|

市场调查报告书

商品编码

1406102

磷酸-市场占有率分析、产业趋势与统计、2024年至2029年成长预测Phosphoric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

预计2024年磷酸市场规模为9,298万吨,预计2029年将达到1,1439万吨,在预测期间(2024-2029年)复合年增长率为4.23%。

市场受到了 COVID-19 大流行的负面影响,该流行病扰乱了关键的供应和生产线,导致严重的供不应求。磷酸的主要用途是生产肥料。这场流行病也导致作物产量下降,人口出现粮食和其他必需品短缺。疫情过后,市场回暖,主要产业復工復产,需求成长。

主要亮点

- 由于大部分磷酸用作化肥原料,预计市场需求将受到化肥行业需求增加以及食品和饮料行业使用量增加的推动。

- 磷酸造成的健康危害和化肥价格急剧上升预计将阻碍市场成长。

- 儘管如此,从磷酸中回收稀土元素以及手性磷酸作为催化剂的商业化预计将为市场提供利润丰厚的机会。

- 亚太地区占据了最高的市场占有率,该地区很可能在预测期内主导市场。

磷酸市场趋势

化肥产业主导市场

- 磷酸基本上是生产肥料的中间体。磷酸一铵(MAP)、磷酸二铵(DAP)和磷酸三钠(TSP)等肥料是由磷酸生产的。

- 磷酸是许多肥料的主要成分,因为它是一种多功能剂,用于植物营养、调节 pH 值、清洁灌溉设备中的石灰沉淀等。磷酸是植物磷的丰富来源。

- 磷肥对植物非常重要,比有机肥效果更好。磷促进植物成熟,促进根系发育。这在干旱地区尤其重要。

- 据Essential Chemical Industry称,全球每年生产超过4,300万吨磷酸,其中约90%用于化肥。

- 据美国农业部对外农业服务局称,中国、俄罗斯、美国、印度和加拿大生产的化肥养分占全球总量的 60% 以上。俄罗斯和美国的化肥产量各占世界总量的不到10%,中国的产量约为25%。

- 2022 年 9 月,美国政府宣布了一项价值 5 亿美元的计画来提高国内化肥产量,并敦促欧盟 (EU) 也采取同样的做法。加拿大已经是全球最大的钾肥供应国,2022年11月宣布将每年增加20%的化肥出口,以填补其他国家停止出货的缺口。

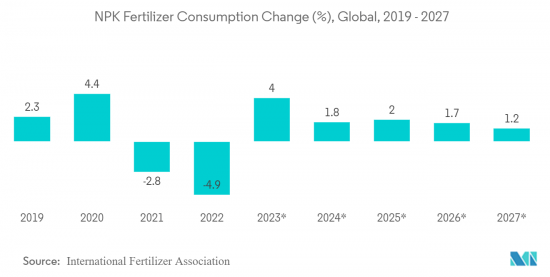

- 根据国际肥料协会(IFA)的数据,中国是最大的化肥用户,消耗了世界化肥供应量的近四分之一。 2022年,中国氮磷钾肥料产量总合5,570万吨。 2021年为5544万吨,2020年为5496万吨。

- 因此,考虑到世界不同地区化肥的成长趋势和产量,化肥产业可能会主导市场,预计将增加预测期内磷酸的需求。

亚太地区主导市场

- 亚太地区在 2022 年占据磷酸市场的主导地位,占有重要的销售份额,预计在预测期内将保持其主导地位。

- 这是因为中国是世界上最大的化肥生产国和消费国。中国、印度、东南亚国家等国家对磷酸的需求不断增加。

- 中国约占全球农业总面积的7%,养活了全球22%的人口。该国是各种谷物的最大生产国,包括大米、棉花、马铃薯等。因此,由于该国广泛的农业活动,对肥料用磷酸的需求正在迅速增加。

- 磷酸也广泛用于磷酸铁锂电池的生产,中国是该领域的主导国家。到2022年,中国销售的所有电动车中44%将使用磷酸铁锂电池,其次是欧洲的6%、美国和加拿大的3%。

- 另一个化肥生产大国印度是第二大用户。印度的大部分使用量都来自印度政府的大量化肥补贴。 22 财年,印度生产了超过 4,200 万吨化肥。印度化肥产量在 2020 财年达到峰值,超过 4,600 万吨。近年来,推出了鼓励公共、合作和私部门投资的优惠政策。

- 磷酸也用于食品和饮料行业,以酸化食品和饮料,例如各种可乐和果酱,以提供浓郁或酸味。根据美国农业部(USDA)统计,印度食品工业位居世界第三大食品工业。该行业在过去几年中稳步增长,印度有望成为世界上最大的食品生产国。到 2025 年,该国食品和杂货 (F&G) 零售市场的销售额预计将超过 8,500 亿美元。

- 因此,上述原因可能会推动亚太地区磷酸市场在预测期内的成长。

磷酸产业概况

磷酸市场已部分整合,多家公司在全球和区域层面开展业务。该市场的主要企业(排名不分先后)包括 OCP Group、Mosaic、PhosAgro Group of Companies、Nutrien Ltd 和 IFFCO。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 化肥产业需求旺盛

- 食品和饮料行业的使用量增加

- 市场抑制因素

- 磷酸对健康的损害

- 价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 磷酸价格走势分析(2018-2023年)

- 技术简介

第五章市场区隔(市场规模)

- 按最终用户产业

- 肥料

- 食品与饮品

- 化学品

- 药品

- 冶金

- 其他最终用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 墨西哥

- 加拿大

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、联盟、协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Aditya Birla Chemicals

- Agropolychim

- EuroChem Group

- ICL

- IFFCO

- Innophos

- JR Simplot Company

- Mosaic

- Nutrien Ltd

- Phosagro

- Sterlite Copper(A Unit of Vedanta Limited)

第七章 市场机会及未来趋势

- 从磷酸回收稀土元素

- 手性磷酸催化剂的商业化

The Phosphoric Acid Market size is estimated at 92.98 Million tons in 2024, and is expected to reach 114.39 Million tons by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 pandemic as it disrupted the main supply and manufacturing lines, leading to acute shortages. The main use of phosphoric acid is for producing fertilizers. The pandemic also led to a decrease in crop production, accompanied by a shortage of food and other essentials among people. After the pandemic, the market picked up speed, and the demand grew as major industries got back to work.

Key Highlights

- Since most phosphoric acid is used to make fertilizer, the rising demand from the fertilizer industry and increasing usage in the food and beverage industry are expected to drive market demand.

- Health hazards caused by phosphoric acid and the high price of fertilizers are expected to hinder the market's growth.

- Nevertheless, the recovery of rare earth elements from phosphoric acid and the commercialization of chiral phosphoric acid as a catalyst are expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Phosphoric Acid Market Trends

Fertilizer Industry to Dominate the Market

- Phosphoric acid is basically an intermediate used to produce fertilizers. Fertilizers like monoammonium phosphate (MAP), diammonium phosphate (DAP), and trisodium phosphate (TSP) are produced from phosphoric acid.

- Phosphoric acid forms a key component for many fertilizers as it is a multi-function agent used for plant nutrition, pH adjustment, and cleansing irrigation equipment from lime precipitation. It is a rich source of phosphorus for plants.

- Phosphorus fertilizers are extremely important for the plant and provide better activities than organic fertilizers. Phosphorus accelerates the maturation of the plant and also provides the development of the roots. This is particularly important for dry areas.

- According to the Essential Chemical Industry, annually, more than 43 million metric tons of phosphoric acid are produced worldwide, of which about 90% are used to make fertilizers.

- According to the USDA Foreign Agricultural Service, China, Russia, the United States, India, and Canada produce more than 60% of the world's fertilizer nutrients combined. Russia and the United States each produce less than 10% of global fertilizers, while China produces approximately 25%.

- In September 2022, the US government announced programs worth USD 500 million to boost domestic fertilizer production, and the European Union is being urged to take similar action. Canada, already the world's largest supplier of potash fertilizers, announced in November 2022 that it will boost its fertilizer exports by 20% annually, filling a gap left by blocked shipments from other countries.

- According to the International Fertilizer Association (IFA), China is the largest user of fertilizer, consuming nearly one-quarter of global fertilizer supplies. In 2022, a total of 55.7 million tons of NPK fertilizer was produced in China. This was 55.44 million tons in 2021 and 54.96 million tons in 2020.

- Therefore, considering the growth trends and production of fertilizers in different regions worldwide, the fertilizer industry is likely to dominate the market, which, in turn, is expected to enhance the demand for phosphoric acid during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the phosphoric acid market in 2022 with a considerable volume share, and it is expected to maintain its dominance during the forecast period.

- This is due to China being the world's largest producer and consumer of fertilizer. In countries like China, India, and Southeast Asian nations, the demand for phosphoric acid has been increasing continuously.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for phosphoric acid, which is used in fertilizers, is rapidly increasing owing to the large-scale agricultural activities in the country.

- Phosphoric acid is also used extensively in the production of lithium-iron-phosphate batteries, and China is the dominant country in this field. In 2022, 44% of the total electric vehicles sold in China used LFP batteries, followed by 6% in Europe and 3% in the United States and Canada.

- India, another large fertilizer producer, is the second largest user. Much of India's usage is fueled by the Indian government's heavy subsidization of fertilizers. In the financial year 2022, over 42 million metric tons of fertilizers were produced in India. Fertilizer production in India peaked in the financial year 2020 at over 46 million metric tons. During the last few years, there has been a favorable policy facilitating investments in the public, cooperative, and private sectors.

- Phosphoric acid is also used in the food and beverage industries to acidify foods and beverages, such as various colas and jams, providing a tangy or sour taste. According to the US Department of Agriculture (USDA), the Indian food industry ranks as the third-largest food industry globally. The industry has been experiencing steady growth over the past several years, with India anticipated to become the largest food producer in the world. The country's food and grocery (F&G) retail market is projected to surpass USD 850 billion in sales by 2025.

- Hence, the reasons mentioned above are likely to fuel the growth of the phosphoric acid market in Asia-Pacific over the forecast period.

Phosphoric Acid Industry Overview

The phosphoric acid market is partially consolidated, with several companies operating on both global and regional levels. Some of the major players in the market (not in any particular order) include OCP Group, Mosaic, PhosAgro Group of Companies, Nutrien Ltd, and IFFCO, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Drivers

- 4.1.1 High Demand for Fertilizer Industry

- 4.1.2 Increasing Usage in the Food and Beverage Industry

- 4.2 Market Restraints

- 4.2.1 Health Hazards Caused by Phosphoric Acid

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Supplier

- 4.4.2 Bargaining Power of Buyer

- 4.4.3 Threat of New Entrant

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Price Trend Analysis of Phosphoric Acid (2018-2023)

- 4.6 Technological Snapshot

5 Market Segmentation (Market Size in Volume)

- 5.1 By End-user Industry

- 5.1.1 Fertilizer

- 5.1.2 Food and Beverages

- 5.1.3 Chemicals

- 5.1.4 Medicine

- 5.1.5 Metallurgy

- 5.1.6 Other End-user Industries

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Merger and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 Agropolychim

- 6.4.3 EuroChem Group

- 6.4.4 ICL

- 6.4.5 IFFCO

- 6.4.6 Innophos

- 6.4.7 J.R. Simplot Company

- 6.4.8 Mosaic

- 6.4.9 Nutrien Ltd

- 6.4.10 Phosagro

- 6.4.11 Sterlite Copper (A Unit of Vedanta Limited)

7 Market Opportunities and Future Trends

- 7.1 Recovery of Rare Earth Elements from Phosphoric Acid

- 7.2 Commercialization of Chiral Phosporic Acid as a Catalyst

美国高纯度电子级磷酸市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按应用

美国高纯度电子级磷酸市场规模和预测、全球和地区份额、趋势和成长机会分析报告范围:按应用 全球磷酸市场规模、份额、成长分析、按方法、按等级 - 2023-2030 年产业预测

全球磷酸市场规模、份额、成长分析、按方法、按等级 - 2023-2030 年产业预测 三氯化磷市场报告:2030 年趋势、预测与竞争分析

三氯化磷市场报告:2030 年趋势、预测与竞争分析 亚磷酰胺市场:按类型、最终用户划分 - 全球预测 2024-2030

亚磷酰胺市场:按类型、最终用户划分 - 全球预测 2024-2030 磷化氢熏蒸市场:型态、类型和应用划分 - 2024-2030 年全球预测

磷化氢熏蒸市场:型态、类型和应用划分 - 2024-2030 年全球预测 亚磷酰胺 - 2024 年至 2029 年市场占有率分析、产业趋势与统计、成长预测

亚磷酰胺 - 2024 年至 2029 年市场占有率分析、产业趋势与统计、成长预测 磷酸市场(应用:肥料、食品添加剂、动物饲料等)- 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测

磷酸市场(应用:肥料、食品添加剂、动物饲料等)- 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测 全球磷酸燃料电池(PAFC)市场预测(至2030年)

全球磷酸燃料电池(PAFC)市场预测(至2030年) 磷酸盐市场 - 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测

磷酸盐市场 - 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测 脱氧核苷酸三磷酸 (dNTP) 的全球市场 2024-2028

脱氧核苷酸三磷酸 (dNTP) 的全球市场 2024-2028