|

市场调查报告书

商品编码

1408868

工业半导体装置:市场占有率分析、产业趋势/统计、2024年至2029年成长预测Semiconductor Device For Industrial Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

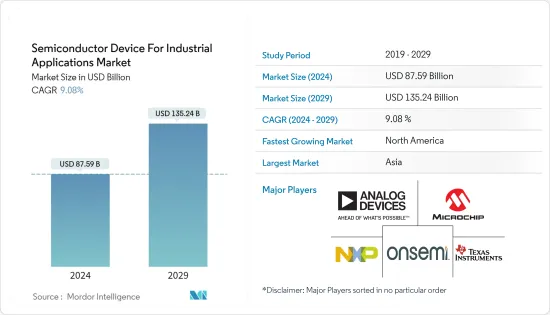

工业半导体装置市场规模预计2024年为875.9亿美元,预计2029年将达到1,352.4亿美元,在预测期间(2024-2029年)复合年增长率为9.08%成长。

主要亮点

- 工业自动化的快速发展导致工业应用中越来越多地采用半导体装置。工业 4.0 正在改变公司製造产品的方式。工业 4.0 是指智慧型互联生产系统,旨在感知、预测或与物理世界交互,以做出支援生产的即时决策。工业 4.0 可以提高製造生产力、能源效率和永续性。

- 工业4.0最重要的组成部分之一是工业物联网,它是指物联网在工业领域和应用中的扩展和使用。工业物联网中半导体的基本核心功能包括感测、连接和运算。例如,在工业物联网中,感测器广泛应用于各个行业,以监控设备、资产、系统和整体效能。

- 工业机器人是工业 4.0 的另一个关键推动者,也是半导体的常见应用领域,它是经过编程的机械设备,可在工业环境中自动执行与生产相关的任务。

- 为了发挥作用,工业机器人需要先进的感测器来捕获关键资讯。感测器可以使用半导体处理单元来收集外部资讯,例如影像、红外线、声音、内部温度、湿度、运动和位置资料。许多工业机器人现在都配备了 3D 视觉系统,通常由多个摄影机和一个或多个雷射位移感测器组成。

- 半导体产业的供需受到了 COVID-19 的显着影响。製造地停工和政府封锁严重影响了世界各地的生产和供应链。工业4.0意识的增强和智慧型工厂的频繁采用加速了随后的市场成长。

工业半导体装置市场趋势

感测器领域在工业应用中占据主要份额

- 感测器是工厂自动化和工业 4.0 的重要组成部分。运动、环境和振动感测器透过线性和角度定位、倾斜检测、调平以及衝击跌落侦测来监控设备的健康状况。

- 基于微加工感测 (MEMS) 元件的专用工业运动感测器可用于工业 4.0 应用。它们具有宽机械频率感测频宽、高可靠性以及高达 105°C 的精确操作。

- 工业感测器系统通常由 24V 直流电源供电,这与消费性系统中由 3V 或 5V 电源供电的感测器有很大不同。因此,工业感测器系统需要额外的电源管理来有效驱动感测器。这些系统使用 IO-Link 等数位输出直接连接到微控制器和无线收发器。

- 被动红外线 (PIR) 感测器或旋转编码器可以成为工业自动化系统中阈值测量的限位交换器。这些工业物联网(IIoT)感测器透过有线或无线工业感测器网路连接到网关,而网关连接到物联网进行即时分析和状态监测。

- 这些感测器通常价格便宜,因为安装和操作所需的时间较短。连接到现有机械的无线感测器和覆盖解决方案具有成本效益,因为它们使用一组标准技术。

- 工业机器人的采用不断增加,并成为实现工业 4.0 的重要元素。为了发挥作用,工业机器人需要先进的感测器来收集关键资料。除了温度、湿度、运动和位置等内部资料外,感测器还采用半导体处理单元,可收集影像、红外线辐射和声音等外部资料。

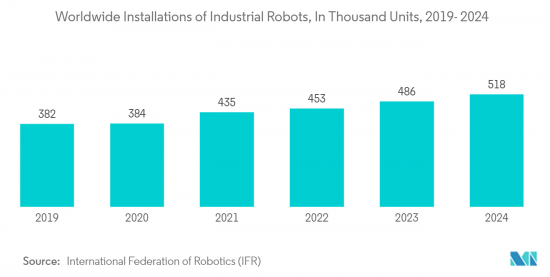

- 据国际机器人联合会(IFR)称,工业机器人的销售量预计将激增。预计2024年,全球工业机器人出口量将达到518万台。这一事实将对工业机器人製造中感测器的采用发挥重要作用,例如 2D/3D 视觉和力/扭矩感测器。

亚洲地区的市场成长显着。

- 亚洲包括中国、日本、印度、韩国和其他亚洲地区。中国正在投资下一代技术并迅速实现工业自动化,在新技术和创新投资方面超过了西方国家。

- 例如,机器人技术在中国工业中的普及。根据《南华早报》报道,2023年上半年中国生产工业机器人222万台,年增5.4%。据工信部数据显示,服务机器人产量353万台,成长9.6%。工业机器人引进的巨大成长率可能会在预测期内推动研究市场的发展。

- COVID-19的发展迫使日本工业部门重新审查既定的生产程序。日本在工业经济自动化方面处于领先地位。日本现在可以透过工业中心向其他地区提供工厂自动化产品。此外,我们也向其他国家出口工厂自动化和工业控制设备。机器人的普及以及具有人工智慧功能的机器人的兴起引发了新技术的诞生,以帮助企业提高生产力并最大限度地减少错误。

- 同样,印度也受益于自动化在推动成长和竞争形势中的关键作用,其产业形势正在发生重大转变。过去几年,印度製造业一直在走向自动化。对此,许多全球企业都有兴趣在印度投资智慧型工厂製造。例如,2022年12月,Schneider Electric计画投资42.5亿印度卢比(约51.3亿美元)在印度班加罗尔开发一座新的智慧工厂。这些趋势可能会在预测期内推动市场成长。

工业半导体装置产业概况

工业半导体装置市场的特点是竞争激烈且碎片化,许多全球和本地公司积极参与。该领域的主要企业包括 Analog Devices Inc.、NXP Semiconductors NV、Microchip Technology Inc.、ON Semiconductor Corporation 和 Texas Instruments Incorporated。这些公司不断追求技术创新并促进与其他行业领导者的合作以保持竞争力。

2023 年 3 月,恩智浦半导体宣布推出 UCODE 9xm。 UCODE 9xm 是一款突破性产品,它将扩充性、适应性强的记忆体与顶级的读写效能相结合。 UCODE 9xm 有助于使用更小的标籤天线,允许对更小的物品进行单独标记并无缝整合到智慧製造流程、供应链管理和追踪应用中。这项演变旨在提高系统的整体可靠性和准确性,为使用者提供标记更广泛的物件类型的多功能性,并带来更全面的供应链视图。

2022 年 6 月,ADI 公司宣布推出 ADTF3175 模组,这是一款工业级高解析度间接飞行时间 (iToF) 解决方案,专为 3D 深度感测和视觉系统而设计。这项创新模组使相机和感光元件能够以令人难以置信的 100 万像素解析度感知 3D 空间,使其适合工业自动化领域的应用。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链/供应链分析

- 评估宏观趋势对市场的影响

第五章市场动态

- 市场驱动因素

- 人们对工业 4.0 和智慧工厂的认识不断增强

- 市场抑制因素

- 半导体短缺限制市场扩张

第六章市场区隔

- 设备类型

- 离散半导体

- 光电子学

- 感应器

- 积体电路

- 模拟

- 逻辑

- 记忆

- 微

- 微处理器

- 微控制器

- 数位讯号处理器

- 地区

- 美国

- 欧洲

- 日本

- 中国

- 韩国

- 台湾

- 世界其他地区

第七章 竞争形势

- 公司简介

- Analog Devices Inc.

- Microchip Technology Inc.

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Texas Instruments Incorporated

- Infineon Technologies AG

- AMS Technologies AG

- STMicroelectronics

- Renesas Electronics Corporation

- Rohm Co. Ltd

第八章投资分析

第九章 市场未来展望

The Semiconductor Device For Industrial Applications Market size is estimated at USD 87.59 billion in 2024, and is expected to reach USD 135.24 billion by 2029, growing at a CAGR of 9.08% during the forecast period (2024-2029).

Key Highlights

- Semiconductor devices are increasingly adopted in industrial applications owing to the rapid growth in industrial automation. Industry 4.0 is transforming the way companies manufacture their products. Industry 4.0 refers to intelligent and connected production systems designed to sense, predict, or interact with the physical world, making real-time decisions that support production. It can increase productivity, energy efficiency, and sustainability in manufacturing.

- One of the most critical components of Industry 4.0 is the Industrial Internet of Things, which indicates the extension and use of the IoT in industrial sectors and applications. Semiconductors' underlying core capabilities for IIoT include sensing, connectivity, and computing. For instance, in IIoT, sensors are widely used in different industries to monitor equipment, assets, systems, and overall performance.

- Another critical enabler of Industry 4.0 and a common area of application of semiconductors is industrial robots, which are mechanical machines programmed to automatically perform production-related tasks in industrial environments.

- For their functioning, industrial robots require sophisticated sensors that obtain essential information. Sensors can use semiconductor processing units to gather external information like images, infrared light, sound, internal temperature, moisture, movement, and position data. Currently, many industrial robots are equipped with 3D vision systems, usually comprised of multiple cameras or one or more laser displacement sensors.

- The semiconductor industry's supply and demand were both significantly impacted by COVID-19. The shutdown of manufacturing sites and government-induced lockdowns severely affected the production and supply chain of the entire globe. The growing awareness of Industry 4.0 and the frequent adoption of intelligent factories accelerated market growth in the following years.

Semiconductor Device For Industrial Applications Market Trends

Sensor Segment to Hold a Significant Share in Industrial Applications

- Sensors are a vital part of factory automation and Industry 4.0. Motion, environmental, and vibration sensors monitor equipment health, ranging from linear or angular positioning, tilt sensing, leveling, and shock to fall detection.

- Dedicated industrial motion sensors based on micromachined sensing (MEMS) elements are available for Industry 4.0 applications. These have a wide mechanical frequency sensing bandwidth, high reliability, and accurate operation up to 105°C.

- An industrial sensor system is often powered by a 24V DC source, which is very different from a sensor in a consumer system powered by a 3V or 5V source. As a result, industrial sensor systems require additional power management to drive the sensors effectively. These use digital outputs, such as IO-Link direct to a microcontroller or the wireless transceiver.

- Passive infrared (PIR) sensors and rotary encoders can be limit switches for threshold measurements in industrial automation systems. Such industrial Internet of Things (IIoT) sensors are linked through industrial sensor networks, either wired or wireless, back to a gateway and then back to the Internet of Things to provide real-time analysis and conditional monitoring.

- These sensors are generally cheaper because they take less time to install and run. A wireless sensor or overlay solution attached to an existing machine is cost-effective, as it uses a standard technology set.

- Industrial robotics adoption is increasing, an essential enabler of Industry 4.0. Industrial robots need sophisticated sensors to gather crucial data for them to function. In addition to internal data on temperature, moisture, movement, and position, sensors can employ semiconductor processing units to collect external data from sources, including pictures, infrared light, and sound.

- According to the International Federation of Robotics (IFR), industrial robot sales are anticipated to rise sharply. Global exports of industrial robots are predicted to reach 5,18,000 units in 2024. This fact will play a significant role in adopting sensors in manufacturing industrial robots such as 2D and 3D vision and force or torque sensors; collision sensors are widely used in it.

Asia Region to Grow Significantly in this Market

- Asia includes China, Japan, India, Korea, and the rest of Asia. China is investing in next-generation technologies, quickly automating the industry, and even positioned to surpass the Western countries in terms of new technology investment and innovation.

- For instance, in the widespread use of robotics in the Chinese industry. According to the South China Morning Post, China produced 2,22,000 industrial robotic units in the first half of 2023, an increase of 5.4% compared to the same period last in 2022. According to Ministry figures, it also generated 3.53 million service robot units, a 9.6% increase. This tremendous growth rate in installing industrial robots will drive the studied market during the forecast period.

- The development of COVID-19 forced the Japanese industrial sector to reexamine its established production procedures. Japan has led the automation of the industrial economy. The nation can now provide factory automation products to other regions through its industrial center. Additionally, it exports factory automation and industrial controls to other countries. Robot proliferation and the rise of robots with AI capabilities have sparked the creation of new technologies that may aid businesses in enhancing productivity and minimizing errors.

- Similarly, India is benefiting from the critical role of automation in driving growth and competitiveness, which has seen a remarkable transformation of its industrial landscape. Over the last few years, India's manufacturing sector has been moving towards automation. Regarding this, many global companies are interested in investing in the manufacturing of intelligent factories in India. For instance, in December 2022, Schneider Electric plans to invest INR 425 crore (around USD 5.13 billion) to develop a new smart factory in Bangalore, India. These trends will drive the studied market growth during the projected period.

Semiconductor Device For Industrial Applications Industry Overview

The semiconductor device market for industrial applications is characterized by fierce competition and fragmentation, with a multitude of global and local players actively participating in the industry. Key companies in this domain include Analog Devices Inc., NXP Semiconductors NV, Microchip Technology Inc., ON Semiconductor Corporation, and Texas Instruments Incorporated, among others. These players continually pursue innovation and foster collaborations with other industry leaders to remain competitive.

In March 2023, NXP Semiconductors unveiled the UCODE 9xm, a revolutionary product that combines expansive, adaptable memory with top-tier read/write performance. The UCODE 9xm facilitates the utilization of smaller tag antennas, making it possible to individually tag smaller items and seamlessly integrate them into smart manufacturing processes, supply chain management, and tracking applications. This advancement is aimed at enhancing the overall reliability and precision of the system, offering users greater versatility in tagging a wider variety of object types, thus leading to a more comprehensive understanding of the supply chain.

In June 2022, Analog Devices made an exciting announcement about the launch of the ADTF3175 module, an industrial-grade, high-resolution indirect Time-of-Flight (iToF) solution designed for 3D depth sensing and vision systems. This innovative module empowers cameras and sensors to perceive 3D space with an impressive one-megapixel resolution, rendering it suitable for applications within the realm of industrial automation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact Assessment of Macro Trends on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Awareness for Industry 4.0 and Smart factories

- 5.2 Market Restraints

- 5.2.1 Shortage of Semiconductors Limits Market Expansion

6 MARKET SEGMENTATION

- 6.1 Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessor

- 6.1.4.4.2 Microcontroller

- 6.1.4.4.3 Digital Signal Processors

- 6.2 Geography

- 6.2.1 United States

- 6.2.2 Europe

- 6.2.3 Japan

- 6.2.4 China

- 6.2.5 Korea

- 6.2.6 Taiwan

- 6.2.7 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Analog Devices Inc.

- 7.1.2 Microchip Technology Inc.

- 7.1.3 NXP Semiconductors NV

- 7.1.4 ON Semiconductor Corporation

- 7.1.5 Texas Instruments Incorporated

- 7.1.6 Infineon Technologies AG

- 7.1.7 AMS Technologies AG

- 7.1.8 STMicroelectronics

- 7.1.9 Renesas Electronics Corporation

- 7.1.10 Rohm Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

半导体拆解服务市场按服务类型、最终用户、应用、技术节点、设备类型和经营模式划分-2025-2032年全球预测

半导体拆解服务市场按服务类型、最终用户、应用、技术节点、设备类型和经营模式划分-2025-2032年全球预测 2025年全球工业半导体市场报告

2025年全球工业半导体市场报告 低功耗半导体雷达系统市场分析与预测(2034年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能

低功耗半导体雷达系统市场分析与预测(2034年):类型、产品、服务、技术、组件、应用、设备、部署、最终用户和功能 2032 年宽能带隙半导体市场预测:按材料类型、设备类型、组件类型、最终用户和地区进行的全球分析

2032 年宽能带隙半导体市场预测:按材料类型、设备类型、组件类型、最终用户和地区进行的全球分析 全球工业半导体市场:成长机会(2024-2029)

全球工业半导体市场:成长机会(2024-2029) 感光半导体装置市场规模、份额、成长分析(按设备、应用和地区)- 产业预测,2025 年至 2032 年

感光半导体装置市场规模、份额、成长分析(按设备、应用和地区)- 产业预测,2025 年至 2032 年 全自动探针台的全球市场全球光敏半导体元件市场

全自动探针台的全球市场全球光敏半导体元件市场 全球可程式逻辑装置(PLD) 市场,2025-2029 年

全球可程式逻辑装置(PLD) 市场,2025-2029 年 日本半导体设备市场(2025-2029)

日本半导体设备市场(2025-2029)