|

市场调查报告书

商品编码

1408767

用于加工的半导体装置-市场占有率分析、产业趋势与统计、2024年至2029年的成长预测Semiconductor Device For Processing Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

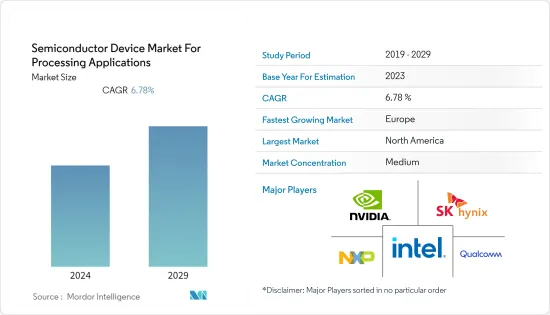

本财年处理半导体装置市场规模预计将达到2,011亿美元,复合年增长率为6.78%,到预测期结束时将达到2,792.6亿美元。

主要亮点

- 半导体产业正在经历快速成长,半导体已成为所有现代技术的基本组成部分。该领域的进步和创新对所有下游技术产生直接影响。

- 半导体构成了所有计算设备的建构模组。例如,许多电晶体组成逻辑闸并处理二进位讯息,即电脑使用的一和零的程式码。这些半导体元件还可以将二进位代码储存为储存区块。

- 随着智慧型手机、个人电脑和笔记型电脑等运算设备的普及,世界各地和网路上即时产生和通讯的资料量正在迅速增加。为了适应这种成长,高效能运算 (HPC) 发挥了关键作用,并且正在经历显着成长。 HPC 是指处理资料、高速执行复杂运算、解决效能集中问题。实现HPC应用需要感测器、光电装置等许多半导体装置。

- 高效能运算 (HPC) 正在成为半导体产业的关键驱动力。

- 此外,COVID-19 的爆发加速了数位平台和云端服务的使用,导致资料中心的发展激增。资料中心是储存和共用应用程式和资料的设施。

- 半导体也是资料中心的关键组件。使用了多种设备,包括中央处理单元 (CPU)、图形处理单元 (GPU)、记忆体、网路基础设施晶片和电源管理。因此,半导体记忆体晶片是资料中心储存和管理资料的重要装置,其效能对于资料中心营运的成功至关重要。

半导体装置市场趋势

积体电路下的记忆体可望带动市场需求

- 半导体记忆体是在积体电路上实现半导体电子元件的数位资料储存装置。记忆体有不同类型,例如 DRAM、SRAM、NOR 快闪记忆体、 NAND快闪记忆体、ROM 和 EPROM。记忆体有DRAM、SRAM、 NAND快闪记忆体、ROM、EPROM等多种类型,广泛应用于电脑、笔记型电脑、相机、行动电话等数位家电。

- 资料中心需求的增加也推动了记忆体组件的需求。目前,北美的大型资料中心计划正在推动对包括DRAM在内的记忆体的强劲需求。然而,以每位用户的资料中心空间衡量,中国的网路资料中心预计将成长至少是美国规模的22倍,至少是日本目前规模的10倍。因此,DRAM拥有巨大的成长机会,正在影响半导体元件产业。

- 此外,便携式系统市场的成长正在推动半导体产业对用于大容量储存应用的非挥发性记忆体(NVM)技术的兴趣。对更高效率、更快记忆体存取和更低功耗的需求不断增长是推动 NVM 市场成长的关键因素。资料中心应用程式越来越需要 NVM 来防止突然断电导致的资料遗失。随着资料中心的增加,下一代非挥发性记忆体的采用也将增加,预计将推动市场成长。

- 此外,根据 WSTS 的数据,2022 年内存组件销售收益预计将达到 1,344.1 亿美元,而 2021 年为 1,548.4 亿美元。然而,内存组件销售收入有所下降,预计为1116.2亿美元,但在不久的将来可能会增长,并在年终实现良好的增长。这些因素可能会促进市场成长。

- 三星正在参与该合作伙伴关係。最终用户可以确信,未来的储存解决方案将得到各种设备供应商和垂直整合的硬体和软体公司的支援。例如,2022 年 3 月,三星电子和西部资料同意合作标准化和普及下一代资料放置、处理和结构 (D2PF) 储存技术。两家公司希望采取这些措施将使行业能够专注于更广泛的应用,并最终为客户带来更多价值。

- 同样在 2022 年 7 月,美光科技宣布已开始量产全球首款采用业界领先创新技术建构的 232 层 NAND,以推动储存解决方案实现前所未有的效能。该公司的232层NAND首次证明3D NAND可以扩展到200层以上,标誌着储存创新的分水岭时刻。

欧洲预计将实现显着成长

- 欧洲地区是全球最重要的技术中心,也是现代科技的重要推手和采用者。先进技术的不断渗透和半导体的日益采用正在推动该地区的市场成长。

- 随着物联网(IoT)的兴起,半导体装置正在整合到各种类型的设备中,扩大了运算和资料储存应用的范围。对这些设备的需求也在稳定成长。材料和架构正在稳步发展,以提高尖端记忆体和逻辑装置、功率半导体装置以及各种感测器的性能。

- 此外,5G 部署预计将实现物联网连接、自动化和边缘技术。具有这种更智慧标准的新设备将要求工厂生产具有更大记忆体和储存容量的更高效能晶圆。

- 5G 网路和技术有望透过改变现有市场领域和产业来进一步革新无线通讯。该公司表示,从2021年到2025年,5G将为欧洲经济所有主要产业创造高达2兆欧元(2.17兆美元)的新销售额。因此,支援 5G 的新设备将需要晶圆厂生产具有更大记忆体和储存容量的更高效能晶圆。

- 2022年3月,英特尔宣布第一阶段计划,未来10年在欧盟投资800亿欧元(868.4亿美元),涵盖整个半导体价值链,包括研发、製造和封装技术。该投资还包括在德国建立半导体製造巨型基地,在法国开发新的研发和设计设施,以及在义大利、波兰、爱尔兰和西班牙投资约170亿日圆用于研发、製造和代工服务。计划投资184.5亿欧元(184.5 亿美元)。

半导体装置产业概况

处理半导体装置市场正在经历适度的碎片化,多个竞争对手在整合加剧、技术进步和不断变化的地缘政治局势中应对波动。在透过创新建立永续竞争优势至关重要的市场中,这种竞争的加剧可能会变得更加激烈。鑑于半导体製造业最终用户的品质期望,品牌标誌在这一形势发挥着至关重要的作用。

市场渗透率异常高,主要是由于英特尔公司、英伟达公司、京瓷公司和高通技术公司等重要的行业领导者的存在。

2022 年 4 月,SK 海力士与其位于圣荷西的子公司 Solidigm 合作,推出了专为资料中心设计的最新固态硬碟 (SSD),称为 P5530。 SSD利用快闪记忆体来储存资料,这款创新设备将SK Hynix的旗舰128层4D NAND与Solidigm的SSD控制器结合。

2022 年 3 月,三星电子和西部资料同意就下一代资料放置、处理和结构 (D2PF) 储存技术的标准化和普及进行合作。两家公司的共同努力旨在简化行业实践并实现更广泛的应用,最终为客户带来更大的价值。

2022 年 1 月,铠侠宣布推出通用快闪记忆体储存 (UFS) 3.1 版嵌入式快闪记忆体装置。这些元件利用该公司开创性的每单元 4 位元四级单元 (QLC) 技术,能够在单一封装中实现最高密度。该技术特别适合高阶智慧型手机等高密度应用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 科技趋势

- 产业价值链/供应链分析

- 产业吸引力波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 宏观经济走势对市场的影响

第五章市场动态

- 市场驱动因素

- 扩大物联网和人工智慧等技术的采用

- 5G的普及和资料中心需求的增加

- 市场挑战

- 供应链中断导致半导体晶片短缺

第六章市场区隔

- 依设备类型

- 离散半导体

- 光电子学

- 感应器

- 积体电路

- 模拟

- 逻辑

- 记忆

- 微

- 微处理器 (MPU)

- 微控制器(MCU)

- 数位讯号处理器

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争形势

- 公司简介

- Intel Corporation

- Nvidia Corporation

- Qualcomm Incorporated

- NXP Semiconductors NV

- SK Hynix Inc.

- Kyocera Corporation

- Samsung Electronics Co., Ltd.

- Advanced Micro Devices, Inc

- ST microelectronics Nv

- Micron Technology Inc.

- Toshiba Electronic Devices And Storage Corporation

- Infineon Technologies AG

第八章投资分析

第9章市场的未来

The semiconductor device market for processing applications is estimated at USD 201.1 billion in the current year, registering a CAGR of 6.78%, to reach USD 279.26 billion by the end of the forecast period.

Key Highlights

- The semiconductor industry is witnessing rapid growth, with semiconductors emerging as the basic building blocks of all modern technology. The advancements and innovations in this field are resulting in a direct impact on all downstream technologies.

- Semiconductors form the building blocks of any computing device. For instance, many transistors make up a logic gate that processes binary information, the code of ones and zeros computers use. These semiconductor devices can also retain binary code as memory blocks.

- With the growing popularity of computing devices like smartphones, PCs, and laptops, the amount of data generated and communicated across a global network, often in real-time, has grown rapidly. To keep up with this growth, High-performance computing (HPC) has become crucial and is seeing significant growth. HPC refers to processing data and performing complex calculations at high speeds to solve performance-intensive problems. Many semiconductor devices like sensors and optoelectronics are required to enable HPC applications.

- High-performance computing (HPC) has emerged as an important growth driver for the semiconductor industry. For instance, Taiwan Semiconductor Manufacturing Co. (TSMC) expects the HPC platform to be the strongest-growing platform in 2022 and the largest contributor to the company's growth, fueled by the structural mega-trend, driving rising needs for higher computing power and energy-efficient computing.

- Further, the COVID-19 pandemic accelerated the use of digital platforms and cloud services, resulting in a surge in data center development. A data center is a facility that stores and shares applications and data.

- Also, semiconductors serve as a primary component for data centers. Different devices are used, like central processing units (CPUs), graphics processing units (GPUs), memory, chips for network infrastructure, and power management. Therefore, semiconductor memory chips are the key devices for storing and managing data in data centers, and their performance is crucial to the success of data center operations.

Semiconductor Device Market Trends

Memory Segment Under Integrated Circuits is Expected to Boost The Demand in The Market

- The semiconductor memory is a digital electronic data storage device implemented with semiconductor electronic devices on an integrated circuit. Different types of memory are available, such as DRAM, SRAM, Nor Flash, NAND Flash, ROM, and EPROM. They find widespread application in digital consumer products like PCs, laptops, cameras, and phones.

- The increasing demand for data centers is also bolstering the demand for memory components. Currently, large data center projects in North America have contributed to the strong demand for memory, such as DRAM. However, according to the measure of data center space per user, China's internet data centers are poised to grow to at least 22 times that of the United States or at least 10 times the current space of Japan. Hence, DRAM has a significant opportunity for growth and thus is impacting the semiconductor device industry.

- Further, the growth of the portable systems market attracted the semiconductor industry's interest in non-volatile memory (NVM) technologies for mass storage applications. The rise in demand for greater efficiency, faster memory access, and low power consumption are some of the significant factors driving the NVM market growth. There is an increasing need for NVM in data center applications to protect data losses from a sudden power outage. With the growth of data centers, the adoption of next-generation non-volatile memory is also expected to increase, driving market growth.

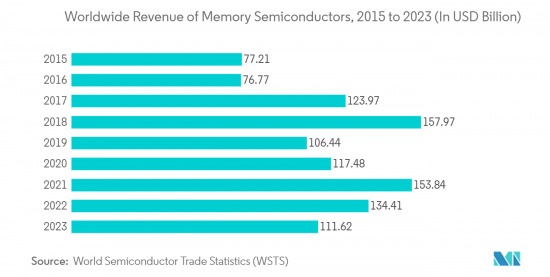

- Moreover, according to WSTS, In 2022, it is projected that revenue from memory component sales will amount to USD 134.41 billion, and in 2021 the recorded revenue of USD 154.84 billion. However, the revenue from memory component sales decreased, with an estimated amount of USD 111.62 billion, but it is likely to grow in the near future, and by the end of 2023, it will achieve good growth. Such factors are likely to boost the market growth.

- Samsung participates in partnerships; end users may be sure that various device suppliers and vertically integrated hardware and software firms will support its upcoming storage solutions. For instance, in March 2022, Samsung Electronics and Western Digital agreed to work together to standardize and promote next-generation data placement, processing, and fabrics (D2PF) storage technologies. They hope that by taking these steps, the industry will be able to concentrate on a wide range of applications that will ultimately provide customers with more value.

- Also, in July 2022, Micron Technology, Inc. announced that it had begun volume production of the world's first 232-layer NAND, built with industry-leading innovations to drive unprecedented performance for storage solutions. The company's 232-layer NAND is a watershed moment for storage innovation as the first proof of the capability to scale 3D NAND to more than 200 layers in production.

European Region Expected to Witness the Significant Growth

- The European region is home to some of the most crucial technology hubs across the globe and a critical driver and adopter of modern technology. The increasing penetration of advanced technologies and the increasing adoption of semiconductors drives market growth in the region.

- With the rise of the Internet of Things (IoT), semiconductor devices are being incorporated into all types of devices, with a wider range of computing and data storage applications. Demand for these devices is also steadily increasing. Materials and architecture are steadily evolving to improve the performance of cutting-edge memory and logic devices, power semiconductor devices, and various types of sensors.

- Furthermore, the rollout of 5G is perceived to be the enabler of IoT connectivity, automation, and edge technologies. New devices in this smarter standard will require fabs to produce higher-performing wafers with even greater capacity for memory and storage.

- 5G networks and technology are further revolutionizing wireless communications by transforming existing market sectors and industries. As per the company, between 2021 and 2025, 5G will drive up to EUR 2.0 trillion (USD 2.17 trillion) in total new sales across all major industries in the European economy. As such, new devices that enable 5G will require fabs to produce higher-performing wafers with even greater capacity for memory and storage.

- In March 2022, Intel issued the first phase of its EUR 80 billion (USD 86.84 billion) investment plan in the EU over the next decade across the semiconductor value chain, including R&D, manufacturing, and packaging technologies. Further in this investment, the company plans to invest approximately EUR 17 billion (USD 18.45 billion) in establishing a semiconductor fab mega-site in Germany, as well as the development of a new R&D and design facility in France, and to invest in R&D, manufacturing, and foundry services in Italy, Poland, Ireland, and Spain.

Semiconductor Device Industry Overview

The semiconductor device market for processing applications is experiencing moderate fragmentation, with several competitors navigating fluctuations amidst growing consolidation, technological advancements, and evolving geopolitical scenarios. This heightened competition is set to intensify in a market where establishing a sustainable competitive advantage through innovation is of paramount importance. Given the expectations of quality from end-users in the semiconductor manufacturing sector, brand identity plays a pivotal role in this landscape.

The market penetration levels are notably high, primarily due to the presence of significant market incumbents such as Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and other industry leaders.

In April 2022, SK Hynix Inc. introduced its latest solid-state drive (SSD), known as the P5530, designed for data centers in collaboration with its San-Jose-based subsidiary, Solidigm. SSDs leverage flash memory to store data, and this innovative device combines SK Hynix's 128-layer 4D NAND, a core product, with Solidigm's SSD controller.

In March 2022, Samsung Electronics and Western Digital reached an agreement to collaborate on standardizing and promoting next-generation data placement, processing, and fabrics (D2PF) storage technologies. Their joint efforts aim to streamline industry practices, allowing for a broader array of applications that ultimately deliver greater value to customers.

In January 2022, Kioxia Corporation announced the launch of Universal Flash Storage (UFS) Ver. 3.1 embedded flash memory devices. These devices harness the company's pioneering 4-bit per cell quad-level-cell (QLC) technology, which has the capability to achieve the highest densities available in a single package. This technology is particularly suited for high-density applications like high-end smartphones

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Industry Attractiveness Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of the Macroeconomics Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Technologies Like IoT And AI

- 5.1.2 Increased Deployment of 5G And Rising Demand For Data Centers

- 5.2 Market Challenges

- 5.2.1 Supply Chain Disruptions Resulting In Semiconductor Chip Shortage

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processors

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Qualcomm Incorporated

- 7.1.4 NXP Semiconductors NV

- 7.1.5 SK Hynix Inc.

- 7.1.6 Kyocera Corporation

- 7.1.7 Samsung Electronics Co., Ltd.

- 7.1.8 Advanced Micro Devices, Inc

- 7.1.9 ST microelectronics Nv

- 7.1.10 Micron Technology Inc.

- 7.1.11 Toshiba Electronic Devices And Storage Corporation

- 7.1.12 Infineon Technologies AG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

半导体拆解服务市场按服务类型、最终用户、应用、技术节点、设备类型和经营模式划分-2025-2032年全球预测

半导体拆解服务市场按服务类型、最终用户、应用、技术节点、设备类型和经营模式划分-2025-2032年全球预测 2025年全球工业半导体市场报告

2025年全球工业半导体市场报告 低功耗半导体雷达系统市场分析与预测(2034年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能

低功耗半导体雷达系统市场分析与预测(2034年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能 2032 年宽能带隙半导体市场预测:按材料类型、设备类型、组件类型、最终用户和地区进行的全球分析

2032 年宽能带隙半导体市场预测:按材料类型、设备类型、组件类型、最终用户和地区进行的全球分析 全球工业半导体市场:成长机会(2024-2029)

全球工业半导体市场:成长机会(2024-2029) 感光半导体装置市场规模、份额、成长分析(按设备、应用和地区)- 产业预测,2025 年至 2032 年

感光半导体装置市场规模、份额、成长分析(按设备、应用和地区)- 产业预测,2025 年至 2032 年 全自动探针台的全球市场全球光敏半导体元件市场

全自动探针台的全球市场全球光敏半导体元件市场 全球可程式逻辑装置(PLD) 市场,2025-2029 年

全球可程式逻辑装置(PLD) 市场,2025-2029 年 日本半导体设备市场(2025-2029)

日本半导体设备市场(2025-2029)