|

市场调查报告书

商品编码

1404508

NaaS(网路即服务):市场占有率分析、产业趋势/统计、成长预测,2024-2029Network as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

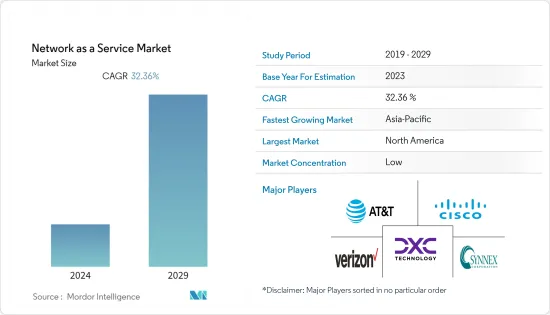

NaaS(网路即服务)市场去年估值为144.6亿美元,预计未来五年将以32.36%的复合年增长率成长,达到783.8亿美元。

NaaS 为组织和企业提供弹性并提高其网路基础设施的效能。按需购买使企业变得更加重视成本,只为他们需要的网路服务付费。 NaaS 对于需要更灵活配置而无需重建网路或重新制定合约的组织也很有用。

主要亮点

- 全球新资料中心基础设施的广泛建设正在推动NaaS市场的成长。推动这一扩张的几个关键驱动因素包括更多地使用云端运算进行资料储存、采用巨量资料分析以及提高工作负载移动性的中心虚拟。这些进步可以提高关键企业应用程式的资源利用率、提高可用性、降低总成本以及提高可靠性和安全性。

- 此外,网路虚拟、云端运算和软体定义网路 (SDN) 领域对基于订阅和按使用付费的业务模式的需求不断增长,对市场轨迹产生了重大影响。越来越多地使用云端服务来满足大型和小型企业的需求,这在塑造产业形势发挥着重要作用。

- NaaS 为企业提供了弹性和提高网路效能的机会。组织可以透过按需购买来支付他们所要求的确切网路服务的费用,从而实现成本效益。 NaaS 还支援需要更灵活配置的企业,而无需重做网路或合约。

- 诺基亚对 100 位 IT 领导者进行了调查,了解他们在整个大流行期间对 NaaS 的期望。这项研究旨在确定主要好处、采用的潜在障碍以及预计未来推出的顶级服务。 47% 的企业技术领导者希望在其组织内实施 NaaS。值得注意的是,虽然 10% 的受访者已经购买了 NaaS 服务,但只有 14% 的受访者表示没有计划从事 NaaS 服务。当谈到 Naas 产品时,这些高阶主管专注于特定标准:62% 的人专注于提高安全性,58% 的人专注于最佳效能,48% 的人专注于保证服务水准和市场成长。我是。

- 然而,NaaS 具有显着的优势。然而,重要的是要意识到某些障碍和潜在的可靠性问题可能会阻碍其在可预见的未来的成长。选择第三方网路基础设施供应商来託管公司的关键基础设施需要信任供应商的长期稳定性。如果供应商无法保持竞争力,企业可能会面临更换关键基础设施的挑战。

- 自COVID-19爆发以来,由于企业采用远距工作模式,对基于云端基础的解决方案的需求显着增长,但零售、製造和BFSI等各行业的收益却出现了大幅下滑。随着远端工作模式的扩展,随着公司增加对云端基础的分析和保证、边缘运算以及人工智慧驱动的网路技术的投资,NaaS 市场预计也会扩大。

- 为了应对 COVID-19,Aruba 对 2,400 名 IT 决策者进行的调查发现,38% 的 IT 领导者增加了对云端基础的网路的投资,35% 增加了对基于AI 的网路的投资。并且正在寻求更敏捷和自动化的混合工作基础架构环境。此外,随着企业适应 COVID-19,NaaS 的采用率将在未来两年内加速 38%。

NaaS 市场趋势

企业越来越多采用云端服务来推动市场

- 技术的不断使用以及客户对远端资料存取的偏好正在推动对云端基础的解决方案的需求。企业逐渐意识到,与维护本地基础设施相比,迁移到云端可以节省资金和资源,从而提高大型和小型企业的采用率。未来五年,云端运算和虚拟可能会降低软体设定成本和硬体使用率。

- 据泰雷兹集团称,去年超过 60% 的企业资料储存在云端,高于 30%。随着越来越多的公司采用云端运算,这些趋势为製造商进入这个市场创造了重要的机会。

- 例如,据印度Druva Inc.称,许多公司正在转向企业资料,尤其是大量非结构化资料。据该公司称,这种资料类型是在企业储存系统上维护的。此外,根据最新的思科世界指数,云端资料中心目前管理所有运算工作负载的 94%,而传统资料中心仅管理 6%。这一数字突显了云端基础的客服中心未来在全球部署的潜力。

- 银行和其他主要企业预计将迅速接受云端基础的服务部署。这是由 IT 行业持续推动基础设施简化以及解决方案开发人员透过从不同提供者采购应用程式和基础设施元件来建立混合云端解决方案的能力所推动的。这些趋势正在推动 NaaS 市场的发展。

北美占据主要市场占有率

- 美国正在发展成为一个拥抱先进技术的经济体,推动网路自动化、云端基础的服务和 NaaS 市场的扩张。未来五年,IT 团队计划采用供应商提供的 NaaS 解决方案,这些解决方案提供混合解决方案,包括软体、云端智慧和管理本地硬体的自主权。

- 在科技采用的先驱美国,首选行动装置数量的显着增加正在推动对增强网路服务的需求。随着云端软体定义网路 (SDN) 和虚拟网路功能 (VNF) 等虚拟设定的成长,该地区的各种网路服务供应商(NSP) 正在支援按需基础架构。然而,为组织规划和获取网路连接需要时间和精力,这对于希望跟上数位趋势并以软体主导的速度运行的企业来说充满挑战。

- 加拿大的 NaaS 市场正在不断扩大,新产品的发布、收购、併购、合作和协作正在改变北美市场。针对 IT服务供应商的网路攻击大幅增加,导致资料外洩。因此,加拿大网路安全中心发布了建议,要求各组织在选择网路服务供应商时更加谨慎。

- 随着自动化和协作设备的部署扩大,市场需求正在显着增加。 NaaS 模式对于小型企业尤其有利。鑑于加拿大有大量小型企业,NaaS 的使用预计在短期内将获得巨大的吸引力。

NaaS行业概况

NaaS市场由几家大公司组成,竞争非常激烈。市场分散,有大大小小的参与者。拥有压倒性市场占有率的主要企业正致力于将基本客群扩展到区域之外。这些公司正在利用策略合作措施来提高市场盈利和份额。该市场的主要企业包括 AT&T Intellectual Property、Verizon 和 Cisco System Inc.。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 企业越来越多采用云端服务

- 扩展 SDN 与现有网路基础设施的集成

- 市场抑制因素

- 隐私和资料安全问题

第六章市场区隔

- 按类型

- LANaaS

- WANaaS

- 按申请

- vCPE

- BoD

- 整合网路SECaaS

- WAN

- VPN

- 按行业分类

- 卫生保健

- BFSI

- 零售/电子商务

- 资讯科技/通讯

- 製造业

- 运输/物流

- 公共部门

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东/非洲

- 北美洲

第七章竞争形势

- 公司简介

- AT&T Intellectual Property

- Verizon

- DXC Technology Company

- TD SYNNEX Corporation

- Cisco Systems, Inc.

- NEC Corporation

- Hewlett Packard Enterprise Development LP

- IBM

- Oracle

- GTT Communications, Inc.

- VMware, Inc.

- Telstra Group Limited

- CenturyLink

- Meta Networks Ltd(Proofpoint)

- Masergy Communications, Inc.

- Juniper Networks, Inc.

- Nokia(Alcatel Lucent)

- Akamai Technologie

- Broadcom

第八章投资分析

第九章 市场机会及未来趋势

The network as a service market was valued at USD 14.46 billion the previous year and is expected to grow at a CAGR of 32.36%, reaching USD 78.38 billion by the next five years. Network-as-a-Service (NaaS) offers organizations and companies greater flexibility and even performance gains in their network infrastructure. With on-demand purchasing, firms can be more cost-conscious and pay only for the necessary networking services. Network-as-a-Service (NaaS) can also enable organizations that need greater flexibility in provisioning without having to rearchitect networks or redo contracts from the ground up.

Key Highlights

- The broad construction of new data center infrastructures worldwide drives the growth of the network as a service (NaaS) market. Several main drivers drive this expansion, including the increasing use of cloud computing for data storage, the incorporation of Big Data analytics, and virtualization within that center to improve workload mobility. These advancements have resulted in better resource utilization, higher availability, lower total costs, and increased reliability and security for critical corporate applications.

- Furthermore, the increasing need for subscription-based and pay-per-use business models in network virtualization, cloud computing, and software-defined networking (SDN) is significantly impacting the market trajectory. The growing use of cloud services, which cater to the demands of large and small organizations, plays a significant role in shaping the industry landscape.

- NaaS gives businesses more flexibility and the opportunity for improved network performance. Organizations can emphasize cost-effectiveness by paying for the precise networking services requested via on-demand purchases. NaaS also enables businesses that need more provisioning flexibility without redoing their network or contract.

- Throughout the pandemic, Nokia studied with 100 IT leaders to learn about their expectations of their network as a service (NaaS). The study sought to identify the significant benefits, potential barriers to adoption, and the top services they will likely acquire. Forty-seven percent of the enterprise technology leaders wanted to implement NaaS within their organizations. Notably, ten percent of respondents had already purchased NaaS services, while only 14 percent said their businesses had yet to make plans to engage in NaaS service. Regarding Naas products, these executives emphasized specific criteria, with sixty-two percent emphasizing improved security, 58 percent wanting optimum performance, and forty-eight percent valuing guaranteed service levels and driving the market's growth.

- However, network as a service (NaaS) offers significant advantages; it's important to acknowledge certain obstacles and potential reliability issues that could hinder its growth in the foreseeable future. Opting for a third-party network infrastructure provider to host critical corporate infrastructure requires faith in the supplier's long-term stability. Businesses may face the challenge of replacing essential infrastructure if the provider fails to remain competitive.

- Since the outbreak of COVID-19, the demand for cloud-based solutions has seen significant growth owing to remote working models being adopted by enterprises; however, various industries such as retail, manufacturing, BFSI, and others have seen a considerable revenue slump. With the growing remote working model, companies are increasing investments in cloud-based analytics and assurance, edge computing, and AI-powered networking technologies, which are expected to boost the NaaS market.

- According to a survey by Aruba of 2400 IT decision-makers, in response to COVID-19, 38 percent of IT leaders plan to increase their investment in cloud-based networking and 35 percent in AI-based networking as they seek more agile, automated infrastructures for hybrid work environments. Also, Network-as-a-Service adoption will accelerate by 38 percent within the next two years as businesses adapt to COVID-19.

Network as a Service Market Trends

Increased Adoption of Cloud Services among Enterprises to Drive the Market

- The growing use of technology and customer preference for remote data access drives the increased need for cloud-based solutions. Companies understand the cost and resource savings benefits of migrating to the cloud rather than maintaining on-premise infrastructure, leading to increased adoption among large corporations and SMEs. During the next five years, cloud computing and virtualization will lower software setup costs and hardware utilization.

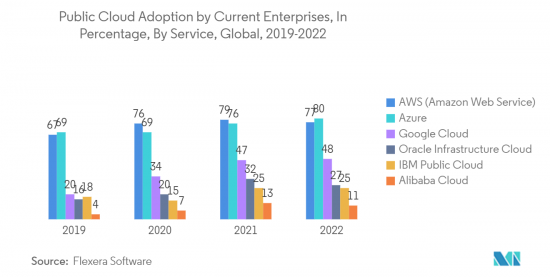

- According to the Thales Group, more than 60 percent of corporate data was kept in the cloud last year, a massive increase from 30 percent. These trends create considerable potential prospects for manufacturers in this market, with the increasing adoption of cloud computing among organizations broadening the market's scope.

- For instance, according to Druva Inc., a company located in India, numerous companies focus on enterprise data, particularly because of its substantial volume of unstructured data. According to the company, this data type is held in enterprise storage systems. Furthermore, according to the most recent Cisco Global Index, cloud data centers currently manage 94 percent of all computing workloads, while traditional data centers handle only 6 percent. This figure emphasizes the global potential for cloud-based contact center deployment in the future.

- Banking and other key businesses are expected to embrace cloud-based service rollout rapidly. This is due to the IT industry's continued quest for simplified infrastructure and solution developers' ability to create hybrid cloud solutions by obtaining application and infrastructure components from different providers. This tendency is helping to drive the Network as a service (NaaS) market forward.

North America to Occupy Significant Market Share

- The United States has developed an economy that embraces advanced technology, propelling the expansion of network automation, cloud-based services, and the Network as a service (NaaS) market. IT teams are set to adopt NaaS solutions from suppliers that offer hybrid solutions, including software, cloud intelligence, and the autonomy to manage on-premise hardware in the next five years.

- As a pioneer in technology adoption, the United States is experiencing a rise in demand for enhanced network services, driven by significant growth in liked mobile devices. With the growth of virtualized settings such as Cloud Software Defined Networks (SDN) and Virtual Network Functions (VNF), various Network Service Providers (NSPs) in the region have enabled on-demand infrastructure. However, planning and acquiring network connectivity for organizations may take time and effort, posting difficulties for businesses attempting to stay up with digital trends and function at software-driven speeds.

- The Canadian NaaS market is expanding due to new product releases, acquisitions, mergers, partnerships, and collaborations that are transforming the North American market. There has been a noteworthy increase in cyberattacks on IT service providers, resulting in data breaches. As a result, the Canadian Center for Cybersecurity has issued recommendations to organizations, allowing them to be more selective when picking network service providers.

- Market demand is increasing significantly as automation and linked device deployment expand. The NaaS model is especially beneficial for small firms since it allows them to delegate day-to-day equipment upkeep and focus on their key capabilities, such as customer service. Given the prevalence of small enterprises in Canada, using NaaS is projected to grow considerable traction soon.

Network as a Service Industry Overview

The Network-as-a-Service Market consists of several major players and is highly competitive. The market is fragmented due to the presence of several small and large players. The key players that hold a prominent market share are focusing on expanding their customer base across regional boundaries. These companies leverage strategic collaborative initiatives to increase their market profitability and share. Some major players in the market are AT&T Intellectual Property, Verizon, and Cisco System Inc., among others.

- January 2022, Fujitsu Network Communications, Inc. introduced software-defined wide area network, or SD-WAN as a Service, for service providers to deliver to their enterprise clients. The solution combines the Silver Peak Unity EdgeConnectSP SD-WAN system with Fujitsu's Managed Network Service and SDN/NFV Consulting Service. The Fujitsu product enables service providers to immediately deliver SD-WAN-as-a-Service to their enterprise customers rather than designing and implementing their solution for months. As a result, service providers can now concentrate on attracting clients and making money by utilizing the advantages of this disruptive technology.

- June 2022 - Kyndryl, a provider of IT infrastructure services, and Cisco announced a technical alliance to assist enterprise customers in accelerating the transformation into data-driven organizations using Cisco technologies and Kyndryl-managed services. By utilizing cloud computing technologies that simplify difficult hybrid IT management with increased visibility, manageability, and flexibility, Kyndryl and Cisco work together to facilitate businesses in transforming their operations. Also, Kyndryl and Cisco are working together to create new private cloud services, network and edge computing solutions, software-defined networking (SDN) solutions, and multi-network vast area network (WAN) options in a setting with high-tech security features.

- September 2022 - Verizon launched a global Network-as-a-Service (NaaS) relationship with Wipro Ltd, a technology services and consulting firm, that speeds enterprises' network modernization and cloud transformation journeys. Wipro's Network-as-a-Service (NaaS) solution, powered by Verizon, comprises a variety of pre-configured and proven service chains on a subscription-based consumption model, allowing network consumption infrastructure to be consumed on demand.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Adoption of Cloud Services among Enterprises

- 5.1.2 Augmentation in Software-defined Networking (SDN) Integration with Existing Network Infrastructure

- 5.2 Market Restraints

- 5.2.1 Privacy and Data Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 LAN-as-a-Service

- 6.1.2 WAN-as-a-Service

- 6.2 By Application

- 6.2.1 Cloud-based Services (vCPE)

- 6.2.2 Bandwidth on Demand (BoD)

- 6.2.3 Integrated Network Security-as-a-Service

- 6.2.4 Wide Area Network (WAN)

- 6.2.5 Virtual Private Network (VPN)

- 6.3 By Industry Vertical

- 6.3.1 Healthcare

- 6.3.2 BFSI

- 6.3.3 Retail and E-commerce

- 6.3.4 IT and Telecom

- 6.3.5 Manufacturing

- 6.3.6 Transportation and Logistics

- 6.3.7 Public Sector

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East & Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 Rest of Middle East & Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 AT&T Intellectual Property

- 7.1.2 Verizon

- 7.1.3 DXC Technology Company

- 7.1.4 TD SYNNEX Corporation

- 7.1.5 Cisco Systems, Inc.

- 7.1.6 NEC Corporation

- 7.1.7 Hewlett Packard Enterprise Development LP

- 7.1.8 IBM

- 7.1.9 Oracle

- 7.1.10 GTT Communications, Inc.

- 7.1.11 VMware, Inc.

- 7.1.12 Telstra Group Limited

- 7.1.13 CenturyLink

- 7.1.14 Meta Networks Ltd (Proofpoint)

- 7.1.15 Masergy Communications, Inc.

- 7.1.16 Juniper Networks, Inc.

- 7.1.17 Nokia (Alcatel Lucent)

- 7.1.18 Akamai Technologie

- 7.1.19 Broadcom

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES & FUTURE TRENDS

2024 年 NaaS(网路即服务)全球市场报告

2024 年 NaaS(网路即服务)全球市场报告 网路即服务将网路营运商转变为以 API 为中心的整合商

网路即服务将网路营运商转变为以 API 为中心的整合商 网路即服务市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测

网路即服务市场:2023-2028 年全球产业趋势、份额、规模、成长、机会与预测 网路即服务市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按类型、服务、最终用户、地区细分

网路即服务市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按类型、服务、最终用户、地区细分 网路即服务市场报告:2030 年趋势、预测与竞争分析

网路即服务市场报告:2030 年趋势、预测与竞争分析 网路·即服务的全球市场

网路·即服务的全球市场 网路即服务市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测

网路即服务市场:按类型、用途和最终用户划分 - 2023-2030 年全球预测 全球网路·即服务市场2023-2027

全球网路·即服务市场2023-2027 NaaS(Network-as-a-Service)的全球市场 - 市场规模、市场区隔、展望、收益预测(2022年~2028年):各类型,各用途,各企业,各终端用户,各地区

NaaS(Network-as-a-Service)的全球市场 - 市场规模、市场区隔、展望、收益预测(2022年~2028年):各类型,各用途,各企业,各终端用户,各地区 NaaS(Network-as-a-Service)市场:各类型,各用途,各企业规模,各业界:全球机会分析及产业预测,2021年~2031年

NaaS(Network-as-a-Service)市场:各类型,各用途,各企业规模,各业界:全球机会分析及产业预测,2021年~2031年