|

市场调查报告书

商品编码

1404445

电脑辅助编码 -市场占有率分析、产业趋势与统计、2024-2029 年成长预测Computer-assisted Coding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

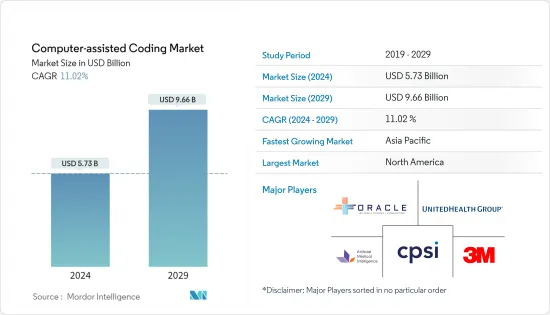

预计 2024 年电脑辅助编码市场规模为 57.3 亿美元,预计到 2029 年将达到 96.6 亿美元,在预测期内(2024-2029 年)复合年增长率为 11.02%。

主要亮点

- COVID-19大流行对电脑辅助编码 (CAC) 市场产生了重大影响。许多医疗机构已经实施了 CAC,使他们能够在大流行期间更准确地翻译患者资讯。

- 例如,2022 年 10 月在 PubMed 上发表的一项研究讨论了疾病管制与预防中心 (CDC) 于 2021 年 10 月引入新的诊断代码 (U09.9)。该代码可在国际疾病分类第 10 版临床修订版 (ICD-10-CM) 中找到,旨在识别 COVID-19 后的病理。在后 COVID-19 情况下,由于医院越来越多地采用编码系统以及医疗保健系统中数位健康解决方案的普及不断提高,预计市场将实现稳定增长。

- 推动市场成长的因素包括越来越多地采用电子健康记录(EHR) 系统、越来越多地使用电脑辅助编码 (CAC) 解决方案来控制急剧上升的医疗保健成本,以及不断提高的患者资料管理监管要求。

- 例如,根据欧盟委员会 2022 年 6 月的报告,欧盟委员会发布了关于欧洲电子健康记录交换标准的建议,该标准将实现医疗资料的跨境传输。这将透过支持欧盟 (EU) 国家的努力来实现,使居民能够从欧盟任何地方安全地存取和交换其健康资料。因此,此类与医疗进步相关的倡议预计将在预测期内推动市场成长。

- 此外,不断增加的软体发布和医疗编码的相关进步预计将在研究期间推动市场成长。例如,2022年10月,Nym为美国各地的放射科推出了放射编码解决方案。此次扩张将公司的自主医疗编码技术引入了第三个门诊专科,扩大了对公司领先业界的收益週期管理 (RCM) 解决方案的访问范围。此外,增加编码平台开发的研究经费预计将在预测期内推动市场成长。

- 例如,2022 年 11 月,主导的人工智慧医疗编码自动化平台 Fathom。在 B 轮资金筹措中筹集了 4,600 万美元,参与方包括他们利用资金来解决提供者面临的挑战并推进自动化医疗编码的标准。因此,透过此类研究,开发和推广编码平台的资金预计将在预测期内增加市场成长。

- 因此,由于政府实施数位医疗保健的措施以及主要企业增加的策略活动,预计所研究的市场在预测期内将出现显着的市场成长。然而,高昂的维护成本和缺乏熟练的系统支援专业人员正在限制市场的成长。

电脑辅助编码市场趋势

预计在预测期内,网路和云端基础的细分市场将占据主要市场占有率

- 基于 Web 的交付可以使用超文本传输协定 (HTTP)、传输控制协定 (TCP)、网际网路通讯协定 (IP) 或其他协定在不同的伺服器电脑上进行,并且可以透过网际网路、虚拟专用网路或无线方式进行交付。透过网路通讯的网路。基于网路的电脑辅助编码系统完全透过网路浏览器访问,不需要或在您的装置上安装任何软体。所有资料和软体均远端託管并透过网路存取。这是基于网路的电脑辅助编码系统的主要优点之一。

- 政府越来越多倡议实施电脑辅助编码、技术进步和开拓的医疗保健组织等因素正在推动这一市场的发展。例如,2023年3月,富士通宣布了一个新的云端基础的平台,允许用户安全地收集和利用健康相关资料,以推动医疗保健产业的数位转型。作为 Fujitsu Uvance 建立永续发展世界的「健康生活」目标的一部分,富士通持续推动健康社会的发展。

- 同样,2022 年 11 月,Google Cloud 宣布与 Hackensack Meridian Health、Lifepoint Health 等公司合作开发的三款新的健康资料引擎 (HDE) 加速器,以支持健康股权、患者流动、基于价值的帮助解决常见护理用例。

- 此外,各国政府正在采取措施支持医疗保健领域资讯科技的发展。例如,2021 年 2 月,作为英国主导采用完全连接、云端驱动的医疗保健服务计划的一部分,超过 200 万个 NHSmail 邮箱被迁移到 Microsoft Azure 云端的一部分 Exchange Online。这使得 NHS 组织和部门的工作人员之间的沟通更加顺畅和高效,并改善了资讯的获取。预计这将增加英国健康资讯科技 (HCIT) 变革管理服务的采用,从而推动该产业在研究期间的成长。

- 此外,该地区政府机构和市场参与企业的联合倡议也促进了市场成长。例如,2021 年 9 月,德国电信的 T-Systems 与 Google Cloud 合作,为德国企业、医疗保健公司和公众建置和提供主权云端服务。两家公司共同开发了下一代主权云端解决方案和基础设施。该公司计划在奥地利和瑞士建立类似的主权云。

- 因此,由于越来越多地采用基于云端/网路的医疗软体以及主要企业的策略活动增加,预计所研究的细分市场将在研究期间显着增长。

预计北美在预测期内将出现强劲成长

- 由于医院越来越多地采用数位医疗服务、主要企业增加策略活动以及北美医疗保健数位化投资的增加,预计北美电脑辅助编码市场将显着增长。

- 例如,Canada Health Infoway 于 2022 年 11 月进行的一项调查发现,94% 的加拿大人对访问数位医疗服务感兴趣。加拿大人还可以在线访问个人健康资讯,包括测试和诊断结果、免疫史和记录、当前用药清单和历史以及专家笔记和记录。因此,由于人们采用数位医疗服务,所研究的市场预计在预测期内将显着成长。

- 此外,北美地区主要企业电脑辅助编码的兴起预计将推动研究期间的市场成长。例如,2022年7月,医疗资讯科技服务供应商Greenway Health推出了Greenway医疗编码服务,这是一种针对门诊诊所的最先进的医疗解决方案。 Greenway Medical Coding 透过个体化编码团队的知识和准确性,帮助诊所实现成本效率、提高盈利并有效收集索赔。

- 同样,2022 年 9 月,即时临床文件、医疗编码和中期收益週期交付虚拟解决方案提供商 AQuity Solutions 收购了位于佛罗里达州坦帕的 Coding Services Group CSG 的所有资产。因此,主要企业的此类策略活动预计将增加对电脑辅助编码的需求并刺激整个北美市场的成长。

- 因此,由于医疗保健环境中数位医疗服务的日益采用以及北美主要企业的策略活动的增加,预计市场在预测期内将呈现显着增长。

电脑辅助编码产业概述

电脑辅助编码市场是一个适度分散且竞争激烈的市场。市场参与企业正专注于产品发布、合作伙伴关係和收购等策略活动,以增强其在全球的产品组合和影响力。市场参与企业包括Oracle、Computer Programs and Systems, Inc. (TruCode LLC)、United Health Group (Optum Inc.)、Artificial Medical Intelligence Inc. 和 3M。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 更多采用电子健康记录(EHR) 系统

- 更多地使用电脑辅助编码解决方案来遏制不断上涨的医疗成本

- 病患资料管理的监管要求提高

- 市场抑制因素

- 安装和维护成本高

- 缺乏现场支援和内部领域知识

- 波特五力分析

- 买家/消费者的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模-美元)

- 副产品

- 软体

- 独立软体

- 整合软体

- 按服务

- 软体

- 按规定型态

- 云端基础

- 本地

- 按用途

- 自动编码

- 管理报告和分析

- 临床编码审核

- 按最终用户

- 医院

- 临床检测/诊断中心

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 其他亚太地区

- 中东/非洲

- 海湾合作委员会国家

- 南非

- 其他中东/非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章竞争形势

- 公司简介

- 3M

- UnitedHealth Group(Optum Inc.)

- Nuance Communications Inc.

- Oracle

- Computer Programs and Systems, Inc.(TruCode LLC)

- Artificial Medical Intelligence Inc.

- Athenahealth Inc.

- Streamline Health Solutions Inc.

- Epic Systems Corporation

- ZyDoc Corporation

- Alpha II LLC

- AGS Health

第七章 市场机会及未来趋势

The Computer-assisted Coding Market size is estimated at USD 5.73 billion in 2024, and is expected to reach USD 9.66 billion by 2029, growing at a CAGR of 11.02% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic significantly impacted the computer-assisted coding (CAC) market since many healthcare organizations implemented CAC, which enabled the translation of patient information more accurately during the pandemic.

- For instance, a study published in October 2022 in PubMed discusses the introduction of a new diagnosis code (U09.9) by the Centers for Disease Control and Prevention (CDC) in October 2021. This code, found in the International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM), is designed for identifying cases of post-COVID-19 conditions. In the context of the post-COVID-19 situation, the market is anticipated to experience steady growth due to the heightened adoption of coding systems in hospitals and the increased prevalence of digital health solutions in healthcare systems.

- Some factors driving the market growth include increasing implementation of electronic health record (EHR) systems, increasing utilization of computer-assisted coding (CAC) solutions to curtail the rising healthcare costs, and increasing regulatory requirements for patient data management.

- For instance, according to the European Commission's June 2022 report, the European Commission issued a recommendation on a European electronic health record exchange standard to enable the transfer of health data across borders. It accomplishes this by supporting European Union (EU) nations in their initiatives to ensure that residents can safely access and exchange their health data from any location within the EU. Hence, such initiatives associated with the advancements in healthcare are anticipated to boost market growth over the forecast period.

- Furthermore, an increase in software launches and related advancements in medical coding is expected to fuel the market growth over the study period. For instance, in October 2022, Nym launched radiology coding solutions for radiology departments across the United States. This expansion offers the company's autonomous medical coding technology to a third outpatient specialty area, expanding access to the company's industry-leading solution for revenue cycle management (RCM). Moreover, an increase in research funding for the development of coding platforms is expected to drive market growth over the forecast period.

- For instance, in November 2022, Fathom, an AI-powered medical coding automation platform, raised USD 46 million in Series B funding co-led by Alkeon Capital and Lightspeed Venture Partners with participation from Vituity's Inflect Health, Cedars-Sinai, ApolloMD, Jonathan Bush, and other healthcare executives. They utilized the funding to advance the standard in automated medical coding in response to the challenges faced by the providers. Hence, owing to such research, funding to develop and promote coding platforms is expected to augment the market growth over the forecast period.

- Thus, owing to the government initiatives to implement digital health care and the rise in strategic activities by the key players, the studied market is expected to witness significant market growth over the forecast period. However, the high maintenance cost and lack of skilled professionals for system support have restrained market growth.

Computer-assisted Coding Market Trends

Web and Cloud Based Segment is Expected to Hold Significant Market Share Over the Forecast Period.

- Web-based delivery is a network that runs on different server computers and communicates by Internet, virtual private network, and the wireless network, using hypertext transfer protocol (HTTP), transmission control protocol (TCP), and internet protocol (IP) or other protocols. A web-based computer-assisted coding system is entirely accessed through a web browser, and no software is installed or required on the device at all. All data and software are hosted remotely and accessed through the Internet. This is one of the main advantages of the web-based computer-assisted coding system.

- The factors, such as increasing initiatives taken by the government for the adoption of computer-assisted coding, coupled with advancements in technology and developments in healthcare organizations, drive the market segment. For instance, in March 2023, Fujitsu launched a new cloud-based platform that allows users to securely collect and leverage health-related data to promote digital transformation in the medical field. As part of its goal for "Healthy Living" under Fujitsu Uvance to build a sustainable world, Fujitsu continues to promote the development of a healthy society.

- Similarly, in November 2022, Google Cloud launched three new Healthcare Data Engine (HDE) accelerators, developed in collaboration with Hackensack Meridian Health, Lifepoint Health, and others, that help organizations address common use cases around health equity, patient flow, and value-based care.

- Furthermore, governments in various countries are taking initiatives to support the growth of information technology in healthcare. For instance, in February 2021, as part of the UK government's program to adopt a fully connected cloud-driven health service, more than two million NHSmail mailboxes were moved to Exchange Online, a part of Microsoft's Azure Cloud. This enabled smoother and more efficient communication between staff across NHS organizations and departments and provided improved access to information. This is likely to increase the usage of health information technology (HCIT) change management services in the United Kingdom and is expected to boost the growth of the segment over the study period.

- Additionally, the joint initiatives taken by government bodies and market players in the region are also driving the growth of the market. For instance, in September 2021, Deutsche Telekom's T-Systems partnered with Google Cloud to build and deliver sovereign cloud services to German enterprises, healthcare firms, and the public. The companies jointly developed a large spectrum of next-generation sovereign cloud solutions and infrastructure. The company planned to build a similar sovereign cloud for Austria and Switzerland.

- Thus, owing to the rise in the adoption of cloud/web-based healthcare software and the rise in strategic activities by the key players, the studied segment is expected to witness significant growth over the study period.

North America is Expected to Witness a Significant Growth Over the Forecast Period

- North America is expected to witness significant growth in the computer-assisted coding market owing to the increase in the adoption of digital healthcare services across the hospitals, the rise in strategic activities by the key players, and the increase in investment towards digitalization of healthcare in North America.

- For instance, in a survey conducted by Canada Health Infoway in November 2022, 94% of Canadians were interested in accessing digital health services. Canadians could also access their personal health information online, including lab tests and diagnostic results, immunization history/records, a list of current medications and medication history, and specialist consultation notes/records. Thus, owing to people's adoption of digital health services, the studied market is expected to witness significant growth over the forecast period.

- Furthermore, an increase in computer-assisted coding by the key players in the North American region is expected to bolster the market growth over the study period. For instance, in July 2022, Greenway Health, a health information technology services provider, launched Greenway Medical Coding services, its newest healthcare solution for ambulatory practices. Greenway Medical Coding offers practices to capture cost efficiencies, improve practice earning potential, and collect insurance payments efficiently with the knowledge and precision of a personalized coding team.

- Similarly, in September 2022, AQuity Solutions, a provider of virtual solutions for real-time clinical documentation, medical coding, and mid-revenue cycle offerings, acquired all the assets of Tampa, FL-based Coding Services Group CSG. Thus, owing to such strategic activities by the key players, the demand for computer-assisted coding will likely increase, fueling market growth across North America.

- Therefore, due to the rise in the adoption of digital health services in healthcare settings and the increase in strategic activities by the key players in North America, the market is anticipated to witness notable growth over the forecast period.

Computer-assisted Coding Industry Overview

The computer-assisted coding market is moderately fragmented and competitive in nature. Market players are focused on strategic activities such as product launches, collaborations, and acquisitions to advance their portfolio and presence across the globe. Some market players include Oracle, Computer Programs and Systems, Inc. (TruCode LLC), United Health Group (Optum Inc.), Artificial Medical Intelligence Inc., and 3M, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Implementation of Electronic Health Record (EHR) Systems

- 4.2.2 Rising Utilization of Computer Assisted Coding Solutions to Curtail the Rising Healthcare Costs

- 4.2.3 Increasing Regulatory Requirements for Patient Data Management

- 4.3 Market Restraints

- 4.3.1 High Implementation and Maintenance Costs

- 4.3.2 Lack of On-site Support and In-house Domain Knowledge

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Software

- 5.1.1.1 Standalone Software

- 5.1.1.2 Integrated Software

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Mode of Delivery

- 5.2.1 Web and Cloud Based

- 5.2.2 On-premise

- 5.3 By Application

- 5.3.1 Automated Computer-assisted Encoding

- 5.3.2 Management Reporting and Analytics

- 5.3.3 Clinical Coding Auditing

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Clinical Laboratories and Diagnostic Centers

- 5.4.3 Other End-Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M

- 6.1.2 UnitedHealth Group (Optum Inc.)

- 6.1.3 Nuance Communications Inc.

- 6.1.4 Oracle

- 6.1.5 Computer Programs and Systems, Inc. (TruCode LLC)

- 6.1.6 Artificial Medical Intelligence Inc.

- 6.1.7 Athenahealth Inc.

- 6.1.8 Streamline Health Solutions Inc.

- 6.1.9 Epic Systems Corporation

- 6.1.10 ZyDoc Corporation

- 6.1.11 Alpha II LLC

- 6.1.12 AGS Health