|

市场调查报告书

商品编码

1408494

工业人工智慧软体:市场占有率分析、产业趋势与统计、2024-2029 年成长预测Industrial AI Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

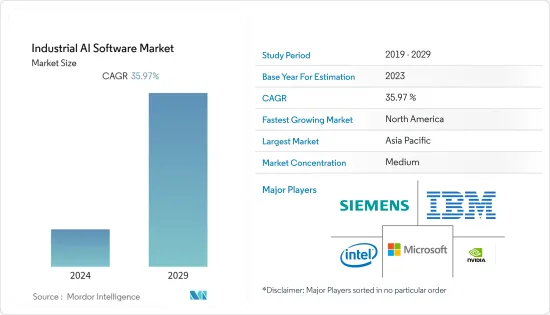

本财年工业人工智慧软体市场价值843.4亿美元。

预计未来五年将达到 3,919.7 亿美元,预测期内复合年增长率为 35.97%。

主要亮点

- 越来越注重从工业资料中获取价值。这增加了对多方面优化的需求,使得人工智慧驱动的决策和营运敏捷性对高阶主管更加重要。为了在当今动盪的市场中取得成功,公司必须同时优化跨业务目标(例如报酬率、经济性和永续性)的资产和流程。

- 欧盟委员会表示,欧洲人工智慧战略旨在将欧盟(EU)打造为人工智慧枢纽,确保人工智慧(AI)值得信赖、人性化。这些目标反映在欧洲透过具体法律和行动追求卓越和信任的方法中。人工智慧卓越的关键是充分利用可用资源并协调投资。欧盟委员会打算透过其「数位欧洲」和「地平线欧洲」计画每年在人工智慧领域投资 10 亿欧元。在数位化十年期间,欧盟委员会也将动员私部门和成员国的其他投资,将年度投资额提高到200亿欧元。

- 虽然人工智慧仍然是一个重要的技术领域,但组织需要有效的方法来扩展其人工智慧实践,并利用人工智慧进行业务来加快人工智慧投资的投资报酬率。随着组织面临着优化工作流程的更大压力,越来越多的公司将求助于 BI 团队来管理和开发 AI/ML 模型。有两个关键因素推动了新的基于 BI 的 AI 开发人员类别的发展:首先,使用自动化平台等工具支援 BI 团队比僱用专门的资料科学家更具扩充性,成本昂贵且永续。其次,与资料科学家相比,BI 团队更接近业务用例,从而由于工作模型要求而加快了生命週期。

- 随着人工智慧技术的进步,政府比以往任何时候都更加重要的是对传统方法进行创新,以实现更好的公民参与、互通性和课责。这些趋势正在推动世界各地企业和组织对人工智慧管治的需求。例如,Google强调了政府与人工智慧从业者和更广泛的民间社会合作,可以在围绕人工智慧应用的期望方面发挥关键作用的五个领域。这包括可解释性标准、安全考量、评估公平性的方法、共同责任框架以及人类与人工智慧协作的要求。

- 相反,虽然大多数企业 IT 采购仅限于简单地选择正确的软体或硬体并最终将其部署以达到目的,但 AI 的根本问题是最初需要持续培训、处理资料和校准才能获得结果。存在限制电子记录中的资料标准化的已知问题。其中包括自然语言处理 (NLP)、威胁开放式创新的专有资料集、由于日誌偏见或彻头彻尾的诈欺而导致的医学文献中常见的偏见,以及历史资料不够具体,无法用于当前的预测。其中包括健康资料的併发症例如:

- COVID-19 大流行带来的挑战表明生产和再分配方面存在弱点,需要进行必要的改变以使供应链更具弹性。报告显示,整个零售供应链中所有运输环节对人工智慧的投资都在增加。每个地区的行业都将工人疾病和原材料短缺视为其供应链面临的最大挑战。在大流行后的情况下,行业对自动化和数数位化的日益关注预计将导致市场对分析和人工智慧解决方案的高需求,并在工业物联网用户中变得更普及。

工业人工智慧软体市场趋势

零售和消费品预计将占据很大的市场份额。

- 推动扩张的因素包括不断增长的网路用户数量、智慧型设备、店内监控的需求以及政府鼓励数位化的努力。零售业的人工智慧 (AI) 建立在企业过去几十年的营运方式之上。

- 人工智慧解决方案和巨量资料分析对于数位业务至关重要,并且有潜力改变从客户体验到业务流程的一切。人工智慧透过缩小从洞察到行动的差距,帮助公司在电子商务、行销、产品管理和其他业务领域更快地做出决策。美国商务部预计,2023年美国零售额将达5.99兆美元。

- 此外,零售商店的增加可能为人工智慧参与者创造机会开发新工具来满足广泛的零售客户的需求。例如,根据美国劳工统计局的数据,2022年第三季美国私人零售企业数量为1,061,539家,高于2022年第一季的1,049,543家。是。此外,根据中国国家统计局的数据,去年中国零售连锁店数量为292,383家。

- 此外,根据《麻省理工学院技术评论洞察》和亚马逊的数据,零售和消费品行业近一半的受访者表示,实施人工智慧将有助于改善顾客关怀。这意味着人工智慧解决方案可以接管增强对话来回答客户问题,并在客户无法提供协助时将其引导至正确的客服人员。此外,47% 的受访者表示人工智慧可以透过帮助管理成本和买家需求来显着改善库存管理。人工智慧追踪电子商务网站和实体店的需求和供应量,确保它们同步。

- 此外,各种零售公司正在实施人工智慧以更好地服务客户。例如,线上委託零售商 ThredUp 推出了 Goody Box,其中包含根据每位客户的风格量身定制的各种二手服装商品。顾客保留他们想要的东西并付费,并退回他们不需要的东西。 AI演算法会记住每位顾客的喜好,以便未来的盒子将更适合他们的口味。客户更喜欢非订阅盒,因为他们可以看到单独的零件。

- 根据美国零售联合会统计,7-11 零售连锁店的母公司 Seven & i Holdings 2022 年在全球经营超过 40,000 家零售店。 7-11 是一家在世界各地营运的连锁便利商店。那一年,Seven & i 的零售店数量超过了一些全球最大的零售商,例如拥有近 10,500 家门市的沃尔玛和拥有约 13,750 家门市的 Schwartz Group。儘管沃尔玛不是拥有最多商店的公司,但它是世界上最大的零售商之一。数量如此庞大的零售店很可能为市场参与者创造机会开发新的解决方案以占领市场占有率。

预计北美将占据很大份额。

- 以美国为首的北美地区,各产业的人工智慧(AI)解决方案市场正在不断扩大。在北美,替代人工智慧的采用准备度和高成长率是其经济影响的最大驱动力,反映了该地区对人工智慧及其采用的主导态度。此外,预计区域层面很快就会出现高度自动化潜力,这也是一个推动因素。

- 根据美国国家科学技术委员会的报告,2022财年(FY22)联邦政府用于资讯科技研发的支出为87.6亿美元,比上年增加4.1亿美元(4.9%)。研究显示,2022 财政年度所有联邦政府研究机构在人工智慧研发上的支出为 25.8 亿金额。这比上年度增加了 1.3 亿美元(成长 5.3%)。报告称,NSF(6.54 亿美元)、NIH(5.51 亿美元)、DARPA(4.57 亿美元)和国防部(3.91 亿美元)将在 2022 财年投资人工智慧研发。最大的资金来源是紧随其后的是能源部科学办公室(1.3 亿美元)。如此庞大的人工智慧支出很可能为参与者提供开发新解决方案以增加市场占有率的机会。

- 人工智慧解决方案在该行业中的优势将使该地区的食品和饮料企业能够在新工厂的试运行中实施人工智慧。例如,2023 年 2 月,推动永续植物来源和水果基食品和饮料未来发展的全球先驱 SunOpta 宣布在德克萨斯州启动新的植物来源饮料生产设施。公告。新的大型工厂将生产全系列植物来源奶、奶精和茶。包装尺寸和配置包括用于外食、货架零售和电子商务的植物性乳製品的 16 盎司和 32 盎司包装,以及常用于高蛋白能量饮料的 330 毫升瓶装。

- 越来越多的证据表明人工智慧 (AI) 将对加拿大的医疗实践产生重大影响。 GE 医疗集团 Edison 平台的推出使得重症监护套件和气胸演算法的开发成为可能。 Edison 能够无缝上传和共用医院的影像,并提供共用网路的共享工作区,来自不同组织的放射科医生可以在其中管理和註释影像。多伦多亨伯河医院是签署资料共用协议开发重症监护套件的四家机构之一,为 GE Healthcare 提供了 156,000 张符合隐私要求的胸部 X 光影像和相关报告。

- 此外,2023 年 9 月,Google Cloud 与科技公司大陆集团宣布建立策略合作伙伴关係,为汽车产业提供创新、灵活且面向未来的数位解决方案。此次合作将把大陆集团的汽车技术专业知识与Google的资料和人工智慧技术相结合,打造新一代安全、高效和以用户为中心的汽车解决方案。此外,两家公司期待将策略伙伴关係拓展到更多合作领域,为客户打造更好的汽车连结和体验。

工业人工智慧软体产业概况

工业人工智慧软体市场表现出适度的分散性,由几家主要企业组成,包括西门子公司、英伟达公司和Cisco。目前市场主导地位集中在少数几家大公司手中,这些公司正在采取策略联盟来扩大市场份额并提高盈利。

2023 年6 月,Alphabet 旗下公司Intrinsic 宣布与西门子合作,带来Intrinsic 的机器人软体,旨在无缝利用基于人工智慧的功能,并且我们已开始探索与西门子数位工业公司的整合和接口,西门子数位工业公司以其可互通和开放的产品组合而闻名。

2023 年 2 月,公认的数位工程和云端转型合作伙伴 Mastech 与创新的人工智慧主导零售软体解决方案提供商 Netail 合作。两家公司之间的策略联盟旨在帮助电子商务和全通路零售商优化其零售价值链,吸引、转换和留住数位消费者。 Mastek 在数位商务和资料分析方面的丰富专业知识与 Netail 的尖端人工智慧技术(在产品选择、定价和客户参与决策中发挥关键作用)相结合,创造出高度协同效应的零售解决方案。这将会成为现实。 Mastek 和 Netail 为线上零售商提供个人化的晶粒、对消费行为的更深入的了解、高效的用户体验、灵活的分类策略和即时的市场可视性。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 巨量资料技术在製造业的应用增多

- 扩大应用基础并更加重视实施数位转型以实现成本降低

- 市场抑制因素

- 敏感或合法资料的资料问题

第六章市场区隔

- 按类型

- 云端基础

- 本地

- 按最终用户产业

- 汽车与运输

- 零售/消费品

- 医疗保健/生命科学

- 航太/国防

- 能源/公共产业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争环境

- 公司简介

- IBM Corporation

- Intel Corporation

- Nvidia Corporation

- Microsoft Corporation

- Siemens AG

- Oracle Corporation

- Cisco Systems, Inc

- Veritone Inc.

- Advanced Micro Devices

- Google Inc

第八章投资分析

第九章 市场机会及未来趋势

The industrial AI software market is valued at USD 84.34 billion in the current year. It is expected to register a CAGR of 35.97% during the forecast period to become USD 391.97 billion by the next five years.

Key Highlights

- Increased focus on capturing value from industrial data. This drives the need for multi-dimensional optimization, meaning AI-enabled decision-making and operational agility are becoming more critical to executives. To thrive in today's volatile market, companies must simultaneously optimize their assets and processes across business objectives such as margins, economics, sustainability, etc.

- According to the European Commission, the European AI Strategy seeks to establish the European Union (EU) as a premier AI hub and to guarantee that artificial intelligence (AI) is trustworthy and centered on people. Such a purpose is translated through specific laws and deeds into the European approach to excellence and trust. An essential part of excellence in AI is making the most of available resources and coordinating investments. The Commission intends to invest EUR1 billion annually in AI through the Digital Europe and Horizon Europe programs. Over the digital decade, it will mobilize other investments from the private sector and the Member States to reach an annual investment volume of EUR 20 billion.

- Although AI is still one of the critical technology areas, organizations require an efficient way to scale their AI practices and use AI in business to accelerate ROI in AI investment. As organizations face more significant pressure to optimize their workflows, more companies will ask BI teams to manage and develop AI/ML models. The two critical factors that will drive this boost of a new BI-based AI developer class: First, enabling BI teams with tools such as automation platforms is more scalable and more sustainable than hiring dedicated data scientists; second, because BI teams are significantly closer to the business use-cases compared to data scientists, the lifecycle from the working model's requirement will be accelerated.

- With the advancement in AI technology, it is becoming more important than ever for the government to innovate its traditional methods to achieve better citizen engagement, interoperability, and accountability. Such trends are driving the demand for AI Governance from enterprises and organizations worldwide. For instance, Google has highlighted five areas where the government, in collaboration with AI practitioners and wider civil society, can play a crucial role in clarifying expectations about AI's application on a context-specific basis. These include explainability standards, safety considerations, approaches to appraising fairness, general liability frameworks, and requirements for human-AI collaboration.

- On the contrary, While most enterprise IT procurement is limited to simply choosing suitable software or hardware and eventually deploying it to serve its purpose, the fundamental trouble with AI is that there's an ongoing requirement for initial training and working with data and calibrating it to deliver the result. There are known problems limiting normalizing data in electronic records. These include natural language processing (NLP), proprietary datasets threatening open innovation, frequent bias in the medical literature due to journal bias and even outright fraud, and the growing complexity of health data such that past data is not specific sufficiently to be useful for current predictions.

- The issues caused by the COVID-19 pandemic suggested the weaknesses in production and redistribution with changes needed to make the supply chain more resilient. An increased investment toward AI in any in-transit element across the retail supply chain was presented. The industries in the various regions then depicted the biggest problems facing the supply chains as employee illness and shortages of raw supplies. The growing industrial focus on automation in the post-pandemic scenario and the move towards digitalization will result in higher demand for analytics and AI solutions in the market, which is expected to be more prevalent among IoT users in industries.

Industrial AI Software Market Trends

Retail and Consumer Packaged Goods is Expected to Hold Significant Share of the Market

- Factors driving expansion include the ever-increasing number of internet users, smart gadgets, the necessity for surveillance and monitoring in physical stores, and government initiatives encouraging digitization. Artificial intelligence (AI) in retail is based on how firms have operated over the last few decades.

- AI solutions and Big data analytics are essential to digital business; they have the potential to alter everything from customer experience to business processes. Artificial intelligence drives faster firms' decisions in e-commerce, marketing, product management, and other business areas by decreasing the gap from insights to action. According to the United States Department of Commerce, retail sales in the United States are expected to reach USD 5.99 trillion in 2023.

- Further, the rise in retail stores would create an opportunity for AI players to develop new tools to cater to a broad range of retail customers. For instance, According to the United States Bureau of Labor Statistics, in the 3rd quarter of 2022, there were 1,061,539 private retail trade establishments in the United States, which is a rise from the 1st quarter of 2022 private retail establishments, i.e., 1,049,543. Further, according to the National Bureau of Statistics of China, there were 292,383 retail chain stores in China last year.

- Moreover, according to MIT Technology Review Insights and Amazon, about half of the retail and consumer goods industry respondents state that deploying AI can help improve customer care. This means an AI solution could take over augmented conversations to respond to client questions and lead the customer to the right agent when it cannot assist. Additionally, 47% of respondents said that AI could significantly improve inventory management by helping to manage costs and buyers' needs. AI tracks quantities of supply and demand at both e-commerce sites and physical locations, ensuring they are in sync.

- Moreover, various retail firms are adopting AI to provide better services to customers. For Example, ThredUp, an online consignment business, introduced Goody Boxes, comprising different used apparel items tailored to each customer's style. Customers keep and pay for the things they want while returning the ones they don't. An AI algorithm recalls each customer's preferences so that future boxes are more tailored to their interests. Customers prefer non-subscription boxes overlooking individual parts.

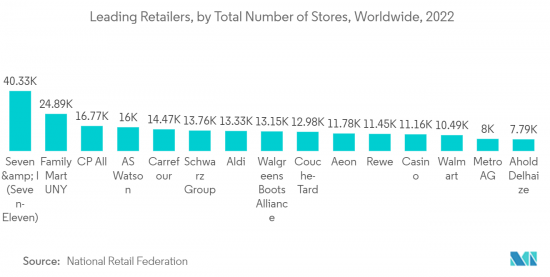

- According to the National Retail Federation, Seven & I Holdings, the parent company of the 7-Eleven retail chain, had over 40,000 retail stores in operation worldwide in 2022. 7-Eleven is a chain of convenience stores that operate in many countries globally. That year, Seven & I had more retail stores than any of the world's leading retail companies, such as Walmart, which had nearly 10,500 retail outlets, or the Schwarz Group, with some 13,750 stores. Although Walmart was not the company with the most locations, it was the world's leading retailer. Such a huge number of retail stores would create an opportunity for market players to develop new solutions to capture the market share.

North America is Expected to Hold a Significant Share.

- The market for artificial intelligence (AI) solutions in various industries is growing in North America, with the United States leading the way. In North America, the readiness for adoption and high fractional growth in replacement AI are the foremost drivers of their economic impact, which reflects the region's leading stance on artificial intelligence and its implementation. Moreover, the high automation potential is expected to occur at the regional level shortly, and it is also aiding the cause.

- According to the National Science and Technology Council report, In Fiscal Year 2022 (FY22), the Federal Government spent USD 8.76 billion USD on research and development in information technology, up USD 410 million or 4.9 percent from the year before. According to the study, USD 2.58 billion was spent on AI research and development in FY22 by all Federal research organizations. This is an increase of USD 130 million (+5.3%) from the prior fiscal year. According to the report, NSF (USD 654 million), NIH (USD 551 million), DARPA (USD 457 million), and the Department of Defense (USD 391 million) were the top funding sources for AI R&D in FY22, with DOE Office of Science (USD 130 million) following closely behind. Such massive spending on Artificial intelligence would create an opportunity for the players to develop new solutions to expand their market share.

- The benefits of AI solutions in the industry would enable the region's food and beverage players to deploy AI to commission new plants. For instance, in February 2023, SunOpta, a global pioneer fueled by the future of sustainable, plant-based, and fruit-based food and beverages, is pleased to announce the launch of its new plant-based beverage production facility in Midlothian, Texas. The new mega-factory will produce a whole line of plant-based milk, creamers, tea, and other items. Package sizes and configurations will include 16-ounce and 32-ounce packages used in food service, shelf-stable retail, and e-commerce for plant-based milk products, as well as 330-milliliter bottles used broadly in high-protein nutritious beverages.

- There is growing evidence that artificial intelligence (AI) is poised to significantly impact the practice of medicine in Canada. The development of the Critical Care Suite and the pneumothorax algorithm was made possible by the launch of GE Healthcare's Edison platform. Edison allows seamless uploading and sharing of images from partnering hospitals and provides a shared Web-based workspace on which radiologists from different organizations can curate and annotate the images, an essential prerequisite to training an algorithm. Humber River Hospital in Toronto, one of four institutions to sign a data-sharing agreement for developing the Critical Care Suite, provided 156,000 privacy-compliant chest X-rays and associated reports to GE Healthcare.

- Further, in September 2023, Google Cloud and technology company Continental announced a strategic partnership to provide innovative, flexible, and future-oriented digital solutions for the automotive industry. The partnership will combine Continental's expertise in automotive technology with Google's data and AI technologies to create a new generation of safe, efficient, and user-focused automotive solutions. Furthermore, the two parties expect to expand their strategic partnership into additional fields of collaboration in the future to build greater in-car connectivity and experiences for customers.

Industrial AI Software Industry Overview

The industrial AI software market exhibits moderate fragmentation and comprises several key players, including Siemens AG, Nvidia Corporation, and Cisco Systems, among others. Market dominance is currently concentrated among a select few major players who employ strategic collaborations to expand their market presence and enhance profitability.

In June 2023, Intrinsic, an Alphabet company, announced a partnership with Siemens to explore integrations and interfaces between Intrinsic's robotics software, designed to facilitate seamless utilization of AI-based capabilities, and Siemens Digital Industries, renowned for its interoperable and open portfolio for industrial production automation and management.

In February 2023, Mastek, a reputable digital engineering and cloud transformation partner, joined forces with Netail, an innovative AI-driven retail software solutions provider. Their strategic alliance aims to empower e-commerce and Omni-channel retailers to optimize their retail value chain while attracting, converting, and retaining digital consumers. Combining Mastek's extensive expertise in digital commerce and data analytics with Netail's cutting-edge AI technology, which plays a pivotal role in decision-making related to product selection, pricing, and customer engagement, will result in a synergistic retail solution. Together, Mastek and Netail will provide online retailers with personalized merchandising, a deeper understanding of consumer behavior, an efficient user experience, a flexible assortment strategy, and real-time market visibility.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Usage of Big Data Technology in Manufacturing

- 5.1.2 Expanding application base and growing emphasis on adoption of digital transformation practices to realize cost savings

- 5.2 Market Restrains

- 5.2.1 Data Privacy Concerns of the Confidential And Legal Data

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Cloud Based

- 6.1.2 On-Premise

- 6.2 By End User Industries

- 6.2.1 Automotive and Transportation

- 6.2.2 Retail and Consumer Packaged Goods

- 6.2.3 Healthcare and Life Science

- 6.2.4 Aerospace and Defense

- 6.2.5 Energy and Utilities

- 6.2.6 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETETIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Intel Corporation

- 7.1.3 Nvidia Corporation

- 7.1.4 Microsoft Corporation

- 7.1.5 Siemens AG

- 7.1.6 Oracle Corporation

- 7.1.7 Cisco Systems, Inc

- 7.1.8 Veritone Inc.

- 7.1.9 Advanced Micro Devices

- 7.1.10 Google Inc

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

法务AI软体的全球市场(~2035年):各元件类型,各部署,价格设定模式,各技术,各应用领域,各终端用户,不同企业规模,不同商业模式,各主要地区,产业趋势,预测内容检测市场预测至 2032 年:按组件、检测方法、内容类型、部署模式、应用、最终用户和地区进行的全球分析

法务AI软体的全球市场(~2035年):各元件类型,各部署,价格设定模式,各技术,各应用领域,各终端用户,不同企业规模,不同商业模式,各主要地区,产业趋势,预测内容检测市场预测至 2032 年:按组件、检测方法、内容类型、部署模式、应用、最终用户和地区进行的全球分析 2025 年至 2029 年软体开发生命週期市场中的全球生成式人工智慧

2025 年至 2029 年软体开发生命週期市场中的全球生成式人工智慧 2025-2029年全球人工智慧写作助理软体市场

2025-2029年全球人工智慧写作助理软体市场 2025-2029年全球AI内容创作工具市场

2025-2029年全球AI内容创作工具市场 全球工业人工智慧软体市场(2025-2029)

全球工业人工智慧软体市场(2025-2029) 全球法律人工智慧软体市场(2025-2029)2032 年人工智慧内容创作市场预测:按类型、组件、技术、应用和地区进行的全球分析AI 内容侦测软体市场(依内容类型、侦测类型和地区)

全球法律人工智慧软体市场(2025-2029)2032 年人工智慧内容创作市场预测:按类型、组件、技术、应用和地区进行的全球分析AI 内容侦测软体市场(依内容类型、侦测类型和地区) 2025年照明改善软体全球市场报告

2025年照明改善软体全球市场报告