in favor due to their ability to deliver software more quickly and flexibly. Continuous delivery aligns well with Agile principles, giving the software minor incremental updates rather than significant, periodic releases. According to Atlassian Corporation, an Australian software company, at least 71% of United States organizations use Agile. Further, Agile initiatives have a 64% success rate, while waterfall projects have a 49% success rate. Agile projects are 1.5X more successful than waterfall projects.

- The rising adoption of cloud computing and Infrastructure as Code has improved scaling and adaptability in infrastructure management. Continuous delivery swiftly allows enterprises to deploy and manage their applications in cloud configurations with cloud platforms and Infrastructure as Code tools. Continuous delivery CI/CD pipelines are automated processes enabling businesses and organizations to build, test, and deploy software quickly and reliably. Cloud infrastructure provides a flexible and scalable platform for running these processes, allowing companies to adapt to changing demands and optimize resource usage. These tools help organizations achieve greater business agility in several vital ways.

- However, open-source continuous delivery projects and tools are set to dominate the commercial straight delivery tools segment, driving the growth of the service steady delivery market. The constant delivery market helps businesses or enterprises change how they deliver services and run their businesses to be more accurate, save money, and be more productive. Also, it creates a lot of helpful information that helps people make better and faster decisions. This information can optimize current processes and operations or predict when, where, and how to offer the best products and services.

- However, the continuous market expansion may need to be improved due to businesses' reluctance to embrace change and integrate new technologies into their existing processes and toolchains. Many companies require support in adopting completely automated techniques for using DevOps and continuous delivery solutions.

Continuous Delivery Market Trends

Increasing Adoption of Cloud Technology in the Continuous Delivery Market

- Implementing continuous delivery tools on the cloud provides high scalability, flexibility, and sharing capabilities with defined authority. The people who make constant delivery tools are taking advantage of the chance to get a piece of the market.

- Continuous delivery tools provide DevOps capabilities that allow teams to collaborate, develop, test, deploy, and manage software on the cloud in one place. This helps end users access everything and build new applications on the cloud.

- Most companies are moving their data to the cloud, so industry players are developing cloud-based solutions to exploit the market opportunity. This is likely to boost market growth over the next few years.

- Google announced Cloud Build, which helps fully manage continuous delivery and integration platforms, helping build, test, and deploy software quickly and at scale. Also, companies are investing in cloud computing, which is expected to help the market grow over the next few years.

- For instance, in the current year, Amazon Web Services (AWS), a cloud computing division of Amazon.com Inc., has announced a significant investment plan for India. The company intends to invest a staggering INR 1.06 trillion (USD 13 billion) in the current year. The increasing demand for cloud services in India drives substantial financial commitment. The investment will primarily focus on expanding and strengthening AWS's cloud infrastructure nationwide.

- With the public cloud, businesses can make changes and run their operations more quickly and effectively in response to changes in the market. It improves the user-friendliness of technology. It has made building incredibly engaging consumer experiences in previously unthinkable ways possible.

- Due to cloud adoption, people and organizations have modified their behavior, and several business lines have gotten things done by getting past technological restrictions. Cloud trends affect how organizations plan to invest, how they make decisions about their digital businesses, how they choose vendors, and what technologies they choose.

- One of the prominent trends in the continuous delivery market is release management, planning, and release automation tools, which make it easier for DevOps applications and tools to deploy software to public or private clouds. Release automation tools, for example, can save time by making it easy for the staff to set up templates for deployment configurations.

North America to Occupy Significant Market Share

- The North American region is projected to have the most significant growth in demand due to the early adoption of cloud-based technologies and IoT by the United States. However, advantages such as increased flexibility and agility and the ability to implement new applications are essential.

- Additionally, companies are adopting cloud-based applications in the North American region, and it was estimated that nearly 35% of SMBs in the United States have already deployed cloud solutions. There have been a series of mergers, collaborations, and acquisitions in North America to take advantage of this opportunity. Steltix, for example, has collaborated with Autodeploy to bring a continuous deployment and delivery software suite to European markets.

- The rise of new technologies like machine learning (ML), artificial intelligence (AI), and predictive and prescriptive analytics, and integrating these new technologies with continuous delivery models, rules, self-learning, data sets, and inference engines will help organizations run more smoothly.

- The primary driver behind these investments has been the continuous evolution of new technologies to utilize previously considered non-commercial volumes. With these investments, North America's retail, healthcare, communications, and manufacturing applications are expected to hold a significant market share.

Continuous Delivery Industry Overview

The continuous delivery market is fragmented. With the adoption of new technologies, many players are entering the market with innovation and development, making the market competitive. Some of the key players include IBM Corporation, Microsoft Corporation, Accenture PLC, Salesforce Inc., Wipro Limited, CA Technologies (Broadcom Company), XebiaLabs (DIGITAL.AI), Electric Cloud Inc. (CloudBees Inc.), Red Hat Inc., and Atlassian, among others.

May 2024: Octopus Deploy, recognized as the industry standard for Continuous Delivery (CD), has unveiled features aimed at streamlining Kubernetes CD for large enterprises. With the introduction of a new Kubernetes agent and external feed triggers for container images and Helm, Octopus Deploy facilitates large-scale deployments to Kubernetes, doing away with the necessity for intricate and costly continuous integration (CI) scripts.

March 2024: CircleCI enhanced its CI/CD platform by introducing a release orchestration feature, empowering developers with greater control over application deployments. This addition allows development teams to deploy a specific subset of code to a live production environment, enabling them to receive immediate feedback on the code's performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Automation Across Business Processes

- 4.2.2 Increasing Adoption Of Cloud Technology

- 4.3 Market Restraints

- 4.3.1 Maintaining Data Security And Privacy

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 impact on the industry

5 MARKET SEGMENTATION

- 5.1 Deployment Type

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises

- 5.3 End User Industry

- 5.3.1 BFSI

- 5.3.2 Telecom and IT

- 5.3.3 Retail and Consumer Goods

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Manufacturing

- 5.3.6 Government and Defense

- 5.3.7 Other End User Industries

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Latin America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 XebiaLabs (DIGITAL.AI)

- 6.1.2 Broadcom Inc. (CA Technologie)

- 6.1.3 IBM Corporation (Red Hata Inc.)

- 6.1.4 Electric Cloud Inc. (CloudBees Inc.)

- 6.1.5 Atlassian Corporation PLC

- 6.1.6 Microsoft Corporation

- 6.1.7 Accenture PLC

- 6.1.8 Wipro Limited

- 6.1.9 Salesforce Inc.

- 6.1.10 Flexagon LLC

- 6.1.11 Clarive Software Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

2026年全球持续交付市场报告2026年全球持续整合工具市场报告

2026年全球持续交付市场报告2026年全球持续整合工具市场报告 持续整合工具市场 - 全球产业规模、份额、趋势、机会及预测(按部署模式、最终用户产业、组织规模、地区和竞争格局划分,2021-2031 年)

持续整合工具市场 - 全球产业规模、份额、趋势、机会及预测(按部署模式、最终用户产业、组织规模、地区和竞争格局划分,2021-2031 年) 持续交付市场规模、份额和成长分析(按部署类型、组件、组织规模、最终用户产业和地区划分)-2026-2033年产业预测

持续交付市场规模、份额和成长分析(按部署类型、组件、组织规模、最终用户产业和地区划分)-2026-2033年产业预测 持续整合工具市场预测至 2032 年:按组件、工具类型、部署模型、组织规模、应用、最终用户和地区进行的全球分析

持续整合工具市场预测至 2032 年:按组件、工具类型、部署模型、组织规模、应用、最终用户和地区进行的全球分析 持续整合工具:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

持续整合工具:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 持续整合工具市场报告:趋势、预测与竞争分析(至 2031 年)

持续整合工具市场报告:趋势、预测与竞争分析(至 2031 年) 持续交付市场、规模、占有率、趋势、行业分析报告:按部署、公司规模、最终用途、地区 - 市场预测,2024-2032 年

持续交付市场、规模、占有率、趋势、行业分析报告:按部署、公司规模、最终用途、地区 - 市场预测,2024-2032 年 持续交付市场规模、份额、趋势分析报告:按配置、按最终用途、按企业规模、按地区、细分市场预测,2024-2030 年

持续交付市场规模、份额、趋势分析报告:按配置、按最终用途、按企业规模、按地区、细分市场预测,2024-2030 年 2024 年至 2031 年持续整合工具市场类型、部署模式、组织规模与地区分布

2024 年至 2031 年持续整合工具市场类型、部署模式、组织规模与地区分布