|

市场调查报告书

商品编码

1432584

蒸发冷却:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Evaporative Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

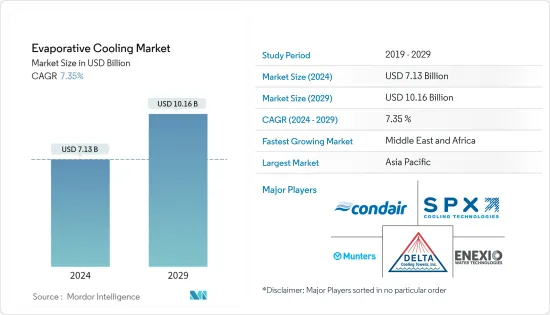

蒸发冷却市场规模预计到 2024 年为 71.3 亿美元,预计到 2029 年将达到 101.6 亿美元,在预测期内(2024-2029 年)复合年增长率为 7.35%。

主要亮点

- 气候变迁使热浪更加频繁,使数百万人面临暴露在致命高温下的风险。随着世界各地的人们感受到气温上升的影响,迫切需要在不减少碳排放下满足冷却需求。

- 蒸发冷却器会用比空调系统更少的零件(例如风扇、帮浦和水)来冷却房间,因此它们可以以一小部分成本和最低的营业成本来冷却各种空间。这种蒸发冷却系统的主要优点之一是拥有低成本。

- 此外,世界各国政府也提供储蓄计画来推广节能技术。例如,蒸发冷却已被证明是一种永续的冷却技术,因此这些系统有资格获得荷兰的能源投资补贴(EIA),可提供超过11%的整体投资净回报。

- 此外,这些系统使用的零件更少,能源效率更高,使蒸发冷却成为市场上最实惠的冷却选项之一。例如,Canstar Blue 估计典型的逆循环分离式系统空调的运作成本约为每小时 0.60 美元。然而,如果在水中添加 0.02 美元,蒸发冷却系统的成本将低于每小时 0.10 美元。

- 这些蒸发冷却系统的主要缺点之一是它们高度依赖周围空气的品质。蒸发冷却过程是由周围空气的干球温度和湿球温度之间的温差驱动的,在中等或高湿度的地区可以忽略不计,从而限制了冷却能力。

- 与此同时,印度供暖、冷冻和空调工程师协会 (ISHRAE) 以及其他全球监管机构敦促在当前的大流行情况下增加新鲜空气的摄入和通风。这迫使最终用户考虑安装蒸发冷却系统。蒸发冷却系统有潜力显着改善室内空气质量,并在使用更少能源的同时提供更安全的工作空间。

蒸发冷却市场趋势

直接蒸发冷却占有很大份额

- 透过利用将液态水转化为水蒸气的汽化潜热,直接蒸发冷却可以降低温度并增加空气湿度。这是最基本、最传统的蒸发冷却类型,应用广泛。预计这些蒸发式空调在美国南部的利基市场有限,因为 7 月中旬的相对湿度超过 40%。

- 直接蒸发冷却系统也适用于需要大量热负荷更换并且愿意使用外部空气来实现这一目的的应用。广泛应用于舒适度标准宽鬆的建筑、仓库、商务用厨房、住宅。因此,系统要求取决于最终使用者和既定的操作性能标准。大多数建筑物的蒸发冷却系统是自然的,但也有间接类型。

- 在大规模部署直接蒸发冷却器的推动下,工业领域在所有最终用户应用中占据了最大的市场占有率。直接蒸发冷却器的工业应用包括建筑物、仓库、工厂、製造单位、发电、石油和天然气、建筑等。

- 此外,工业部门正在实施先进的蒸发冷却系统,以便在问题发生之前预测维护需求。现代冷却技术采用物联网 (IoT) 技术,包括感测器、连接、软体和其他允许系统与其他连接设备通讯的组件。物联网解决方案透过收集有关设备健康状况和空气品质的资讯来增强预防性保养。

- 因此,许多公司都专注于直接蒸发冷却 (DEC),这是最节能的资料中心冷却方法。例如,为了发展其资料中心冷却部门(包括自然蒸发冷却),Munters 于 2021 年 4 月将其维吉尼亚员工转移到新设施。这座占地 365,000 平方英尺的生产、研发和销售设施是该公司 3,600 万美元的投资目标。

亚太地区占主要市场占有率

- 预计东南亚地区空调销售需求强劲,在气温上升和收益增加的推动下,到2040年空调销售量预计将达到3亿台,其中印尼预计将供应全球空调台的一半。

- 此外,根据国际能源总署的研究,冷却设备的销售主要在中国、美国和日本,其中印度和印尼的销售量增幅最为显着。虽然中国过去十年销售超过5亿台,但印度和印尼的空调需求成长相对较快,两国安装量年均成长超过15%。 (印度)

- 南亚地区对空调的需求快速成长,需要经济且简单的冷却技术。考虑到这些国家的碳排放目标,蒸发冷却是最好的解决方案之一。东南亚是亚太地区成长最快的资料中心市场之一。

- 然而,随着微软、谷歌和苹果等世界领先的科技公司製定了碳中和和零可持续性目标的标准,随着尖端节能技术的开发,永续性将成为资料中心提供商之间的关键差异化因素在亚洲。

- 资料中心冷却占总能源需求的 35% 至 40%,使其成为亚洲永续性的主要障碍。目前,亚洲大多数资料中心都采用风冷,这是一种效率极低且昂贵的解决方案。

- 该地区的公司正在转向蒸发冷却技术。例如,蒸发冷却等冷却技术使资料中心永续。随着资料中心越来越需要满足数位化的需求,这些技术使公司能够采用间接蒸发式、直接蒸发式、混合系统和液体冷却来提高电力使用效率(PUE),并整体减少能源使用。

蒸发冷却产业概述

蒸发冷却市场竞争适中,由多家大型企业组成。从市场占有率来看,目前几家大公司占据市场主导地位。凭藉主导市场占有率,这些领先公司正专注于扩大海外基本客群。主要企业包括 Delta Cooling Towers Inc.、Condair Group AG 和 SPX Cooling Technologies 等公司。竞争和快速的技术进步预计将在预测期内对公司的成长构成威胁。

2023年5月,小米有品推出米家智慧蒸发冷风扇,提供顾客清爽舒适的室内环境。该公司推出的智慧电风扇旨在实现通风、降温、加湿三效合一。配备循环水冷却系统,可透过添加水或结晶来提供各种冷却效果。创新的无线水箱专利设计,随时可将水箱从主机上拆下清洗,卫生便捷。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- 评估 COVID-19 对产业的影响

- 蒸发冷却热点分析

- 住宅和商业领域部署的替代/替代冷却技术的比较分析

第五章市场动态

- 市场驱动因素

- 对经济高效的冷却解决方案的需求

- 市场限制因素

- 对外部气候的依赖

第六章市场区隔

- 按冷却方式分

- 直接蒸发冷却

- 间接蒸发冷却

- 两级蒸发冷却

- 按用途

- 住宅

- 商业用途

- 工业的

- 农场

- 其他用途

- 按分销管道

- 大型零售店

- 暖通空调承包商和经销商

- 其他分销管道

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争形势

- 公司简介

- Delta Cooling Towers Inc.

- Condair Group AG

- SPX Cooling Technologies

- Baltimore Aircoil Company Inc.

- Munters Group AB

- Colt Group Limited

- Phoenix Manufacturing Inc.

- Bonaire

- ENEXIO Water Technologies GmbH

- CFW Evapcool

- Celsius Design Limited

第八章投资分析

第9章 未来趋势

The Evaporative Cooling Market size is estimated at USD 7.13 billion in 2024, and is expected to reach USD 10.16 billion by 2029, growing at a CAGR of 7.35% during the forecast period (2024-2029).

Key Highlights

- As heat waves happen more frequently owing to climate change, millions of people are in danger of exposure to temperatures that could be fatal. People worldwide have been impacted by rising temperatures, making it imperative to address the need for cooling without having a negative carbon footprint, which has been a significant element driving the industry.

- Because evaporative coolers employ fewer parts than air conditioning systems, such as a fan, pump, and water, to chill the room, they can cool various spaces for a meager cost and with minimal operational costs. These evaporative cooling systems' low ownership costs are one of their main benefits.

- Additionally, various governments worldwide have been offering saving programs to promote energy-efficient technologies. For example, as evaporative cooling has been a proven sustainable cooling technology, these systems have been made eligible for the Energy Investment Deduction (EIA) in the Netherlands, which could result in more than 11% net benefit on the entire investment.

- Furthermore, because these systems use fewer components and are, therefore, more energy efficient, evaporative cooling has been one of the most affordable cooling options on the market. For instance, Canstar Blue estimates that the typical reverse cycle split system air conditioner may run at about USD 0.60 per hour. However, with an additional USD 0.02 for water, an evaporative cooling system may cost less than USD 0.10 per hour.

- These evaporative cooling systems' high reliance on the surrounding air quality has been one of their main disadvantages. Since the evaporative cooling process is driven by the temperature difference between the ambient air's dry and wet bulb temperatures, this difference is negligible for moderate and highly humid regions, which results in a constrained cooling capacity.

- On the other hand, the Indian Society of Heating, Refrigerating and Air Conditioning Engineers (ISHRAE), among other regulating authorities globally, has urged more fresh air intake and ventilation in the current pandemic scenario. Due to this, end users are now compelled to consider integrating evaporative cooling systems, which might significantly improve indoor air quality and offer secure workspaces with less energy use.

Evaporative Cooling Market Trends

Direct Evaporative Cooling to Hold a Major Share

- By utilizing the latent heat of evaporation, which transforms liquid water into water vapor, direct evaporative cooling reduces the temperature and raises air humidity. It is the most basic, traditional, and widely utilized form of evaporative cooling. These evaporative coolants are anticipated to have a limited niche market in the United States, mainly in the south, where the relative humidity at noon in July is above 40%.

- The direct evaporative cooling systems are also appropriate for applications that require significant heat-load replacement and are willing to use outside air to do it. Their applications are widely used in buildings, warehouses, commercial kitchens, and residential settings with laxer comfort standards. The system requirements, therefore, depend on the end users and the established operational performance criteria. Most buildings' evaporative coolers are natural systems, while some indirect ones are also employed.

- The industrial sector accounts for the largest market share among all end-user applications, driven by the large-scale deployment of direct evaporative coolers. The industrial applications for direct evaporative coolers include Buildings, warehouses, factories, manufacturing units, power generation, oil and gas, construction, and many more.

- Additionally, the industrial sectors implement advanced evaporative cooling systems to foresee the need for maintenance before a problem arises. The most recent cooling technologies, which employ Internet of Things (IoT) techniques, contain sensors, connections, software, and other components that let the system communicate with other connected devices. IoT solutions enhance preventative maintenance by collecting information on equipment status and air quality.

- As a result, many businesses concentrate on direct evaporative cooling (DEC), frequently the most energy-efficient method of cooling a data center. To grow its data center cooling sector, which includes natural evaporative cooling, Munters, for instance, shifted its Virginia staff to the new facility in April 2021. A 365,000-square-foot facility for manufacturing, R&D, and sales was the company's USD 36 million investment target.

The Asia-Pacific Region to Hold Significant Market Share

- The Southeast Asian region is anticipated to experience a significant demand for AC sales, driven by rising temperatures and rising earnings, expected to reach 300 million units by 2040; it is anticipated that Indonesia will supply half of the world's air conditioning units.

- In addition, research from the International Energy Agency states that cooling equipment sales are dominated by China, the United States, and Japan, with India and Indonesia experiencing the most significant rise. Although China sold over 500 million units in the past ten years, India and Indonesia had a relative increase in demand for air conditioning that was more rapid, with average yearly installations expanding at a pace of over 15% in both countries. (India)

- South Asia is experiencing exponential growth in the demand for air conditioning, driving the need for economic and simple cooling techniques. When considering these nations' targets for reducing carbon emissions, evaporative cooling is one of the finest solutions. Southeast Asia boasts among the Asia-Pacific region's fastest-growing data center marketplaces, although the sustainability of these facilities is still a problem for the area.

- Nevertheless, it is anticipated that in the upcoming years, sustainability will become a key differentiator in Asia between data center providers, particularly as leading tech companies around the world, like Microsoft, Google, and Apple, set standards with carbon neutral and zero sustainability goals and as cutting-edge energy-efficient technology is developed.

- Since data center cooling accounts for between 35% and 40% of overall energy demand, it represents a significant hurdle to sustainability in Asia. Most data centers in the area currently employ air-based cooling, a very ineffective and expensive solution.

- Companies in the area are switching more and more to evaporative cooling techniques. For instance, data centers can be sustainable thanks to cooling technology like evaporative cooling. As data centers become more prominent to accommodate the demands of digitalization, these technologies enable businesses to employ indirect evaporative, direct evaporative, hybrid systems, and liquid cooling to reduce Power Usage Effectiveness (PUE) and overall energy usage.

Evaporative Cooling Industry Overview

The Evaporative Cooling Market is moderately competitive and consists of several major players. In terms of market share, few of the major players currently dominate the market. With a prominent share in the market, these major players are focusing on expanding their customer base across foreign countries. The major players include companies like Delta Cooling Towers Inc., Condair Group AG, SPX Cooling Technologies, etc. The competition and rapid technological advancements are expected to pose a threat to the growth of the companies during the forecast period.

In May 2023, Xiaomi Youpin launched the MIJIA Smart Evaporative Cooling Fan, which provides its customers with a refreshing and comfortable indoor environment. The smart fan launched by the company has been designed to provide three effects in one - blowing, cooling, and humidifying. It would be equipped with a circulating water cooling system, which allows the addition of water and ice crystals to bring different cooling effects. The innovative wireless water tank patent design allows the tank to be removed from the body for cleaning at any time, ensuring hygiene and convenience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes Products

- 4.4 An Assessment of the Impact of COVID-19 on the industry

- 4.5 Analysis of the Evaporative Cooling Hotspot

- 4.6 Comparative Analysis of Alternative/Substitute Cooling Technologies Deployed in the Residential and Commercial Sectors

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Cost-effective Cooling Solution

- 5.2 Market Restraints

- 5.2.1 Dependency on External Climate

6 MARKET SEGMENTATION

- 6.1 By Type of Cooling

- 6.1.1 Direct Evaporative Cooling

- 6.1.2 Indirect Evaporative Cooling

- 6.1.3 Two-stage Evaporative Cooling

- 6.2 By Application

- 6.2.1 Residential Applications

- 6.2.2 Commercial Applications

- 6.2.3 Industrial Applications

- 6.2.4 Confinement Farming

- 6.2.5 Other Applications

- 6.3 By Distribution Channel

- 6.3.1 Big-box Retailers

- 6.3.2 HVAC Contractors and Distributors

- 6.3.3 Other Distribution Channels

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Delta Cooling Towers Inc.

- 7.1.2 Condair Group AG

- 7.1.3 SPX Cooling Technologies

- 7.1.4 Baltimore Aircoil Company Inc.

- 7.1.5 Munters Group AB

- 7.1.6 Colt Group Limited

- 7.1.7 Phoenix Manufacturing Inc.

- 7.1.8 Bonaire

- 7.1.9 ENEXIO Water Technologies GmbH

- 7.1.10 CFW Evapcool

- 7.1.11 Celsius Design Limited